CSIQ - Canadian Solar: Panel Manufacturers Not Likely To Be Good Long-Term Compounders

2023-09-25 08:21:53 ET

Summary

- Canadian Solar is an international producer of solar ingots, wafers, cells, modules, and other solar power.

- A recent decline in the price of polysilicon caused a contraction in gross margins in this most recent quarter. Long-term, the price of solar panels continues to drop.

- Canadian Solar appears to be a fairly healthy company stuck in a lackluster industry, so they struggle to produce attractive returns.

- After reviewing their financial situation and valuation, I currently rate CSIQ as a Hold.

Thesis

With the Inflation Reduction Act providing sustained financial incentives to transition to renewable sources of energy, and the aggregate cost of photovoltaics now lower than all other forms of energy, I find myself looking for potential investments in solar. Because the cost of panels has gone down so much, I now view photovoltaic panels as mostly fungible commodities.

This commoditization phase of a good leaves most producers in a place where they are saddled with ever worsening gross margins. The sellers of commoditized products often struggle to upsell their customers by producing a value-added experience. This has left me with the conclusion that I should be limiting my focus to solar panel ancillaries instead of producers.

However, Canadian Solar Inc. ( CSIQ ) has caught my attention because they have managed to achieve reasonable margins and returns at times in the past. As the industry continues to mature, they may even be able to find ways to improve their profitability. After looking over their financials and valuation, I currently rate Canadian Solar as a Hold.

Company Background

Canadian Solar is an international producer of solar ingots, wafers, cells, modules, and other solar power and battery storage products. They were incorporated in 2001 and are currently based in Guelph, Canada. The company operates in two segments: Canadian Solar Inc. Solar and Global Energy.

The CSI Solar segment offers standard solar modules and battery storage solutions, as well as solar system kits that are a ready-to-install packages comprising of inverters, racking systems, and other accessories; and engineering, procurement, and construction services."

The Global Energy segment engages in the development, construction, maintenance, and sale of solar and battery storage projects; operation of solar power plants; and sale of electricity. This segment also provides operation and maintenance (O&M) services, including monitoring, inspections, repair, and replacement of plant equipment; and site management and administrative support services for solar projects, as well as asset management services."

Long-Term Trends

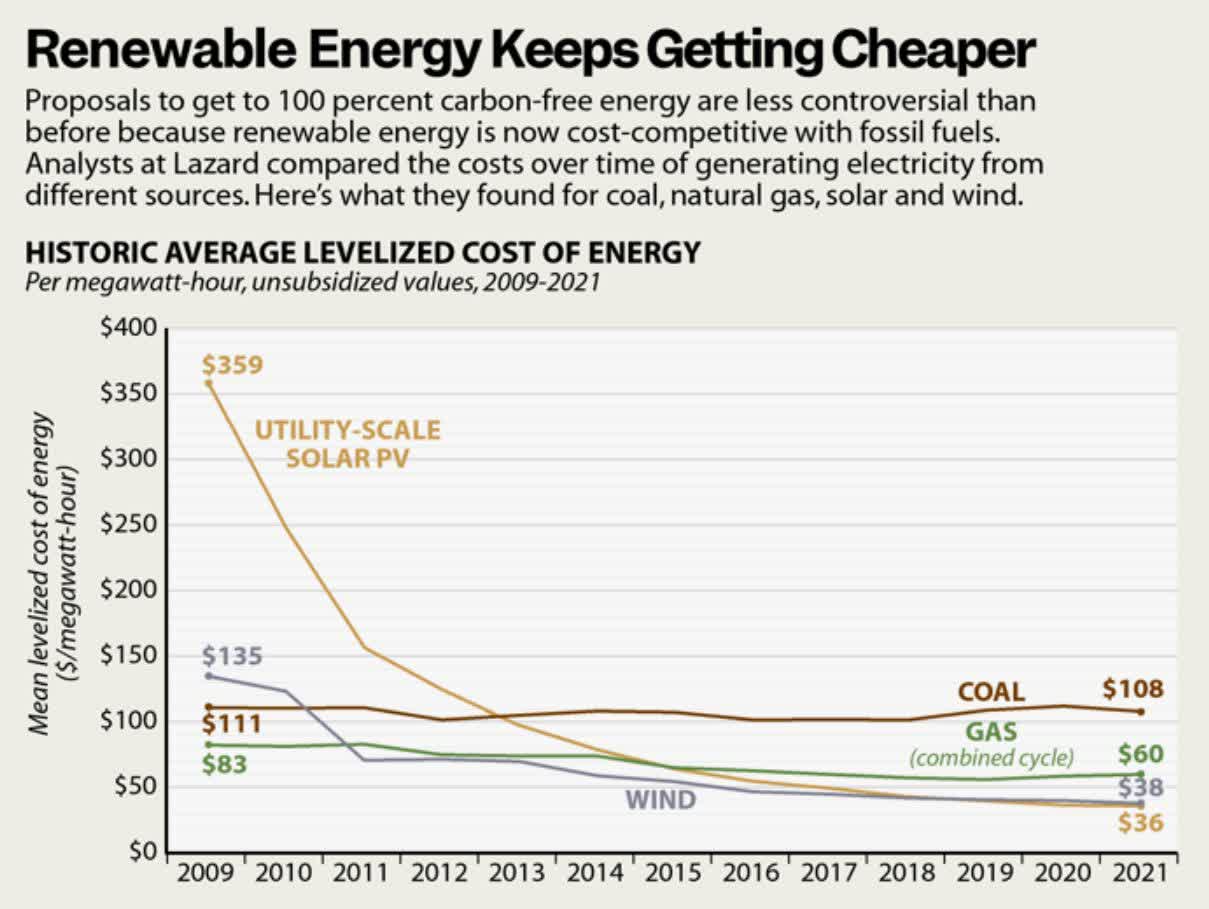

In the United States, the solar energy market is expected to have a CAGR of 16.48% through 2028. Globally, the solar panel market is expected to have CAGR of 18% until 2030. Much of this is being driven by the fact that the levelized cost of photovoltaics has fallen below all other energy sources.

Levelized Cost Of Energy (Lazard, Dan Gearino, Insideclimatenews.org)

{kind=link}

Guidance

Their most recent earnings call transcript revealed that prices fell dramatically in the second quarter after it was revealed the company experienced a margin contraction.

{kind=link}

CSIQ Guidance (Q2 2023 Earnings Call Transcript)

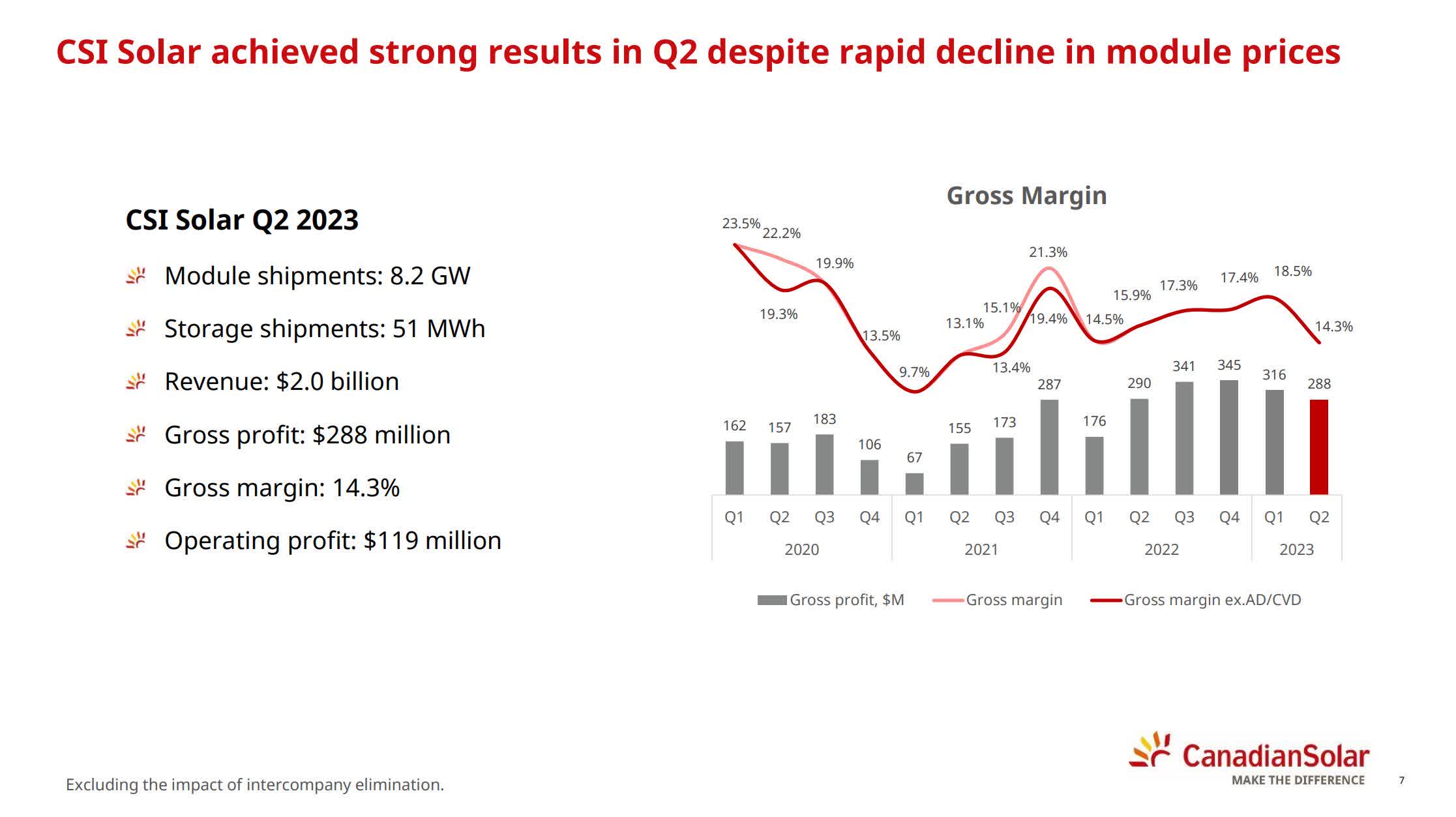

Here we can see why the share price fell after the last quarterly report.

{kind=link}

CSIQ Rapid Decline In Module Prices (Q2 2023 Investor Presentation, Page 7)

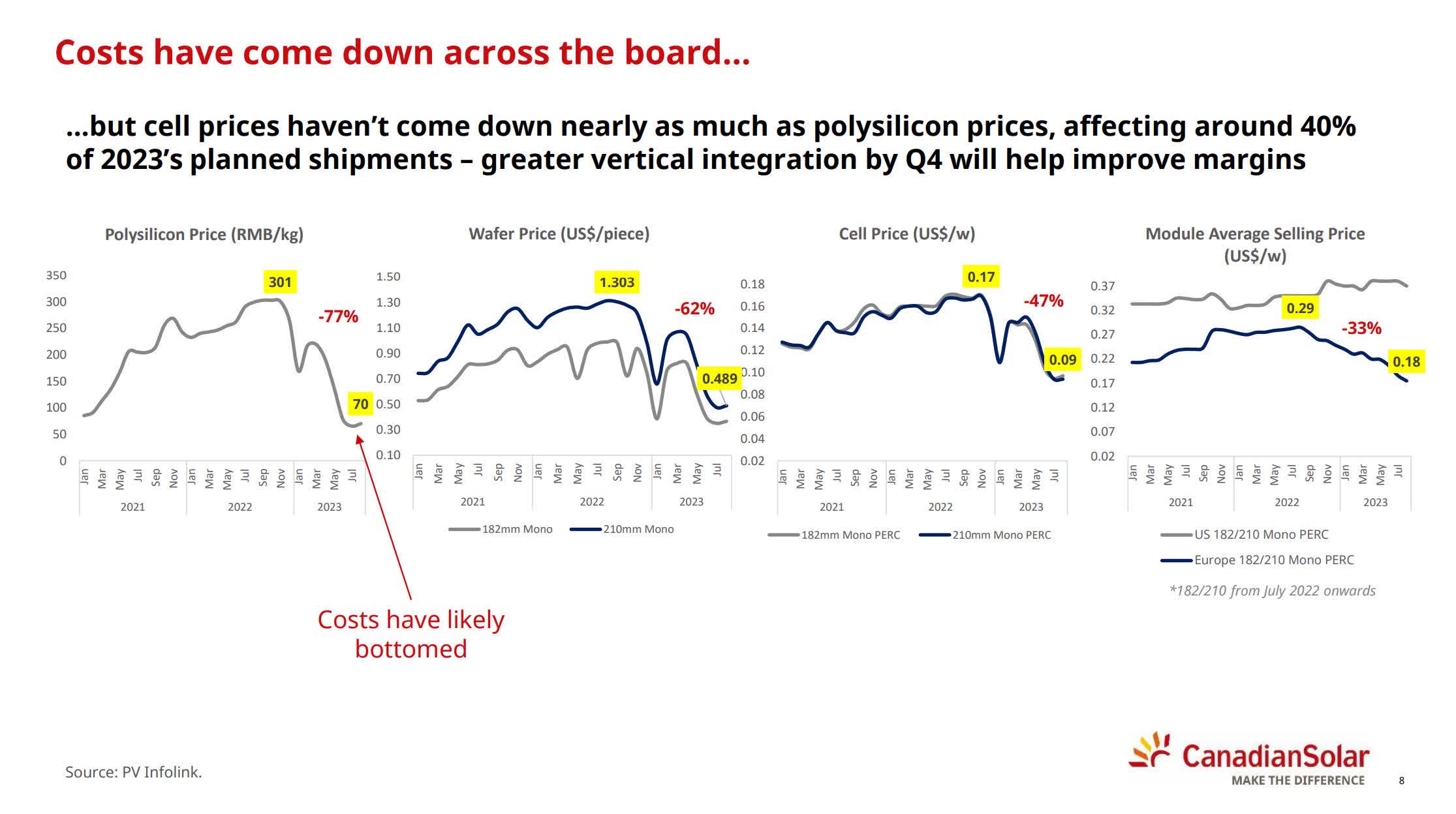

The good news here is that cell prices have not fallen as much as polysilicon. Although they are experiencing a significant gross margin contraction from the drop in the price of polysilicon, this expansion between the difference in cost and price should work toward improving the rest of their profitability metrics on a relative basis. Meaning, they are taking in less revenue under the new environment, but the revenue they do bring in has slightly better margins. With the company still stuck with many inelastic costs, I believe this is what caused the significant decline in valuation after this earnings report.

{kind=link}

CSIQ Decline In Costs (Q2 2023 Investor Presentation, Page 9)

Annual Financials

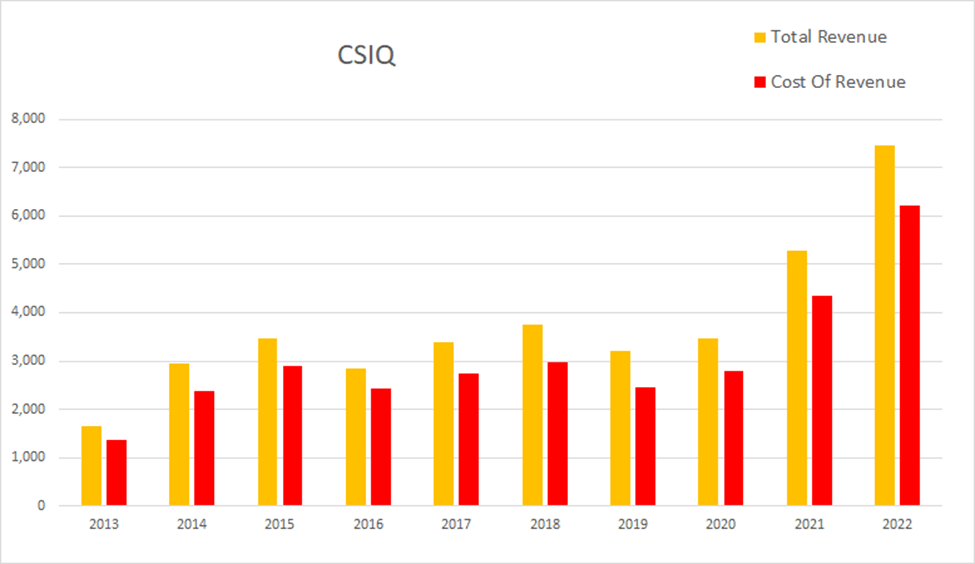

Canadian Solar has been growing revenue significantly over the last decade. I believe the extremely low cost of solar is going to continue providing sustained demand for the industry. In 2013 they had an annual revenue of $1,654.4M. By 2022 that had grown to $7,468.6M. This represents a total rise of 351.44% at an average annual rate of 39.05%.

{kind=link}

CSIQ Annual Revenue (By Author)

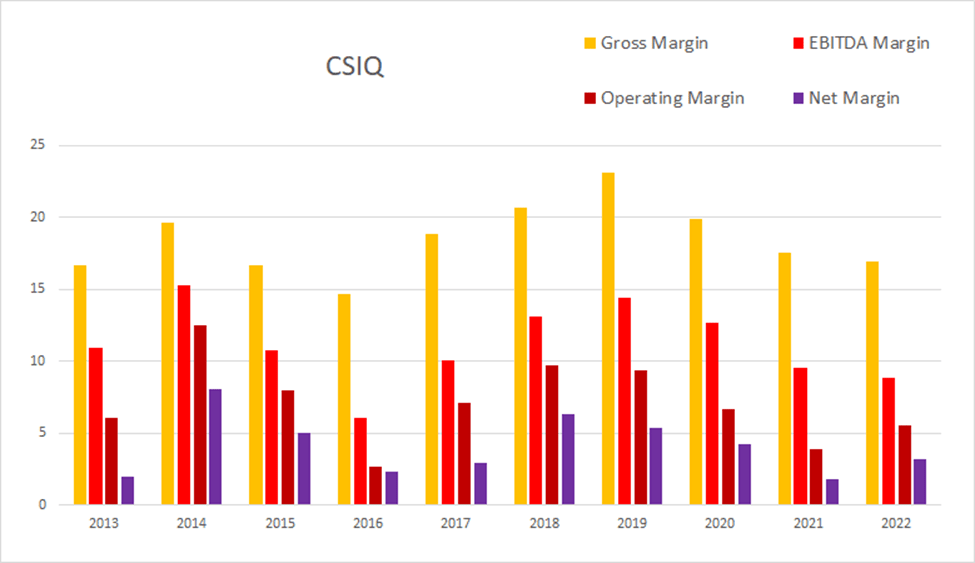

Their margins are consistently positive and occasionally become attractive. As of the most recent annual report, gross margins were 16.93%, EBITDA margins were 8.83%, operating margins were 5.54%, and net margins were 3.21%.

{kind=link}

CSIQ Annual Margins (By Author)

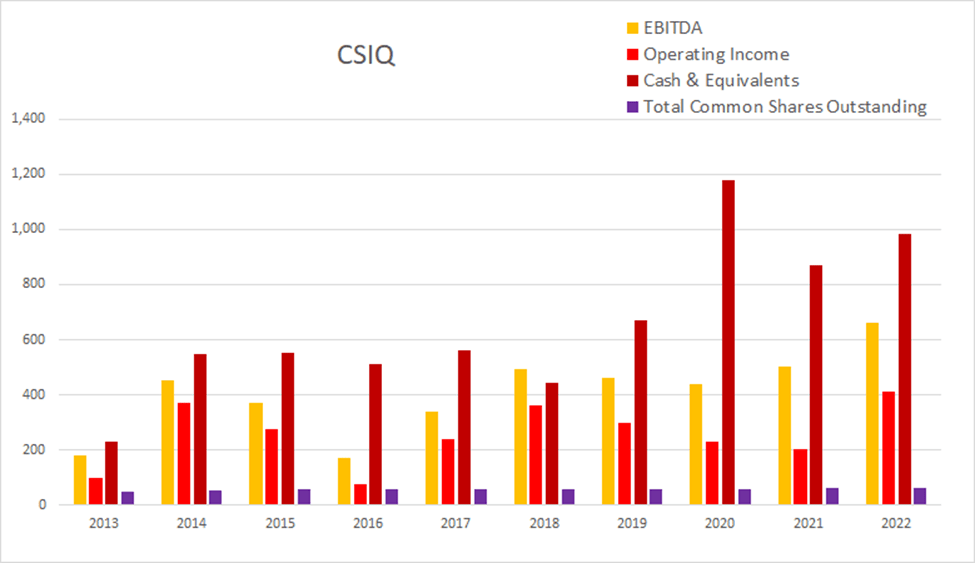

Although their share count has been rising over the last decade, their income growth has outpaced it. When a company can effectively convert dilution into future income, it can be seen as accretive instead of toxic. Total common shares outstanding was at 51M in 2013. By the end of 2022 that had risen to 64.5M. This represents a 26.47% increase in share count, which comes out to an average annual rate of 2.94%. Over that same time period operating income rose from $99.3M to $413.8M, a 316.7% total increase, at an average rate of 35.19%.

{kind=link}

CSIQ Annual Share Count vs. Cash vs. Income (By Author)

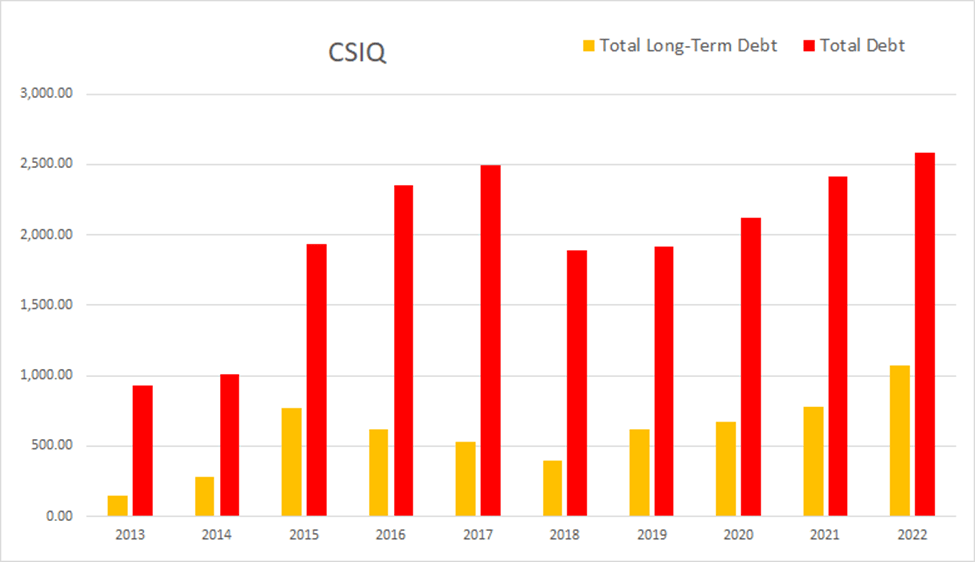

Their debt situation appears to be quite manageable. As of the 2022 annual report, they only had -$32.8M in net interest expense, total debt was $2,579.4M, and long-term debt was $1,071M.

{kind=link}

CSIQ Annual Debt (By Author)

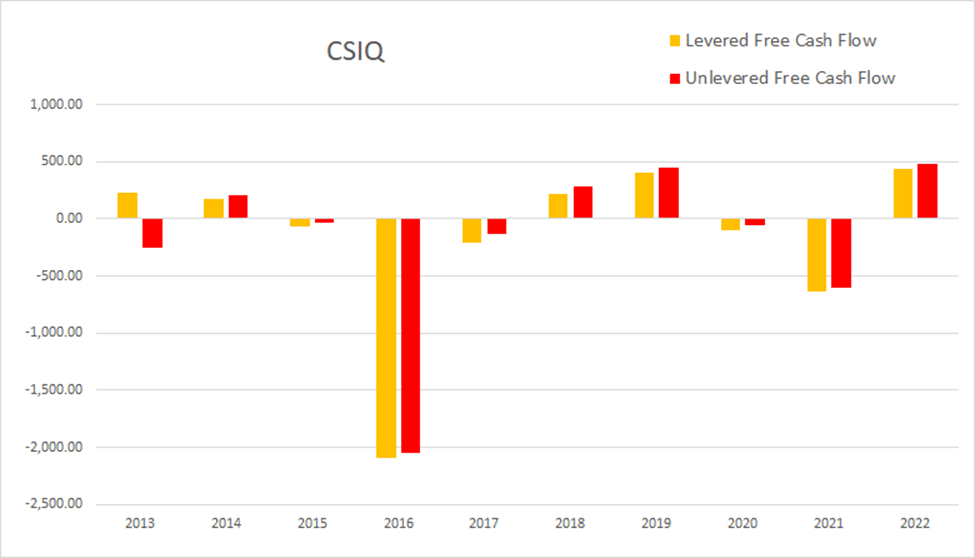

While their margins have been consistently positive, their cash flow has not. As of this most recent annual report, cash and equivalents ware $981.4M, operating income was $413.8M, EBITDA was $659.8M, net income was $240M, unlevered free cash flow was $480.2M, and levered free cash flow was $435.1M.

{kind=link}

CSIQ Annual Cash Flow (By Author)

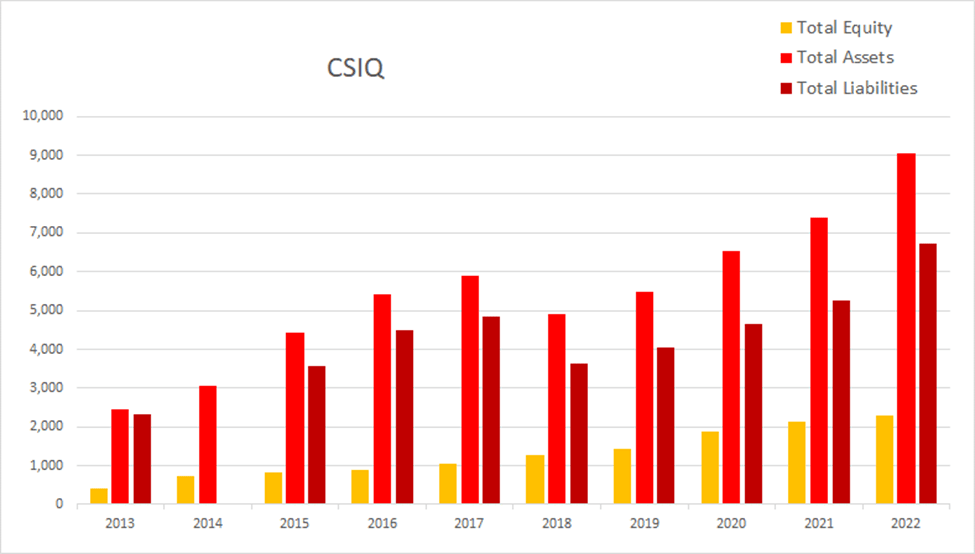

Their total equity has been steadily rising.

{kind=link}

CSIQ Annual Total Equity (By Author)

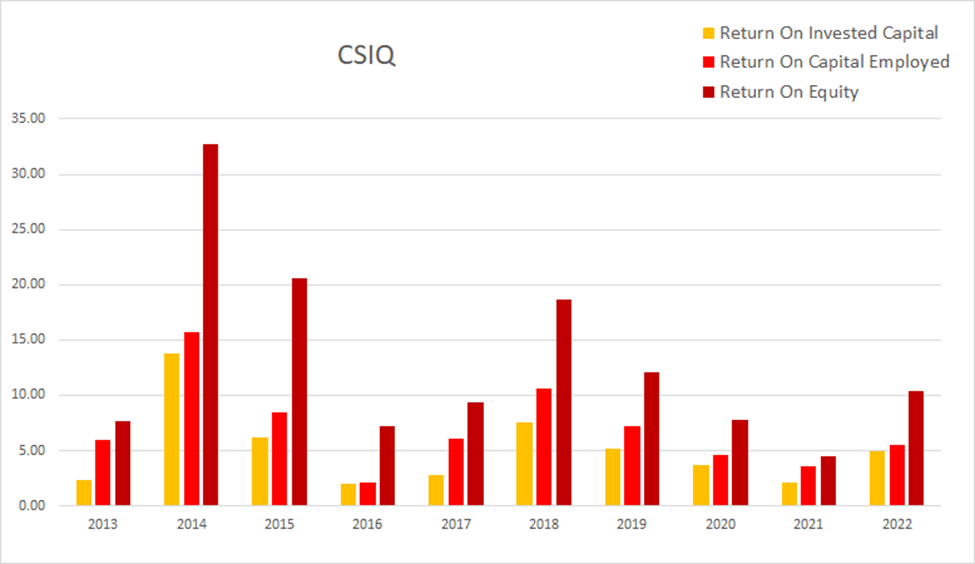

Their returns have been attractive at times in the past, but vary significantly from year to year. As of the most recent annual report ROIC was 4.91%, ROCE was 5.50%, and ROE was at 10.40%.

{kind=link}

CSIQ Annual Returns (By Author)

Quarterly Financials

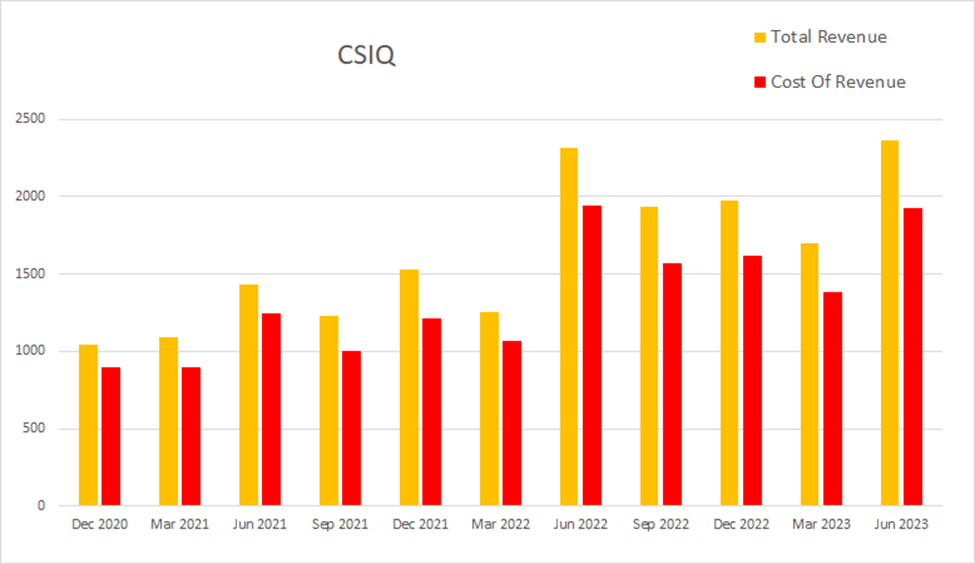

Their quarterly financials are showing a significant rise in demand. I believe much of this is due to the effects of the low cost of solar combined with the subsidies provided by the Inflation Reduction Act. Eight quarters ago Canadian Solar had a quarterly revenue of $1,429.7M. Four quarters ago that had risen to $2,314.2M. By this most recent quarter that had reached $2,364M. This represents a total two-year increase of 65.35% at an average quarterly rate of 8.17%.

{kind=link}

CSIQ Quarterly Revenue (By Author)

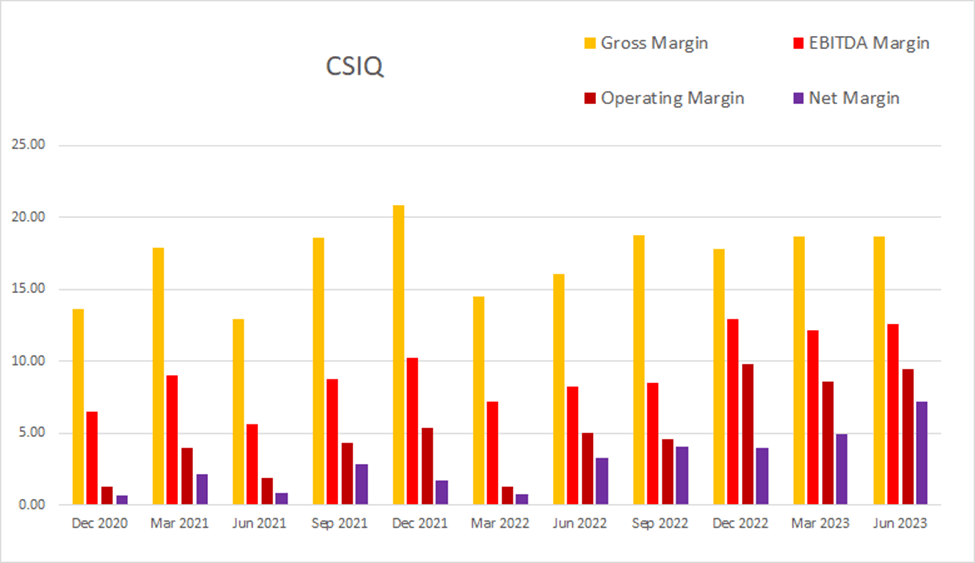

The earnings call transcript referenced gross margins of 14.3%. This value includes write downs and adjustments made to reflect the new pricing situation. However, merely dividing their gross profit by their total revenue produces a gross margin of 18.64%. EBITDA margins were 12.57%, operating margins were 9.48%, and net margins were at 7.19%.

{kind=link}

CSIQ Quarterly Margins (By Author)

Their dilution rate appears to have dropped. The sum of their last eight quarters of dilution comes to 7.46%; the sum of the last four quarters is 0.93%.

{kind=link}

CSIQ Quarterly Share Count vs. Cash vs. Income (By Author)

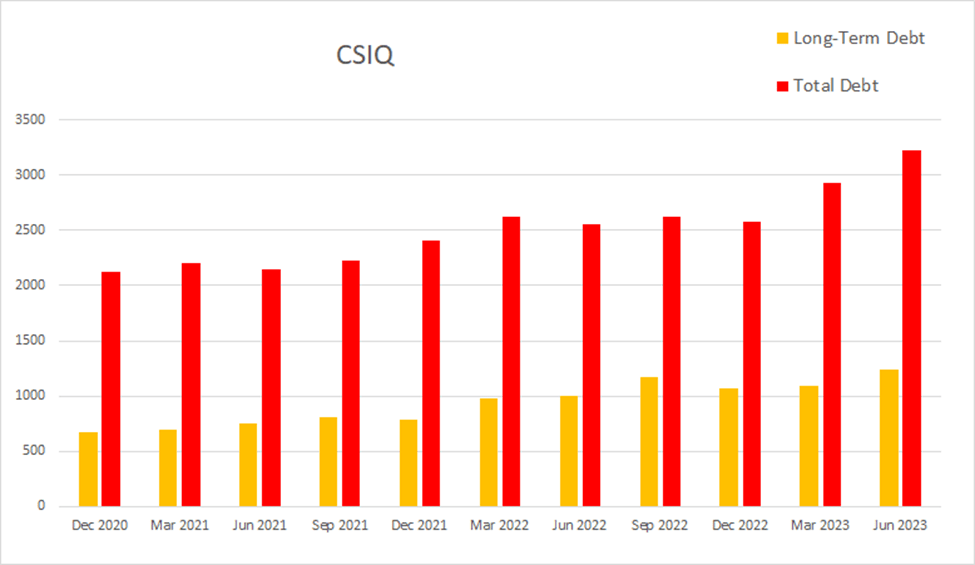

This most recent quarter, Canadian Solar had -$19M in net interest expense, total debt was at $3226.3M, and long-term debt was at $1240.8M.

{kind=link}

CSIQ Quarterly Debt (By Author)

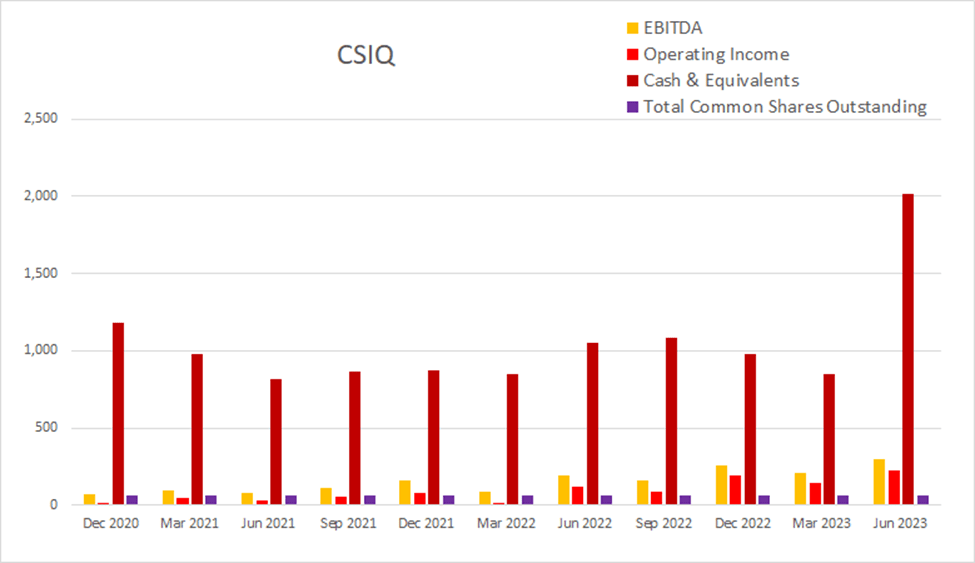

As of the most recent earnings report, cash and equivalents were $2,011M, quarterly operating income was $224M, EBITDA was $297.1M, net income was $170M, unlevered free cash flow was $163.2M, and levered free cash flow was $182.3M. Seeking Alpha has no data for most of their quarterly cash flow statements, so I did not produce a cash flow chart.

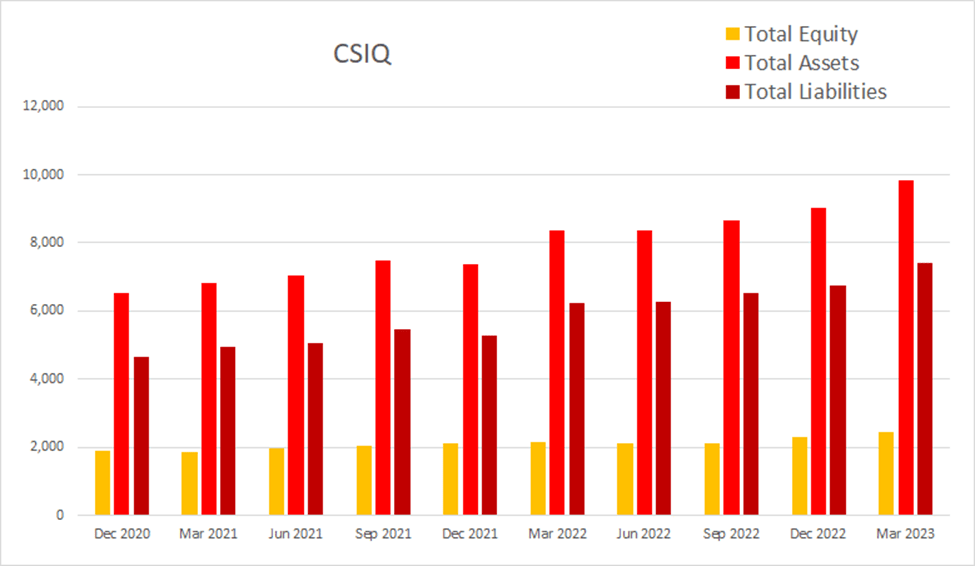

Total equity continues to slowly rise.

{kind=link}

CSIQ Quarterly Total Equity (By Author)

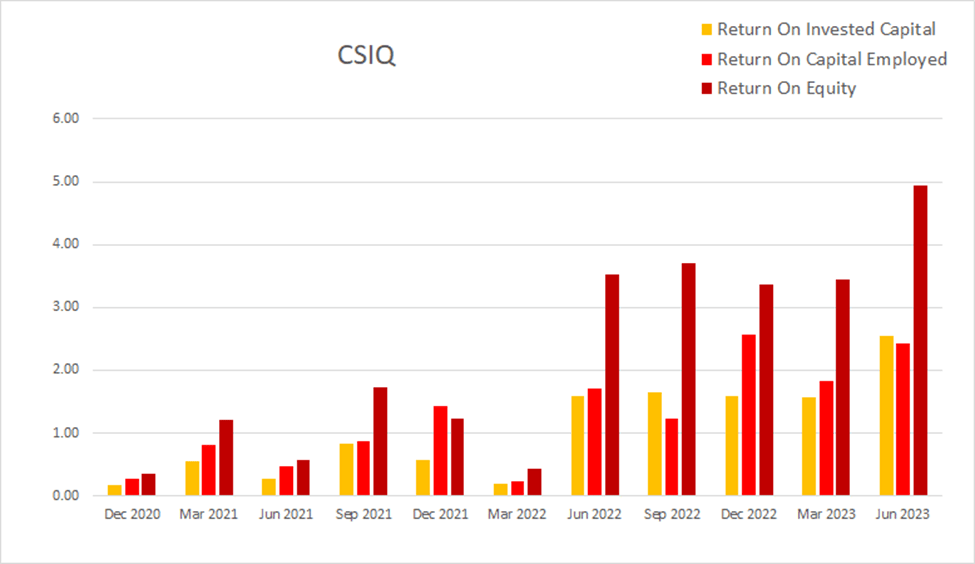

Their quarterly returns have been unsteadily growing since the end of 2020. As of the most recent earnings report ROIC was 2.55%, ROCE was 2.43%, and ROE was 4.94%.

{kind=link}

CSIQ Quarterly Total Equity (By Author)

Valuation

As of September 22nd, 2023, Canadian Solar had a market capitalization of $1.69B and traded for $25.81 per share. They do not pay a dividend, so using their forward P/E of 4.55x, and their EPS Long-Term CAGR of 26.50%, I calculated a PEGY of 0.1717x and an Inverted PEGY of 5.824x. As the PEGY value is significantly below 1x, it implies CSIQ is significantly undervalued.

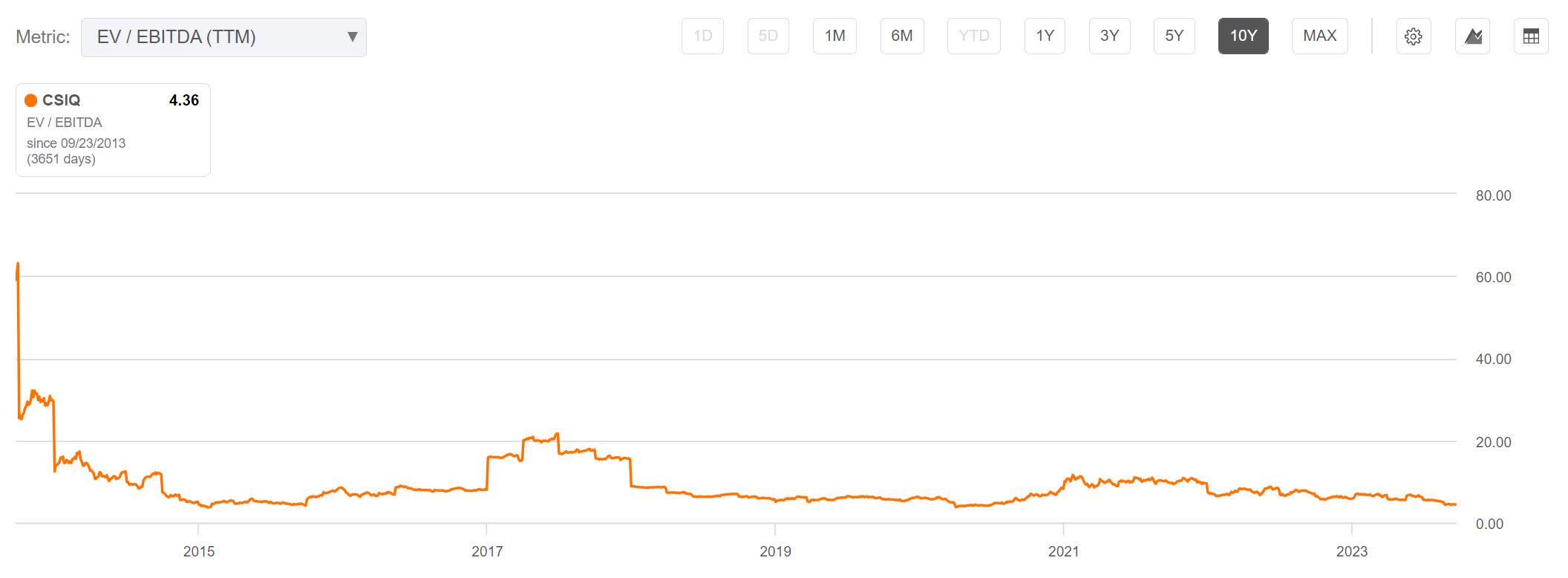

As undervalued as it appears to be right now, CSIQ has a history of falling into valuation troughs. The lowest of these troughs has both P/E and EV/EBITDA values down in the high 3x's. P/E is currently at 4.44x, and EV/EBITDA is currently at 4.36x. I do not believe this is the floor of the current trough.

{kind=link}

CSIQ 10-Year P/E (Seeking Alpha)

{kind=link}

CSIQ 10-Year EV/EBITDA (Seeking Alpha)

Risks

Canadian Solar exists in an industry where competition and subsidies are forcing commoditization. The entire industry is under stress from this margin contraction, and I have to believe the cost of panels will continue dropping. If this company were unable to continue finding profits through ever tightening gross margins, it may eventually lose its operational viability.

The photovoltaic panel industry may eventually enter periods of strong demand cyclicality, which would produce significant inventory gluts and margin declines for producers.

Catalysts

The company may eventually find a way to bring its cost of production down more quickly than its competitors. If it were able to more effectively stay out ahead of the slowly dropping prices, it could outlast most of them. All of the producers have to pay for the same materials, so this may be more a matter of keeping administration costs as low as possible.

The same periods of cyclicality cited in the risks should also produce attractive buying opportunities if one invests into the producers when the glut and inventory problems are at their worst. As they clear up, margins should expand and then valuations should react accordingly.

Conclusions

Overall, Canadian Solar appears to be a fairly healthy company stuck in a lackluster industry. Even though it is trading at a very low valuation, I don't buy things merely because they are cheap. Even if CSIQ never becomes worth investing in as a long-term compounder, it may be worth buying after sector-wide decline as a recovery play. I believe it is worth keeping an eye on long-term.

For further details see:

Canadian Solar: Panel Manufacturers Not Likely To Be Good Long-Term Compounders