CAMT - Camtek: A Cyclical Play At A Great Price Point

2023-10-06 16:18:53 ET

Summary

- Camtek Ltd. has seen significant improvement in revenues and margins, with 2022 being a successful year for the company.

- Some consolidation is expected in 2023 before demand picks up again, but overall growth is projected for the coming years.

- Camtek is a leading player in the semiconductor industry and offers a strong opportunity for exposure to the sector.

Revenues and margins for Camtek Ltd. ( CAMT ) have improved immensely over the last few years and 2022 become a very busy year for the company as the top line landed at $321 million. CAMT seems to remain on a good trajectory but some consolidation seems likely in 2023 before demand resumes and CAMT can once again enter into the growth cycle. A slight quarterly growth is expected for the remaining part of 2023 and it's also set to continue going into 2024. The company is included in the semiconductor materials and equipment industry where demand has been immense the last few years but has since resigned somewhat. It has become clear that the industry comes and goes in cycles and semiconductors should be viewed as a cyclical investment.

These cyclical investments are often associated with trying to time the market and buying when demand seems to slip and margins begin falling. That seems to have been in the latter part of 2022 for CAMT and the rebound has been impressive since. As the market is forward-looking and so should you be, the future growth of CAMT seems solid, and getting in now makes sense. I'm rating CAMT a buy as a result.

A Brief Look At The Business

As we know, CAMT operates in the semiconductor industry as a developer and manufacturer of inspection and metrology equipment for advanced interconnect packaging and memory and image sensors among other niche segments in the broader semiconductor industry. The company has some systems called Eagle-i system that primarily focus on delivering 2D inspection and metrology capability for companies in the sector.

Company Performance (Investor Presentation)

The company has experienced strong demand following the surge of semiconductors and the introduction of more advanced AI programs. Now almost any company you come across seems to be looking into how to introduce some of the capabilities of the semiconductor industry into their own or how AI could further enhance operational performance.

{kind=link}

With a leading position in the market, I think that CAMT offers one of the best opportunities to gain strong exposure to the industry, without perhaps the same amount of cyclicality and volatility added. Many companies in the industry are expected to post a significant YoY decline in 2023, whilst CAMT seems to be holding up rather well. That speaks volumes about the type of business you are getting into right here in my opinion.

Quarterly Result

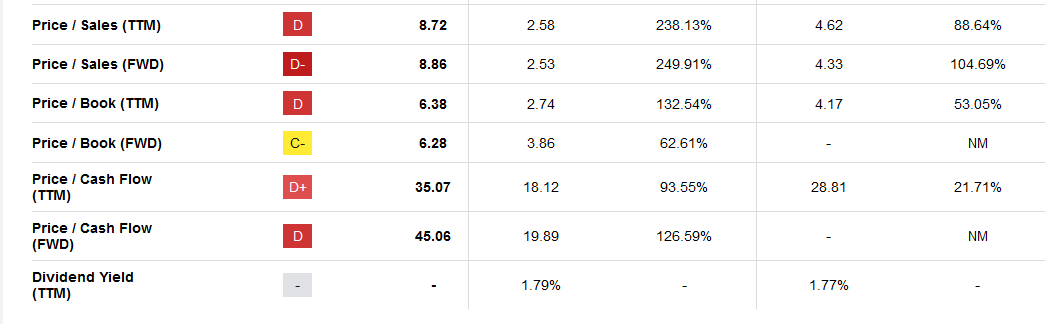

Looking at the last results from CAMT, it seems that they managed to come out ahead of their expectations as revenues landed at $73 million in total. As for the coming quarter, the projections are that revenues will post a slight quarterly growth and come in at $77 - 79 million. A beat here I think would further solidify the higher valuation that CAMT is receiving right now. The p/s, for example, is at 6.7 right now but as demand rebounds I think that it will be more justified, as we know, the market is forward-looking.

{kind=link}

The CEO Rafi Amit made some comments on the stronger demand the company is experiencing and this is especially reassuring to see as the stronger flow of orders is a good indicator of better times ahead. Expectations are also that 2024 will be a record year for the company, both in terms of revenues and earnings. As for what the market is expecting of CAMT, it seems that an EPS of $2.17 is expected. My opinion on the projections heavily relies on demand continuing strongly for the second half of 2023, and CAMT being able to build a strong backlog of orders going into 2024. I think a failure in doing so could perhaps result in earnings coming in just in line with projections; but a major beat would send the share price up even higher, in my view.

Risks

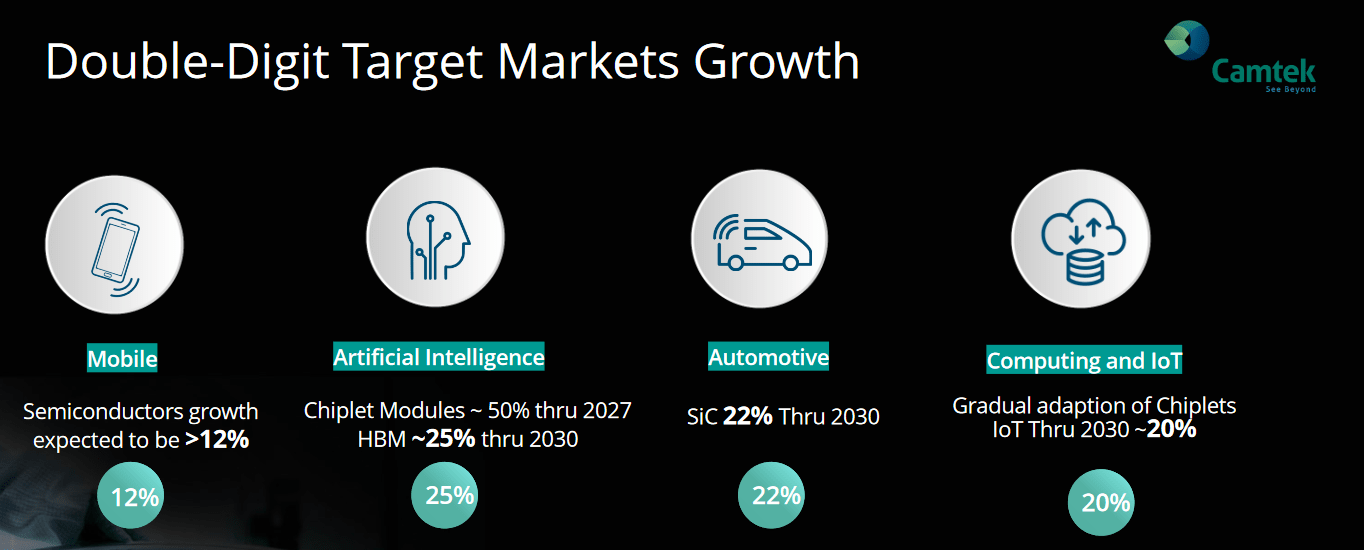

The semiconductor market finds itself amidst a substantial correction cycle, driven by a marked decline in demand across a spectrum of devices, including PCs, smartphones, tablets, and consumer electronics. This pronounced downturn in demand has sent reverberations through the industry, prompting a recalibration of strategies and expectations. The market has shown itself to be a cyclical one driven by companies wanting to stock up inventory levels and capitalize on coming demand . That usually means that demand for semiconductors could be a good indicator for customers to companies like CAMT projecting they will have a surge in demand.

Market Growth (Investor Presentation)

Notably, the high-end memory segment has borne the brunt of this correction, with prices experiencing a pronounced descent of nearly 50% over the past year. This swift and substantial price adjustment reflects the intricate balance between supply and demand dynamics that govern this intricate market. These price adjustments are something that needs to be watched by companies like CAMT. If the company can display a strong resilience in margins, then potentially a higher valuation may be suitable, which seems to be the case for CAMT right now.

An equally significant facet of this recalibration revolves around the supply chain intricacies associated with key components, particularly for the production of phones, personal computers, and data center chips. The ebbs and flows in demand have led to a renewed equilibrium in lead times within the supply chain, marking a return to more conventional and manageable production timelines. Since the COVID pandemic, however, the supply chain issues have eased up significantly and high shipping costs seem to be a thing of the past. I don’t think this will play out to be a challenge for CAMT in the medium term.

Valuation & Wrap Up

CAMT has proven itself very capable of growing quickly in the semiconductor industry and building out a broader customer base. The company has maintained margins very well and even if 2023 doesn't offer a YoY growth that maybe a lot of investors would have wanted, the fact that CAMT is barely posting a decrease when many other companies and peers are doing significantly lower revenues and earnings speaks a lot about what you get with an investment in CAMT.

{kind=link}

I like the price point right now even after the run-up it has had and paying a slight premium to the sector is often necessary when you want to get into a company. In the long run, I believe CAMT will be a winner and I want to be along for the ride. Rating CAMT a buy.

For further details see:

Camtek: A Cyclical Play At A Great Price Point