CSIQ - Canadian Solar Q2 Earnings: Selloff Overdone Stock Attractively Priced

2023-08-23 08:33:51 ET

Summary

- Canadian Solar's post-earnings selloff is overdone.

- The company reported a strong quarter with increased revenues and EPS but provided disappointing forward guidance.

- The company is diversifying into energy storage solutions, which helps to reduce their exposure to volatile solar economics and positions the company for future growth.

- CSIQ stock is trading at a low PE and below their book value. We believe Canadian Solar stock is attractively priced at these levels.

Thesis

The post-earnings selloff in Canadian Solar (CSIQ) appears to be overdone. The company is diversifying their business into energy storage solutions, reducing the business risk and positioning themselves for future growth. The stock is trading at a bargain valuation and we believe it is undervalued, though it may take some time for the company to gain respect from the market.

Canadian Solar Q2 Earnings Results

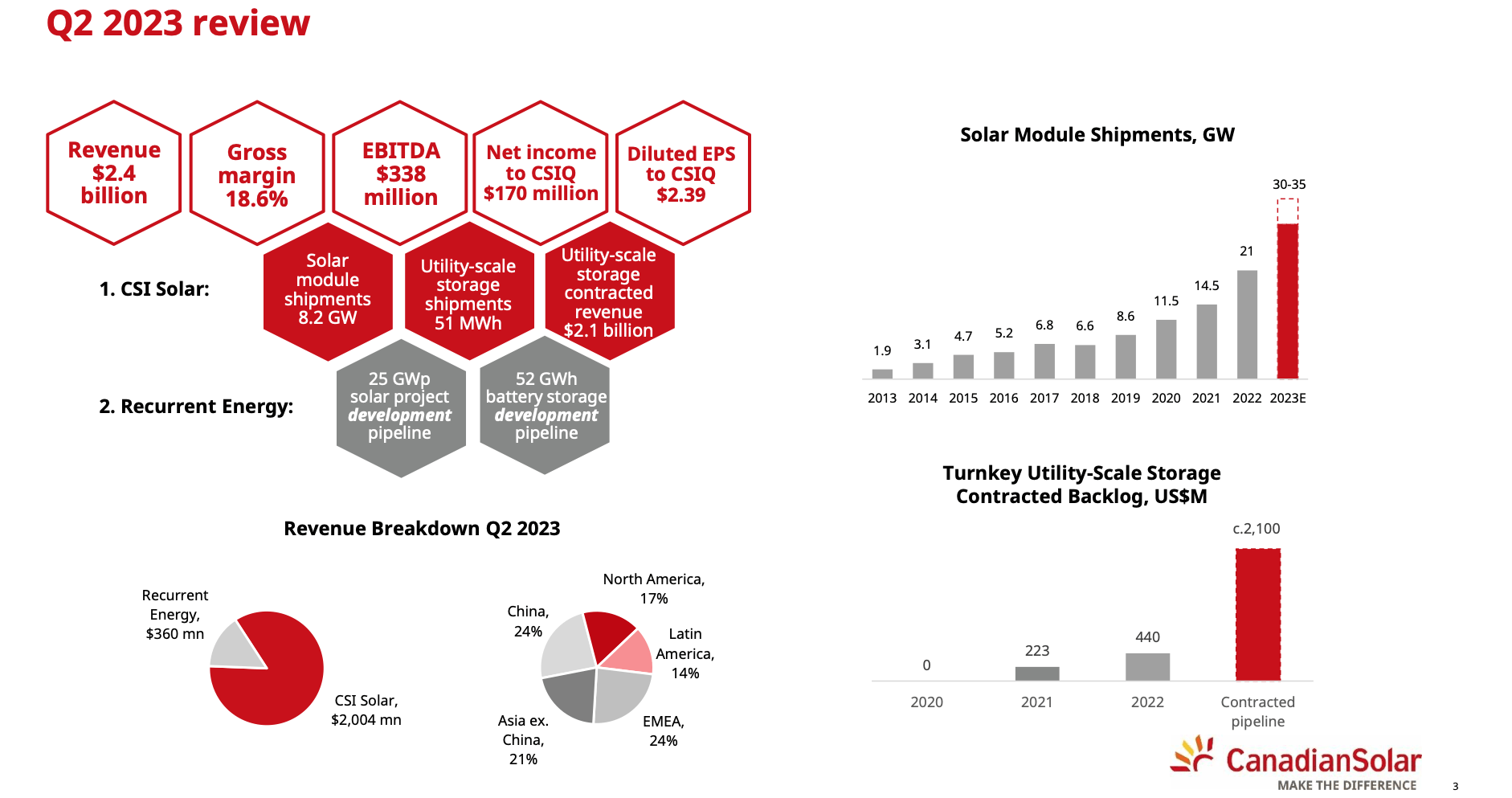

Canadian Solar reported a stellar quarter that saw a 39% increase in net revenues quarter-over-quarter and EPS of $2.39 per diluted share compared to EPS of $1.19 per diluted share in the first quarter of 2023 and EPS of $1.07 per diluted share in the second quarter of 2022. The company continues to execute flawlessly and is diversifying their business into energy storage. This will help to reduce the risk in the stock and serve as a growth driver going forward.

Canadian Solar Q2 Earnings Presentation

{kind=link}

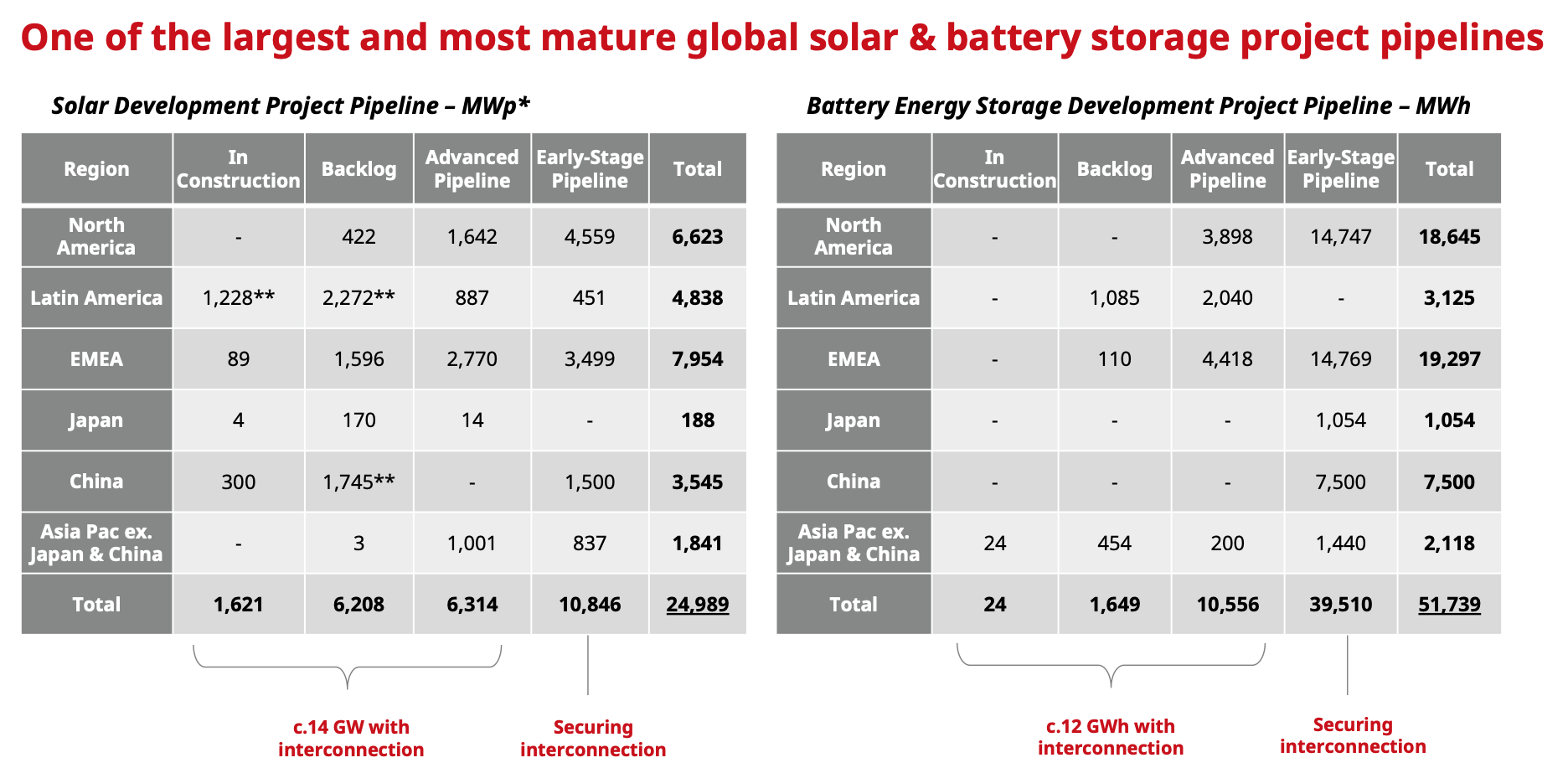

The company's large backlog provides revenue visibility and further de-risks the stock. Of particular importance is the growth in the battery and energy storage pipeline. Investors should continue to monitor this segment going forward and see if the backlog continues to increase as projects enter the construction phase. If this is the case, Canadian Solar will be on the road to successfully diversifying their business and positioning themselves for further growth, even if solar panel ASPs decline and input costs rise.

Canadian Solar Q2 Earnings Presentation

{kind=link}

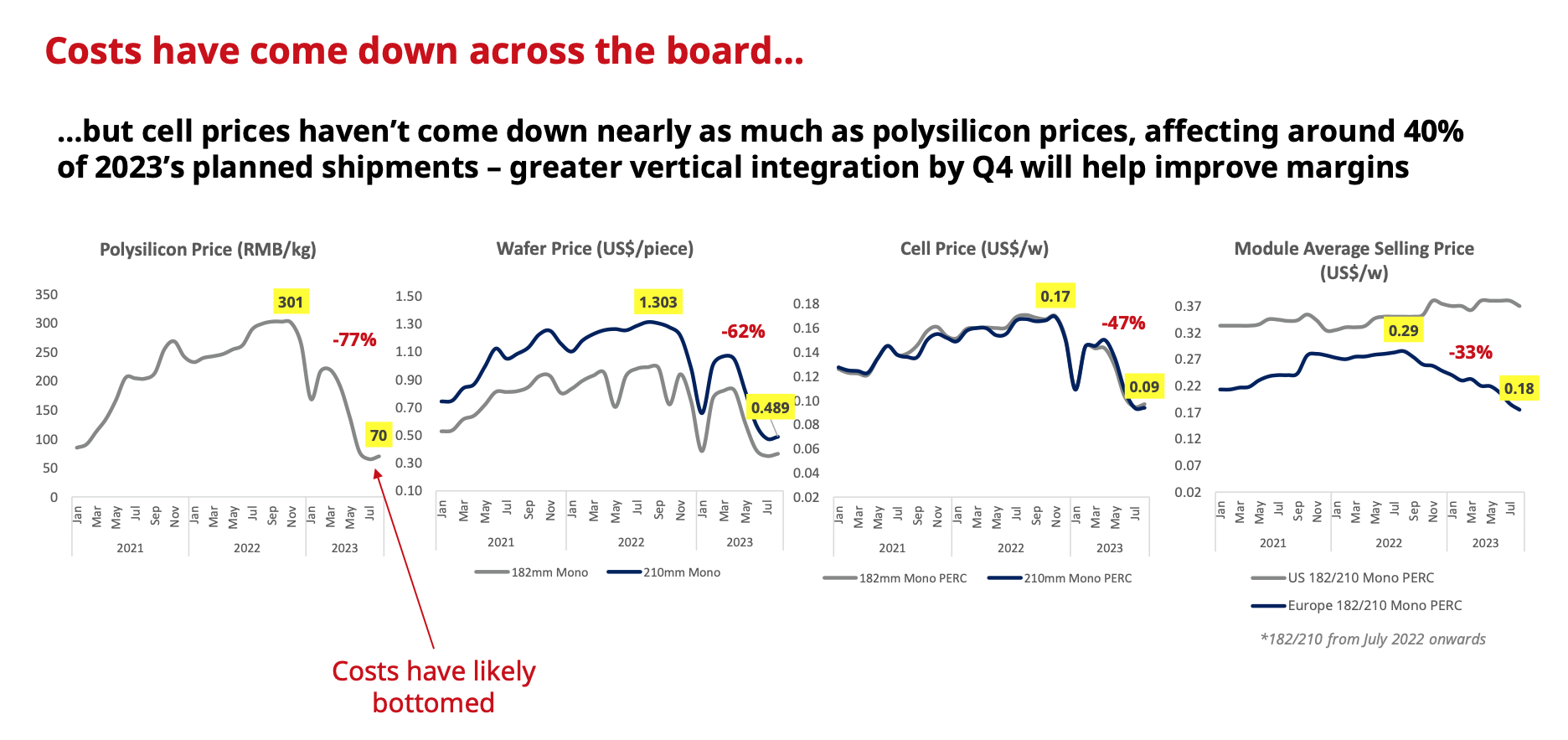

While net revenues were up only 2% year over year, the company managed to significantly reduce their costs, resulting in a near doubling of operating income year over year. This shows that management understands how to keep costs down in a challenging environment, and will likely be able to expand operating margins further if ASPs trend upward.

Canadian Solar Q2 Earnings Release

Canadian Solar Q2 Earnings Presentation

{kind=link}

Despite their ability to operate more efficiently, management gave lackluster forward guidance. The company forecasted full-year revenue of $8.5B-$9B compared to previous guidance of $9B-$9.5B. This updated guidance is well below the $9.35B analyst consensus. Guidance for Q3 sales of $1.9B-$2.1B was also well below the $2.51B consensus. Their outlook for full-year module shipments was maintained at 30-35 GW. This likely means that management expects ASPs to trend downward over the coming quarters.

Despite the company's disappointing guidance, we believe that they are currently undervalued. The stock has a lot of negativity priced into it already.

CSIQ Stock Price Action and Valuation

The disappointing guidance given by Canadian Solar's management has caused the stock to nosedive. This can be used as a buying opportunity by bullish investors, though the stock could continue its downward trend in the short term as traders continue to sell out of the name.

On a fundamental basis, the company is exceedingly cheap, trading at a PE under 6 and below book value. This wide of a discount appears to be unwarranted, especially when compared to solar peer First Solar (FSLR). In particular, the price to book value of the two companies stayed relatively similar up until the middle of 2022. During that time, First Solar likely rallied due to enthusiasm surrounding the Inflation Reduction Act. In our mind, such a wide discount is unwarranted and Canadian Solar can reasonably trade at half the book value multiple of First Solar and/or half the normalized PE multiple of First Solar. In an ideal world the valuation gap between the two companies would merge further, however US stocks are generally given a premium by investors and over the short term some foreign companies can be shunned for seemingly unexplainable reasons. Investors should be realistic with what they expect the stock to do in the short-medium term, as it can take a long time for relative valuation gaps to close, especially in international markets. Canadian Solar successfully diversifying into energy storage could end up being the catalyst that helps to give them a higher valuation as it reduces their exposure to the volatility of solar panel ASPs and input costs.

Risks

A major risk to Canadian Solar is the potential for their supply chain to become disrupted. This would impede the company's ability to convert their backlog into revenue, and cause significant difficulties for management.

Another potential risk is a slower than anticipated transition to renewables. This would dent the near-term demand for solar panels and energy storage, leading to lower revenue and profitability for Canadian Solar.

While both of these risks could end up being material, for the time being so much is already discounted into the stock that the risk/reward is attractive at these levels.

Key Takeaway

Canadian Solar is fundamentally undervalued, and the market has overreacted to their forward guidance. The company is taking the necessary steps to diversify their business and position themselves for future growth. Investors can use this dip as a buying opportunity but should have tempered expectations for what the stock will do in the short-medium term.

For further details see:

Canadian Solar Q2 Earnings: Selloff Overdone, Stock Attractively Priced