JKS - Canadian Solar: Underfollowed Value Play With Potential For Strong Growth

Summary

- Canadian Solar Inc. trades heavily discounted according to forward-looking metrics in comparison to peers in the solar industry.

- We believe Canadian Solar stock has as much as 60% long-term (~2 years) upside with at most 30% downside risk going forward.

- With a diversified portfolio of products and potential for further government-backed ESG narratives, we believe tailwinds will only further improve Canadian Solar Inc. stock's outlook in 2023-24.

Canadian Solar Is An Underfollowed Leader In One Of The Fastest-Growing Industries

Canadian Solar Inc. ( CSIQ ) is one of the world's largest solar power companies, with a market cap of ~$2.7 billion and growing. The company, headquarter in Canada, is a leading vertically-integrated provider of solar energy solutions, with a diversified portfolio of products that target both the utility and commercial & industrial solar power markets. The company is one of the few solar manufacturers that is vertically integrated, meaning it operates throughout the entire value chain of solar product development, from ingots and wafers to cells, modules, and complete systems ( Figure 1 ).

This gives Canadian Solar a cost advantage over its competitors, as well as a better understanding of the end-market requirements for its products. The company is also a leading provider of solar energy solutions, with a diversified portfolio of products that target both the utility and commercial & industrial solar power markets. In addition, Canadian Solar has a strong commitment to ESG (environmental, social, and governance) standards, which is evident in its industry-leading sustainability scores . All of these factors make Canadian Solar an attractive investment at its current discounted levels.

{kind=link}

Figure 1. Canadian Solar offers a wide range of solar products, from modules to inverters to complete systems and even energy storage solutions.

The company’s shares have rallied over the past year up over 66%. However, Canadian Solar’s stock price still trades at a discounted valuation. Given the company’s strong growth prospects, large scale operations, and diversified customer base, we believe that Canadian Solar’s stock is a strong buy at current levels and could offer as much as 50% further long-term upside conservatively. The company is also a leader in the fast-growing solar energy storage market and is well-positioned to benefit from the increasing demand for renewable energy.

Current Valuation

As of January 24, 2022, Canadian Solar Inc.'s stock was trading at around $43 per share. This gives the company a Price to Earnings ratio of ~16.7x earnings, a price to sales ratio of 0.4x revenue, and EV to sale ratio of ~0.64x sales (Figure 2). On average, the company trades at an approximate 60% discount to competitors according to these values. Only JinkoSolar ( JKS ) trades at competitive valuation levels, and we prefer Canadian Solar over Jinko due to the ever-present uncertainties that Chinese-headquartered investments bring.

Figure 2. Canadian solar trades at half that of most solar companies, minus Jinko Solar, a Chinese powerhouse.

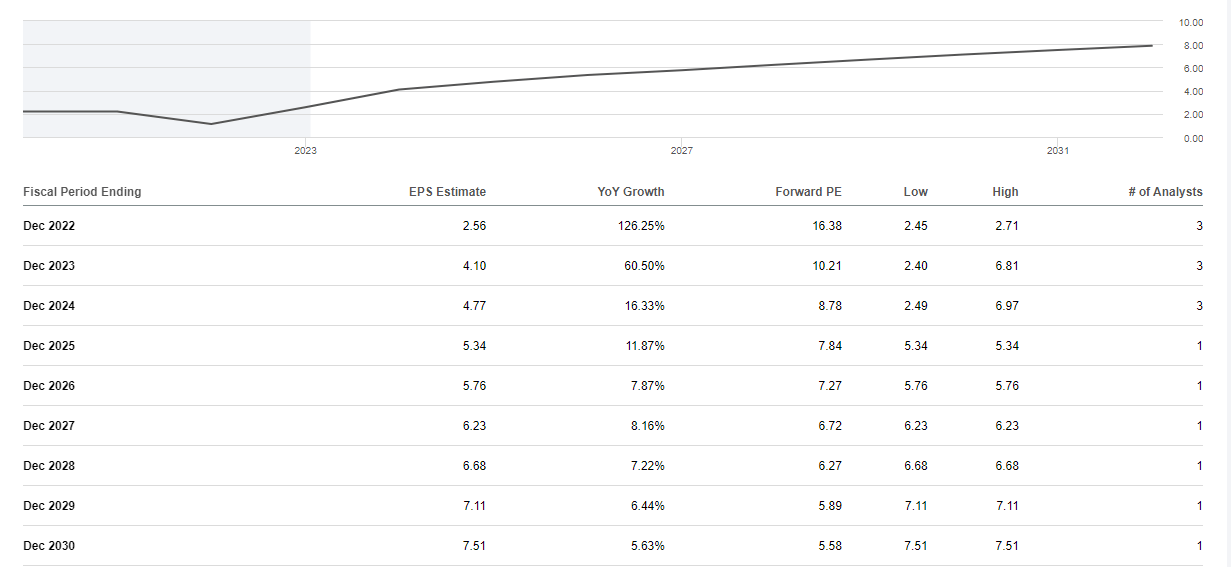

Wall Street analysts believe strong earnings and revenue growth is on the horizon for CSIQ, making an already discounted stock potentially even cheaper going forward if the company can hit estimates ( Figure 3 ). Therefore, we believe since the stock trades at an average discount of ~59% lower than competition based off of critical valuation metrics, and that growth is expected to outperform peers, that for the foreseeable future, 60% upside is conservatively possible by the end of 2024.

{kind=link}

Figure 3. Canadian solar is expected to grow multiple times faster than competitors over the next 2-3 years in both EPS & revenue.

Further catalysts, such as an international shift to green energy stipend by investments from governments across the world (Canadian Solar is found in over 23 countries across 6 continents ), will only provide further tailwinds and allow for potentially higher returns as markets slowly return to normal.

Risks

Canadian Solar has been in operation for over 20 years and is headquartered in Canada, giving them plenty of experience in a fairly new field of technology. While Canadian Solar's stock has been on a tear in recent years, up over 175% since 2018, there are a number of risks investors should be aware of before considering an investment. First, the solar industry is notoriously cyclical in the past and is highly dependent on government subsidies and incentives to remain competitive to natural gas & oil. When these subsidies are reduced or eliminated, as has happened in a number of countries in recent years with elections of new leaders with different political & economical views, Canadian Solar's stock has tended to take a hit (2015/2016).

Second, the company has a large amount of debt, which stands at around $2.6 billion. This debt load could become a problem if the solar market weakens and Canadian Solar is unable to refinance its debt and provide market-beating growth. With over $1B cash currently on hand, we do not see this as a major issue, but it should be monitored from quarter to quarter.

Lastly, the solar industry is highly competitive, and Canadian Solar faces stiff competition from other companies, such as First Solar ( FSLR ) and SunPower ( SPWR ). We believe the overall market share of solar vs. other forms of energy is growing at a pace that will allow most solar competitors to flourish alongside CSIQ and do not see this as a huge issue for the foreseeable future.

Overall, there appears to be a fairly strong level of support around the $30 level, and we do not see CSIQ dipping below this unless major negative news were to break. This would hint at ~30% potential downside, giving the stock a 2:1 upside to downside ratio in our opinion, which is an enticing investment offering from just about any stock.

Overall Investment Summary

In conclusion, Canadian Solar Inc. is a stock worth considering for investment in 2023. Discounted valuations and tailwinds from ESG and government support should help propel the stock higher. We believe even after the recent rally there could be as much as 60% long-term upside left in Canadian Solar stock. Canadian Solar Inc. has a solid balance sheet, a strong history of profitability, and a diversified portfolio of products and geographies. With just around 30% downside risk in our view, Canadian Solar stock deserves a strong look for investors looking for a solar play in 2023-24. Competitors trade at much higher prices despite having lackluster growth projected for coming years, unlike Canadian Solar Inc.

For further details see:

Canadian Solar: Underfollowed Value Play With Potential For Strong Growth