CAN - Canaan: Time To Buy Shovels?

2023-10-19 06:10:10 ET

Summary

- Canaan's ASIC business has been in decline due to the broad softness in the cryptocurrency market.

- The company has a large glut of inventory and is moving units at deep discounts.

- One of the company's largest peers, Bitmain, has reportedly had difficulty paying its employees. This could theoretically be an opportunity for Canaan.

- I still think it's slightly early to go long CAN before a post-halving rebound.

As the Bitcoin ( BTC-USD ) network quickly approaches the next block reward halving in April of next year, many eyes are generally on the price of BTC and if/when exuberance will return to the market. In my personal portfolio, I've curated a handful of Bitcoin proxy stocks that I believe will outperform if Bitcoin reaches new highs as is widely expected in the industry. Most of those stocks are Bitcoin miners and they are highly speculative wagers on my part.

One highly speculative Bitcoin proxy stock that I'm not holding is Canaan (CAN). Canaan might not be a company that shows up on a lot of watch lists, but the company has played an integral part in the Bitcoin story. This Singapore-based company was the first to publicly sell ASIC machines in 2013. In a gold rush, finding the right miner to back may yield the best reward. But the safest play outside of simply being long gold directly is perhaps selling the miners their shovels. That's what Canaan does.

During the absolute mania in all risk assets following COVID lockdowns and stimmy checks, CAN shares ripped roughly 1,900% in a matter of just five months between late 2020 and early 2021. Unfortunately for CAN shareholders, even though Bitcoin has enjoyed a sizeable 70% relief rally in 2023, CAN shares are flat on the year and down 42% over the last 12 months.

{kind=link}

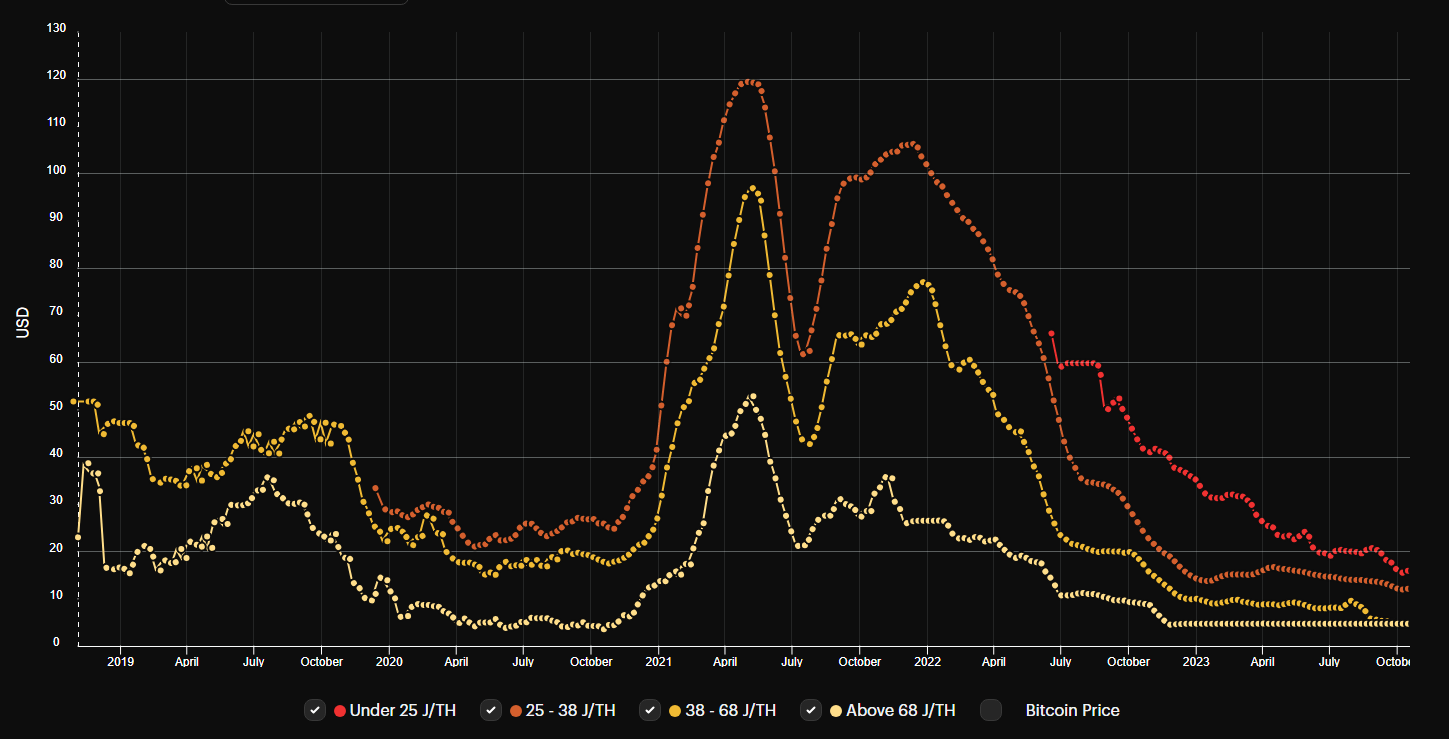

Part of the problem is the lackluster pricing power for ASICs in an environment where mining profitability is depressed. When the price of Bitcoin rises, the value of the machines that mine BTC also rise. This led to a boom in the price of ASICs between October 2020 and April 2021 - CAN's stock price responded. But when the opposite happens and mining isn't as profitable, machine prices struggle and Canaan isn't moving units at the prices that it once was.

Q2 Revenue

In the second quarter, Canaan reported a 34% sequential increase in revenue from $55.2 million to $73.9 million. Q2's top line represented a 70% decline versus the same time period from 2022. Cost of goods sold for the quarter amounted to $143.9 million. This was up 33.7% from Q2-22.

Factoring in total operating expenses of $46.7 million, the total net loss for the quarter was $110.7 million dollars.

A large factor in this net loss was a $54.7 million non-cash charge that included an inventory write-down and impairment of property and equipment. As we'll see in the next section, the inventory levels are very high and the company as essentially resorted to fire selling dated hardware at large markdowns.

| Rev in millions | Q2-22 | Q2-23 | YoY % |

|---|---|---|---|

| Total Revenue | |||

| $245.9 | |||

| $73.9 | |||

| -69.9% | |||

| Mining Revenue | |||

| $7.8 | |||

| $15.9 | |||

| +105.1% | |||

| Mining % of Total | |||

| 3.2% | |||

| 21.5% | |||

Source: Canaan

One bright spot for Canaan so far in 2023 has been the growth in mining revenue. At $15.9 million in Q2, mining as a percentage of total revenue has grown from just 3.5% in 2022 to 21.5% in the last quarter.

Balance Sheet

Looking at the balance sheet, the inventory problem sort of jumps off the page. The company has depleted cash and equivalents from over $422 million at the end of 2021 to just $66.1 million at the end of June:

It's worth noting Canaan only drew down cash by $5.9 million from Q1 to Q2. However, cash and total current assets have been in decline for six quarters and inventory has been difficult to move. Again, this is due to problems with machine pricing that go hand in hand with the decline in Bitcoin's price. When the machines aren't as profitable to run, the demand for machines declines and we're seeing the entire industry impacted by this dynamic.

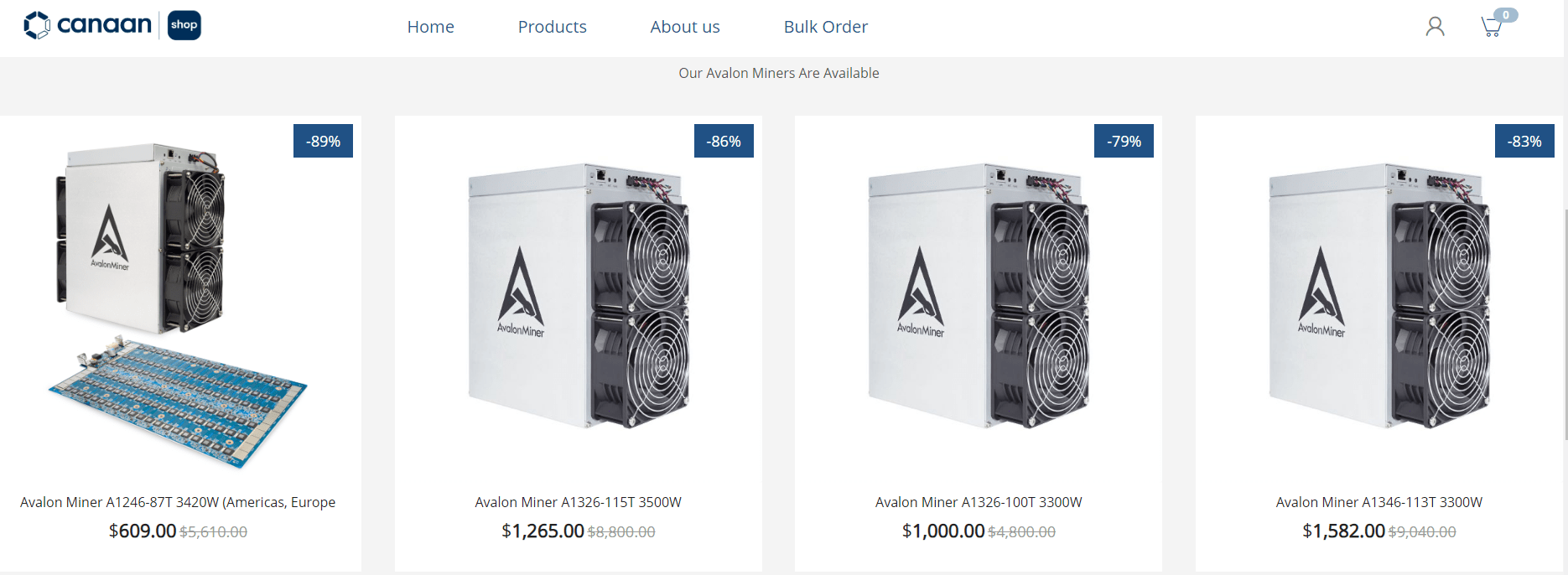

With the upcoming release of the company's new A14 miner series, Canaan is currently selling unused previous generation Avalon A13s for as much as 86% off MSRP:

{kind=link}

This can theoretically turn around for Canaan if the price of Bitcoin starts to increase before the halving next year. But from where I sit, Canaan is in a difficult position and may need to tap its ATM with H.C. Wainwright soon or sell some of the 747 BTC stack on the balance sheet. That BTC is currently valued at about $21 million and gives Canaan about $87 million in total liquidity that it can draw from counting the cash.

Competitive Catalyst?

The three giants in the mining hardware market have historically been Bitmain, MicroBT, and Canaan with Bitmain commanding 60% share of the market based on estimates from DA Davidson last year. Crypto winter has been brutal for just about every company in the cryptocurrency ecosystem and ASIC manufacturers have been feeling it as well. Recently, we've even seen reports that Bitmain has had to temporarily delay payments to employees due to cash flow issues in September. According to crypto journalist Colin Wu, those employees were made whole earlier in October:

It should be noted that only the performance-based portion of some employees' salaries was initially not distributed and has now been paid. Furthermore, the regular basic salaries were also paid on the 30th as per the usual schedule.

In my view, this reported cash crunch that is impacting Bitmain is telling and I think it's something crypto miners and mining investors should be keeping an eye on going forward. I also see it as a possible opportunity to gain share for Canaan if we see demand return. However, I think the broader problems facing Canaan might outweigh the possible reward from taking a speculative wager on CAN even at these depressed share price levels.

Risks

One of the few bright spots in Canaan's second quarter was the growth in mining revenue and it appears that segment is now dealing with challenges as well. On the conference call, CEO Nangeng Zhang disclosed that policy changes in Kazakhstan and a partner default in the United States will impact 3 EH/s in mining power during the company's third quarter. That's a significant hit and accounts for about half the company's EH/s. Canaan is guiding for just $30 million in Q3 revenue.

Summary

While cash levels are down dramatically over the last 18 months, the company's fortunes can turn around fairly quickly if/when Bitcoin's price heads higher. If the surge in BTC price following the incorrect report of BlackRock's (BLK) spot ETF approval is any indication, this market moves fast on positive news. The old adage is past performance is not indicative of future returns and a 5% Fed Funds is certainly a possible factor in it being "different this time."

But BTC is usually much higher in the 6 to 12 months following the halving. The gold rush hasn't started yet. But when it does, I think CAN will be a beneficiary once again. Of course, the big unknown is time. I'm not long this one personally, but I'm not ruling it out either as we get closer to the halving.

For further details see:

Canaan: Time To Buy Shovels?