CSIQ - Canadian Solar: Near-Term Risk Long-Term Upside

2023-11-28 23:03:21 ET

Summary

- EBITDA estimates for 2023 and 2024 have been downgraded due to lower sales and module prices.

- The company expects inventory de-stocking activities in Europe and in the US.

- Despite short-term risks, Canadian Solar is still undervalued and has the potential for market share growth. Even lowering our estimates, the company's valuation is cheap.

Today, we are back to comment on Canadian Solar's performance ( CSIQ ); however, this year, we already analyzed the company twice, commenting on the CSI Solar Co IPO process on the Shanghai Stock Exchange and also on the H1 results, looking at Canadian Solar's growth coupled with an underappreciated assets portfolio . After the Q3 results, we decided to dive deep into the financials and comment on the latest company news.

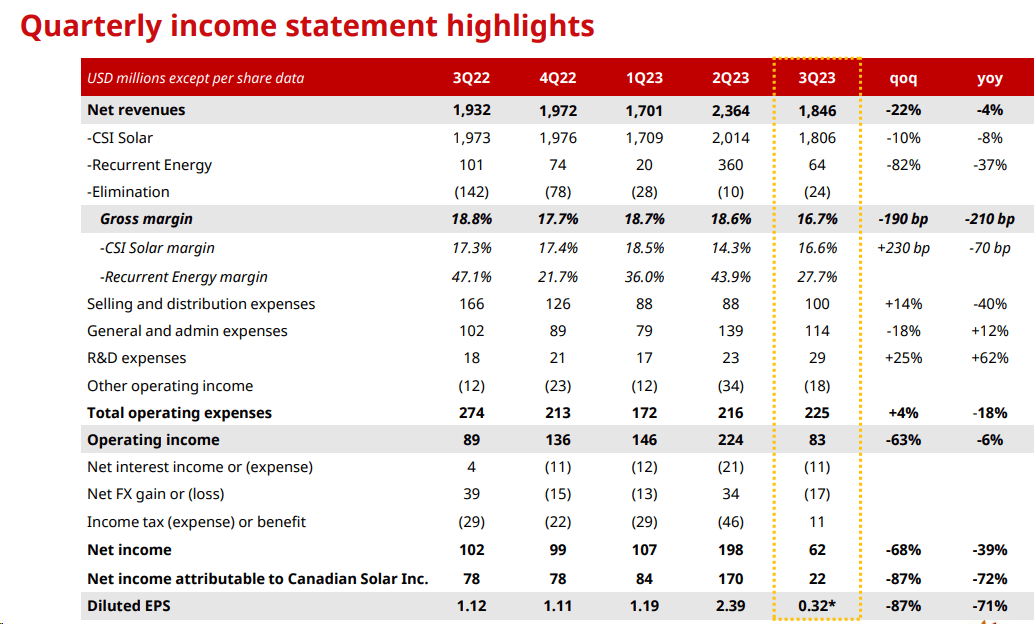

Firstly, Q3 results were disappointing and came below our expectations. The company delivered top-line sales of $1.84 billion compared to our internal numbers of $1.95 billion, and more importantly, the company's gross margin was also at 16.7%, below our estimates (18.4%). Despite that (once again), the company had a $35 million inventory write-down of DG modules, and if we excluded this negative one-off, the quarterly gross margin would have reached 18.5%. Lower sales were achieved due to lower project sales and lower module ASPs. Looking at the divisional level, the CSI Solar segment gross margin was 16.6%, up from 14.3% achieved in Q2, while the Recurrent Energy segment gross margin was sequentially down due to a tough comp in Q2. In numbers, the division was down from 43.9% to 27.7%. Going down to the P&L analysis and cross-checking Wall Street consensus estimates, Canadian Solar's diluted EPS reached $0.32 and was below expectations, which, on average, was forecasting $0.78 (Fig 1).

{kind=link}

Canadian Solar Q3 Financials in a Snap

Source: Canadian Solar Q3 results presentation - Fig 1

Changes in Estimates

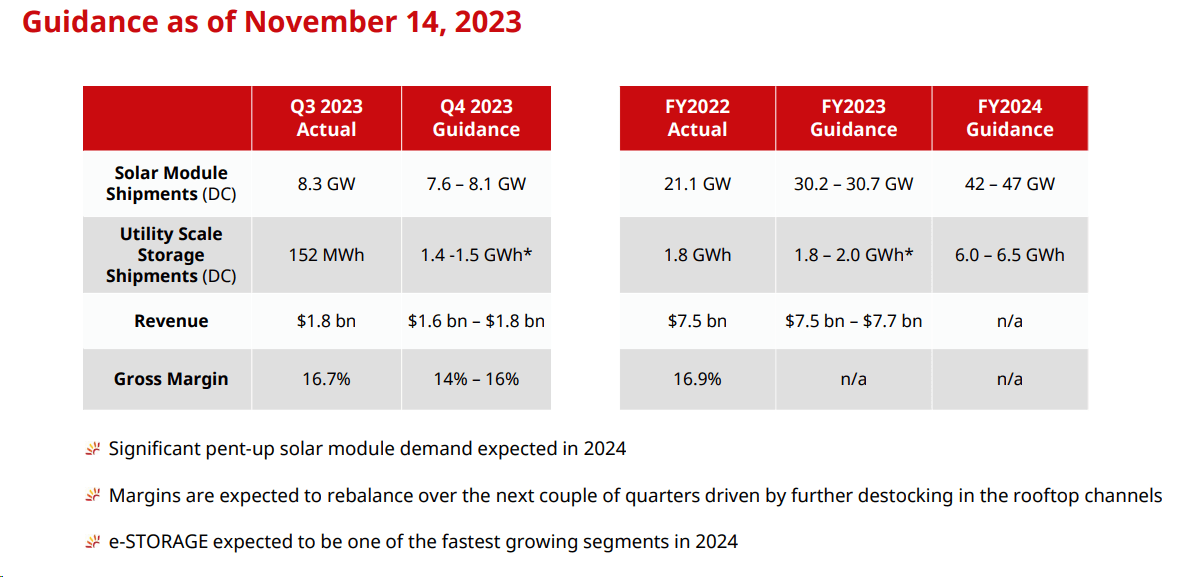

Our previous publication forecasted an EBITDA value of $1 billion in 2023 and $1.3 billion in 2024. Post Q3 results and aligning the company's outlook released in mid-November, we are now downgrading our EBITDA estimates to $825 million in 2023 and $1.1 billion in 2024. This implied a Q4 EBITDA of $132 million. Q4 guidance was well below expectations, with a gross margin forecast in the 14%-16% range backed on sales from $1.6 to $1.8 billion. Our previous estimates forecast $2.6 billion in sales with a gross margin of 18.9% (below Wall Street at 19.1%). The company forecasts Q4 energy storage shipments of 1.4-1.5 GWh and module shipments of 7.6-8.1 GWh (Fig 2).

{kind=link}

Canadian Solar Q4 Outlook and 2024 FY update

Fig 2

Still a Buy with near-term risk to consider

In a nutshell, we can say that Q3 was a miss. We expect a weak Q4, but we are still optimistic for 2024.

- On a quarter-to-quarter basis, the solar backlog was down by 3%, but on a yearly basis, the pipeline moved up by 6% to an impressive backlog of 26.5 GW;

- During the Q&A call, the CEO highlighted the strong demand elasticity vs. the module prices. Management's view for a 2024 shipment growth of 50% may be optimistic. We do not see the US module demand up 50% in our forecasted numbers. The EMEA and North America regions represent nearly 50% of the company's geographic shipment mix, and our check with the distributor suggests module growth of approximately 30%. In addition, Canadian Solar expects channel inventory in Europe and the US over the next 3/6 months. For the above reason, we are lowering our EBITDA estimates accordingly;

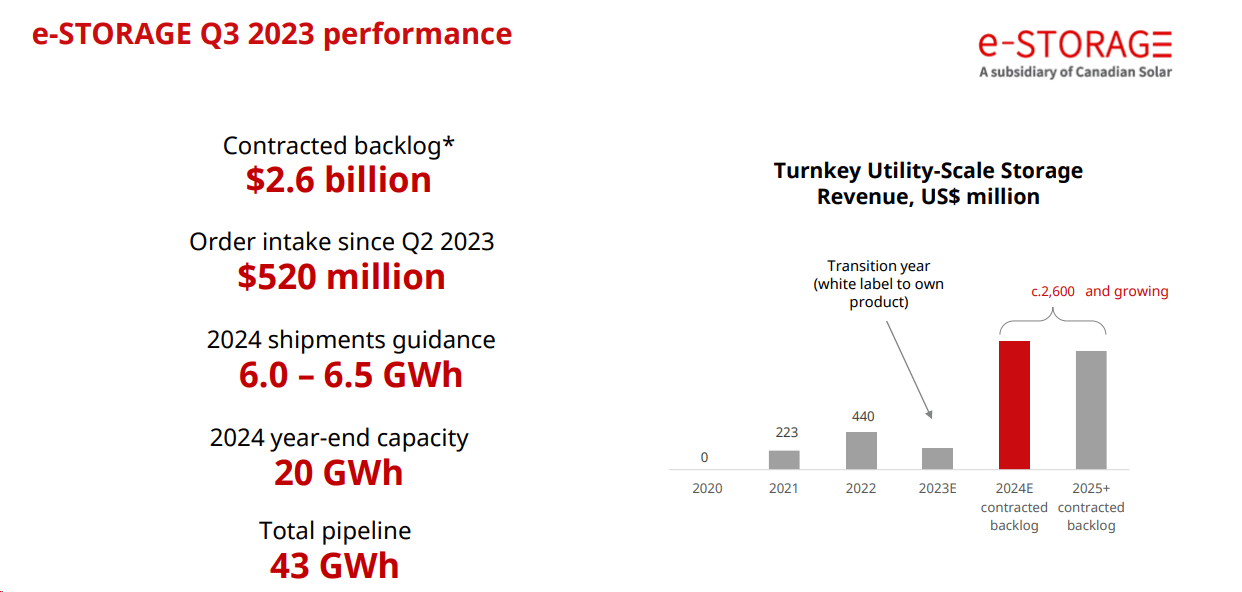

- The battery storage pipeline reached approximately 55GWh in Q3 and includes 12GWh of battery storage interconnections. Canadian Solar expects about half of the backlog, which is equivalent to 6-6.5GWh, to be delivered in 2024 (Fig 3);

- Here at the Lab, we are also priced in additional risk from developers. These risks are not leaning only toward the supply chain but also a higher-than-expected interest rate environment. Despite that, we are confident that Canadian Solar will likely continue to gain market share, but we also believe short-term risk-reward is now more unfavorable until macroeconomic data improves;

- The company's recent disclosure of a UFLPA detainment is critical to report. Although our internal team is not modeling any material impact, the company might need help selling in the ASPUS market.

{kind=link}

Fig 3

Conclusion and Valuation

Looking at the CSI Solar Co stock price performance , Canadian Solar's equity stake is valued at approximately $4 billion. As a reminder, Canadian Solar owns "approximately 64% of CSI Solar Co, assuming the over-allotment option is not exercised, or approximately 62% of CSI Solar Co, assuming that the over-allotment option is exercised in full. " Even if the company has a total net debt of $1.4 billion, Canadian Solar is paying a quarterly interest rate of approximately $15 million. This is because the company debt is linked to Utility Scale development and will be removed when the project is sold. Even if we are downgrading the company's financials, Canadian Solar is still highly undervalued and trades at a 2024 EV/EBITDA lower than 3x. Even if we price a significant decline in global module ASPs, we should also consider a solar industry channel inventory over the coming quarters. In addition, even factoring in the Q3 results and a weaker-than-anticipated Q4 has a low P/E despite being a growth company. As a result, on a standalone basis, post Q3 results, we decreased our 2024 core EPS estimate to $3.85, and for the above reason, we lowered our target price to $30.8 per share from a previous valuation of $44 per share. We still believe that Wall Street analysts " should switch to a different valuation methodology given the CSI carve-out with a listing in June 2023." Near-term risk-reward seems less favorable. Downside risks include higher production capacity, lower government subsidies, and higher tariffs on Chinese panels imported into the EU, the US, and Canada.

For further details see:

Canadian Solar: Near-Term Risk, Long-Term Upside