CSIQ - Canadian Solar: Buy But Only At $31 Per Share

Summary

- The renewable energy and solar market is expected to grow by double digits for the rest of the decade.

- Canadian Solar is a leading player with a 9% market share on the global solar module market.

- Growth is expected to explode in 2023 with some analysts forecasting growth of 80% per year (while management expects 55%).

- Personally, I take a conservative approach and will only buy at a level where the company only needs to grow its EPS by 16% to be considered fairly valued. That level happens to be major support at $31 per share.

Dear readers/followers,

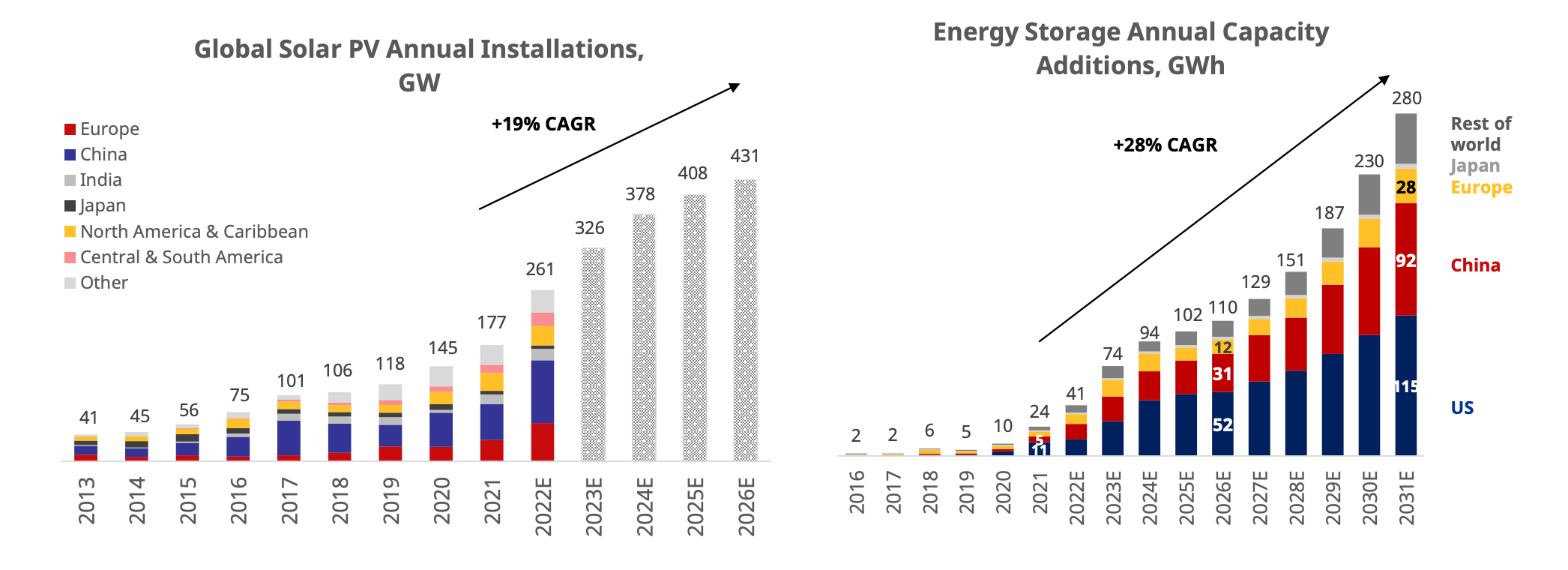

After my recent article on Hannon Armstrong (HASI), I want to expand on the idea of investing in renewable energy. I believe the sector is likely to face serious tailwinds over the next decade as countries try to transition away from their dependency on fossil fuels. Demand for solar panels is expected to grow by 19% for the next 5 years, while energy storage solutions are expected to enter the exponential market growth phase with growth of up to 28% per year. This is further supported by the fact that solar penetration as a percentage of total electricity generation is just 3% (compared to hydro at 15% and coal at 33%).

{kind=link}

Also, the recently passed Inflation Reduction Act will provide 10-years of tax credits in an effort to support green energy, which could significantly help companies that operate within the space. So today I want to analyze Canadian Solar ( CSIQ ) which is one of the world's largest solar companies with a 9% market share on the global solar module market.

Overview

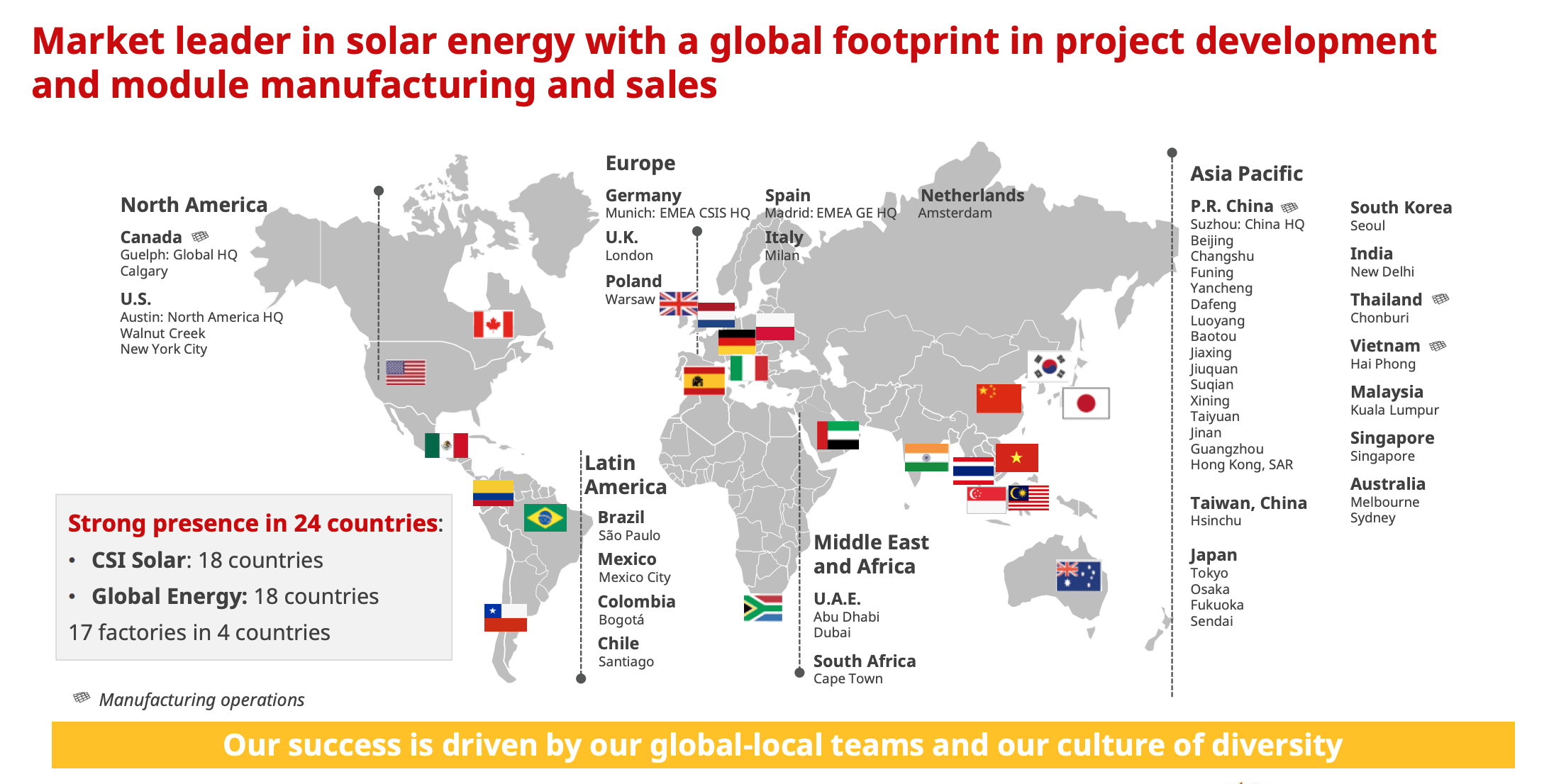

Canadian Solar is a Canadian based solar power company that focuses on manufacturing solar panels and energy storage solutions for the residential, commercial and utility sector. The company is a global player with presence in 24 countries worldwide and with factories in Canada, China, Thailand and Vietnam. Revenue is generated around the world with 31% coming from North America, 23% from China, 15% from EMEA, 12% from Latin America and the rest from Asia excluding China.

{kind=link}

CSIQ has a competitive advantage over its competition because it is vertically integrated. This means that the company is involved in the whole process of developing and manufacturing its products through the whole supply chain, resulting in lower costs and better end results at the company knows exactly what it needs.

Financials

The company operates two main lines of business:

- CSI Solar - primarily concerned with manufacturing of solar panels and related systems primarily for utility-scale solutions (50% of total), commercial/industrial use (39% of total) and finally for residential use (11% of total)

- Global Energy - focused on energy storage solutions

Most of the revenue (about 80%) comes from CSI Solar, but Global Energy tends to have higher margins, although they can be pretty volatile as seen below.

{kind=link}

It is very evident that the business is highly cyclical as quarterly EPS tend to oscillate between zero and $1.60 per share. This makes it hard to forecast. For 2023 management is guiding towards delivering 30-35 GW of solar modules which is a 56% increase compared to 2020, consequently revenue is expected to increase by a similar percentage to $11.4 Billion. This has been reaffirmed by preliminary unaudited Q4 results that the company released just yesterday.

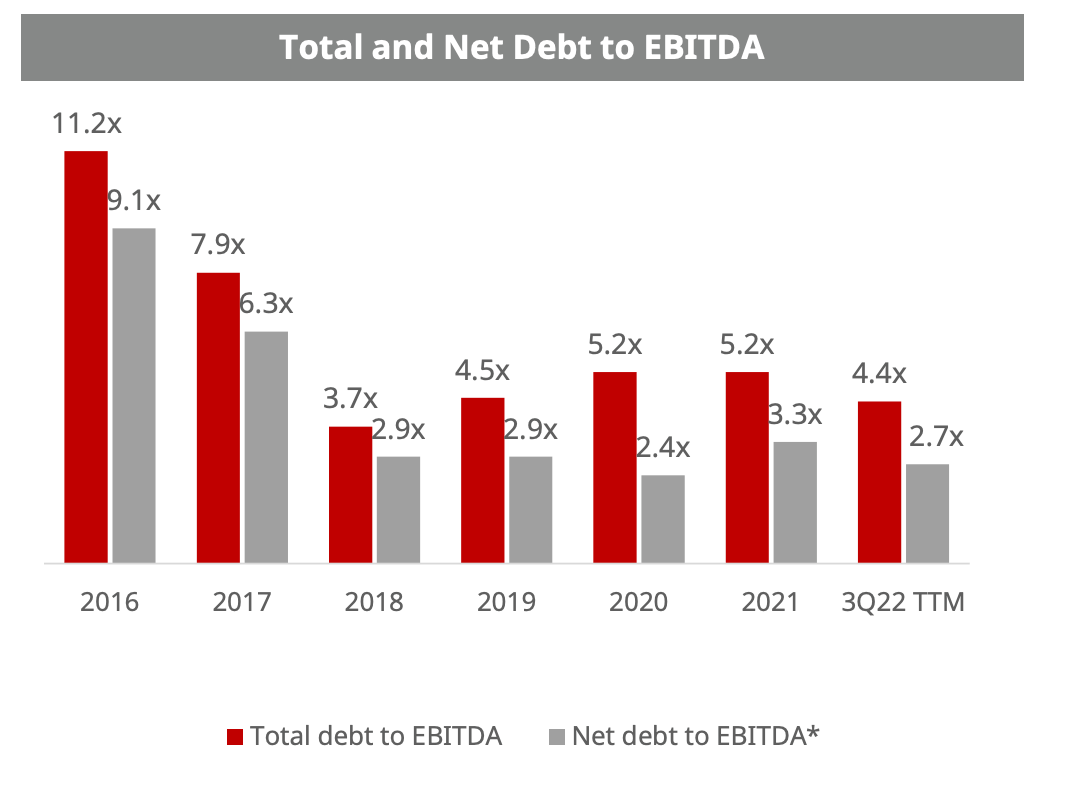

The company has about $2.7 Billion in debt and $1.1 Billion in cash. Notably both total and net debt to EBITDA have decreased YoY. Though I consider these levels of debt healthy, they could put pressure on earnings if revenues decline or if interest rates stay high for a prolonged period of time and the company has to refinance its debt at higher rates.

{kind=link}

Valuation

Based on a relative valuation, CSIQ currently trades at a P/E of 16.6x and a forward P/E of 7.1x. The difference is huge and essentially implies that earning are expected to almost double in 2023. Personally, I don't like to rely on such high growth in my valuation and with only three analysts covering the stock, I won't put too much weight on the forward P/E. With that said if we assume that management delivers on their target of 56% growth (EPS of $4.40) that would imply a much more reasonable forward P/E of 8.6x. Historically the stock has traded at a P/E closer to 9-10x which still leaves about 10-15% of upside if the stock normalizes (of course only if management delivers).

When compared to peers, JinkoSolar (JKS) which is a Chinese-based company which operates in a very similar way trades at a P/E of 14x. Of the two I would choose Canadian Solar every day for the simple reason that I don't like investing into Chinese companies and consider them more risky for political reasons. I don't think other companies, such as SunPower ( SPWR ) or Enphase ( ENPH ) are relevant comparables as they are focused much more on the residential market and have significantly higher PEs.

From a technical standpoint, the company has a pretty significant support level around $31 per share. At this level a forward P/E ratio of 9.5x (which is fair from a historical standpoint) would only imply earnings growth of 16% in 2023. That's way under the forecast and management's guidance and actually something I am willing to put my money on.

{kind=link}

Remember how I generate alpha:

- start with a thesis why a given industry/sector should outperform

- stay overweight in those sectors for as long as the thesis is valid

- look for companies with sound fundamentals that are either undervalued or fairly valued with exceptional growth prospects

- if a company becomes overvalued, trim the position and rotate into another stock/sector that is still undervalued

- if a company becomes increasingly undervalued and the thesis is still valid, add to the position

- generate alpha and repeat

My total return then comes from the dividend yield, EPS growth and multiple expansion as the valuation normalizes over time. I always target a total return in excess of market returns (>8%) to generate alpha.

What things do I look for when selecting individual stocks to buy?

- strong and safe fundamentals

- good management teams with a track-record of caring about shareholders

- healthy EPS growth

- well-covered dividend

- discount relative to peers and/or historical fair multiples

- other catalysts

Investor Takeaway

Canadian Solar is a solid company, but valuing it is tricky because of how cyclical the company is. Quarterly earnings per share have oscillated between zero and $1.60 for the past 10 years without really showing a clear trend. But with the renewable energy industry and solar in particular expected to grow by double digits for the rest of the decade, analysts expect growth to pick up significantly in 2023. I don't feel comfortable assuming 50%+ growth in the current economic environment so I will wait for the stock to come to me.

I currently rate Canadian Solar as a " HOLD " but will flip to a " BUY " if we come to $31 per share or lower. At this level the company only needs to grow its EPS by 16% to be considered fairly valued today and that's something I am comfortable with.

For further details see:

Canadian Solar: Buy But Only At $31 Per Share