CSIQ - Canadian Solar: IPO Catalyst To Price In

2023-06-13 16:51:34 ET

Summary

- Canadian Solar reported Q1 revenue of $1.7 billion and a gross margin of 18.7%, with a 2023 fiscal year top-line sales outlook narrowed toward the high end of guidance.

- The company's majority-owned subsidiary, CSI Solar Co, recently completed its IPO process, raising approximately $844 million and trading at a premium compared to Canadian Solar's valuation.

- The Inflation Reduction Act might be an additional positive catalyst to sustain medium-term growth.

In our initiation of coverage, we positively reported how Canadian Solar ( CSIQ ) was " Ready To Gain Back Margins ". Considering also that Q1 is usually a softer quarter, the company reported a solid gross margin evolution.

{kind=link}

Source: Canadian Solar Q1 results presentation

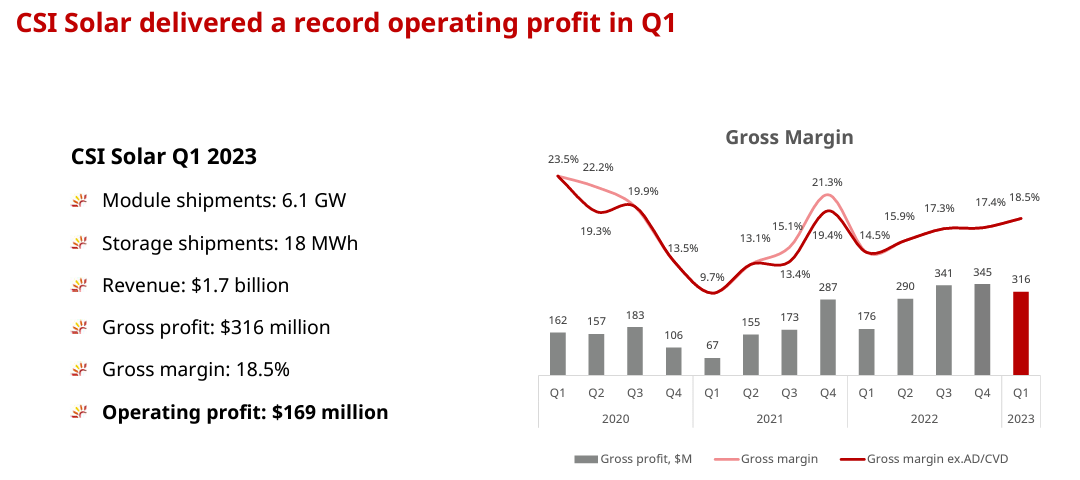

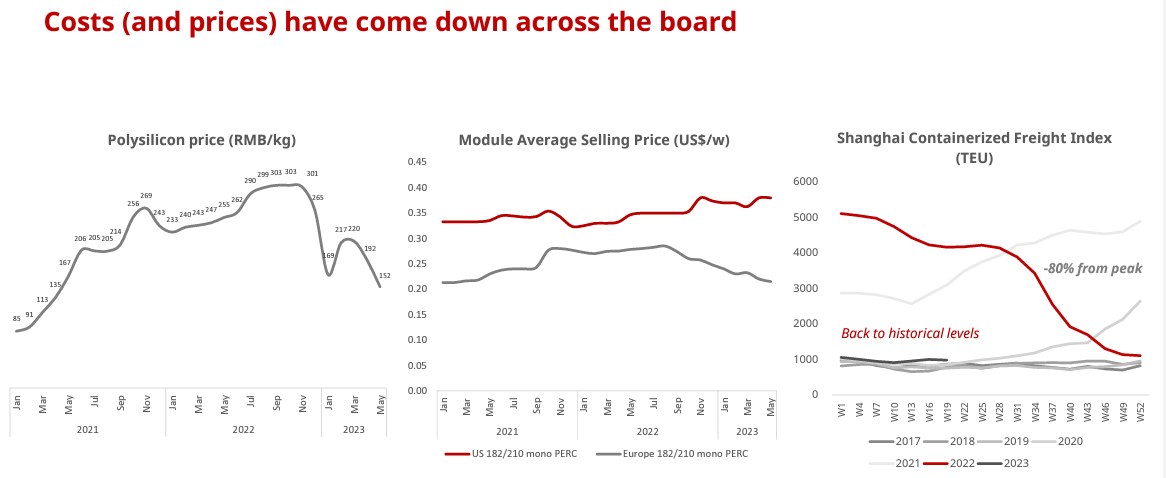

Very briefly, CSIQ delivered Q1 revenue and gross margin aligned with Wall Street expectations, while opex was lower than anticipated. This was due to declining input cost in the module average selling price (Fig below). More important to emphasize is the fact that the 2023 Fiscal Year top-line sales outlook was narrowed toward the high end of the guidance. This should be supportive of Canadian Solar's stock re-pricing. Q1 revenue figures reached $1.7 billion with a gross margin of 18.7%. In addition, diluted earnings per share beat Wall Street's expectations which were forecasting $0.61 (the company achieved an adj. EPS of $1.19). Canadian Solar also forecasts an easing in the supply-chain constraint and reports that logistics is now normalizing. The solar backlog is sequentially up, but the company's pipeline remained flat at ~25GW.

In our future estimates, we are leaving CAPEX guidance unchanged at $1.5 billion (this is due to previous investments in capacity expansions); however, we add a new negative one-off due to an IPO cost of $50 million estimated for the second quarter. We are forecasting Q2 revenue at $2.5 billion with a gross margin of 20.5%. This is mainly driven by declining raw material prices (polysilicon prices).

{kind=link}

Thanks to the inflation reduction act (IRA) and the bonus credits , we believe that Canadian Solar will target a new module capacity expansion. And again, even if we are not pricing this positive development, this might unlock additional shareholders' value.

{kind=link}

IPO unlocking shareholders' Value

On June 9, Canadian Solar announced that its majority-owned subsidiary CSI Solar Co finalized its IPO process. CSI shares are now trading on the Shanghai Stock Exchange. In detail, CSI Solar issued 541 million shares at a price of RMB 11.10 ($1.56). The IPO proceeds were worth approximately RMB 6.0 billion ($844 million) and were above our internal model forecast of $600 million. Looking at CSI Solar's implied multiple valuations, the company is being valued at a 2023 EV/EBITDA multiple of 4.6x, and a 2024 EV/EBITDA multiple of 4.0x. In our calculation, we are assuming that half of CSIQ's financial obligation and the majority of the company's cash resides at CSI Solar.

Valuation

Chinese stockholders usually seem more friendly to manufacturing companies and willing to pay higher multiples than US investors. This was the likely reason behind the Chinese listing, and here at the Lab, we believe this was the first management consideration in selecting the right country. As already mentioned, CSI Solar was valued at 4.6x 2023E EBITDA compared to CSIQ's implied multiple at 3.9x. This implies a ~20% premium on the US valuation. However, looking at the IPO prospectus, the lowest average price quoted by institutional investors was above RMB 16 per share. So, we are not surprised to see CSI Solar stock price appreciation from RMB 11.10 to RMB 14.80 on the first day of trading. If CSI Solar will reach RMB 16 per share, it would imply a 2023E EV/EBITDA multiple of 6.8x with a 74% premium to CSIQ's current multiple. Therefore, in a base case scenario, valuing CSIQ at a CSI Solar IPO valuation price implies at least a 20% upside. Here at the Lab, we ended up valuing CSIQ at $44 per share, moving our rating from an equal weight valuation to a buy rating. It is still unclear if the valuation gap will be closed given the above differences in investor preferences. For this reason, CSIQ may continue to trade at a discount; however, having said that, CSI Solar stock price appreciation might force the gap to close. To support our new buy rating, we should also mention that Canadian Solar is trading at 7.8x our 2023 EPS estimate, a discount to the 1-3-5 year periods versus its historical average.

{kind=link}

Source: Bloomberg

Risks

Downside risks include 1) excess capacity that might cause compressed margins, 2) project execution risks with higher cash burn, 3) new tariffs on panels imported by other countries, 4) lower subsidies from governments, and 5) new technologies in the renewable energy space that might negatively affect Canadian current business model.

For further details see:

Canadian Solar: IPO Catalyst To Price In