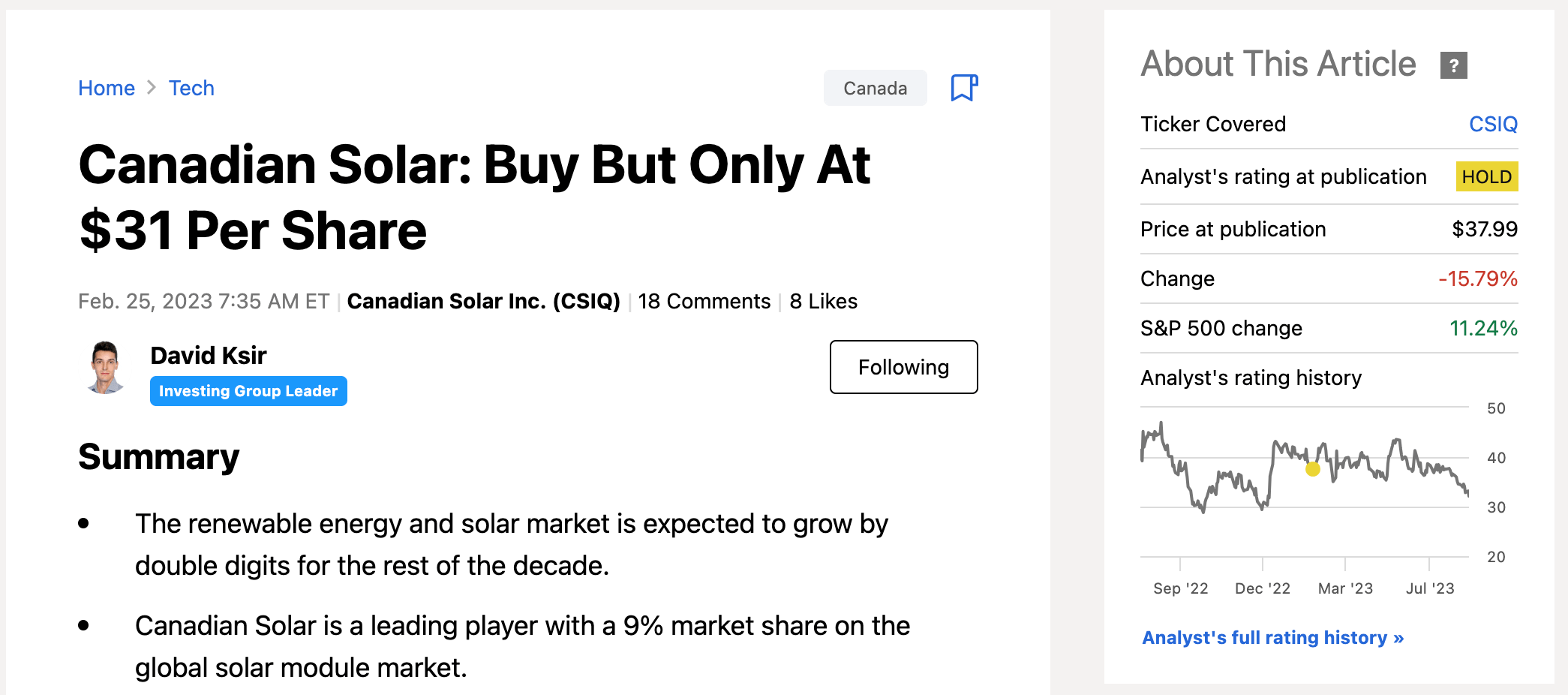

CSIQ - Canadian Solar Has Become Undervalued On Fears Of Lower Guidance

2023-08-17 05:29:02 ET

Summary

- Canadian Solar is positioned in a high-growth sector, with the solar market expected to grow at a CAGR of 19% for the next five years.

- The company operates in both solar panel manufacturing and energy storage solutions, with the latter expected to contribute significantly to earnings.

- CSIQ stock has a potential upside, with a forward P/E ratio of 6.7x assuming no further growth and a price target of $45 per share if EPS reaches $5.

Dear readers/followers,

I started coverage on Canadian Solar ( CSIQ ) back in February with a HOLD rating at $38 per share. While many investors were eager to buy the stock back then, I didn't like the fact that the market was expecting 50%+ growth in earnings in 2023. The implied growth assumption was simply too aggressive for my appetite and I was sceptical the company would deliver, especially in a tough economic environment. I turns out that I was right as the stock has underperformed significantly since then.

{kind=link}

I like to stay conservative which is why I only assumed 16% growth this year (way below managements 55% growth guidance) and used an average historical P/E of 9.5x to calculate a conservative entry point at $31 per share.

In early March, I sold $33 July puts at $2 (and informed everyone in the comment section below the original article). These puts have now expired worthless, so I pocketed the full $2 premium.

Today, the stock trades much lower at $32 per share, so including the premium received, I could open a position with a break-even below $31 per share. Now it's time to update my thesis, based on most recent earnings and based on recent developments that have dragged solar stock much lower.

Canadian Solar - positioned in a growth sector

The company is a leading global solar panel producer with a 9% market share on the global solar module market. In addition to panel production, the company is also involved in energy storage solutions.

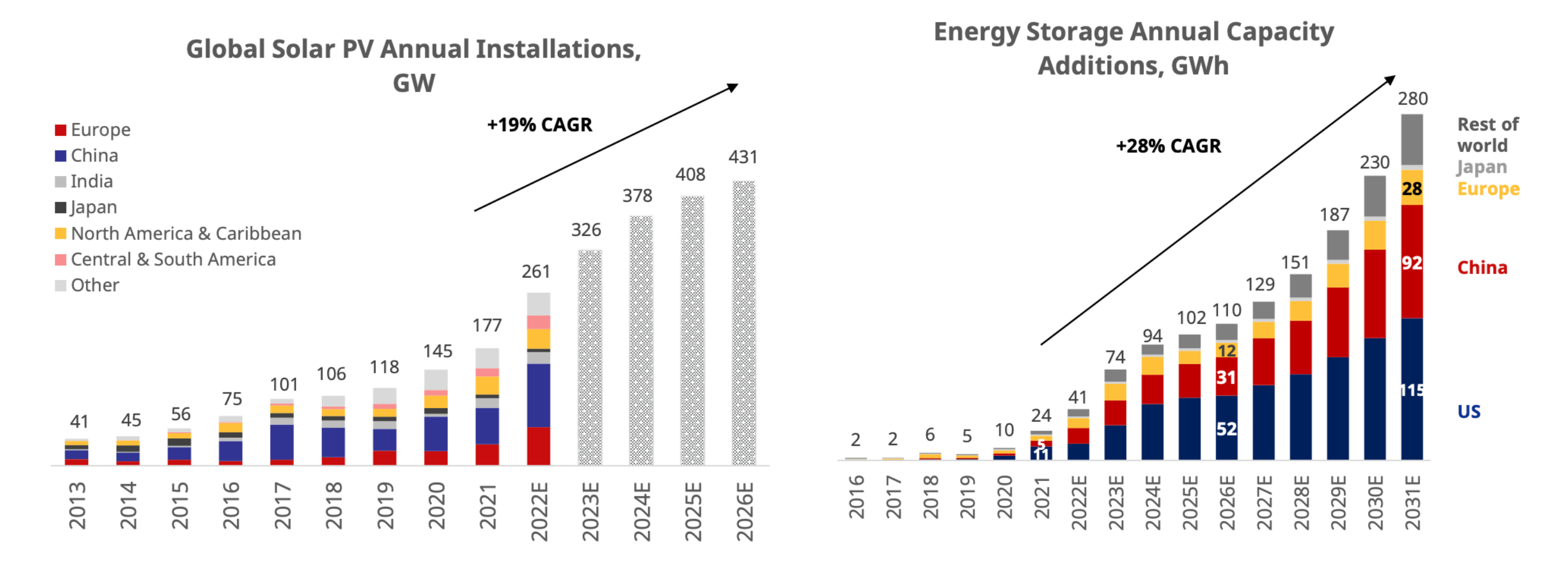

What's important is that the solar market is expected to be a high growth market for the foreseeable future, especially as governments around the world continue to push their green initiatives. Demand for solar panels is forecasted to grow at a 19% CAGR for the next five years, while storage solutions are expected to grow by up to 28%.

{kind=link}

And the thing is that the growth runway is actually quite long, way beyond the next five years, as solar now accounts for just 3% of electricity generated (compared to hydro at 15% and coal at 33%).

Financials

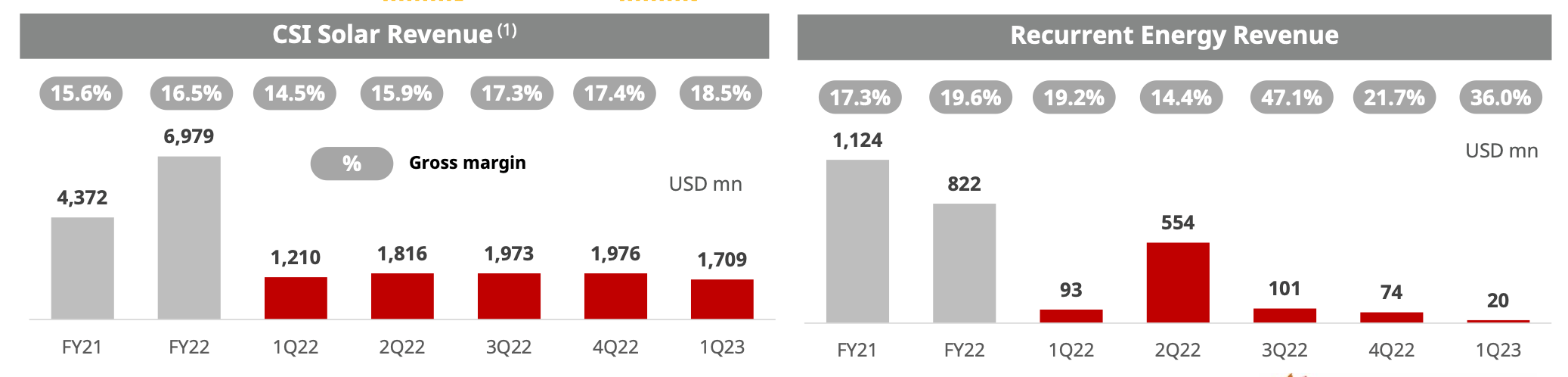

The company operates in two main segments - CSI Solar (i.e. solar panel manufacturing) and Energy (i.e. storage solutions). Revenues have historically been driven primarily by panel manufacturing, but as energy solutions enter their exponential growth stage, they're expected to contribute to earnings a lot, thanks to very high margins.

{kind=link}

During Q1, the company deliver 6.1 GW of solar modules and earned revenue of $1.7 Billion - in line with last year's average, but below Q3 and Q4. For Q2 guidance calls for 8.1-8.4 GW delivered.

Since panel production is the primary driver of the company's results, I will be watching their Q2 earnings, which are scheduled for August 22, to see if they can meet their guidance targets for Q2 and if they change their aggressive full year guidance which currently calls for 55% YoY growth in deliveries (30-35 GW).

Frankly, following SolarEdge's ( SEDG ) recent announcement of disappointing guidance for Q3, citing recent headwinds related to high interest rates, I'm not sure if Canadian Solar will be able to deliver what they promised and expect a revision in guidance downward. The market largely seems to agree as all solar stocks have sold off following SEDG's announcement.

Valuation

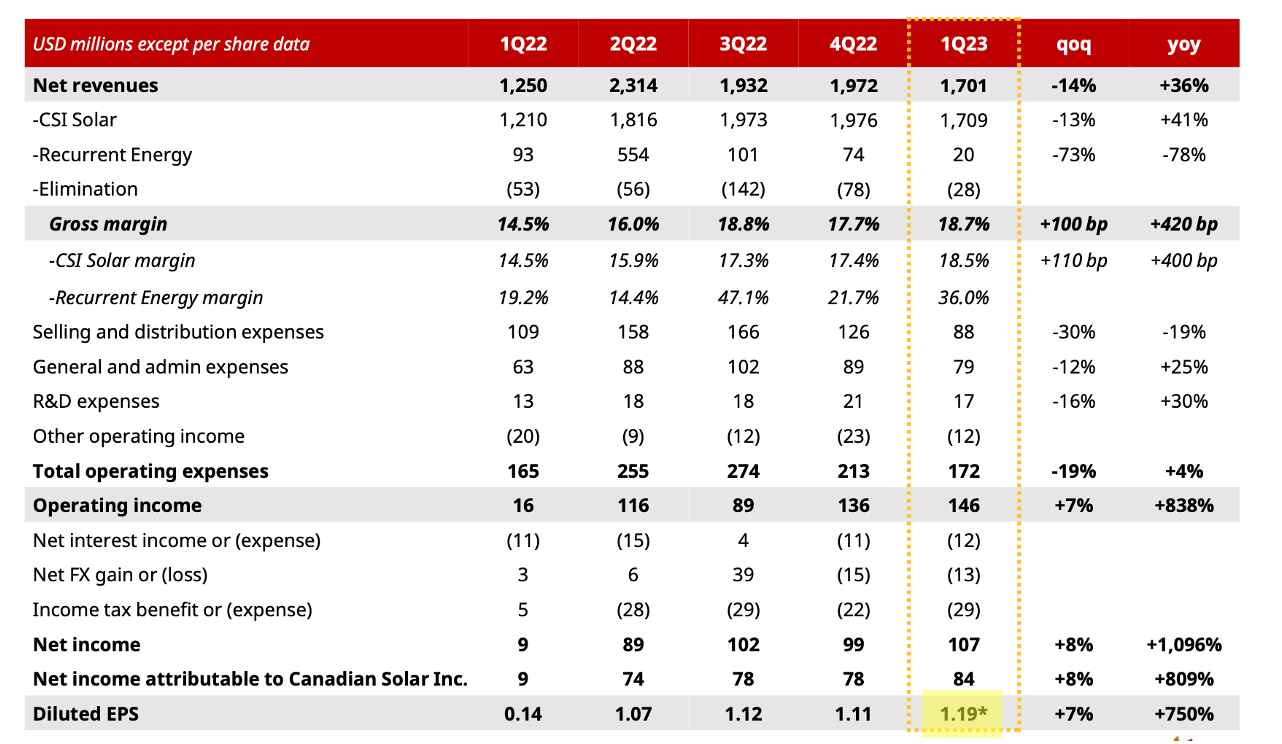

During the first quarter, the company has delivered EPS of $1.19.

{kind=link}

For the sake of valuation, let's first assume no further growth for the rest of the year. That would mean an annualized EPS of $4.76 and therefore a forward P/E ratio of 6.7x. Note that historically, the stock has traded around 9-10x earnings, which suggests that the stock indeed has some upside.

A more realistic scenario is that the company will grow its revenues from $7.4 Billion in 2022 to something like $8.5 Billion this year (guidance right now calls for $9-9.5 Billion, but I do expect to be revised downward in Q2 earnings). That would be about a 15% annual growth and would translate into an even lower forward P/E ratio of 5.8x.

That leaves quite a bit of upside when the stock returns to even 9x earnings. In particular, EPS of $5 (which is considerably below guidance and consensus) would imply a price target of $45 per share, or 40% upside from current levels.

I believe the market has overreacted a bit on SolarEdge's announcement of lower guidance and as a result we have an opportunity to enter Canadian Solar at a very promising level. That's why I upgrade my rating to BUY here at $32 per share.

As many of you know, in addition to renewable energy (and financials), I mostly write about REITs. Recently I have published by bullish thesis for the sector. I encourage you check it out, because I believe that the sector has many of the same catalysts as renewable energy, including solar.

For further details see:

Canadian Solar Has Become Undervalued On Fears Of Lower Guidance