CDUAF - Canadian Utilities: Not Exactly Cheap But Fundamentally Appealing

2023-03-24 17:37:35 ET

Summary

- In this article, I'll be looking over Canadian Utilities. The company has long been on my watchlist, and given it's been dropping a bit, I'm eager to give my view.

- Canadian Utilities is a great company overall - and I'd say it has some excellent upside worth considering at the right price.

- CU definitely isn't "cheap" here - but for some of you, it might be that this price is enough to make you interested.

Dear readers/subscribers,

In this article, I will share my thesis with you regarding the company Canadian Utilities ( CU:CA ) (CDUAF). The company is actually a subsidiary of Atco, the holding company, and offers both gas and electricity services across key areas, with key segments such as generation, transmission, and distribution of electricity, as well as its pipeline network not only for gas but water as well. Aside from this, CU also has a Retail energy segment.

I like utilities, and I invest in plenty of them - Let me show you why I may consider, at the right price, adding CU to that part of my portfolio.

Canadian Utilities - What the company is and does

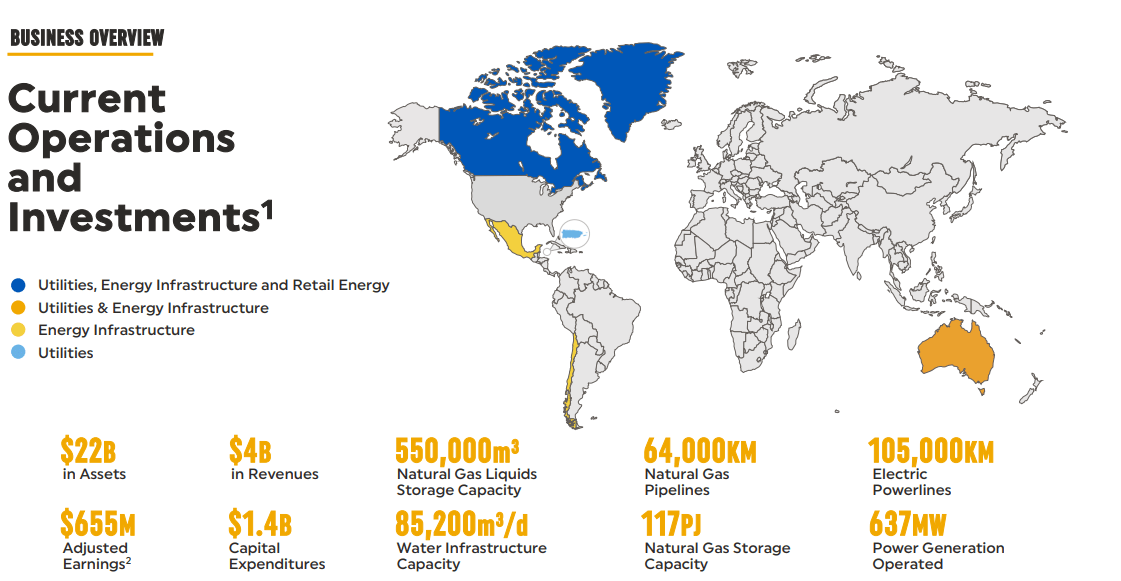

Canadian Utilities is "an ATCO" company. In this piece, we don't look specifically at ATCO though, we focus on CU. And CU is far from uninteresting on its own. With 5,000 employees managing $22B in distributing, producing, and other types of infrastructure assets, the company brings an impressive list of things to the table, including revenues, Natgas capacity, water capacity, power generation, powerlines, and gas lines.

{kind=link}

The company has an interesting set of business units, found in Energy infrastructure, which comprises the generation of electricity, storage/industrial water, and clean fuels. The utility Unit meanwhile, focuses on the distribution, and transmission of electricity and natgas, as well as the above-mentioned and described international operations that are housed in the company.

The company's strategy mimics the strategy of almost any utility you can think of. Leverage its expertise in its operational areas, invest in the infrastructure and assets, optimize and harden, where necessary, its portfolio, and in turn drive cash flows and earnings.

Expansionary targets are aimed at LATAM, NA, and Australia to drive growth. The company has a rate base of $14.9B, driving over $650M in annual earnings, and from that paying $460M in dividends.

Most of the company's money comes from Natgas - about 46.2% of the FY22 revenue, with 36.9% from electricity. The company manages a very decent GM of 67.5%, down to a 28% OM and a net income margin of 15.6%. The company's gross and operating margins are at the top of its sector - CU is better than 85% of its regulated utility peers on a global basis. When it comes down to net margins, the company is still in the top 75%, but it's RoE/RoA and ROIC are average for what utilities usually manage.

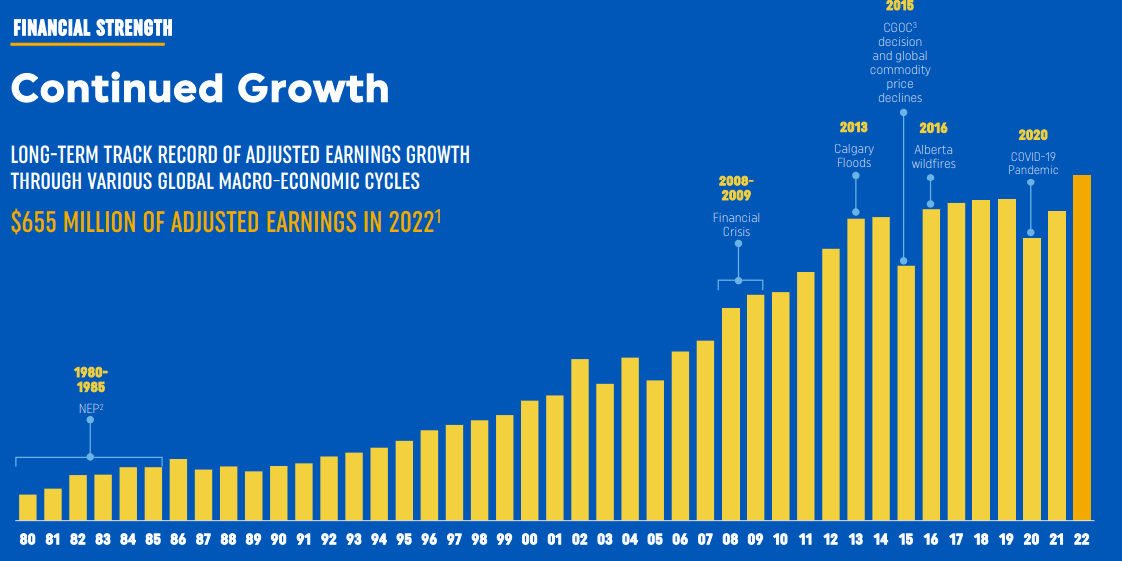

However, the company is overall very solid fundamentally. With positive RoA, CFROA, growing returns, good overall ratios, and growing margins (at least for the past few years), CU manages to check a lot of boxes. Its growth track record is very solid.

{kind=link}

I believe it's fair to say that growth has somewhat slowed down since 2013 and onward, due to a mix of natural disasters, COVID-19, and other factors. It doesn't really take away from what the company is capable of, but it does mute forward expectations somewhat.

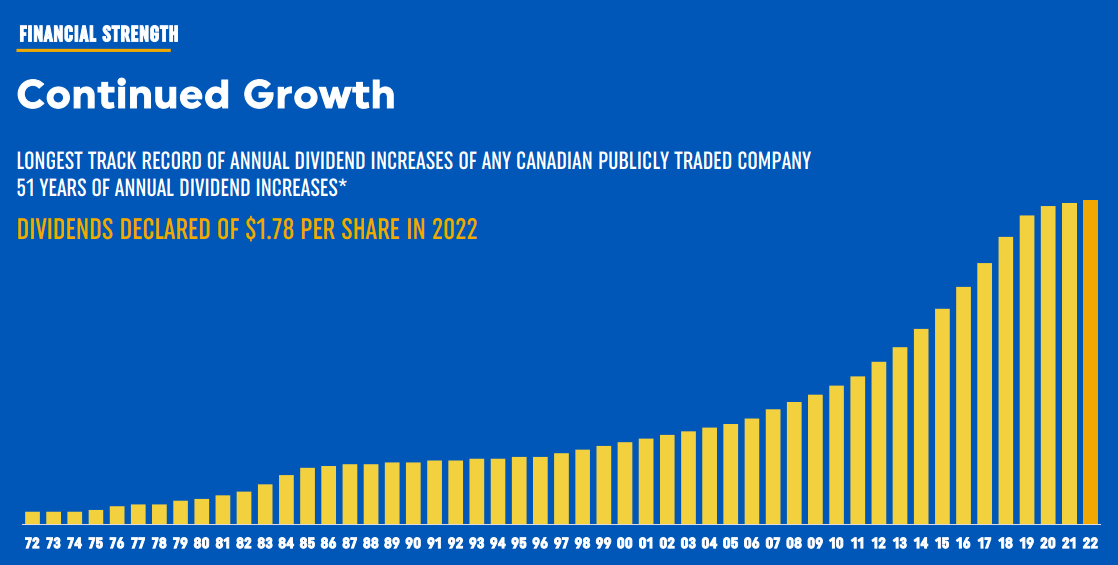

Dividend growth, as a result of this, has definitely been slowing down, and the payout ratio has been increasing. It's trended between 45-100+% and is currently at 86%, which is probably one of its biggest flaws in terms of comps.

{kind=link}

To put it simply, don't expect CU to grow its payout as quickly as it historically has. The earnings as they are now, and are expected to be in the near term, don't appear to support that. Current growth estimates for the adjusted EPS are around 1.35% on an annual basis until 2025E. This also explains in part why the company typically trades at 15-17x P/E but is now down to 14.8x. More on that later.

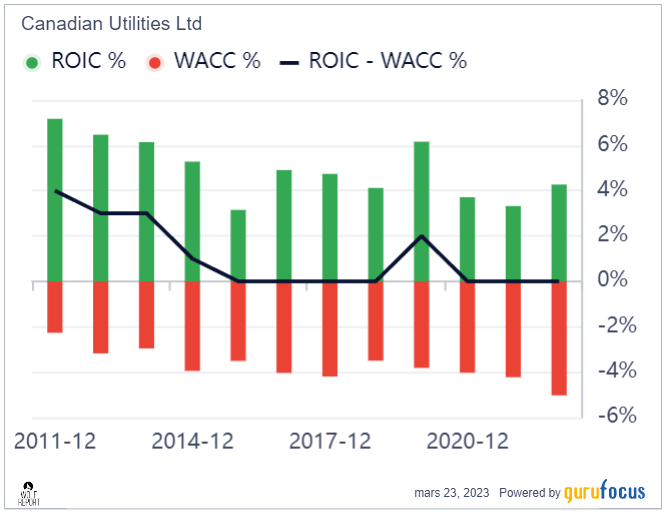

Another risk worth mentioning is that CU isn't the best deliverer of value in terms of its projects. Its ROIC is on par with its cost/WACC, which means that the current projects/ambitions the company has ventured into, haven't added much value to the company. This was something that we could see more positively back in 2011-2013 when there was a 3-4% spread, but it's been mostly flat for more than 6 years at this point, with the exception of 2018. As an example, Enel ( ENLAY ), a utility I hold a significant, 5%+ position, has a positive spread with a good ROIC of 3% above the company's weighted average cost of capital for 2022. This metric is important to me, especially in a utility.

{kind=link}

This doesn't make CU unbuyable - I'm only seeking to explain and highlight some of the flaws I see here, that in my view don't exist in all utilities I look at. CU is still a great business, and it has annualized RoR of 9.3% over a 20-year period, which is above both capped utilities and the return for the composite. This in itself is worth noting.

CU, like many players in the space, is working towards its net-zero goal, which includes cleaner fuels, more renewables, more energy infrastructure and storage, higher efficiency, and other targets you've heard about 20 times from other utilities around the globe at this point.

CU is also very highly rated - BBB+ in terms of credit, and despite its overall high debt of close to 60% to capital, or a debt-to-equity ratio of 1.39x, well above the industry average of 0.96x, it still has good access to capital and isn't in a worrying position.

The yield of over 5% is also a highlight here - as is the company's record of profitability, which is better than almost any one peer you compare it to. The company is, as with other regulated utilities, a stable base of recurring OCF and dividends. It's mission-critical for any modern society.

Also, CU is a dividend king - one of the few in Canada.

Again, do not underestimate CU, because there is plenty to like here. While I look at debt, I do not consider it worrying, because we're, once again, looking at a utility business.

4Q22 results were released in early March. Big news included the recent close of the Suncor (SU) portfolio and the question on many CU investors' minds is whether the company will seek to monetize some of these assets or add some JV/Partner to some of them. What CU has in front of it will require plenty of capital to fund, and CU isn't in the perfect position to do this on its own - especially not in a rising interest rate environment. The company itself admits this, saying the capital requirements exceed its historical sources and abilities (Source: CU earnings Call). I'm also keeping a close eye on the company's ESG targets and growth projects - as I've eluded to, the company's current return on invested capital in relation to its funding costs is not appealing - and I believe this will actually get worse with rising interest rates.

Put simply, if the company seeks to put money to work in value-destructive ESG (or other) projects, I intend to discount it.

The "basic" thesis here though, remains attractive. CU is a high-yielding utility with a good regulated rate base, and decent prospects of maintaining its profitability, even if growth is likely to be muted going forward.

That brings me to the following valuation thesis.

Canadian Utilities valuation

Overall, Canadian Utilities is undervalued respective to its usual premium. But as you've seen, there are reasons for this undervaluation. The company is not "as good" as it once was, with return metrics definitely showing a trend toward the negative direction, meaning lower than they once were. This needs to be considered.

Why?

Because there are utilities that are cheaper and don't face the same issues.

Declining operating margins, declining revenue (per share), and worsening financial metrics and profitability metrics should never be underestimated but understood.

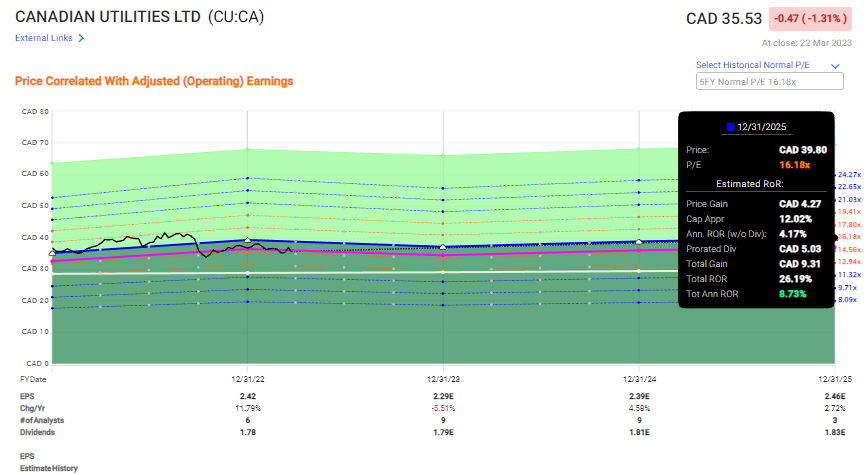

If you value this company at 15-16x, as would be the historical average, and take into account an average EPS growth rate of 0.6% per year until 2025E, you could make returns of 8.73% per year, coming to about 26.2% RoR in 3 years.

{kind=link}

This is not "bad" as such - and it certainly seems safe, given the company we're covering here.

However, I do feel compelled to draw your attention to some of CU's excellent global comps - and the holding company ATCO is actually one of them, even if the yield isn't as high. It also suffers from some of the same issues in terms of margin decline, and the ROIC spread isn't better - but it does score higher in terms of safety. And if you're willing to look beyond Canada, which I believe you should be, you can find great businesses like Enel, Electricite de France ( ECIFF ), Engie ( ENGIY ), E.ON ( EONGY ), and others - all of the ones I mentioned are much bigger in terms of market cap, they also have great yields, and they come at an excellent undervaluation. Most of them do have other issues - issue-free companies do not exist as such - but they are at the very least comparable to this one.

Analysts following the company do exist - 9 of them from S&P Global. They stick to the more premium view in terms of price targets, from $37 low to $43 high (that's Canadian dollars), but then choose not to follow their own averages, which comes to $39.33%, a 10.7% upside from today's share price, but only one "BUY" recommendation.

Consequently, I do not believe these targets or opinions should be adhered to closely - or at all, because obviously these analysts also see some of those inherent risks to the company. FCF-based DCF models do work for CU, and with a 10% discount rate and an FCF of $2.85, and a growth rate of 4-5%, this gives us a margin of safety of a whopping 0.14% and a target stock price of around $35.5. Any change to this growth rate, say moving it down a single percent, takes 6-8% off that MoS.

I say again, too little safety here.

The upside for CU is slim. You can make returns here that are potentially market-beating, if only by a hair.

However, given the company's challenges, and its already-present declines in margins and profitability, I give the company a rating of "HOLD", and an introductory share price of no more than $33/share for the Canadian native ticker. At 13x normalized P/E, where I think this company may return double digits from, I could be convinced to change that.

Thesis

- Canadian Utilities is a foundationally solid business, but one that has been encountering growth and margin issues for the past few years. Its high yield and established rate base make it safe, but I don't see much growth potential in the business. Due to a relatively non-discounted valuation, I cap the realistic upside at 8-10% per year.

- This is not enough for me, and I rate the company a "HOLD". At a cheaper price, or if the company can turn around its returns/profitability, I would be willing to change this, but in today's environment, I don't see this easily happening.

- My PT for CU is a conservative $33/share.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Not cheap enough at this point, neither as a "cheap" price nor in terms of realistic upside. I say "no" at this time.

For further details see:

Canadian Utilities: Not Exactly Cheap, But Fundamentally Appealing