CSIQ - Canadian Solar: Q3 Earnings Highlight Prospects For Future Margin Gains

2023-12-18 12:49:28 ET

Summary

- Beneath the surface, Canadian Solar's Q3 earnings report shows (with inventory write-downs in mind) an increase in gross profit within the CSI Solar department.

- The CSI Solar department demonstrated resilience and adaptability in navigating market challenges and mitigating the impact of declining module prices.

- Canadian Solar's strategic shift toward retaining projects in the Recurrent Energy division aims to secure predictable revenues and long-term value creation.

Investment Thesis

A potential positive margin trajectory for Canadian Solar ( CSIQ ) in the next two years together with a substantial stock price decline of almost 50% since June, possibly makes a compelling case for the stock being undervalued. In the upcoming sections, I'll delve into why I'm confident about this upward trend in margins and why it's the linchpin of my bullish stance.

Introduction

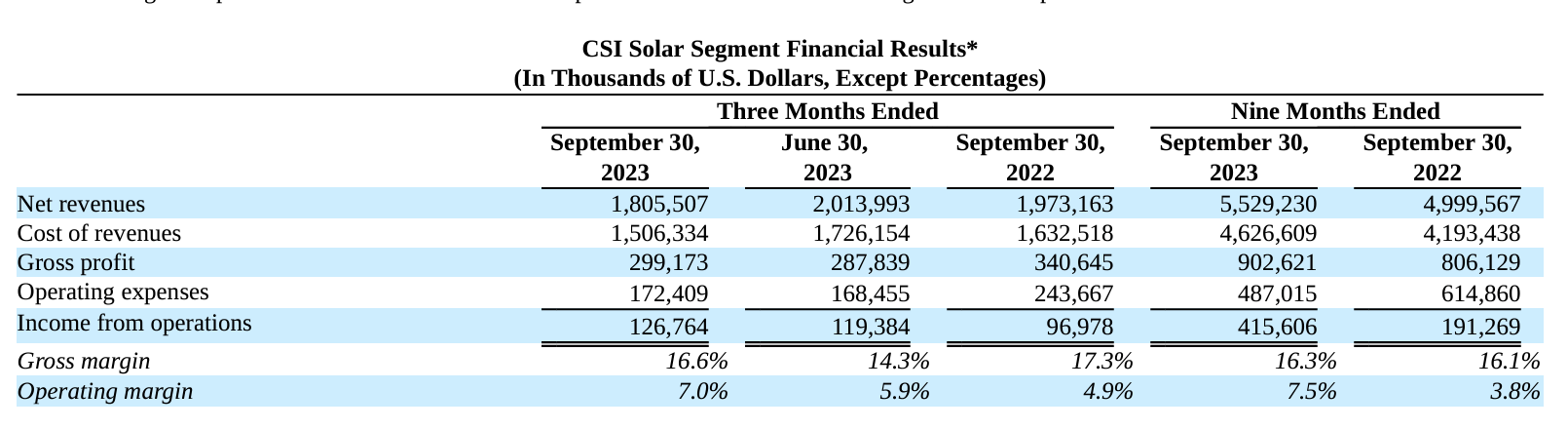

Canadian Solar, a stalwart in the renewable energy sector with an estimated revenue of almost $8 billion in calendar year 2023 , recently unveiled its Q3 earnings report . It has garnered mixed reactions from investors, but I want to argue that, beyond the surface, the report reveals a more nuanced financial narrative. With a notable highlight being the QoQ increase of the gross margin within the CSI Solar department (16.6% compared to 14.3% in Q2). Additionally, as we examine the management's commentary, another key point emerges: the potential for retained sites within the Recurrent Energy division to generate predictable, recurrent revenue streams - something the industry has been lacking.

Q3 Financial Snapshot

While some investors may have expressed disappointment, a closer examination of Canadian Solar's Q3 earnings reveals glimpses of positive indicators. Notably, the increased gross margin within the CSI Solar department stands out as a beacon of strength. This upward QoQ trend, coupled with the inventory write-downs ($35 million) dragging down gross margin in the back of our minds, the financial report presents a more nuanced perspective. As Yan Zhuang (CEO of CSI Solar) stated in Q3's earnings call on the gross margins of the CSI Solar division:

This was partially offset by lower solar modules price. It also included a $35 million inventory write-down, which was specifically for modules in warehouses intended for certain distributed generation markets. Without the write-down, CSI Solar's gross margin would have been 18.5%.

{kind=link}

CSI Solar's margin development (Canadian Solar)

Considering these write-downs, the gross margin all of a sudden appears much healthier considering it was 18.5% on an effective operating basis. As depicted in the above image, it surpasses both the previous quarter and the corresponding quarter from last year. The same positive trend is observed in the operating margin. For the last (fourth) quarter, the company roughly expects a similar gross margin and revenue profile from CSI Solar as was the case in the third quarter. While especially the gross margin was better than it looked on the surface in Q3, I'm expecting a lot more from the margin front in both 2024 and 2025.

CSI Solar Department's Potential Profits

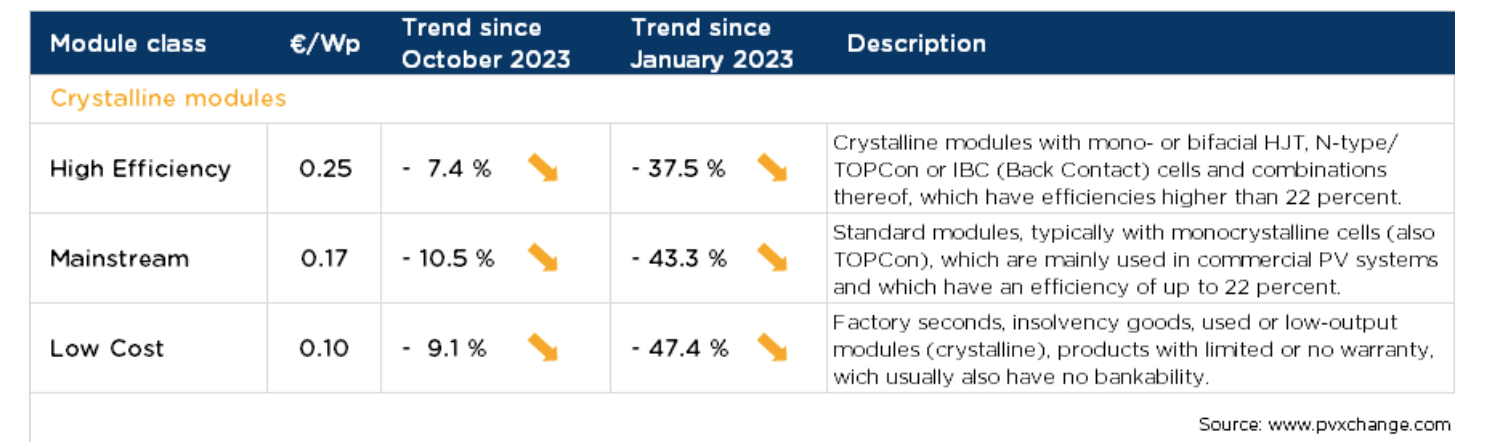

General solar module prices have seen a significant decline across the board in the last year as can be seen in the below table:

{kind=link}

Decline in solar module prices (pvXchange)

But, the fact that the CSI Solar department has been able to increase their gross margin both on a sequential as on year on year basis, shows significant adaptability in their cost control. This nuanced achievement highlights the department's agility in navigating dynamic market conditions, ensuring that the impact of declining module prices on the overall cost structure was mitigated.

The impact of interest rate increases on module prices is a crucial aspect to consider in understanding the dynamics of the solar market. The recent rise in interest rates has exerted downward pressure on module prices, posing a challenge for companies like CSI Solar. However, amidst this challenge lies an optimistic outlook. Forecasts suggest that selling prices are poised for a rebound, particularly when the rate environment stabilizes in the near future. On top of that, the solar industry is a price-elastic market: when prices drop enough, the demand will come in hard and will surpass the available supply. Something that of course will positively impact the price of solar modules, as Yan Zhuang also stated in Q3's earnings call:

So we anticipate a strong coming back in Europe and other markets as well. So and this is -- we're in a price-elastic market. So with such a price reduction, the demand is going to be stimulated to a much higher level. It just may not happen right away, but it's going to be -- maybe some delay in a few quarters, a couple of quarters will come back on the utility side as well.

This anticipated recovery in selling prices is not only a positive signal for the industry but also serves as a catalyst for bolstering gross profits in the coming quarters. The stabilization of the rate environment is expected to restore market confidence and contribute to the overall health and profitability of the solar sector, allowing companies to capitalize on the renewed market dynamics and potentially offset the challenges posed by earlier interest rate increases.

For 2024, CSI Solar is also poised for increased vertical integration. They're doing this by building out their in-house capacity of both ingot, wafer and cell manufacturing ( the key links of solar module manufacturing ). By having all the links of solar module manufacturing in-house, the company is significantly less dependent on third parties and, more importantly, is also able to streamline and optimize the complete manufacturing process from beginning to end. The anticipated benefits may include a notable reduction in the cost of revenues and thereby margin expansion. This foresight into the future underscores CSI Solar's commitment to sustainable growth and long-term profitability. See the image below on how both ingot and wafer capacity are expected to more than double in a year, which gives them the ability to deliver more than 50.4 GW vertical integrated solar modules a year from 2025 onwards:

{kind=link}

Significant capacity expansion (Canadian Solar)

To wrap this together, it wouldn't be surprising to witness CSI Solar's gross profit comfortably surpassing the 20% mark in the latter part of 2024, potentially escalating further in 2025. The company's strategic initiatives, including increased vertical integration and overall increase of solar module prices, position it for a far better future (higher gross margins) than that it's valued for today. As revenues ascend beyond the $8 billion mark, even a marginal shift in percentage points in gross profit can wield a substantial impact on the bottom line and overall profitability.

CSI Solar - Valuation

In evaluating CSI Solar, it's crucial to note that the following estimates are personal but I think I have adopted a conservative approach. Considering the capacity expansions in the pipeline, conservative projections suggest that CSI Solar could achieve at least $8 billion in revenue in 2024 and $9.5 billion in 2025. With a gross margin of 19% in 2024 and 20% in 2025, the corresponding gross profits would be $1.52 billion and $1.9 billion, respectively. Assuming a yearly growth of around 10% in operating expenses, this would lead to operating expenses of $750 million in 2024 and $825 million in 2025. Consequently, the projected operating profits are $750 million in 2024 and over $1 billion in 2025. As of December 16th, it's noteworthy that Canadian Solar's total market capitalization stands at just over $1.5 billion. Considering the $1 billion in operating profit in 2025, the subdivision of CSI Solar has the potential to generate almost 66% of Canadian Solar's complete market capitalization in operating profit by 2025. It's also worth emphasizing that any percentage point of gross margin expansion beyond the conservative estimate of 20% in 2025 (which is not completely unrealistic, as I have shown in the previous section) would contribute nearly $100 million to the operating profit, highlighting further the potential for Canadian Solar's favorable valuation.

| Year |

| 2024 |

| 2025 |

| Revenue |

| $8 billion |

| $9.5 billion |

| Gross profit |

| $1.52 billion |

| $1.9 billion |

| Operating expenses |

| $750 million |

| $825 million |

| Operating profit |

| $752 million |

| $1.075 billion |

It's imperative to recognize that Canadian Solar (only) holds 64% stake in CSI Solar. This leads to $480 million in operating profits attributed to Canadian Solar in 2024 and a projected $688 million in 2025, applying a conservative price-to-operating-profit ratio of 5 reveals a potential price target of $37.13 for 2024 and $53.22 for 2025. It's worth noting that this evaluation focuses solely on the ownership stake in CSI Solar, with the valuation excluding the 100% ownership of Recurrent Energy.

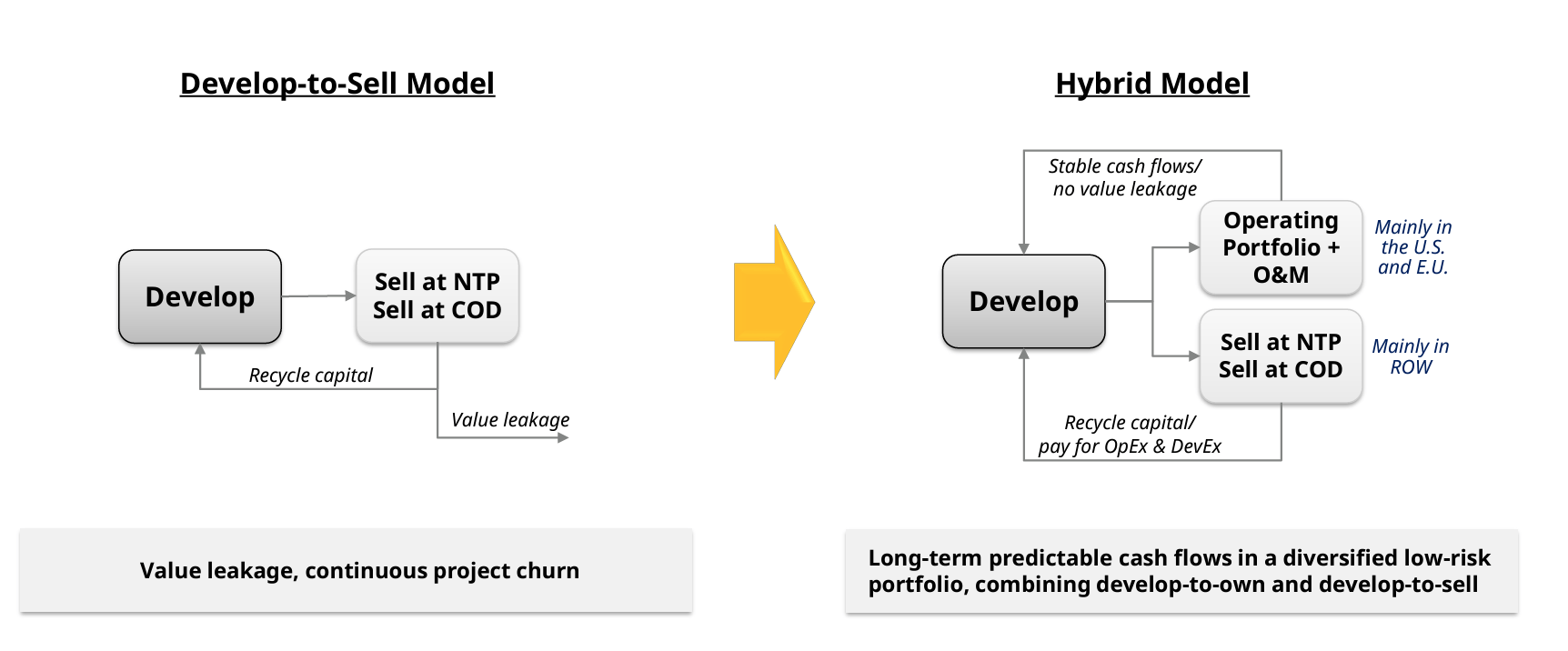

Recurrent Energy Department

Now the Recurrent Energy department, Canadian Solar's project development platform. In the last couple of months, this department made a strategic shift by choosing to limit the selling of large projects. A decision aimed at securing more predictable revenues (the selling of the energy produced and/or stored by the project) and potentially benefiting from the increasing value of these project assets over time. While this strategic shift meant foregoing the immediate advantage that large project sales often provide to the bottom line of the earnings statement, it underscores Canadian Solar's focus on long-term value creation. As Ismael Guerrero, CEO of the Recurrent Energy department, stated during last Quarters earnings call:

We are transitioning from mostly being a pure developer to a developer plus asset owner and operator. Over time, this will allow us to deliver more stable, forecastable growth, as over 70% of the revenues of the assets we intend to retain control of are fully contracted and diversified in low-risk addresses only.

And Shawn Qu, overall CEO of Canadian Solar, added:

Recurrent is shifting from develop and flip to develop and hold project. So, Recurrent is growing, but they are not selling project. We think we have been leaving too much money on the table by selling the project just after or before COD. We think our projects are very valuable, and connection points are also very valuable and you're not going to see this kind of PPA or this kind of connection point anymore. So, we think that by holding those projects, though, the value will grow.

{kind=link}

Better economics after strategic shift (Canadian Solar)

But, it has to be said that the retention of specific projects within the Recurrent Energy division introduces a substantial unknown into the equation. The question of how these retained projects will contribute to profitable recurrent revenues represents a critical aspect that could significantly influence Canadian Solar's future financial performance. As the company strategically navigates this shift, clarity on the magnitude of these retained project revenues and the associated profit margins becomes paramount. Right now, we're pretty much in the dark about this. Understanding the financial impact of these strategic decisions is essential for investors to gauge the long-term sustainability and profitability of Canadian Solar. The company's ability to articulate a comprehensive vision regarding the scale and financial outcomes of retained projects will be instrumental in providing investors with the insights needed to make informed decisions and fortify confidence in Canadian Solar's strategic trajectory. I will not value Recurrent Energy independently because there are still too many unknowns to make a reasonable estimation of future cash flows.

The Need for an Investor Day

In light of the substantial developments within Canadian Solar and Recurrent Energy in particular, I believe the call for a new Investor Day is imperative. The last gathering of this nature occurred in May 2015 , and given the transformative strides made since then, investors eagerly await updated insights into the company's strategic roadmap. An Investor Day can serve as a crucial platform for Canadian Solar to transparently communicate its trajectory regarding future capital allocation. As the company hinted at the normalization of investments post-2025, with the completion of most new plants and thereby scaled manufacturing capacity, investors may seek clarity on how capital will be allocated and optimized. Will they increase manufacturing capacity even more in the back end of the decade, or will capital be distributed in other ways? Additionally, a detailed outline of the potential recurrent revenues stemming from the Recurrent Energy division is paramount. An Investor Day would not only offer a comprehensive view of Canadian Solar's financial landscape but also instill confidence by addressing key concerns and showcasing the company's vision for sustained success. There seems to be so much potential, but also so many unknowns.

Risks

Investing in Canadian Solar carries inherent risks that investors should be mindful of. Firstly, the company operates in an industry where earnings are subject to fluctuations influenced by market dynamics, regulatory changes, and global economic conditions. Additionally, the solar sector, including energy storage, often grapples with relatively low-profit margins due to factors such as intense competition and evolving technology. Furthermore, the industry itself can be susceptible to commoditization. Despite these risks, it's crucial to acknowledge the broader context — the solar and energy storage industry is positioned for decades of secular growth. The global shift towards sustainable energy sources, coupled with increasing environmental consciousness, creates a substantial market opportunity . Therefore, while acknowledging the risks associated with Canadian Solar, investors may find the long-term growth potential, coupled with the company's strategic positioning in this burgeoning industry, an intriguing opportunity that comes with higher risk but also higher returns.

Conclusion

In conclusion, I'm slapping a Buy rating on it, mainly because I see those profit margins potentially doing a happy dance in the next two years. And let's be honest – if these margins do the tango, this company is highly undervalued. But at the same time, I'm keeping an eager eye on how this strategic shake-up in the Recurrent Energy division plays out, because we don't have enough information and numbers yet on how this could help the overall bottom line of Canadian Solar.

For further details see:

Canadian Solar: Q3 Earnings Highlight Prospects For Future Margin Gains