CAMT - Camtek: Too Pricey For New Investors To Jump In

2023-11-28 20:51:27 ET

Summary

- Camtek is a manufacturer of inspection machines for semiconductors, known for their accuracy and reliability.

- The company has a strong financial position with high liquidity and low long-term debt.

- The company's historical growth and current valuation suggest it is overvalued, therefore I assign a hold rating for now.

Investment Thesis

Camtek Ltd. ( CAMT ) recently reported, so I wanted to take a look at the company´s financial performance over the last decade to see if it is a good time to start a position from the perspective of an investor who has no position yet. The financial health is great, however, I don’t think the FW PE ratio is justified with such growth assumptions, even if we look at more optimistic assumptions than what I usually go with. Therefore, I initiate the coverage of Camtek with a hold rating until the company proves it can grow at a much faster pace than in the past or until the share price drops to a reasonable level.

Briefly on the Company

Camtek is a manufacturer of inspection machines that inspect and measure semiconductors to make sure these semiconductors are made correctly and function properly. This way the electronic devices that use these semiconductors work properly and do not break.

The company´s machines use optical inspection to check the surfaces of semiconductors for any defects using light. Another way of inspecting for defects is to use X-ray imaging, which the company also specializes in.

The company´s products are used worldwide and are known for their accuracy and reliability. Furthermore, the company is the leading provider of metrology and inspection equipment in the industry. So, let´s look at the company in more detail.

Financials

As of Q3 ´23, the company had $363m in liquidity against $196m in long-term debt. This is not a bad position to be in. The company makes more interest income than it pays out in interest on debt, so it is safe to say the company is at no risk of insolvency. This financial position allows for flexibility on how the management wants to spend the company´s cash flow, whether that is through repurchasing stock, inorganic growth through acquisitions, or paying a dividend. I prefer the company to reinvest its cash flow, as that is in my opinion the best way to award shareholders in the long run.

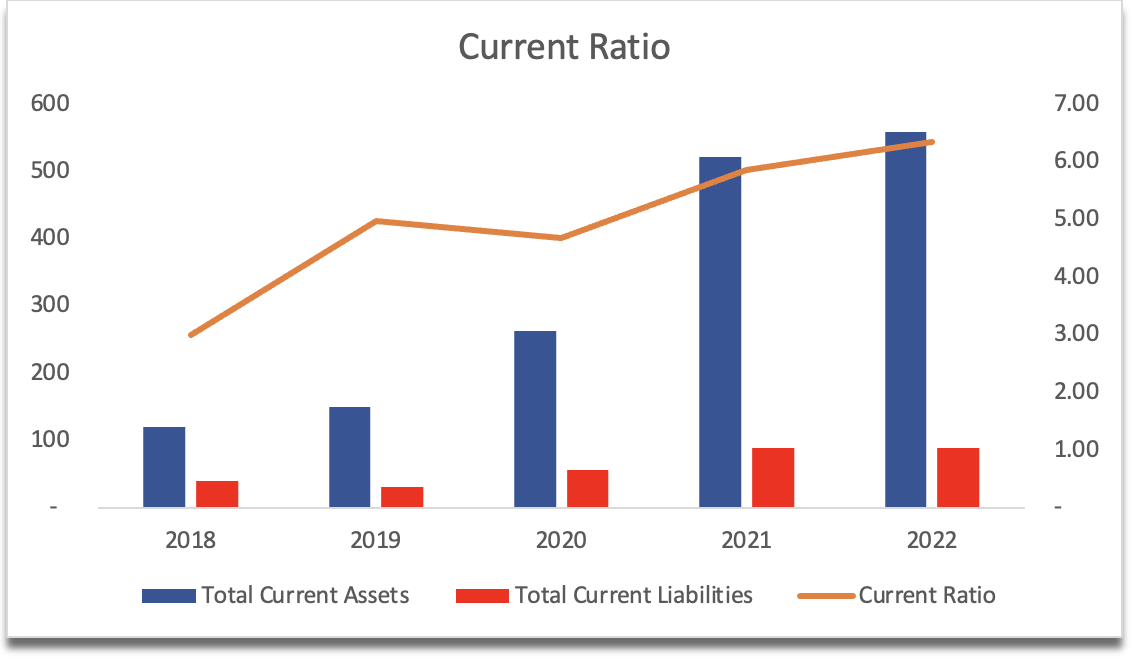

The company´s current ratio has been very high in the last few years, which is not bad, however, it feels like a missed opportunity for better use of assets. The good thing is the company can cover its short-term obligations with ease, but the capital left over could have been used to further the growth of the company. I would like to see the ratio come down to around 2 in the future as that I believe is an efficient ratio. I would like to see the company take some initiative and put the capital available to good use, for instance, an acquisition for further growth and market share expansion.

{kind=link}

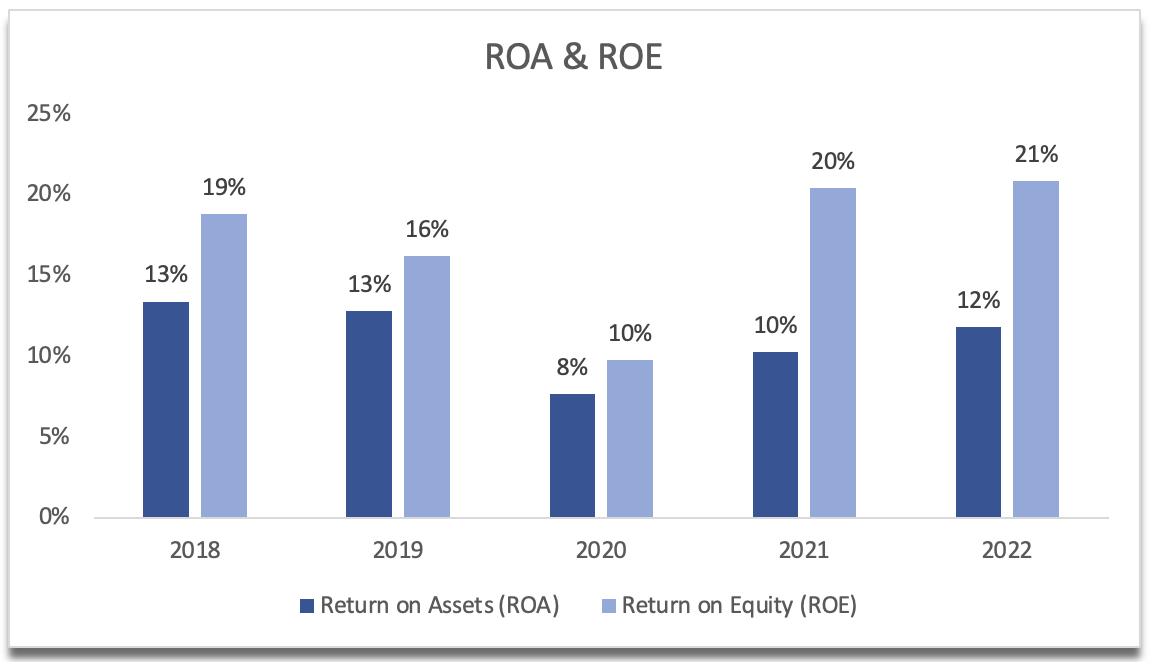

In terms of efficiency and profitability, the company´s ROA and ROE have been decent in the last couple of years, driven by improvements in the bottom line, which tripled from FY20 to FY21 and a further 33% increase a year after that. The revenue increases can be attributed to the number of products sold, during which the pandemic played a large role as the world opened up more and more.

{kind=link}

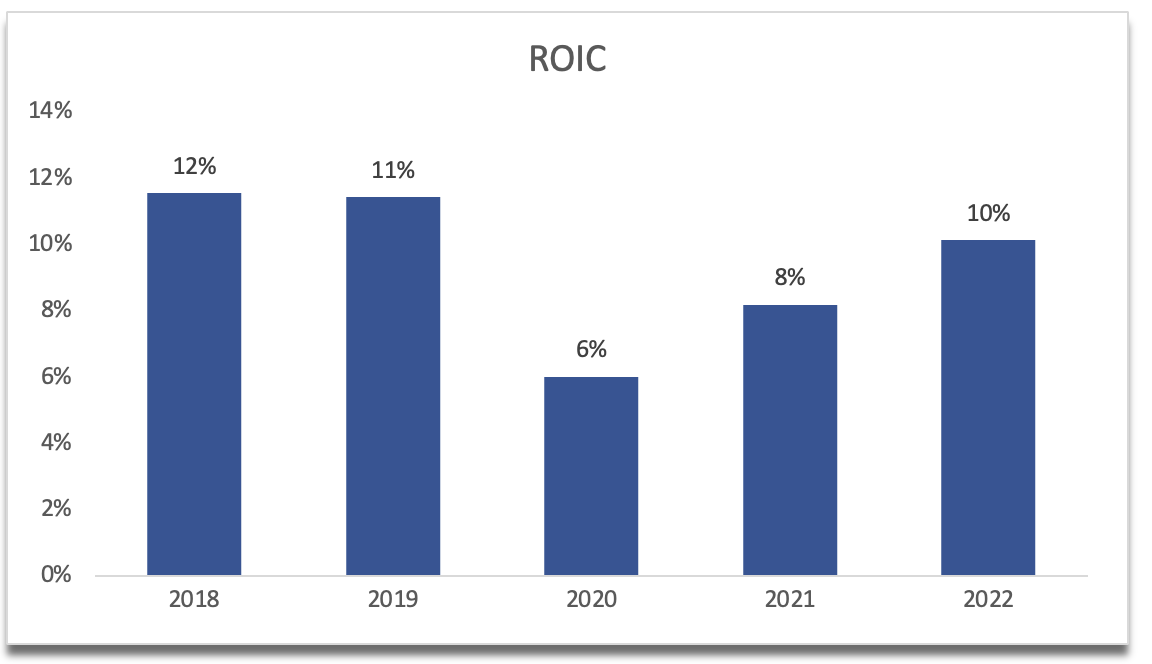

The company´s ROIC has improved since the pandemic lows also, however, it is still slightly under pre-pandemic levels. It is trending upward, which is a good sign. Furthermore, it is at around the minimum I´d like to see a company achieving. It tells me that the management can deploy capital in profitable projects. Camtek is running efficiently and profitably, however, I wouldn’t be surprised if we see some dips in these metrics for FY23 due to the tough conditions and the negative sentiment the semiconductor industry experienced recently, which are the oversupply of inventory, and the soft demand for the products that is bringing down prices globally.

{kind=link}

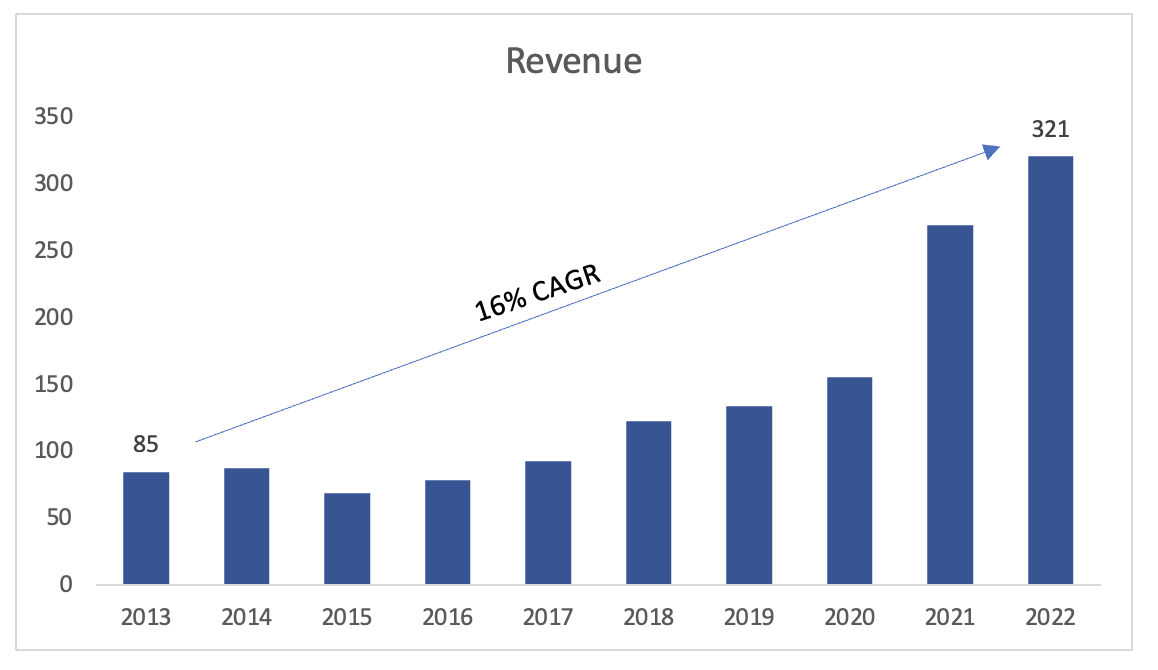

In terms of revenues, the company managed a respectable 16% CAGR over the last decade of operations, however, given the negative sentiment and the estimates for FY23 of around -2% , I don’t think the company will manage to achieve such growth for the next decade, so it seems that the company´s FW PE (non-GAAP) of around 33 is too high.

{kind=link}

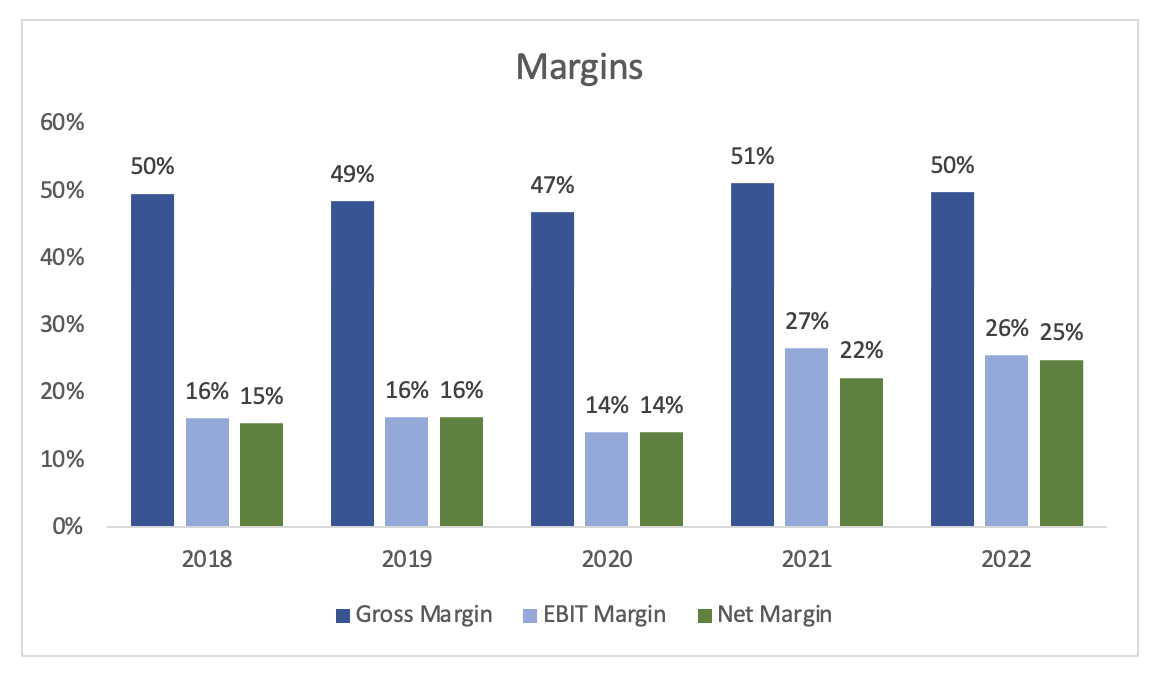

In terms of margins, these also improved substantially since the pandemic lows. The company has become more efficient and profitable in the last couple of years, which is a very positive sign, however, I would expect margins to come down slightly in FY23 due to the mentioned reasons. So far GAAP gross margins sit at around 47% and operating around 21% as of 9 months ended September. Once the sentiment turns positive, I would expect the company to return to its previous profitability

{kind=link}

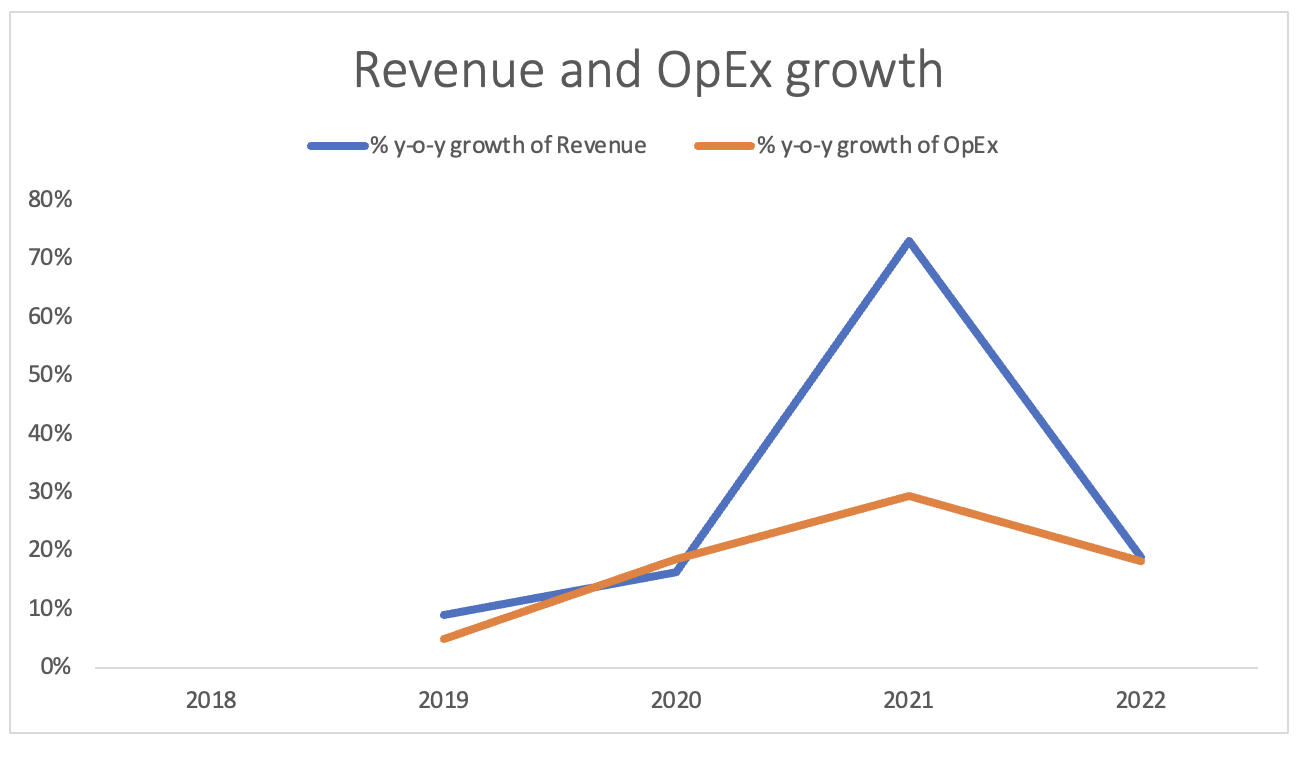

A big help in this improvement in efficiency and profitability was FY21, when revenues increased by 73%, while operating expenses only increased by around 29%, which tells me the company is very scalable. In the future, I would expect operating expenses to increase slower than revenues as it looks like the company is capable of keeping costs under control.

Revenue growth and OpEx Growth (Author)

{kind=link}

Overall, the company seems to be very healthy, like many other semiconductor companies that I covered in the past had a great balance sheet with very few liabilities, which should help the company weather the uncertainty and negativity in the sector.

Comments on the Outlook

The market likes certainty, that´s clear. And the next year for CAMT is pretty much set already and should be priced in. The management reported that the backlog for 2024 is robust with many orders to be delivered that year. Around 240 systems are to be delivered for installation in 2024, as per the transcript . So, for this reason, I think the market already reflected a decent year for the company. To me, that is rather very short-sighted as I usually look for companies that have a lot of long-term potential. That is not to say the CAMT won't be able to achieve a robust backlog for the next year, however, I believe that with such announcements, the company´s share price won´t go anywhere for the next while since the good news has been priced in and there is more risk to the downside now.

Unfortunately, the company doesn't provide any information other than slight mentions of what their backlog looks like in the upcoming half year to an year. When asked about the specifics of the backlog, and whether the company reports this number in their 20-F report Rafi Amit had this to say in their Q4 ´21 earnings call:

No, actually we do not provide in our 20-F which is the equivalent of 10-K for US companies or foreign issuers. We do not provide any backlog information. So we typically, we do not provide it also in our conference calls.

The company is headquartered in Israel, which is in the middle of a war right now, however, I don’t think the operations will be affected since the facilities are very far from the border according to the management, which minimizes the risk of interruptions. I would still expect the company´s share price to fluctuate a lot more than any other stock that is not headquartered in a warzone, especially if the conflict escalates further.

According to CEO Rafi Amit, high-bandwidth memory, or HBM will see 22% CAGR, while chips will see 35% CAGR for the next 4 years. About 60% of the company´s profits come from these segments, so if the company can manage to capture such growth numbers, then that is great, however, I will have to be a little more conservative as FY23 doesn't look very good already, and I do not think the company will give a very good guidance for FY24, even with the robust backlog. Furthermore, the company grew at a 16% CAGR for the last decade, which doesn’t provide me comfort. We will have to wait and see how the demand for the company´s products turns out to be in Q1 and Q2 of ´24.

Valuation

For valuation, I will present two different assumptions and intrinsic values. For the first one, I went with the company achieving much higher than historical growth due to the very optimistic HBM and Chips outlook the management mentioned. Below are those revenue assumptions for the base, optimistic, and conservative cases.

Optimistic Revenue Assumptions (Author)

{kind=link}

For the margins, I decided to go with non-GAAP ones because the management focuses on that much more, which I don’t like, however, I will entertain the idea mostly because the difference is not very large between GAAP and non-GAAP. Below are those assumptions that take out the effects of share-based compensation.

{kind=link}

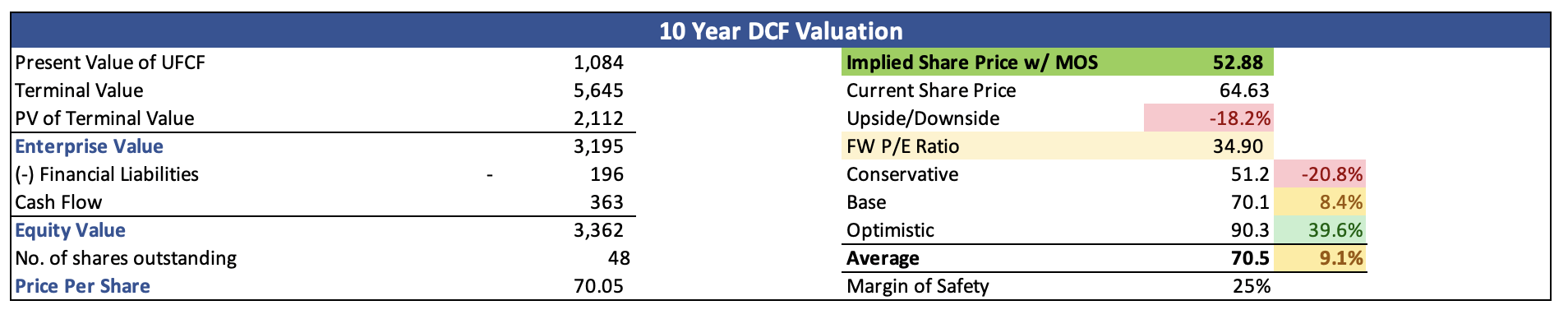

I also went with the company WACC of 10.3% as my discount rate for the DCF and 2.5% terminal growth rate. On top of these generous assumptions, I added a 25% margin of safety. I was considering higher, however, the company´s balance sheet is quite healthy, which made me rethink. With that said, the company´s intrinsic value is around $53 a share, which means CAMT is trading at a premium of around 18% to its fair value.

Optimistic Intrinsic Value (Author)

{kind=link}

Now let´s look at the assumptions I prefer for the company. These will be much more conservative than above, to give me an extra margin of safety. Below are my conservative assumptions for revenues in the three cases.

Conservative Revenue Assumptions (Author)

{kind=link}

For the margins and EPS, I decided to stick with the same percentages so EPS will be driven by the difference in revenue growth. Below are those assumptions.

Margins and EPS driven by lower rev assumptions (Author)

{kind=link}

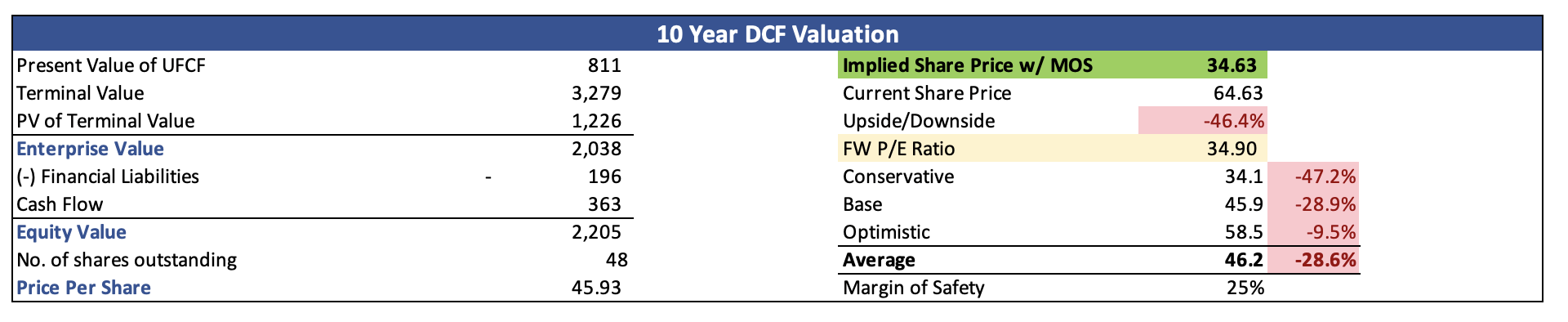

For consistency, I stuck with the same discount rate and terminal growth rate, so the main driver of difference will be the revenue growth. With that said, the intrinsic value of CAMT and what I would be willing to pay for it is $34.63 a share, which tells me that the company is very overvalued right now.

Conservative/Realistic Intrinsic Value (Author)

{kind=link}

Closing Comments

So, even with the optimistic revenue growth, Camtek seems to be very overvalued, and I tend to agree with this conclusion. Historical 16% CAGR did not support the company´s FW PE ratio of around 34 (non-GAAP). Unless the company can double the CAGR for the next decade, Camtek is not a company I would be looking to invest in right now. What I will do is set a price alert for around $45 a share and re-assess. I know it may seem like it´ll never come down to this price, but I´ve seen worse things happen.

At this price level, the risk/reward is unfavorable for me, therefore, I am initiating the coverage with a hold rating, as in hold off until metrics improve, or the share price comes down. The risks of further escalation, which don’t affect operations, will most likely affect the share price as it has with many other companies that have their HQs in Israel. This is a company that I will set and forget for a couple of months as it is trading well above my PT.

For further details see:

Camtek: Too Pricey For New Investors To Jump In