CSIQ - Canadian Solar: Difficult Not To Be Bullish

Summary

- Canadian Solar is rapidly growing. That said, there's a fair amount of volatility in its revenue growth rates.

- For instance, Canadian Solar's Global Energy segment fell 28% y/y. This is not what you'd expect from a business that is expected to rapidly grow in the medium term.

- On the other hand, the business is highly profitable and cheaply valued.

Investment Thesis

Canadian Solar ( CSIQ ) manufactures solar power products, including solar panels, modules, and solar power systems for residential, commercial, and utility-scale power generation.

The business is clearly growing rapidly. But the growth rates are bumpy. Very bumpy. Nonetheless, the business is profitable with its profitability rapidly rising.

Like any investment, there are risks. But altogether, I believe that paying about 10x forward EPS could be quite an attractive investment proposition. Particularly if one believes that over time we'll increase our global exposure to solar panel energy sources.

Canadian Solar's Near-Term Prospects

Canadian Solar is a geographically diversified solar panel manufacturer, with two business segments, CSI Solar and Global Energy.

Its biggest segment, CSI Solar consists of solar module manufacturing. While Global Energy is focused on energy storage projects.

Even though its Global Energy business is about 5% of the size of its CSI Solar segment, what Global Energy lacks in size it makes up with profitability.

CSIQ Q3 2022 presentation

As you can see above, Global Energy's income from operations was $27 million in Q3. However, what I found surprising is that there was very little mention throughout the earnings call of why Global Energy saw its revenues drop 28% y/y.

Furthermore, in its earnings call , Canadian Solar expresses a view that it prefers to be small and profitable, rather than growing for growth's sake.

Canadian Solar is more than just size. We prioritize the quality and profitability of the pipeline we are building. We are selective on the projects that we decide to move ahead with and we are not afraid of walk away from projects with less attractive risk return profile.

And this leads me to discuss its revenue growth rates.

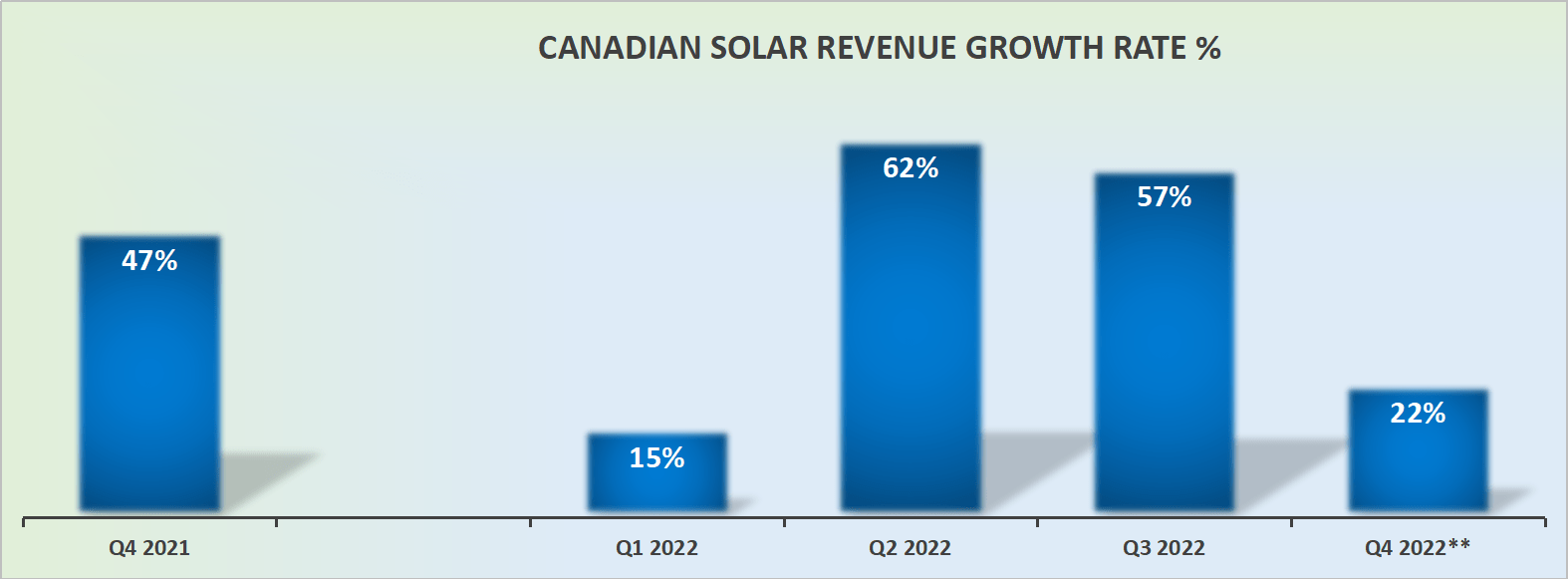

Revenue Growth Rates are Highly Cyclical

{kind=link}

The chart above is a reminder of just how cyclical Canadian Solar's growth rates can be. Accordingly, with this volatility in its growth rates, attempting to look out and accurately estimate its near-term sustainable growth rates becomes incredibly challenging.

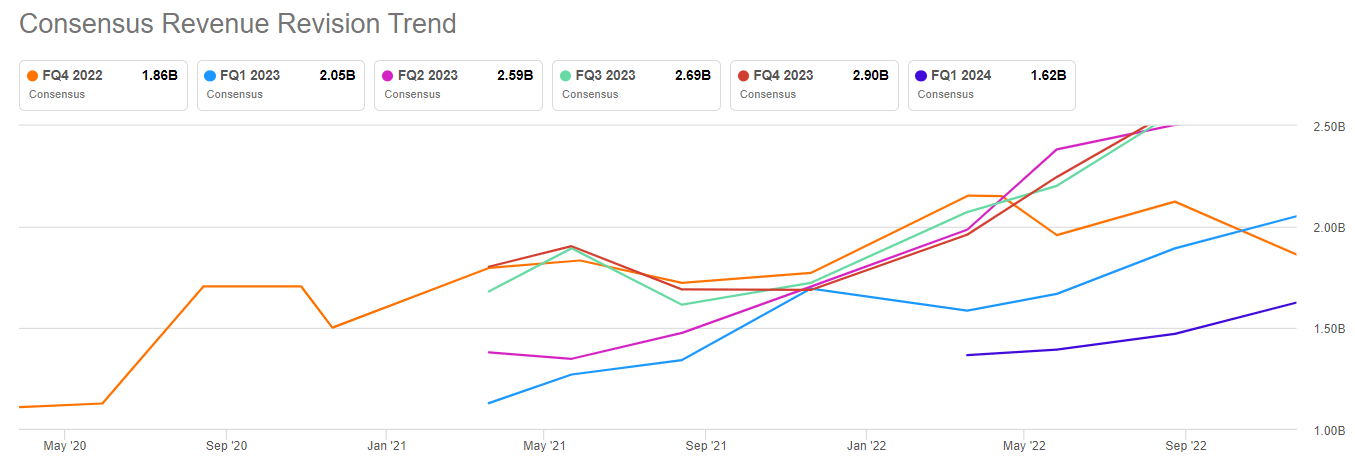

Along these lines, note just how uncertain analysts following Canadian Solar have been in estimating its revenue growth rates.

{kind=link}

That being said, the following section is helpful in distracting us from Canadian Solar's bumpy and uncertain revenue growth rates. Consider next the crown jewel of this investment thesis.

Profitability Profile is the Crown Jewel

{kind=link}

The table above reminds us of two aspects. Not only has Canadian solar a history of being profitable. But also, its profitability is rapidly rising.

As a point of reference, its income from operations for Q3 alone was practically half of the profitability of the whole of 2021.

Key Investment Risks

Undoubtedly, there's a lot of excitement over the solar panel market. This will mean that there are going to be periods where the stock is very volatile.

More crucially, there will be times when solar modules are significantly oversupplied. As a result, the industry is expected to experience significant cyclicality because solar panel makers are only really able to compete on price.

Government support initiatives continue to aid solar panel demand. But if this financial support is reduced, this could dent customer demand, which would negatively impact Canadian Solar's pricing power.

In the long term, positive regulations and grid infrastructure will be a tailwind for solar panel demand. But in the near term, since solar panels are a source of electricity generation and natural gas prices have come down substantially in North America, customer appetite for solar panels could be muted.

The Bottom Line

There are several near-term catalysts that may propel the stock higher. These include:

- Its carve-out IPO of CSI Solar Co., Ltd.

- Potential increase in revenues if Canadian Solar is able to receive subsidies from the Inflation Reduction Act.

- Continued rapid growth in profitability.

Altogether, paying 10x forward earnings for a highly profitable business doesn't strike me as expensive.

For further details see:

Canadian Solar: Difficult Not To Be Bullish