SOVO - Campbell Soup's Acquisition Of Sovos Brands Likely To Close

2023-11-30 15:29:58 ET

Summary

- Campbell Soup Company is acquiring Sovos Brands, Inc. for $2.7 billion, or $23 per share.

- The deal is facing concerns from the FTC regarding anti-competitiveness, causing a delay in the closing.

- The annualized return for the deal looks decent, but given the uncertainties around the closing timeline, it is not enough for now.

Sovos Brands, Inc. (SOVO) is a packaged food company. Its brands include Michael Angelo's, Noosa's, and Rao's. It is being acquired by Campbell Soup Company ( CPB ) for $2.7 billion, or $23* per share. I've put an asterisk behind it because there are some odd terms that I'll get to later. Campbell Soup used to be much larger but is currently only an $11 billion market cap company.

Sovos received a 2nd request from the FTC indicating some concerns around the anti-competitiveness of the deal. This widened the spread quite a bit, and now Sovos trades around $21.84. That means there's a 5.3% upside to the deal ultimately closing.

Boards have approved the transaction. Sovos shareholders need to vote, but I don't foresee problems there. Major shareholders are supportive of the deal. Closing was initially expected to have occurred before the end of the year. With the 2nd request in, that's not going to happen. Closing before the end of the year would have been possible without this request, but it still would have been fast. The companies are probably not too surprised with the 2nd request because they negotiated out a ticking fee.

If the merger is not effective by May 7, 2024, an additional $0.00182 per day accrues to Sovos shareholders. That comes down to $0.50 of additional compensation if it takes until the outside date of February 27. This helps to make it less painful for arbs to hold this as a regulatory process drags on. But it doesn't make it great. Everyone would still prefer an expedient solution.

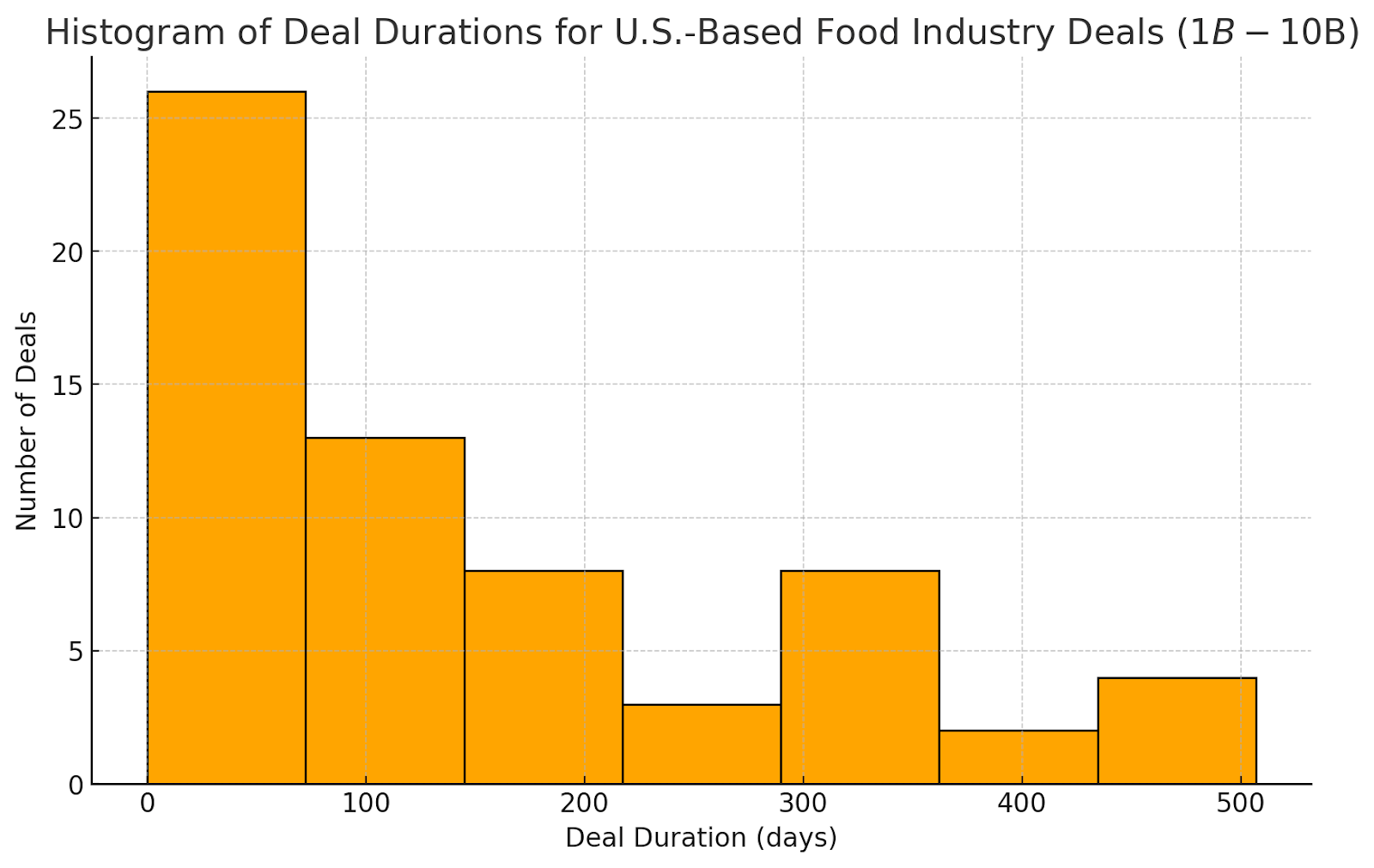

The graph below shows how long it has historically taken for food deals to close if the deal value fell in the $1 billion to $10 billion range:

{kind=link}

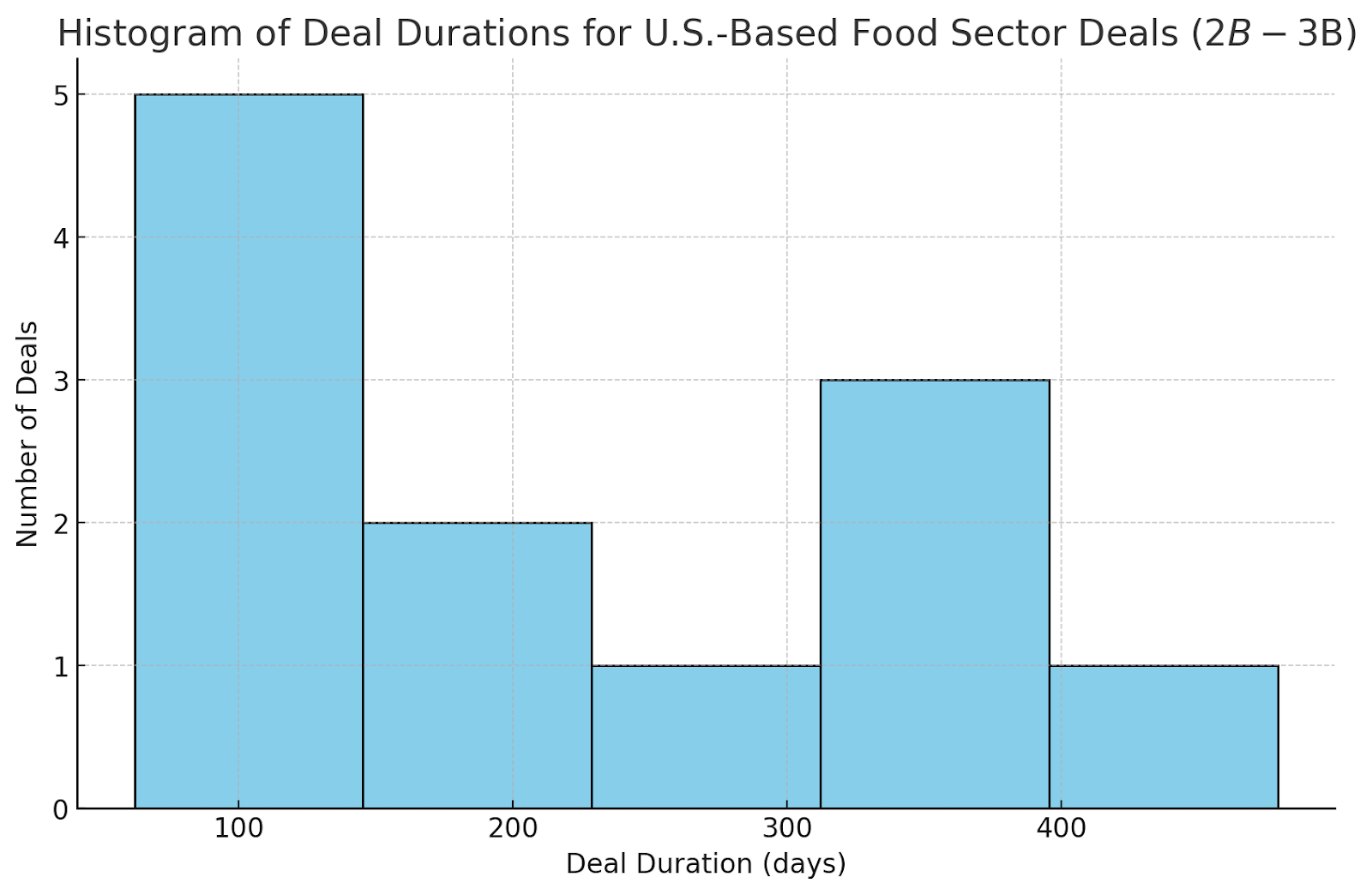

This deal is likely to take longer instead of shorter because of the 2nd request. I'd lean more towards the 200-300 days. I also pulled up the data for U.S. deals between $2 and $3 billion in value. That looks quite similar:

{kind=link}

There are not really enough deals in that sample to be very sure. There is also enormous variability in how much time it takes for deals to close. But it does show roughly the same profile as the graph that included a lot more deals and a wider market cap range.

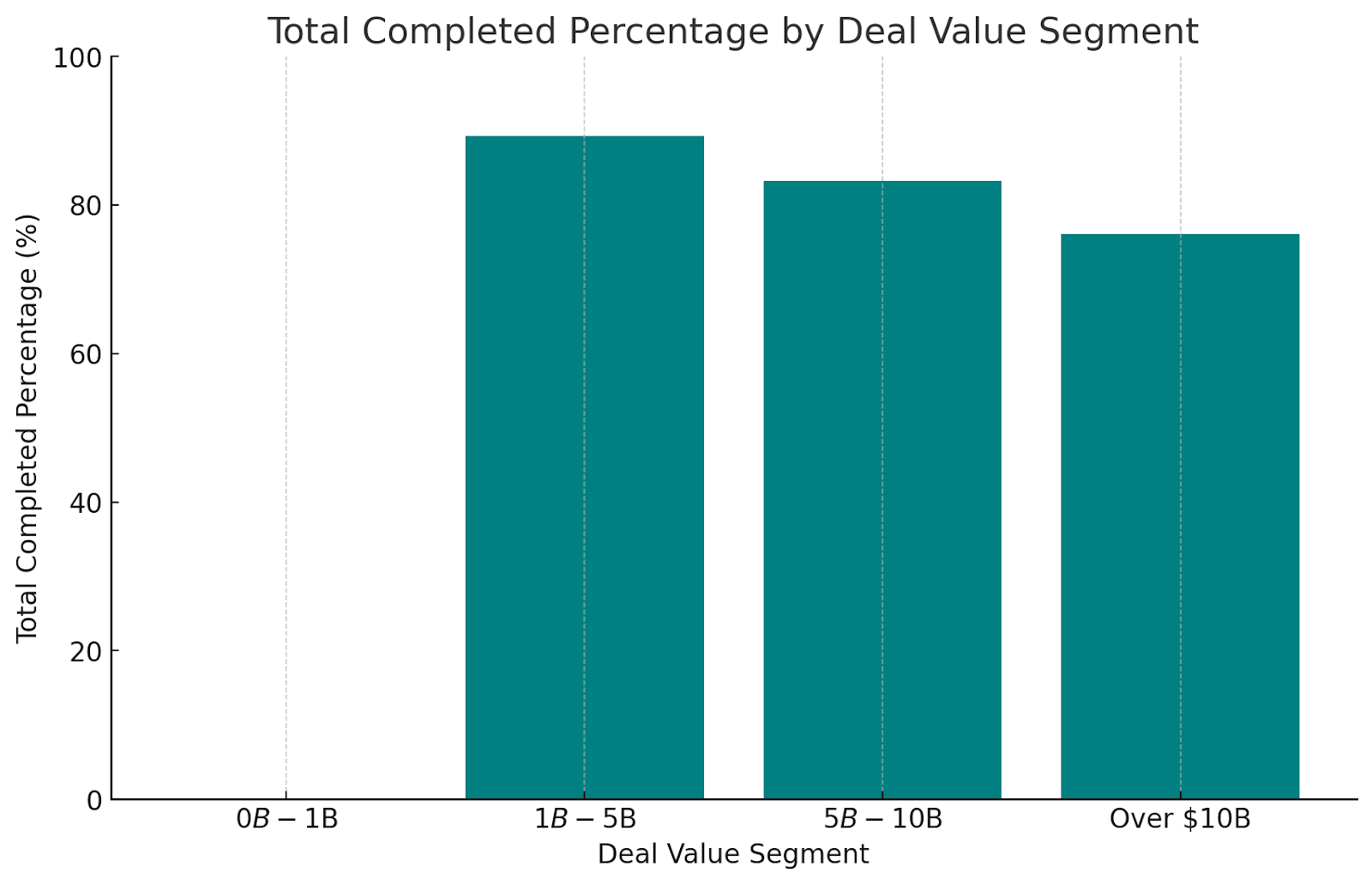

I also looked into how many deals in the food industry are ultimately completed. That's close to 90% for deals of this size.

{kind=link}

The odds decrease because of the 2nd request. However, I'm not adjusting that percentage too much, as it does seem likely to me that any problems identified by the government can be addressed in this instance. This is because of the relative size of the parties, the presence of direct major competitors but also a number of strong market forces at the distributor level.

We are already 115 days into this deal. If this closes around the 200-day mark, we're only 85 days away, if it closes around the 300-day mark we're 185 days away and if it closes only after 400 days we're 285 days away. The annualized return looks like this for each instance:

| Time Period (Days) | Annualized Return (%) |

|---|---|

| 85 | |

| 25.17 | |

| 185 | |

| 10.88 | |

| 285 | |

| 7.11 |

Only the 285-day period is influenced by the ticker fee to a relevant degree.

The return profile doesn't look so bad to me. Taking everything together, though, I'm not sure it is attractive enough. One thing that helps is that the break price is likely somewhere at the $17-$18 level based on the pre-deal price. That's 17-22% down. Admittedly, it doesn't increase my confidence that the packaged food index hasn't done great since the announcement:

And neither did small caps:

I think this is an okay deal to hold Sovos Brands, Inc. shares here if you don't have other better ideas. The odds of this declining to a 10%~ annualized return type deal are high enough that I'm passing on this one for now. It could surprise with a quick close, but if I roll the dice a thousand times here, I don't think I'm going to love the average outcome.

For further details see:

Campbell Soup's Acquisition Of Sovos Brands Likely To Close