CSIQ - Canadian Solar Is Embarking On A Serious Expansion Path

Summary

- Canadian Solar's management sees the secular tailwinds in the industry and has the ambition to take full advantage, embarking on an epic expansion plan, including building their own poly plant.

- The CapEx needs will be large but a carve-out IPO will finance most of the poly plant.

- The company coming out of the other end of this process will be a much bigger venture.

- The process is not without risk but the company's history of profitability should allay most concerns.

- The share price has fallen back after the excellent Q2 results and is attractive.

Canadian Solar (CSIQ), a top manufacturer of solar panels and energy storage products and projects, produced very good Q2 results.

Reasons to buy

- Secular tailwinds

- The stock price has fallen back, valuation is very reasonable

- History of profitability

- Big ambitions in energy storage and projects

Secular tailwinds

That the company should benefit from considerable industry and policy tailwinds should come as no surprise:

- The ever-declining cost of solar energy makes it ever more viable in ever more places.

- The electrification of transport.

- The sinking cost of energy storage gives another boost to solar energy and provides another market opportunity as well.

- Policies aimed at reducing the speed of climate change, like the Inflation Reduction Act passed this year in the US.

- Concerns about energy dependence as a result of the Russian invasion of Ukraine.

The company has also been profitable on an ongoing basis for the past 5 years even on a GAAP basis:

Bankable

While solar panels are a near commodity and the industry is plagued by cyclical downturns that can lead to rapid price declines, margin erosion, overcapacity, and inventory corrections and write-downs.

However, these price declines set the stage for recovery as solar's competitive position versus other energy sources improves further, and given the secular tailwinds, the cycles have become milder.

What is also important to realize is that while panels are a near commodity and hence companies enjoy limited pricing power, the bigger, more established, and fundamentally more sound companies are more 'bankable' and they tend to be spared the worst of the cyclical shake-out.

The company is one of the more bankable brands ( PV Tech ):

PV Tech

This isn't surprising given the company's large project business, which actually tends to make companies less sensitive to cyclical downturns.

Energy storage

The company has launched a successful energy storage business and they are investing significantly in developing their proprietary battery storage products and support products and software.

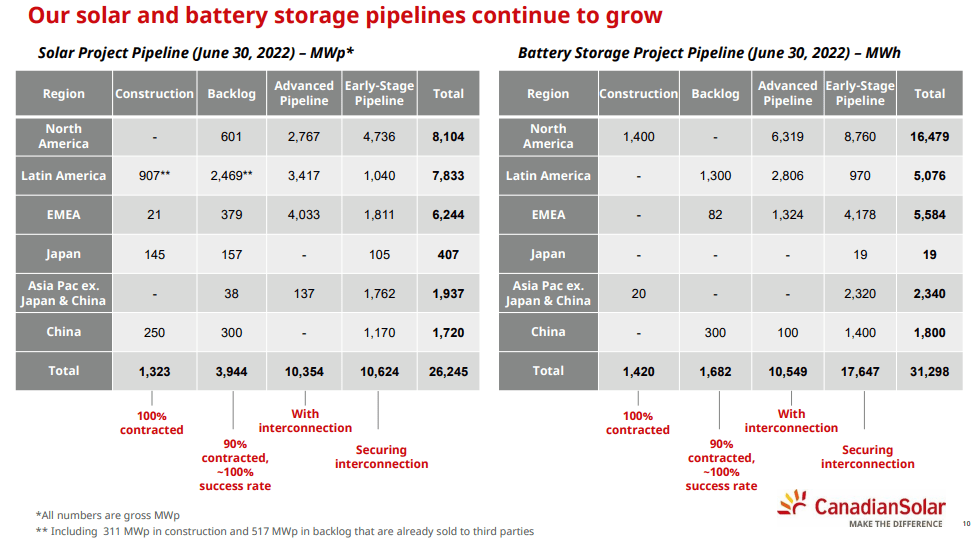

The company shipped 1GWH of energy storage in H1/22, this is a pretty big business for the company already and has a whopping 31 GWp (GigaWatt peak power) in the pipeline (see graph below):

Project business

{kind=link}

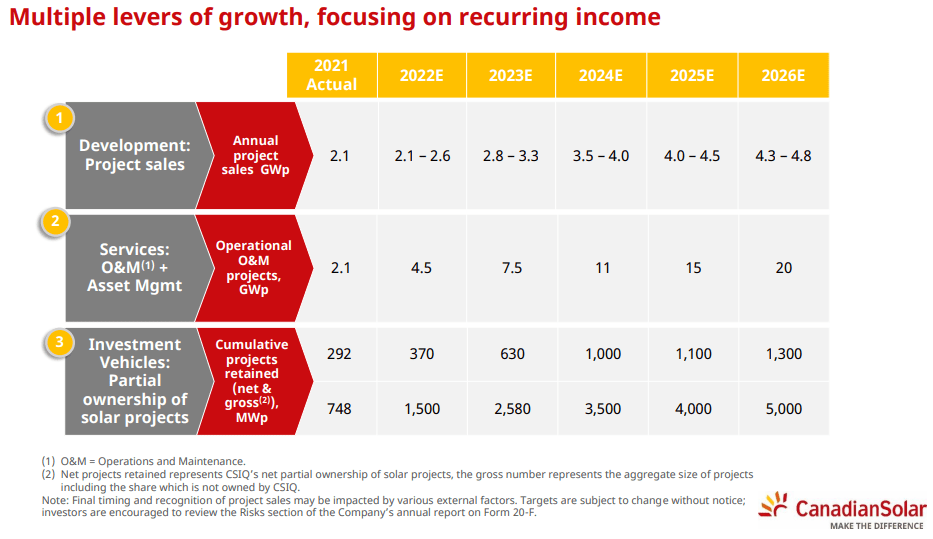

The company designs, develops and manages energy plants consisting of PV panels with or without energy storage. Most of these projects are sold, but the company increasingly maintains minority stakes and sells electricity before the projects are sold, both of which produce recurring revenue.

It also supplies O&M service contracts involving stuff like monitoring, repair and, site management and administrative support services. The company has developed some specialized solutions ( 20-F ):

We have deployed a number of unique technologies including semi-automated module washing, autonomous vegetation management, machine learning technologies in predictive maintenance and drone inspection.

It already had 3.1GW of projects under O&M services at the end of Q2 and the target is 20GW by the end of 2026 (see below). The company has formed a couple of funds to pool capital to develop, build and accumulate solar projects, one with the Macquarie Group (JGIF) and the more recent CSFS Fund I in Italy.

They have a global monitoring platform (CSEye) to monitor projects in real time (20-F):

to automatically receive alerts about exceptions, and to automate the reporting of performance, technician work orders, warranty claims, spare parts, health & safety incidences, manage system alarms and reports, all of which can be accessed through cloud applications. Our proprietary algorithms analyze the performance of the self-owned and third party power plants that we operate and maintain on a daily basis and identify potential problems. For example, they raise alarms when inverters or strings are under-performing.

The company not only sells projects, but it also earns an increasing amount of recurring revenues (selling electricity and providing O&M services) from projects.

{kind=link}

The company has 3GW + 2.4GW of projects under O&M agreements, with another 2.4GW coming soon and a target of 20GW for FY26.

The company concluded another big project after the quarter closed, a stand-alone 350 MW/1400 MWh energy storage project in which it retains a 205 ownership and providing O&M services.

Interconnection becomes an ever more critical element and the company had 16.6GW of solar and 13.7GWh of storage interconnection points globally from the Q2CC:

In the past, this used to be a developer's ability to contract PPAs for feeds. However, with the growing deployment of incremental sources of electricity, a higher incidence of extreme climate events and geopolitical uncertainties, our ability to secure reliable interconnection points will be a key driver of our long-term success. As of Q2, we had 16.6 gigawatts of solar and 13.7 gigawatt hours of storage interconnection points globally. The pipeline expansion we are achieving give us significant runway for growth in the coming years and allow us to be more selective in developing the highest quality assets.

CapEx

CSIQ earnings deck

Management has plans for what can only be described as a dramatic capacity expansion, especially if one adds the plans to build its own polysilicon plant. The reasons for this are simple, demand is accelerating and management also sees an opportunity to win market share, here is their rationale ( Q2CC ):

We believe we are seeing a once in decade opportunity to gain global market share and further enhance our long-term defensive competitive advantage. To achieve that; great control over our technology, cost and supply chain is critical. This is why we made the strategic decision now to invest into polysilicon capacity as well. While we are still believing that polysilicon pricing will ultimately come down, we believe that directly control our supply chain is critical to our long-term competitiveness from a cost supply security and decarbonization standpoint.

The poly plant will be located in Qinghai Province, where 90% of electricity comes from renewable sources. Management expects 100% of their production facilities on renewable energy before 2030. It is a somewhat controversial step but management answered the case (Q2CC):

Now we have done almost two years of visibility study. And what we observed is that now, first of all, on the technology side, the Siemens method or the refined Siemens method to produce poly, that has become a standard. There are standard design institutes, for example, in China, which handles the factory design for almost everybody from the current poly-only makers to the newcomers. And there are also a handful of chemical production -- chemical manufacturing, engineering and EPC companies, who is specified in the subcontract work for certain part of poly. Therefore, the process, especially the granular process, is different. But for the Siemens process, the technology becomes standardized.

The CapEx is now at the same level per watt as solar cells, that is, it has come down in recent years.

While building the poly plant will only start next year, the company will spend $850M on CapEx this year, the bulk of it in H2 (as it spent $210M in H1). For those that worry about the high CapEx, management tried to allay these concerns (Q2CC):

so every $100 CapEx, we only need to take $30 from our bank account and the other $70 can be financed with the local banks. So the CapEx number, it sounds a big one. However, consider we have about $2 billion of cash, we still have enough capacity to fund our expansion excluding the polysilicon project.

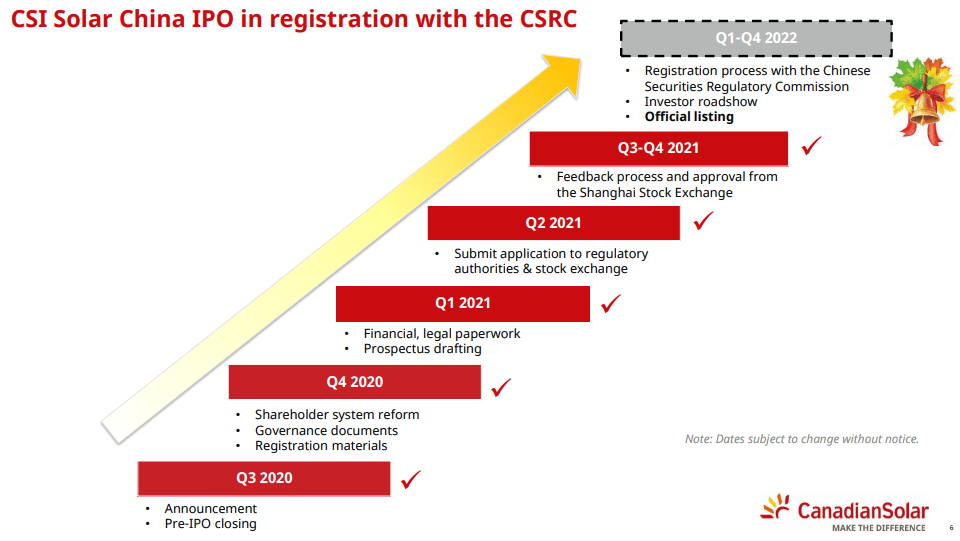

Next year with the poly plant this figure will rise quite a bit but the poly plant's financing depends on a successful IPO in China:

{kind=link}

The carve out IPO will result in a decrease in Canadian Solar's ownership in CSI Solar subsidiary from 80% to approximately 64%.

Financials

{kind=link}

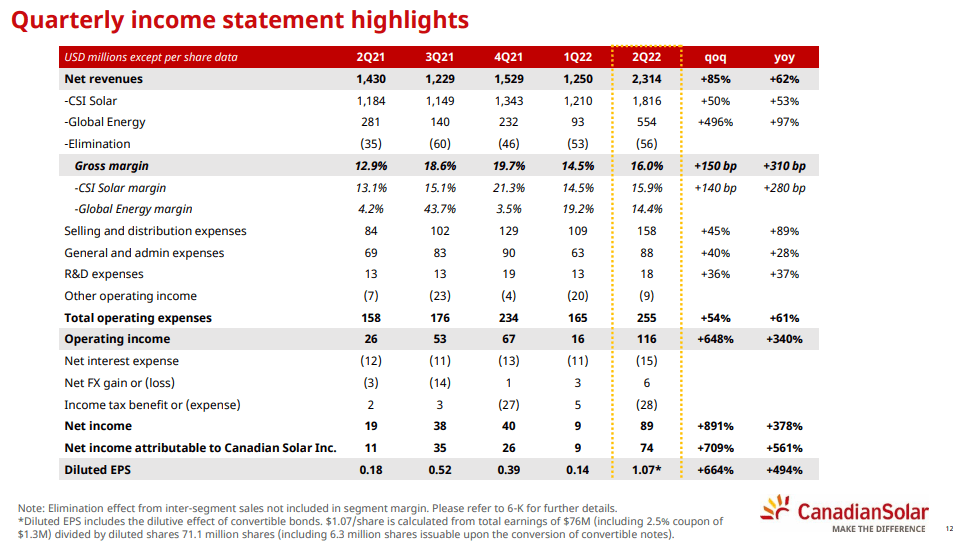

The CSI Solar segment revenue by 74% and gross profit by 161% y/y. The growth in the Global Energy segment (projects) was even more spectacular at 97% y/y and 496% q/q, selling 880MW in power projects for $554M in revenue producing a gross margin of 14.4%.

Quarterly revenue in this segment can be lumpy and the pace will slow down a little in H2. Here is a neat overview of the main factors of the CSI segment:

{kind=link}

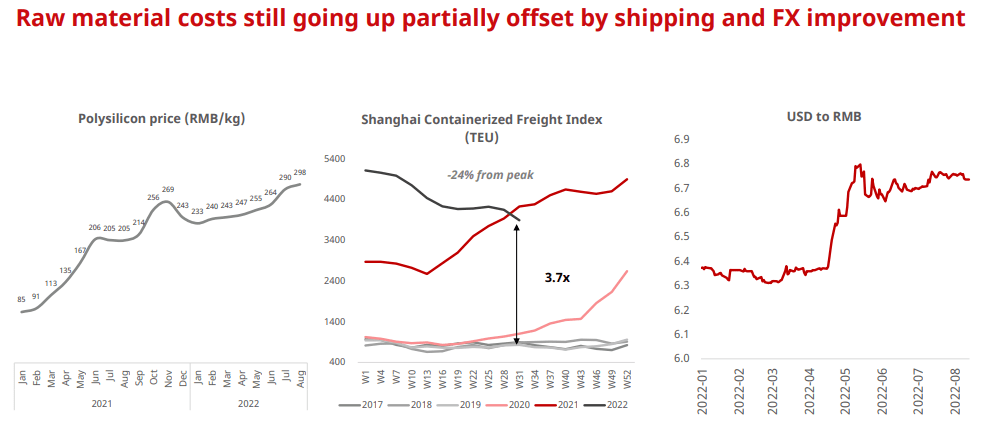

Logistic costs are starting to come down (but are still high historically), and the company is benefiting from forex developments (the fall in the Chinese renminbi against the US dollar), turning a headwind in the past two years into a tailwind.

{kind=link}

Poly prices are still rising, one reason the company wants to build its own plant, even if the rise isn't expected to continue in the medium term as new poly capacity is coming online.

Pricing, shipment cost and favorable forex developments are absorbing the poly cost increases.

In Q2 the company had run up its inventories which benefited Q2 results and these aren't going to be repeated in H2/22.

The company has $1.95B in cash ($895M of which is restricted) and $2.7B in debt and expects to have ownership of 370MW of solar projects by the end of the year.

Outlook

{kind=link}

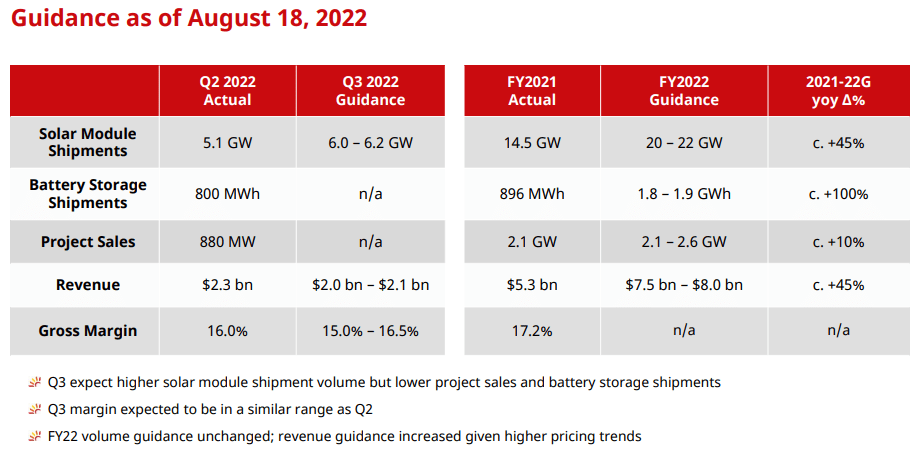

FY22 revenue (not volume) guidance was increased as prices and currencies are developing more favorable than earlier assumed. Earnings will take a bit of a hit from increased H2 CapEx though.

Risks

While there are undoubtedly secular tailwinds blowing in favor of both solar and energy storage and Canadian Solar is one of the top bankable names, they are also embarking on a large expansion path and we have to keep in mind that the industry is rather capital intensive.

So the first risk is funding, cautious investors might want to wait until there is more light on the proceeds of their CSI IPO in China to see what the remaining fund requirement is in a rising rate environment.

The solar sector is also notoriously cyclical and goes through bouts of overcapacity, falling prices and inventory write-downs (and even capacity destruction).

While Canadian Solar's track record and with the energy transition becoming ever more urgent and supported by policy should give investors a considerable degree of comfort, in our view, but these risks are not zero.

Cheap?

The share price has retrenched considerably since it published these stellar Q2 results as the second half results will be less exuberant due to a large increase in CapEx and less project income.

Valuation metrics in solar are notoriously low, which isn't all that surprising given the cyclical nature of the industry and the low gross margins. However, with its history of profitability, rapid expansion and an EPS estimated at $1.93 this year rising to $3.53 next year the valuation seems too low to us.

Conclusion

Solar energy is enjoying strong secular tailwinds and Canadian Solar is racing to expand capacity and building its own polysilicon plant to become less dependent on third party suppliers.

It's difficult to assess the billion dollar+ financing required for their 2023 CapEx including the poly plant without knowing more details of their Chinese spinoff IPO and the large CapEx requirements are a little more troubling in times of rising rates.

Not everybody is convinced the poly plant is a good idea but management claims that the technology is now standardized.

However, the company's history of profitability and the tailwinds blowing in the industry should give the investor a considerable degree of comfort and the prospect of rapidly rising production is pretty realistic.

While not without risk, we think that the recent retrenchment in the share price offers a pretty decent entry point in one of the big bankable solar companies which is embarking on a huge expansion.

The high CapEx needs will likely prevent any free cash flow from appearing the next 18 months at least, but the company that's coming out of the other end of this will be a much bigger beast.

Their ambition with the solar projects is also indicating huge expansion, especially in the area of O&M management.

Investors could benefit from the recent softness in the share price whilst those who want more certainty could wait for the results of the Chinese IPO of CSI, to be able to better assess their funding needs in a rising rate environment.

For further details see:

Canadian Solar Is Embarking On A Serious Expansion Path