CU - Canadian Utilities: Undervalued But Fundamentals Lack Substantial Growth Avenues

2023-09-20 09:13:23 ET

Summary

- Canadian Utilities, a subsidiary of ATCO Group, reported a decline in revenue, net income, and free cash flow in Q2'23.

- The company focuses on optimizing cost structures, investing in core earnings, and transitioning towards renewables.

- CU's stock has underperformed compared to its peers in the utility industry, but it is undervalued according to discounted cash flow and relative valuation models.

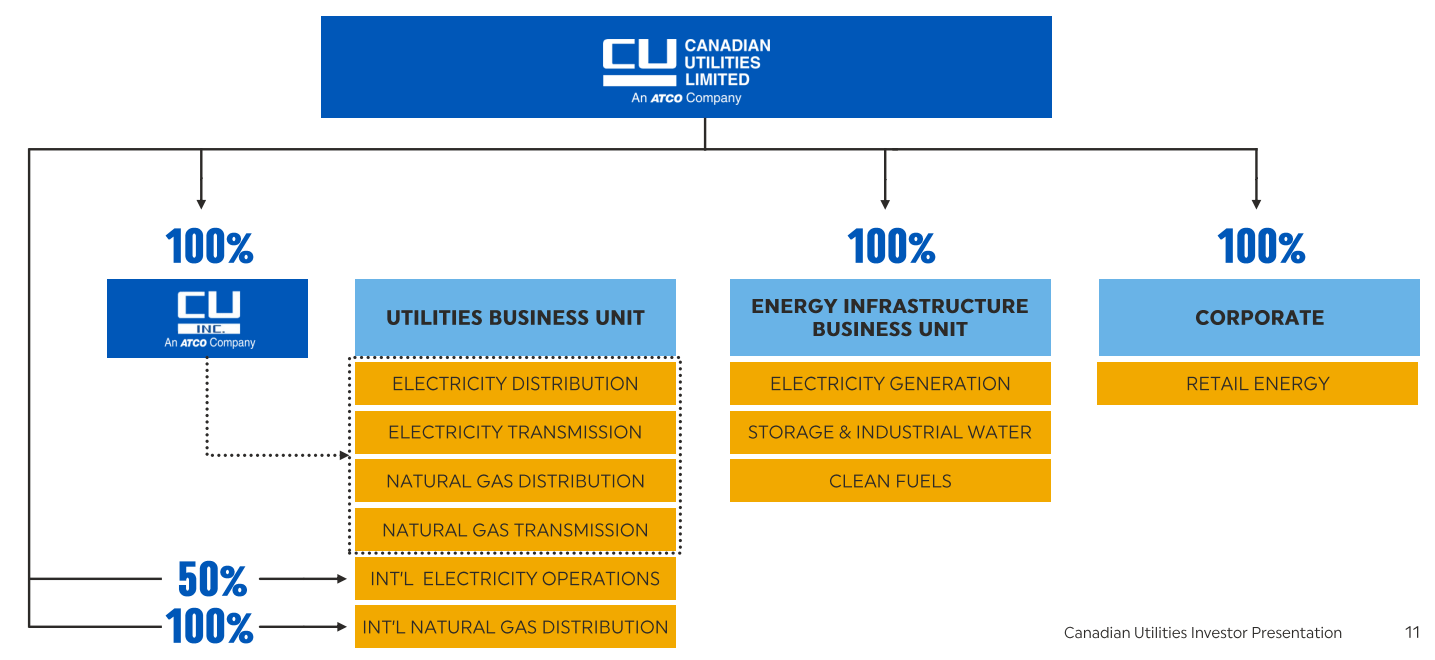

Canadian Utilities ( CU ) is a Calgary, Canada-based multinational asset-holding business, which operates as a direct subsidiary of the ATCO Group (ACO.X:CA) of Companies. The business is currently segmented into three primary verticals; its utilities business unit, which includes the firm's electricity and natural gas operations, its energy infrastructure business, and retail energy business.

{kind=link}

Through these activities, in Q2'23, CU has achieved a revenue of $879.00mn- a 5.79% decline, alongside a net income of $105.00mn- a 30.46% decline- and a free cash flow of -$39.00mn- a 126.00% decline driven by falling financing and operating free cash flows.

Introduction

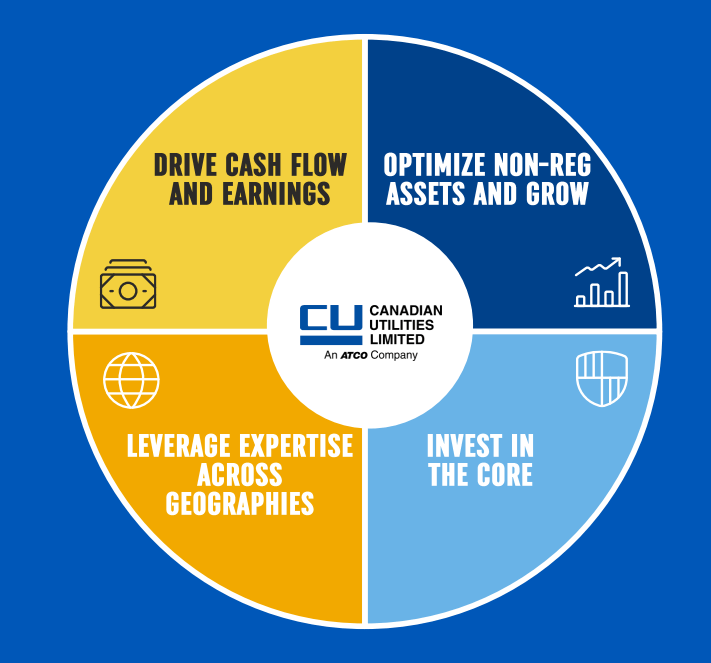

Driving the value of the business, CU focuses on a fourfold virtuous cycle of optimized cost structures, investments in core earnings, a diverse geographic rate base, all in the effort to secure stable and incrementally growing free cash flows and net earnings.

{kind=link}

On a more granular level, CU aims to gradually invest in the energy transition towards renewables, support operational reliability and resilience, ensure greater ESG inclusion with climate change and environment stewardship, connect with local and regional partners, and invest in CU's people.

Canadian Utilities Investor Presentation 2023

Although CU thus runs from a strong operational base and remains undervalued, the company professes lower growth capabilities than peers, with a higher implicit beta, leading me to rate the company a 'hold'.

Valuation & Financials

General Overview

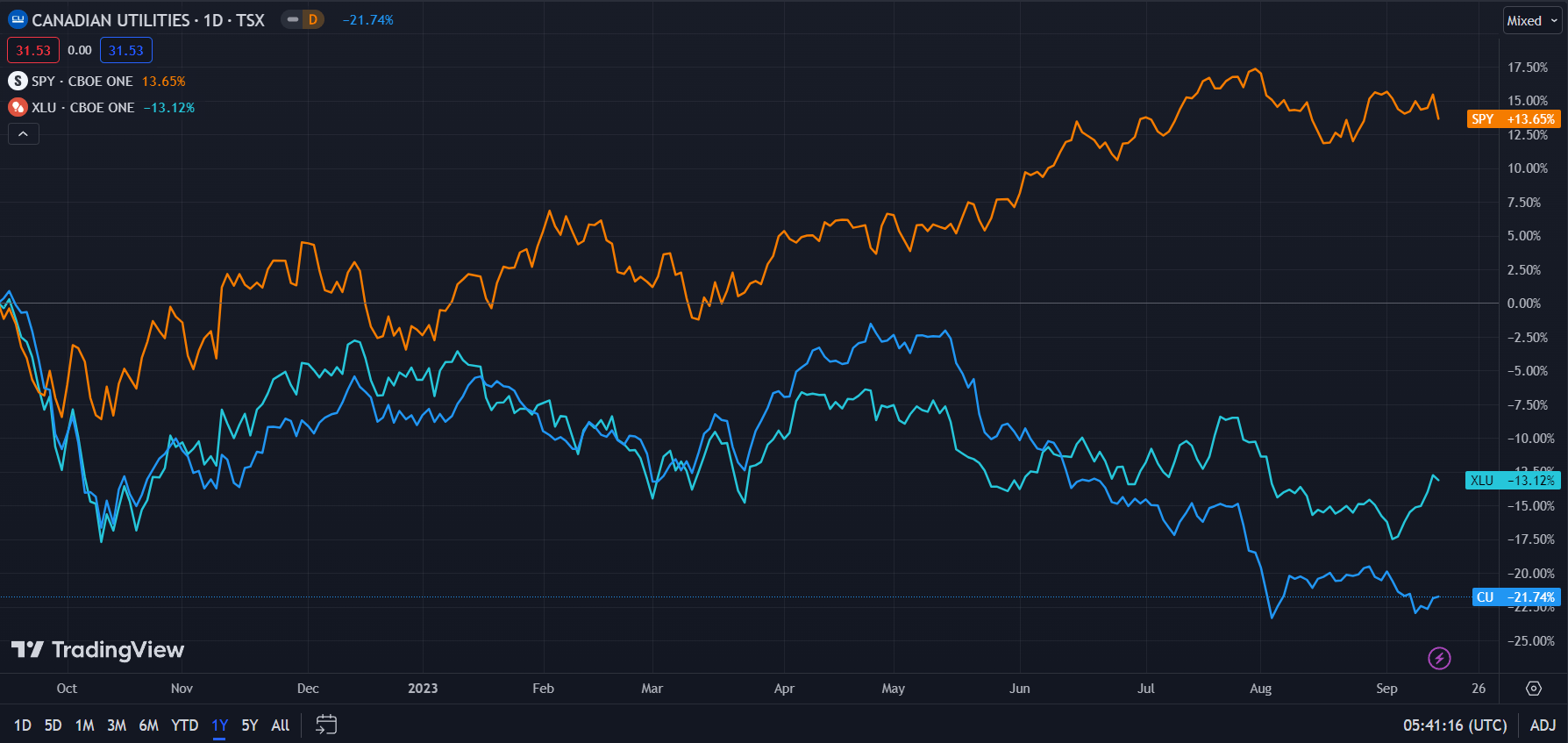

In the TTM period, CU's stock- down 21.74%- has experienced poorer price action than both the Utilities Select Sector SPDR Fund ( XLU )- down 13.12%- and the broader market, as represented by the S&P500 ( SPY )- up 13.65% in the same period.

Canadian Utilities (Dark Blue) vs Industry and Market (TradingView)

{kind=link}

While the underperformance of the general utility industry is a testament to the industry's poorer risk-adjusted returns relative to treasuries, CU's greater decline manifests the firm's greater volatility.

Comparable Companies

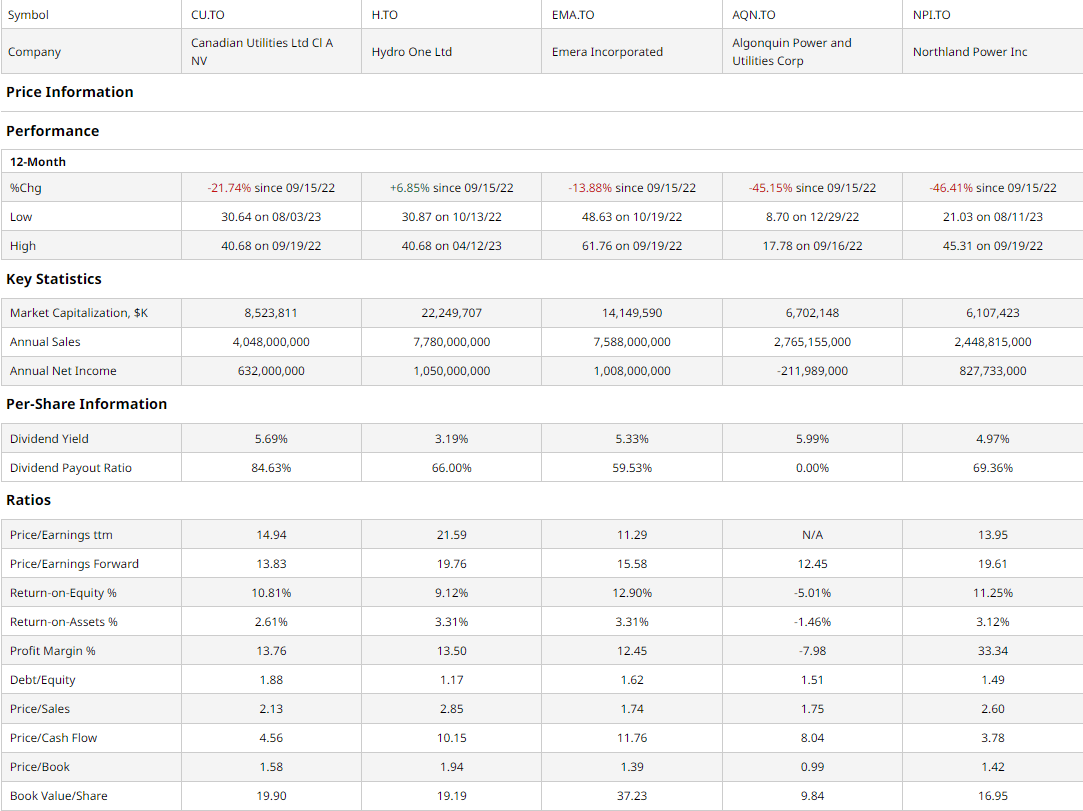

The utility industry remains highly consolidated, with a marginal number of direct regional competitors and high barriers to entry. As such, I sought to compare CU with similarly sized Canadian utility companies. This group includes Toronto-based electricity transmission and distribution utility, Hydro One (H:CA), Halifax-based energy holding firm, Emera (EMA:CA), Oakville-based renewable energy and utility conglomerate, Algonquin Power and Utilities Corporation (AQN:CA), and Toronto-based multinational power producer, Northland Power (NPI:CA).

{kind=link}

In the trailing 12-month period, CU has experienced a 21.74% price decline, in the middle of the peer group but still a significant devaluation. Nonetheless, CU may experience limited upside, with greater value demonstrated on a multiples basis but lower growth potential.

For instance, CU maintains the second-lowest forward P/E ratio in addition to the second-lowest P/CF after Northland. Moreover, although CU has the highest payout ratio, it sustains the second-highest dividend and returns the second-highest book value per share.

On the flip side, the firm has a reduced capacity for growth, with the third-lowest ROE and the second-lowest ROA, demonstrating the company's inability to foster growth with core assets. Furthermore, CU's free cash flow allocation is diminished by the highest debt/equity of the peer group and the highest payout ratio.

Valuation

According to my discounted cash flow valuation, at its base case, the net present value of CU is $33.81, meaning, at its current price of $31.63, the stock is undervalued by 6%.

My model, calculated over 5 years without perpetual growth built-in, assumes a discount rate of 10%, accounting for CU's higher equity risk premium- with higher beta than peers- and higher relative debt levels. Additionally, remaining conservative, I estimated a 5Y forward revenue growth rate of 2%, lower than the trailing revenue growth rate of 3.08%.

{kind=link}

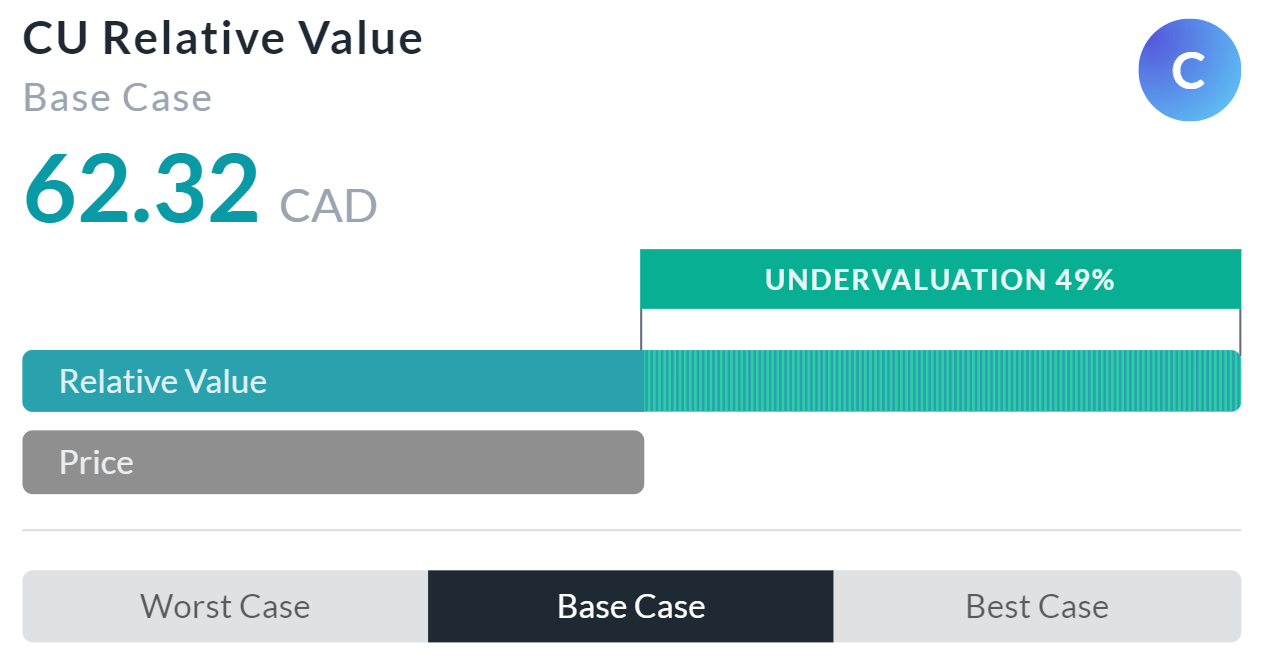

Alpha Spread's multiples-based relative valuation tool more than supports my thesis on undervaluation, estimating a base case undervaluation of 49%, with a relative value of $62.32.

However, due to Alpha Spread's inability to adequately incorporate CU's debt levels or discount dividends, I believe the relative valuation model overvalues the firm.

As such, using a weighted average skewed towards my DCF, the fair value of CU is $35.57, with the company currently undervalued by 12%.

CU Remains Foundationally Strong But Has a Lower Growth Ceiling

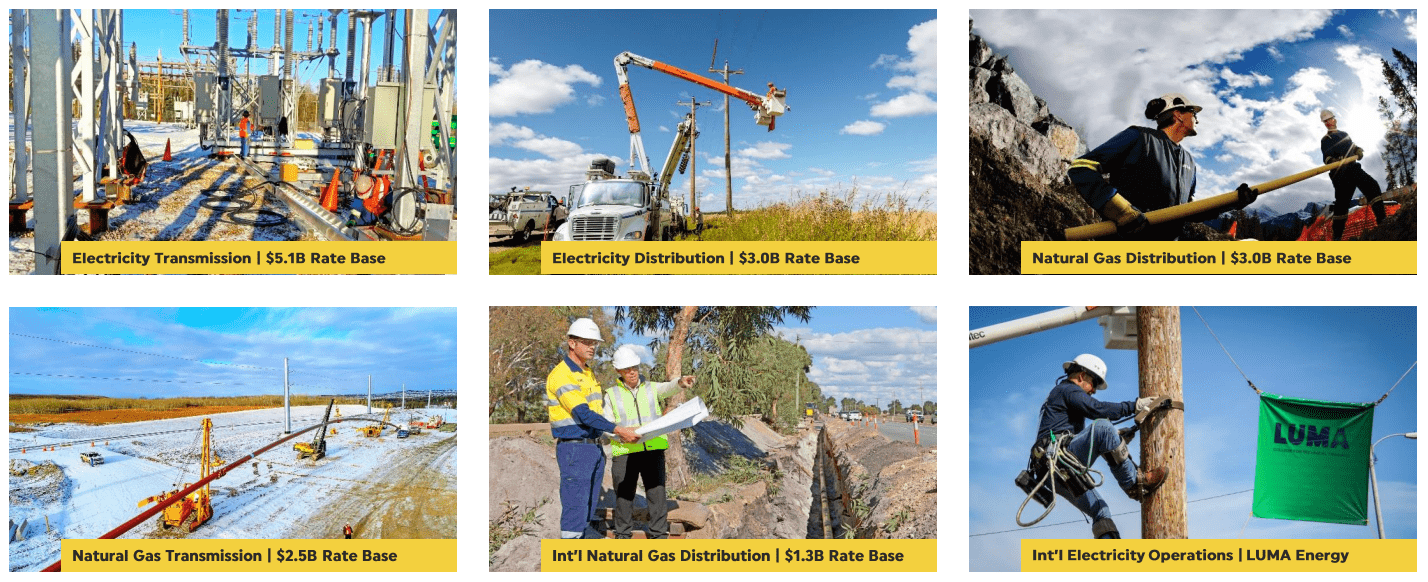

CU's core competency remains its inelastic rate base, with rate growth a key avenue for cash flow incline. The vertical diversity of CU's rate base- with a presence across the utility value chain including electricity transmission and distribution, and natural gas transmission and distribution- only reinforces the stability of CU's long-run cash flows.

{kind=link}

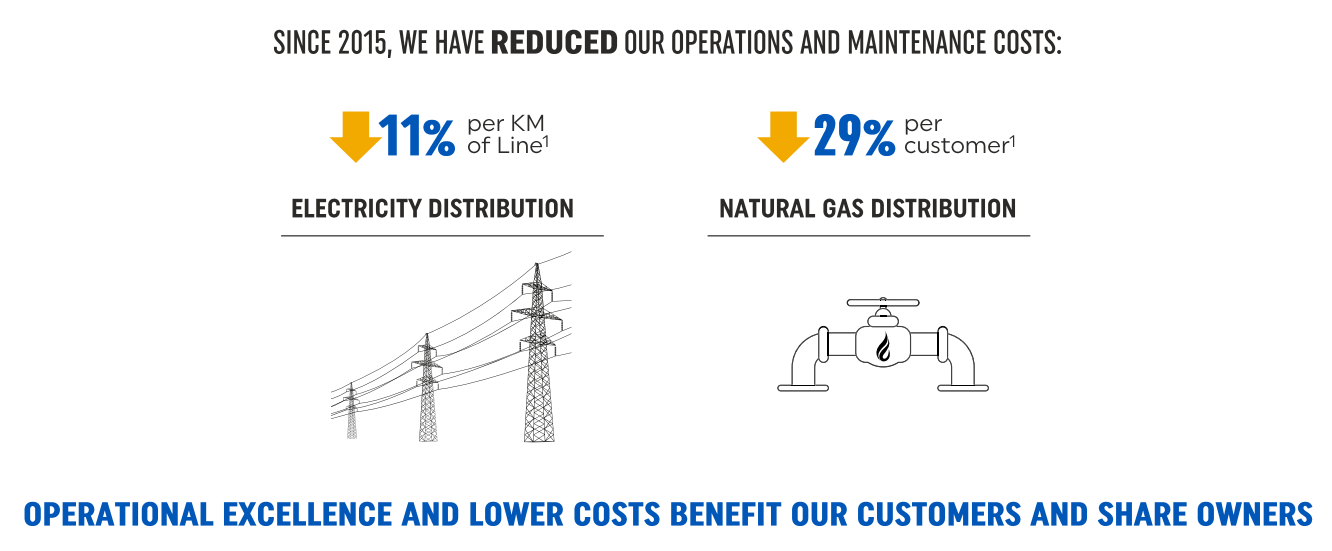

The firm further aims for a degree of margin expansion through the optimization of its cost base, aiming for operational efficiency and lower overhead. The firm has, in the past 8 years, successfully reduced the operational cost of electricity distribution by 11% and the cost of natural gas distribution by 29% per customer. However, the ability to optimize costs does have diminishing returns, with cost savings becoming increasingly marginal.

{kind=link}

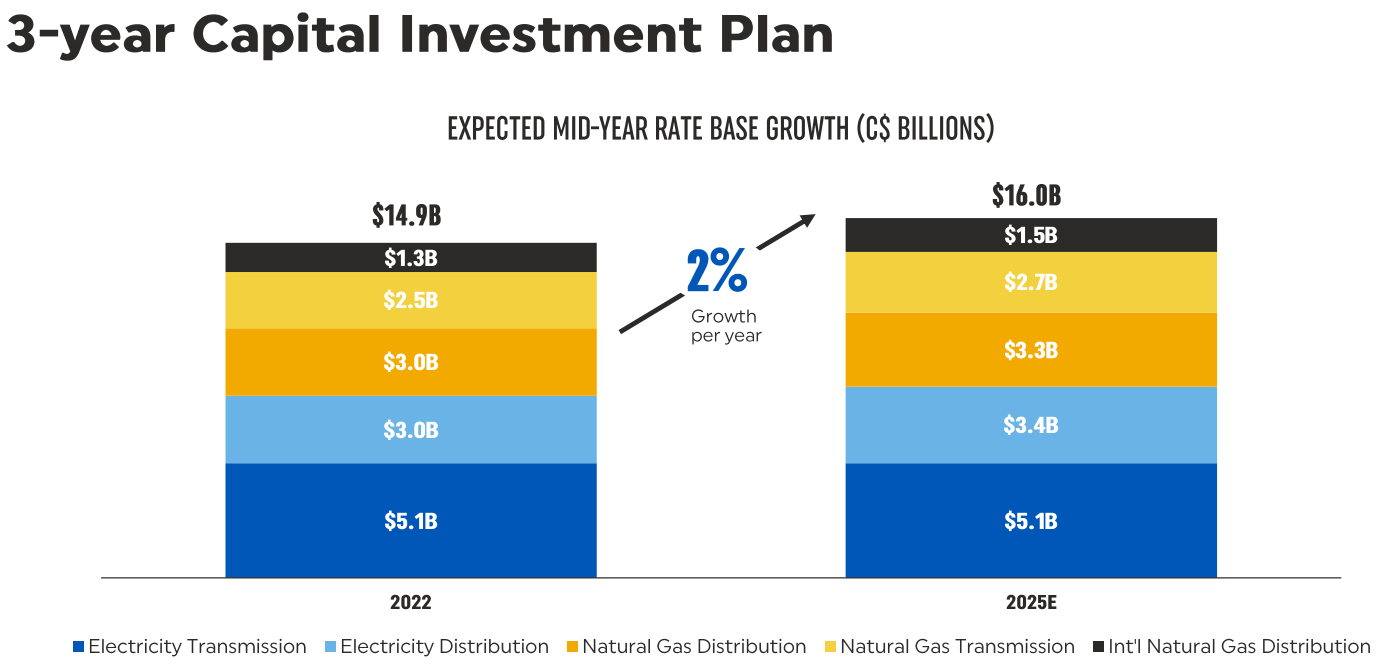

CU's capital investment plan summarizes my broader thesis for the company, aiming for slow, incrementalist growth and focusing on core elements. Through its 3Y capital plan, the company sees 2% annualized rate base growth, lower than industry averages and a testament to my thesis of lower fundamental upside.

{kind=link}

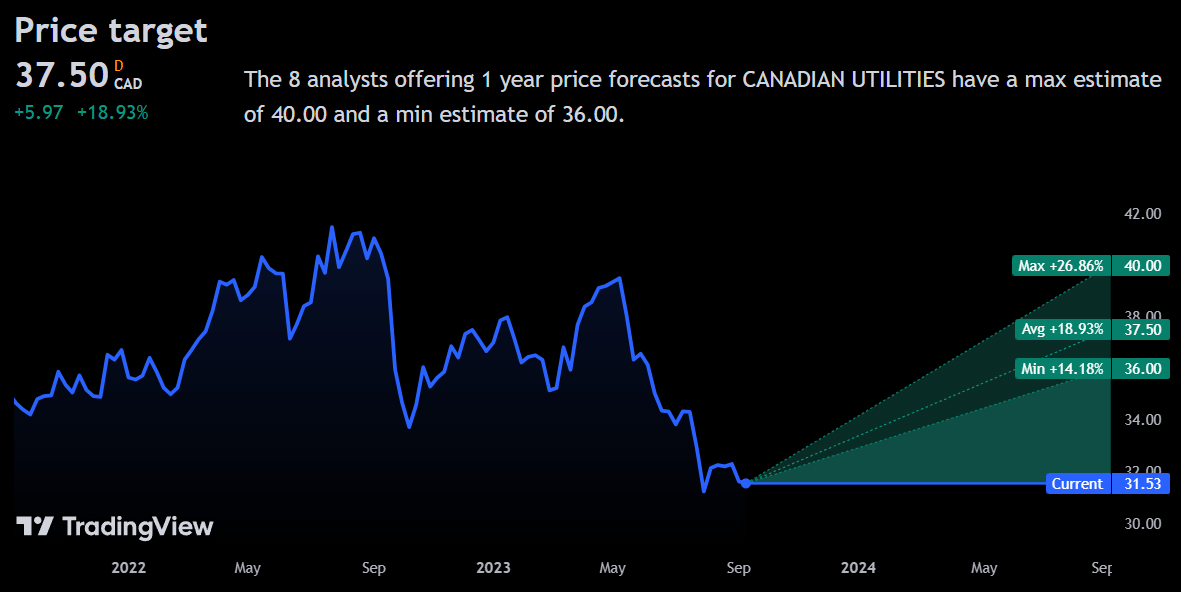

Wall Street Consensus

Analysts largely disagree with my 'hold' rating of the stock, estimating an average 1Y price target of 18.93% to a price of $37.50.

{kind=link}

Even at the minimum projected price of $36.00, analysts expect the stock to experience 14.18% growth.

I believe analysts misconstrue the undervaluation of utilities as a whole as a greater undervaluation for CU, who do not possess cash flow resilience and reversion capabilities to the same level as peers, given poorer historic price action.

Risks & Challenges

Sticky Interest Rates May Continue to Compress the Stock Price

As aforementioned, rising interest rates have been the primary driver behind CU's price decline, with the superior risk-adjusted returns of bonds, and similar price dynamics and investor appetite for utilities leading to the utilities industry facing reduced stock prices. If interest rates remain high, CU, even among utilities, faces greater fundamental risk, with a higher debt level and dividend payout ratio leading to highly depressed free cash flows.

Inflationary Pressures May Reduce Profitability

On the flip side, with Canadian core inflation numbers remaining stubbornly high and experiencing upward reversion from the previous month, CU is also confronted with higher operational costs, reducing the company's earnings capabilities and reversing its price optimization procedures. As such, CU and investors are likely to see reduced profitability.

Conclusion

Going forward, CU remains a fundamentally strong company which is slightly undervalued but maintains limited growth upside, leading to the stock's neutral rating.

For further details see:

Canadian Utilities: Undervalued But Fundamentals Lack Substantial Growth Avenues