CANO - Cano Health: Potential Buyout In The Making

Summary

- Cano Health currently presents an interesting investment opportunity with a potential short-term 58% upside.

- Recently, rumors appeared that Cano Health has received acquisition interest, with healthcare industry giants CVS Health, Humana and UnitedHealth among the rumored buyers.

- Given ongoing pressure from two prominent activists and industry consolidation trends, I expect a company sale to be announced shortly.

A Potential company sale might be brewing up behind the scenes. Cano Health (CANO) owns and operates senior primary care health centers in nine US states, with a primary focus on Florida. Recently, Bloomberg , Reuters and WSJ reported that the company has received acquisition interests, with health industry giants Humana (HUM), UnitedHealth (UNH) and CVS Health (CVS) mentioned as the front-runners to buyout CANO. Acquisition rumors follow activism from several of CANO's shareholders. In March, Daniel Loeb's Third Point (2.2% of voting power) started to push the company towards strategic alternatives, arguing that CANO should address the value gap (arising from the company going public through a SPAC) by initiating a company sale. Then, in August, Owl Creek Asset Management (owns 1%) delivered a letter, also considering the company undervalued versus peers and industry transactions. As it stands, it seems that the management/insiders (who own 55%) have been under pressure from two prominent activists to sell the company. Not surprisingly, in August, CANO's management stated that the company is open to all strategic alternatives and has hired financial advisors. Reportedly, the second round of discussions is currently ongoing , with the deal possibly finalized in the upcoming weeks. Reports do not mention the acquisition price, however, peer/transaction multiples (also mentioned by the activist Owl Creek) suggest $14/share might be a reasonable price tag - this would imply a 58% upside from current levels.

Buyout rumors come amid broader healthcare industry consolidation trends as large healthcare insurers are scooping up healthcare providers in an effort to combine insurance and healthcare provider activities. The industry is currently in a shift towards value based care - a model where providers are paid based on patient health outcomes (as opposed to the traditional fee-for-service model where patients pay for each service rather than outcome). Naturally, the value-based care model closely aligns the interests of both health insurance firms and healthcare providers. Numerous industry executives, including Humana's Medicare President, have noted that value-based model has benefits for providers/insurers, including noticeably higher contribution margins, thus pushing up incentives for consolidation. Not surprisingly, these dynamics have spurred a number of acquisitions of healthcare providers by major health insurers. CVS is currently buying health care platform provider Signify Health (Sep'22), UNH is scooping up home care provider LHC Group (announced in Mar'22) and HUM has already acquired home healthcare provider Kindred at Home (Aug'21). The industry has also seen increasing M&A activity from non-insurers entering the space, including Amazon (AMZN) acquiring primary care company One Medical (announced in Jul'22, by the way CVS was one of the bidders there as well) and Walgreens Boots Alliance (WBA) purchasing a majority stake in primary care provider VillageMD (Oct'21). These dynamics and the fact that CANO might be an attractive target have also been recently reiterated by CANO's CEO:

I expect continued consolidation and acceleration in the paradigm shift of value-based care. And what this means for us is yet another validation of how attractive our asset is and the industry as a whole.

A Potential acquisition would make strategic sense for either of the rumored buyers HUM, UNH or CVS given CANO's extensive presence in Florida's primary care market. CANO is reportedly the largest independent value-based primary care provider to Medicare/Medicaid patients in the state. Meanwhile, three potential suitors currently rank as the three largest primary care insurers in the Florida. Humana and Cano have seemingly deep ties - HUM has been invested in Cano Health prior to CANO's IPO and still owns an undisclosed stake. Currently, CANO is HUM's biggest independent primary care provider in Florida. Interestingly, as part of their earlier agreement, HUM has a right of first refusal , meaning that HUM can match any acquisition offer made for CANO. Notably, HUM has significantly expanded its investment in primary senior care in the last five years, recently stating that the TAM is very large at $700bn. As part of its joint venture with PE firm Welsh Carson, Humana now aims to open 100 new CenterWell senior primary care clinics in the next three years. From the CEO's remarks during Q2'22 earnings call :

We do see some great opportunity today, both CenterWell primary care and the home are agnostic and continue to see great growth, serving both other payers and other parts of the Medicare system. And at the same time, we're also seeing opportunity within our primary - within our pharmacy area to offer some agnostic opportunities there. So the ability for it to integrate and also to expand beyond the Medicare side of the business is really at the heart of what you see us more formally creating the CenterWell service side, while on the insurance side, continuing to leverage the efficiencies across the various different insurance platforms.

Meanwhile, CVS's management, in addition to the recent acquisition of Signify Health, has recently stated that their priority is the same - to expand into the primary care segment:

From the Morgan Stanley Global Healthcare Conference :

Well I think we are urging, obviously - we're very urging, I just ask our teams and I think if you think about our strategy, really we've been very clear that we want to extend into care delivery and we're starting with Signify. We can't always determine the order. Obviously primary care is something we believe we need to advance because we really want to enable consumers to have a differentiate experience and improve health outcomes. So we're playing our game.

From the CVS Q2'22 earnings call :

As you would expect, we are being very disciplined both strategically and financially, as we pursue kind of our M&A strategy. We can't be in the primary care without M&A. We've been very clear about that.

Valuation

{kind=link}

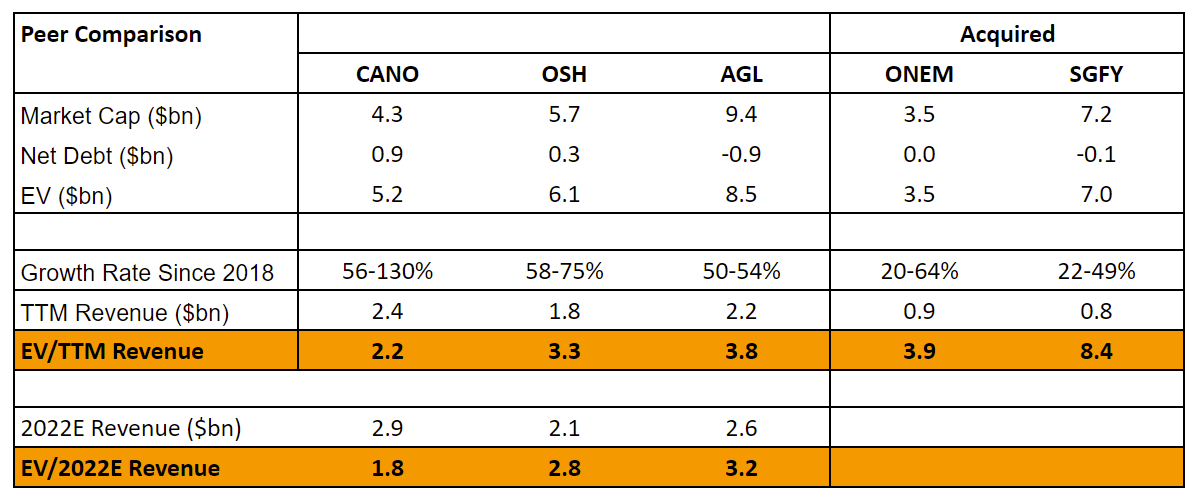

At current price levels, CANO seems undervalued on a TTM/2022E revenue basis relative to larger peers OSH (also owns and operates primary care centers) and AGL (runs primary care physician networks so not as comparable). Moreover, recently announced ONEM and SGFY acquisitions were done at noticeably higher multiples. Activist Owl Creek notes the following reasons for why CANO might be trading at a discount to peers/industry transactions:

Unfortunately, Cano has consistently traded at a discount to its peers due to its SPAC heritage, its hybrid model (owned and operated medical centers along with affiliates), and heavy concentration in the South Florida market. One could argue for some discount due to one or more of these factors, but the valuation discrepancy between Cano and peers is highly punitive.

Another activist Third Point also agrees that the undervaluation is explained by both SPAC heritage and the company's shareholder base (given dual class structure and high insider ownership):

However given recent developments at the Issuer and taking into account the market's largely unfavorable view of companies taken public through special purpose acquisition vehicles, the Reporting Persons believe the Board of Directors should immediately engage financial and legal advisors to commence a review of strategic alternatives.

[…]

The Reporting Persons believe this strategic review should focus on a sale of the Issuer, and that a properly run sales process is likely to result in offers representing a substantial premium to the Issuer's trading price. The Reporting Persons believe that the Issuer is unlikely to achieve such valuation on a stand-alone basis, in part due to structural issues with its shareholder base.

The activist Owl Creek has stated that CANO has been undervalued by the market despite having higher 2022E revenues than both OSH/AGL and being on track to exceed 2022 membership/revenue/EBITDA guidance. Using a 3x revenue multiple based on peers OSH/AGL and Amazon's acquisition of ONEM, Owl Creek arrives at an acquisition price tag of $14/share. The markets have moved down a bit since the letter was written, so a 3x multiple would now translate to a $13/share price.

More background on CANO

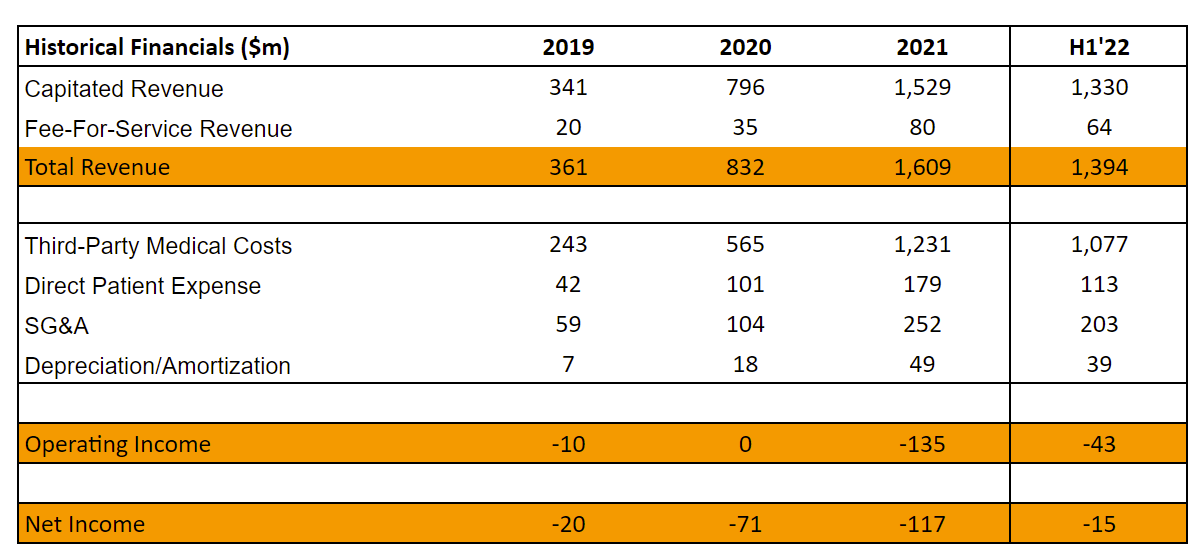

Historical financials are provided below:

{kind=link}

Financially, since going public in 2020, CANO has managed to record high revenue growth - 93% in 2021. Notably, the growth has to a large degree been driven by acquisitions, including purchase of University Health Care and Doctor's Medical Center for a total of $900m (announced in Jun'21 and Jul'21). This has allowed the company to significantly increase its patient base as number of memberships has expanded from 156k to 282k over the last year. That said, the business is yet to turn profitable and is still burning cash - $135m in 2021 operating losses.

From a liquidity perspective, the company is quite highly levered with $878m in net debt (compared to $4.2bn market cap). Given CANO's business model, the company needs extensive capital to accelerate further growth. At current share price levels, any equity raise would seem highly dilutive given that even after the buyout rumors the stock trades below pre-2022 levels of $9-$16/share.

CANO's shares are rather tightly held with 55% of the voting power (Class A + Class B shares) held by the management + insiders. CANO went public in 2020 through a SPAC backed by Starwood Capital CEO Barry Sternlicht who now holds 9% voting power. Another 33% of total shares are owned by a PE firm InTandem Capital Partners which has backed the company since 2016. Both Sternlicht and InTandem's managing partner Elliot Cooperstone currently sit on CANO's board. Interestingly, Cooperstone was previously the CEO of Prodigy Health Group which was acquired by Aetna, a subsidiary of CVS Health. Another 17% are held by six institutional investors, including FMR (7%), BlackRock (3%) and Millennium Asset Management (2%), among others.

Risks

For further details see:

Cano Health: Potential Buyout In The Making