GOOS - Canada Goose: Waiting For The Targeted Earnings Growth

2023-12-18 17:46:50 ET

Summary

- Canada Goose has had a good long-term track record or revenue growth.

- The company has ambitious financial targets including a revenue target of $3.0 billion CAD by FY2028 and doubled EBIT margins.

- The outlined financial targets don't seem like good baseline expectations, as the current financial performance is far from the targeted level, and long-term growth hasn't resulted in good operating leverage.

- Currently, the stock already seems to be priced with skepticism around the financial targets, and the stock price seems to be mostly in line with my financial expectations.

Canada Goose ( GOOS ) produces and sells luxury apparel with a key focus on winter outerwear. The company has been able to grow revenues through an increasing global brand awareness, segmenting itself as a quality product. Despite achieving a good amount of growth, Canada Goose’s stock has had a total negative return from the 2017 IPO. Earnings have been spent on achieving the growth making no room for dividend payments, either.

{kind=link}

DTC Acceleration Meant to Fuel Future Topline Growth

Historically, Canada Goose has been able to grow revenues very rapidly – from FY2014 to current trailing figures , the company has a revenue CAGR of 22.0%. Concerningly, the company’s growth has slowed down significantly in recent years; in FY2023, Canada Goose’s revenues only rose by 2.6% in USD, and the slow growth seems to be continuing into FY2024.

{kind=link}

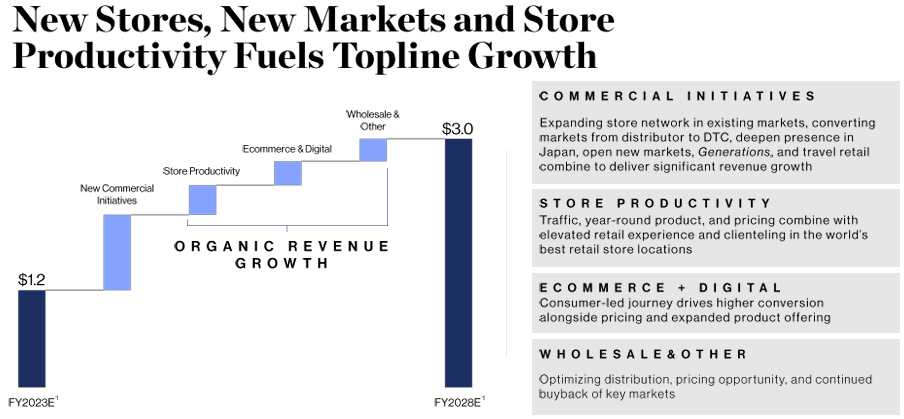

The recent performance is partly disturbed by the pandemic, and after the pandemic effect subsided, the macroeconomic turbulence has played a part in slower growth. On a more long-term basis, the company is still targeting very high growth – for FY2028, Canada Goose targets revenues of $3.0 billion in CAD (or $2245 million USD with the exchange rate at the time of writing), representing a CAGR of 19.8% from FY2023. The company targets to grow the topline through a direct-to-consumer growth approach with increasing store footprint across multiple geographical areas, as told in the February Investor Day . In addition to a growing network of stores, Canada Goose targets growth through increased store productivity, digital growth, and improved wholesale distribution:

{kind=link}

Although the company does seem to have significant growth initiatives, I wouldn’t take the target of $3.0 billion CAD for granted – growth from FY2020 to current trailing figures is 8.5% despite an already increasing DTC footprint. The positioning for growth is clear, but the ambitious target doesn’t seem like a good baseline expectation in my opinion.

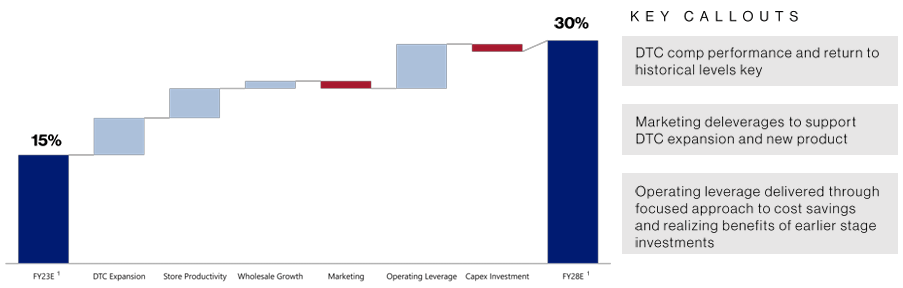

Canada Goose also targets very ambitious margin expansion into FY2028 – from a FY2023 adjusted EBIT margin of 14.4%, the company targets an EBIT margin increase of 15.6 percentage points into 30%. The margin expansion is meant to be leveraged through the direct-to-consumer strategy, leaving more margins for Canada Goose. In addition, the revenue growth is estimated to bring a very significant amount of operating leverage through increased scale and productivity.

{kind=link}

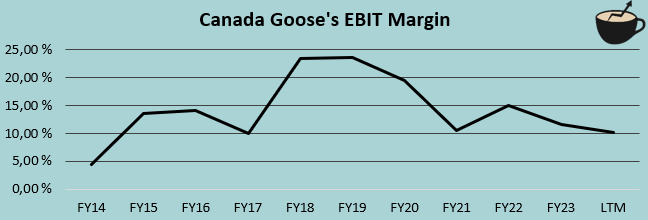

After a very turbulent historical margin performance, the margin expansion target seems excessive – so far, the achieved revenue growth hasn’t resulted in higher margins, as the current GAAP EBIT margin stands at 10.1% with trailing figures. The most significant factor for the margin expansion is expected to be SG&A leverage, as Canada Goose targets SG&A to account for 40% of revenues in FY2028 compared to a current trailing level of 58%. Although the investor day presentation does mention reasonable SG&A efficiencies through cost of goods improvement, better sourcing and technology, a more efficient organization and operating model, and marketing, I don’t believe that the targeted level is a reasonable baseline expectation – the historical margin performance doesn’t seem to have signs of such operating leverage.

{kind=link}

As a takeaway, I don't believe that the financial targets should be taken for granted. The current financial performance does seem to be disturbed by macroeconomic concerns, but in my opinion a financial demonstration of the targets is needed to price in the ambitions into the stock.

An Important Upcoming Quarter

The third quarter in Canada Goose’s fiscal year represents a very large part of the company’s annual revenues – in FY2023, Canada Goose generated around 47% of the year’s revenues in the quarter due to the company’s winterwear focus.

For Q3/FY2024, the company has outlined a revenue guidance of 575 million CAD to 700 million CAD, representing a year-over-year growth of 0% to 21%. The revenue range is very wide – the management’s views about the quarter seem clouded. The company outlines challenging macroeconomic conditions and turbulent geopolitical environments as the reason for outlook pressure for the second half of FY2024 – the company lowered its FY2024 guidance with the Q2/FY2024 report. In Q2/FY2024, the company grew its revenues by 1.4% year-over-year in CAD. Canada Goose communicated that the company started to see a slowing of momentum from September; the current Q3/FY2024 revenue guidance could still be too high.

Looking at Google Trends, the current year’s search peak for “Canada Goose” is a bit higher than in the previous year; although a very weak sign as a single indicator, the search volume could signal some year-over-year growth. As a baseline expectation, I would expect the company to hit the lower end of its Q3/FY2024 guidance.

"Canada Goose" Google Search History (Google Trends)

Market Also Seems Skeptical of the Financial Targets

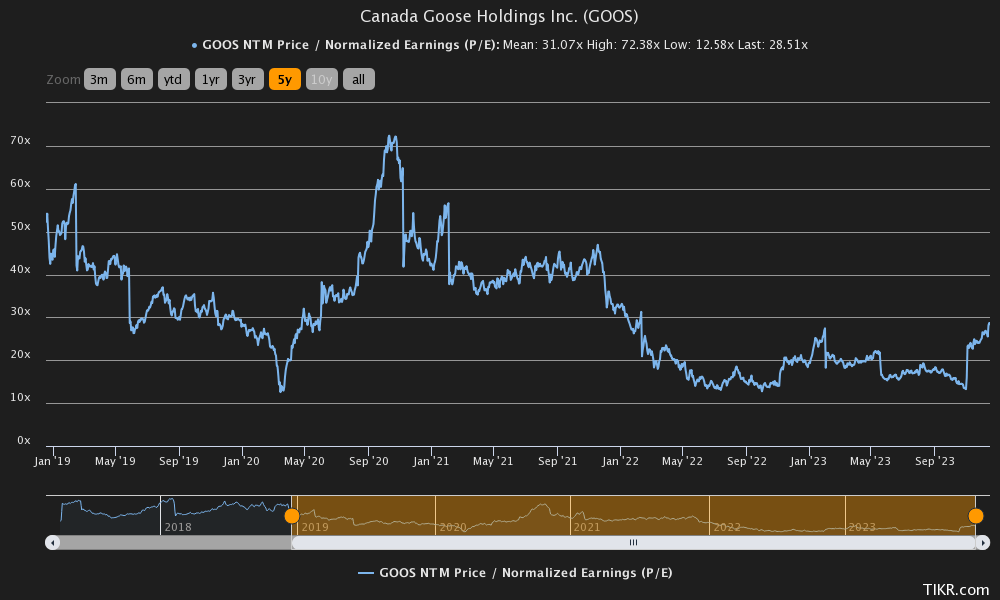

Due to the significant earnings growth potential and targets, Canada Goose has traded at a high forward P/E multiple – in the past five years, the average forward P/E has been 31.1, with a current forward ratio slightly lower at 28.5. The current ratio jumped with the Q2/FY2024 report from low double-digit figures, as EPS estimates for the upcoming year were lowered very significantly.

{kind=link}

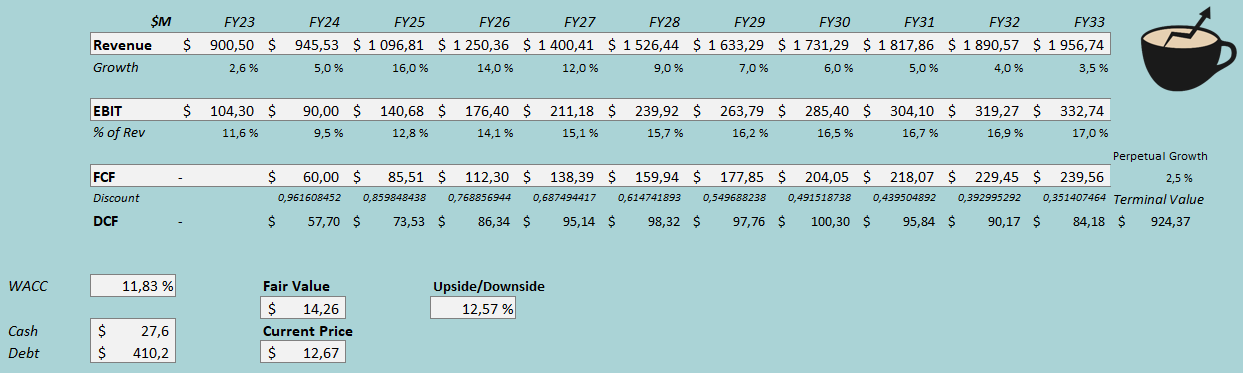

To demonstrate the valuation better, I constructed a discounted cash flow model with my financial assumptions. In the model, I estimate Canada Goose to achieve revenue growth and margin expansion, although not at the level that the company targets.

For the revenue growth, I estimate revenues of $1526 million for FY2028, compared to the target of $2245 million with current exchange rates; the revenue CAGR of 12.7% from FY2024 to FY2028 is a good baseline expectation in my opinion. From FY2023 to FY2033, the estimated revenue CAGR is 8.1%, with the growth ending into a perpetual rate of 2.5%. I estimate the margins to also scale with the growth; after a weak FY2024 estimate of a 9.5% GAAP EBIT margin, I approximate a margin expansion of 7.5 percentage points into an eventual EBIT margin of 17%. The margin is well below Canada Goose’s adjusted EBIT-% target of 30%, but seems like a more probable achieved level in my opinion.

With the mentioned estimates along with a cost of capital of 11.83%, the DCF model estimates Canada Goose’s fair value at $14.26, around 13% above the stock price at the time of writing. The stock seems to be priced slightly favorably, but I don’t see the risk-to-reward as good enough for a buy rating at the current level, until Canada Goose demonstrates its earnings growth capabilities better; the market’s pricing seems to indicate the same conservatism towards the investor day targets.

{kind=link}

The used weighed average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q2/FY2024 Canada Goose had $7.9 million in interest expenses. With the company’s current amount of interest-bearing debt , Canada Goose’s annualized interest rate comes up to 7.68%. The company uses a good amount of debt in its financing, and I estimate the debt profile to stay quite similar with a long-term debt-to-equity ratio of 30%. For the risk-free rate on the cost of equity side, I use the United States’ 10-year bond yield of 3.90% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Canada Goose’s beta at a figure of 1.60. Finally, I add a small liquidity premium of 0.3%, crafting a cost of equity of 13.66% and a WACC of 11.83%.

Takeaway

At the current price, Canada Goose seems like a fair investment, although I wouldn’t expect very significant outperformance at the moment – Canada Goose’s highly ambitious long-term financial targets don’t seem like good baseline expectations, and with my estimates, the stock has slight undervaluation. If the financial targets are achieved, Canada Goose’s stock would have very significant upside with the current price. Still, as the current financial performance doesn’t seem to be in line with the targeted level, I only have a hold rating for the time being.

For further details see:

Canada Goose: Waiting For The Targeted Earnings Growth