LW - Campbell Soup Company: Despite Some Deterioration Shares Still Offer Tasty Upside

2023-12-07 09:06:16 ET

Summary

- Campbell Soup Company exceeded expectations for adjusted earnings and revenue for the latest quarter, leading to a 7.1% increase in its stock price on December 6.

- Despite declining revenue and profits, the long-term picture for the company is bullish.

- Management reaffirmed guidance for the 2024 fiscal year, projecting revenue growth and increased EBITDA.

- And shares are cheap enough to warrant upside from this point on.

December 6 ended up being a really fantastic day for shareholders of Campbell Soup Company ( CPB ). Although the company fell short of expectations when it came to earnings per share, it exceeded forecasts with both adjusted earnings and revenue for the first quarter of its 2024 fiscal year . On top of this, management reaffirmed guidance for the 2024 fiscal year, demonstrating once again the quality of the operation that they run. In response to this development, shares of the company shot higher, closing up 7.1% for the day. Despite this move, the stock looks attractively priced, both on an absolute basis and relative to similar firms. While the picture is far from perfect because of declining revenue and profits year over year, I would argue that the long term trajectory for the company is bullish and shares still warrant a ‘buy’ rating from when I last wrote bullishly about the enterprise earlier this year.

A mixed, but fine, picture

The last article that I wrote about Campbell Soup Company was published in early August of this year. In that article, I talked about the firm's rather pricey purchase of smaller competitor Sovos Brands ( SOVO ). Even though I felt that the transaction was, at best, fairly valued, I still maintained that shares of the soup giant deserved to move higher because of how cheap they were. Since the publication of that article, the stock has unfortunately moved up by only 0.8%. But at least that's not far from the 1.1% increase seen by the S&P 500 over the same window of time.

{kind=link}

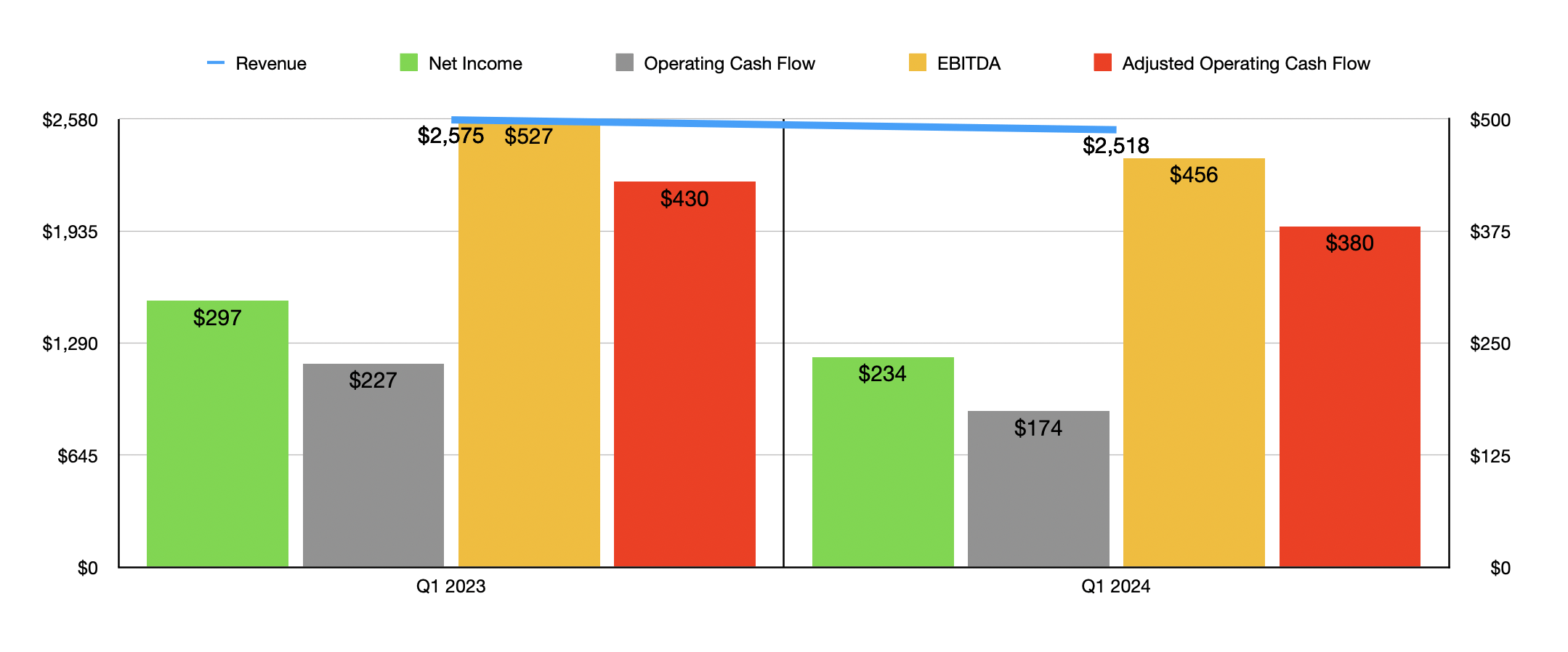

To be clear, for most of the time between the publication of that last article and today, Campbell Soup Company has sorely underperformed the S&P 500. The only reason why we have seen and improvement recently is because of the pop experienced in response to earnings. To start with, we should touch on revenue figures reported by the company. During the first quarter of the 2024 fiscal year, sales for the business came in at $2.52 billion. While this represents a decline of 2.2% compared to the $2.58 billion reported one year earlier, it was actually about $48 million higher than what analysts forecasted.

{kind=link}

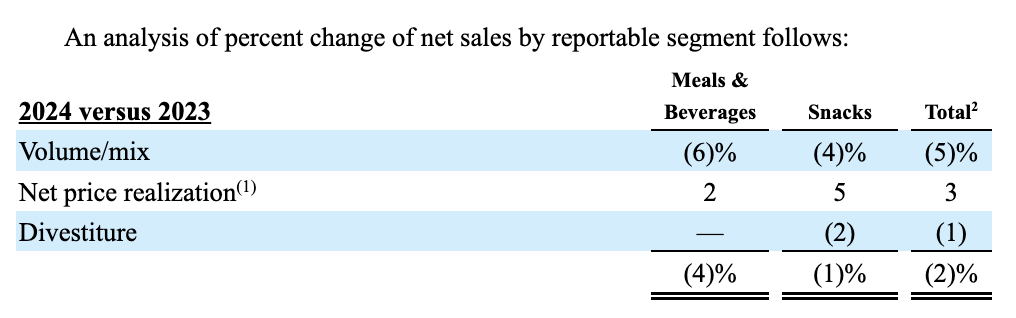

The drop in sales during this window of time was driven by a drop in volume and a change in product mix sold. The hit associated with these two things totaled 5% across the company, with the Meals & Beverages portion of the business experiencing a 6% hit and the Snacks category experiencing a 4% hit. Management did not provide much in the way of detail on this. But they did say that the picture would have been worse were it not for price increases pushed onto customers. Those price increases amounted to an improvement for sales of about 3%. Leading the way was a 5% hike in the Snacks category. It's also worth noting that the firm was negatively impacted to the tune of 1% by asset divestitures.

{kind=link}

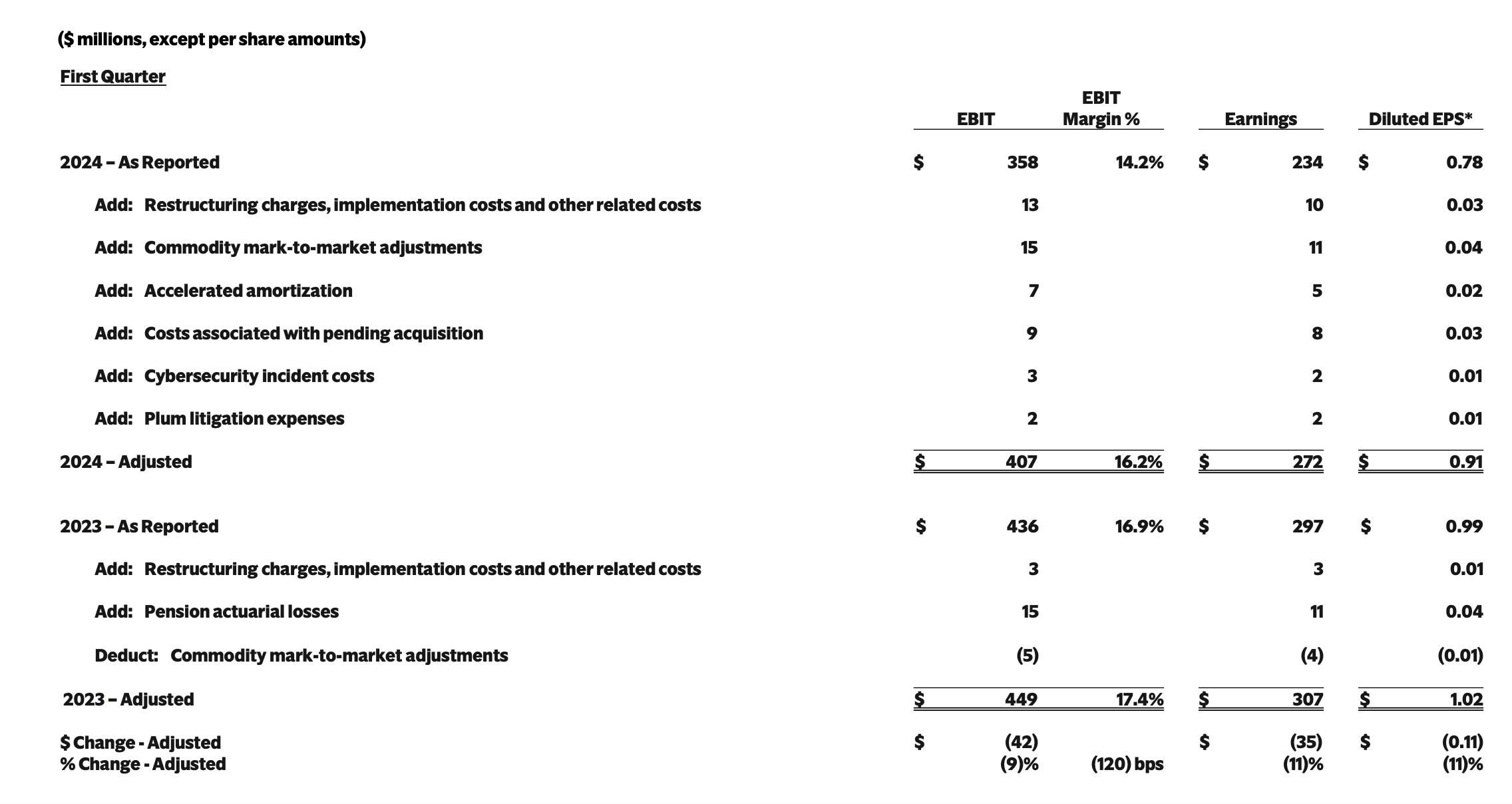

While the company surprised from a sales perspective, it failed to do so from an earnings perspective. Profits per share totaled $0.78. That's down from the $0.99 per share reported in the first quarter of 2023 and it ended up being $0.04 per share lower than what analysts expected. Fortunately, adjusted earnings came in at $0.91. While that is still down from the $1.02 reported the same time last year, it ended up being $0.09 above what analysts thought. As a result of these per share figures, net income for the quarter came in at $234 million. That's down from the $297 million seen one year earlier. Over that same window of time, adjusted profits fell from $307 million to $272 million.

{kind=link}

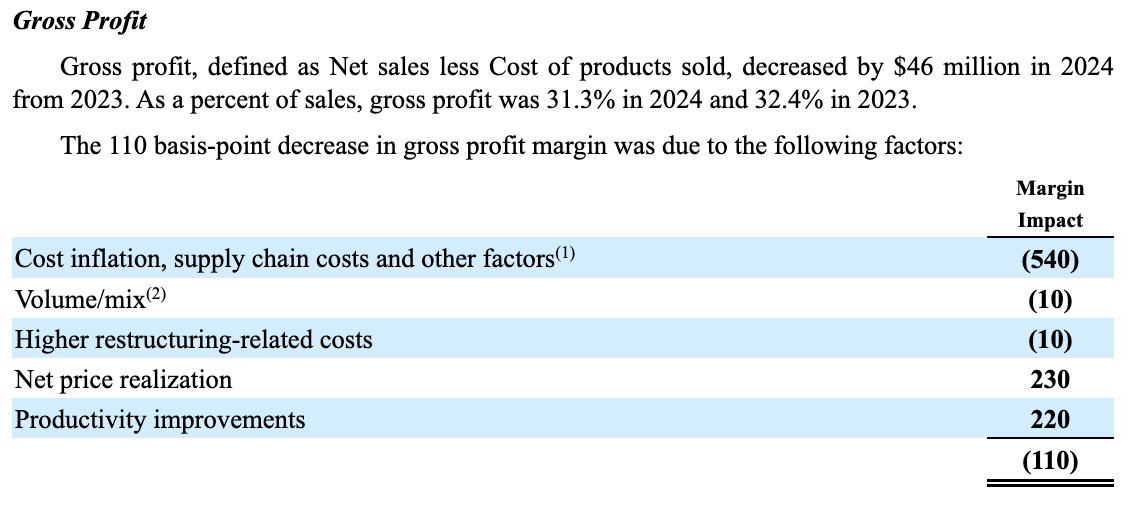

While the drop in revenue certainly contributed to the weakness in the bottom line, it's also worth noting that the company experienced some margin pressure during the quarter. The firm's gross profit margin contracted from 32.4% to 31.3%. Most of the hit involved cost inflation and supply chain costs. But these were mostly offset by 230 basis points of higher pricing and 220 basis points of productivity improvements. Management deserves a significant amount of credit for implementing cost savings initiatives over the past few years. In fact, even in this quarter that we are talking about, the company recorded $2 million of restructuring charges and millions of additional dollars in implementation costs across the organization in order to become leaner. Unfortunately, that didn't stop other profitability metrics from worsening year over year. Operating cash flow declined from $227 million to $174 million. If we adjust for changes in working capital, we get a drop from $430 million to $380 million. And finally, EBITDA declined from $527 million to $456 million.

{kind=link}

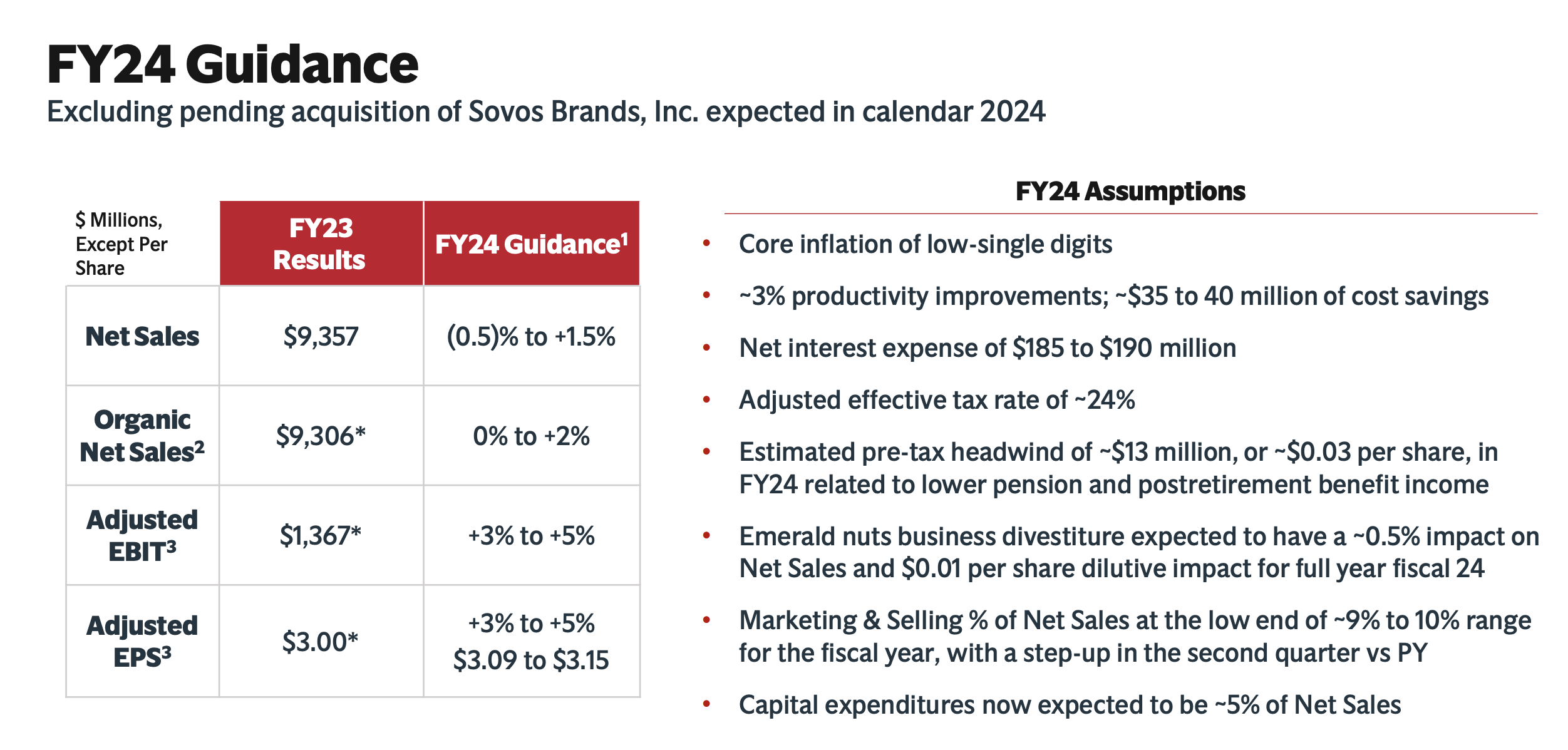

Despite missing when it came to bottom line results, management still believes that initial guidance for 2024 is realistic. They are forecasting revenue growth of as much as 1.5%. Though it is possible it could contract by as much as 0.5%. Organic revenue should be between flat and up 2%. Earnings per share guidance implies, at the midpoint, profits of $932.9 million, while EBITDA should grow by between 3% and 5%. At the midpoint, that would imply a reading of just under $1.7 billion. No guidance was given when it came to adjusted operating cash flow. But based on my estimate, it should come in at around $1.32 billion.

{kind=link}

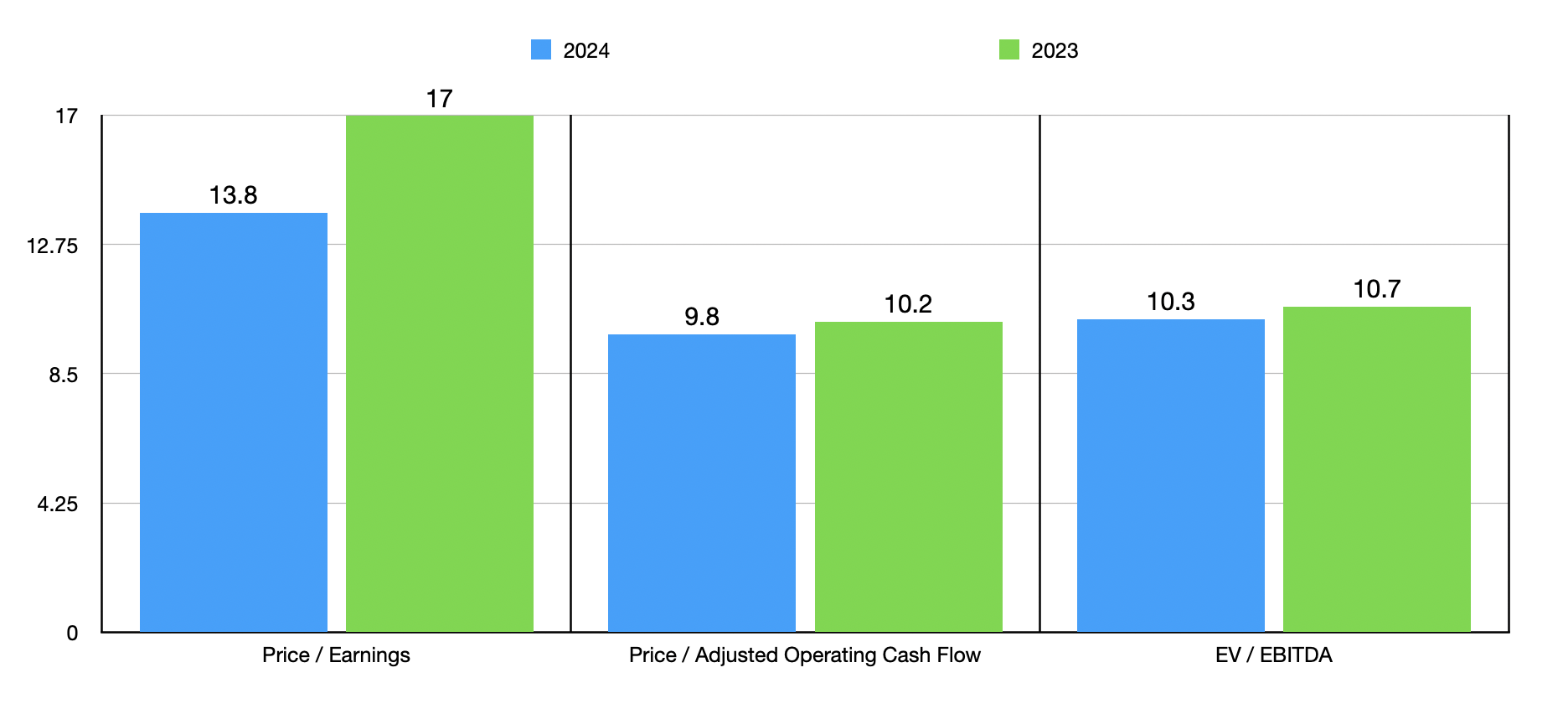

Using these figures, I was able to value the company as shown in the chart above. As you can see, the stock does look cheaper on a forward basis. But because the end of the 2024 fiscal year is so far away, I think it would be more prudent to value the company using the data from 2023. With that in mind, I created the table below that shows how shares are priced compared to five similar companies. Using the price to earnings approach, three of the five firms were cheaper than Campbell Soup Company. This number drops to one of the five using the price to operating cash flow approach. And if we use the EV to EBITDA approach, then our prospect ended up being the cheapest of the group. Even if we were to use the forward estimates, the only thing that would change is that only one of the five companies, as opposed to three of them, would be cheaper on a price to earnings basis.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Campbell Soup Company |

| 17.0 |

| 10.2 |

| 10.7 |

| The J.M. Smucker Company ( SJM ) |

| 23.3 |

| 8.5 |

| 24.1 |

| Conagra Brands ( CAG ) |

| 13.1 |

| 12.0 |

| 11.6 |

| Lamb Weston Holdings ( LW ) |

| 14.6 |

| 16.3 |

| 13.8 |

| Kraft-Heinz ( KHC ) |

| 15.0 |

| 12.5 |

| 11.3 |

| The Hershey Company ( HSY ) |

| 20.4 |

| 16.7 |

| 15.4 |

Takeaway

Based on all the data provided, I must say that I am quite comfortable with how Campbell Soup Company performed during the quarter. Although earnings came in lower than anticipated, adjusted earnings were comfortably higher than expected. Shares still look attractively priced and I believe that the long-term outlook for this enterprise is positive. The stock certainly deserved the upside it experienced. And I would argue that it deserves enough additional upside to justify the ‘buy’ rating I assigned it earlier this year.

For further details see:

Campbell Soup Company: Despite Some Deterioration, Shares Still Offer Tasty Upside