CAJ - Canon: A Diamond In The Rough Or A Cautionary Tale? A DCF Analysis

Summary

- Solid FY22 numbers, positive outlook and further expansion into US are promising.

- Solid financials with great cash flow overall.

- Can be a good long-term investment if we see actual growth.

- DCF analysis with conservative numbers says the stock is a bargain.

Investment Thesis

With the year-end earnings released, I decided to look at the financials of Canon (CAJ) to see if there is a potential for a long-term position on the horizon. Stellar FY22 results and low P/E ratio caught my attention and even with low growth in USD terms, the company is a buy based on my DCF valuation and gives some exposure to international markets.

This article will focus mainly on the company's financials and a little bit about the company's potential growth to come up with some reasonable growth assumptions for the next 10 years to see if this is worthy of a long-term hold and if the company has some solid prospects. The growth assumptions will be conservative with a decent margin of safety baked into the DCF analysis.

FY2022 Results

A couple of weeks ago the company published its full-year 2022 results on its investor relations site. The numbers I saw were very good. The company has been steadily growing still in double digits. Growth in the printing and imaging segments is going strong thanks to the return to office across the world. It seems that this will continue to improve over the coming years as more and more companies go back to their offices after the pandemic. The printing Segment had a solid 16.7% y-o-y growth, while Imaging had 22.9% growth.

Sales in Japan increased only 4% year on year, however, the Americas have shown a 30% increase in sales, followed by Europe at a 15.5% increase and Asia and Oceania at 7.1%, giving the total sales increase y-o-y of almost 15%. That is quite a solid year for the company. All these results lead to a bottom-line increase of 13.6% y-o-y.

What's Ahead for the Company

The management believes it will see strong demand for their office MFDs and their interchangeable lens digital cameras. People demand high-quality personal devices and Canon is no slouch here for sure. This optimism has swayed my valuation model somewhat; however, I am toning it down just to be on the safe side.

We have been in the pandemic era for the last 3 years now. The concerns will always linger, but I do believe that these concerns will be much smaller than they have been one or two years ago when productivity was obliterated across all offices and people started to work from home. Right now, many companies have adopted the hybrid environment, with some places making their employees work from home only 2 days a week. Some are fully back in the office, and some are still WFH. The demand for Canon's MFDs I believe will continue to grow as we get out of the pandemic; however, it may not be as robust as it was pre-pandemic.

Growth in the US

In November of 2022, the company announced that they are establishing a new subsidiary that will strengthen its presence in the US medical market. This will accelerate growth for the segment which grew 6.9% y-o-y and 17.4% in Q4 of 2022. The medical segment is the third largest revenue generator for the company and more exposure to the most influential medical market in the world will most definitely accelerate the growth of the segment. The company's increased presence in the US with the newly established Canon Healthcare USA will have great synergies with already established Canon Medical Systems USA. We will see the results of this move in the next year or so.

The company is not just sitting around. I can see that they are trying to establish themselves as a leader in many segments, which can only be good for current and future shareholders.

Financials

Let's have a look under the hood at how the company has been performing over the last 5 years and how healthy the books are.

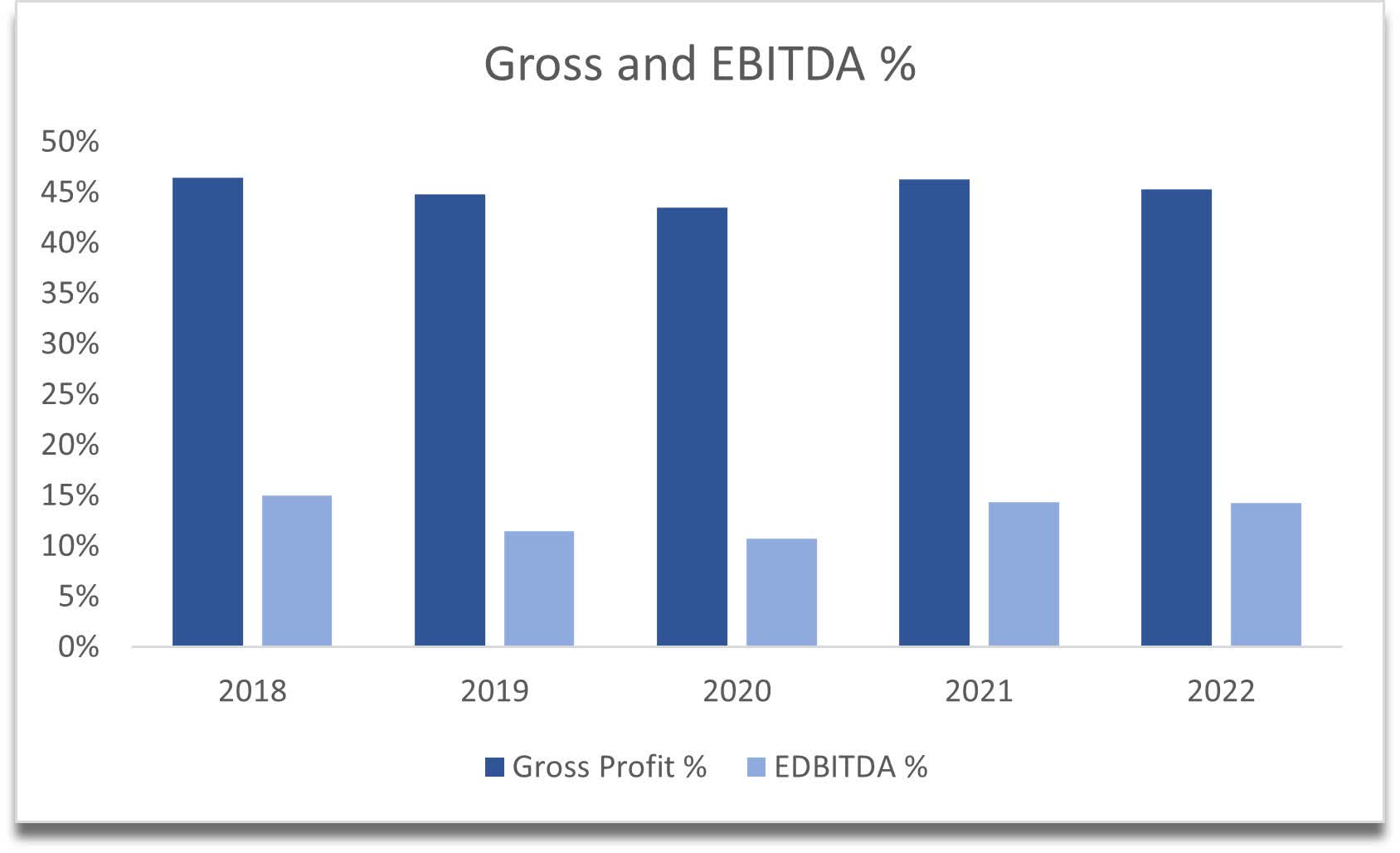

First things first, let's have a look at the margins. Gross margins have been hovering around 44% to 46% for the last 5 years, which may not look the best, but it all depends on the industry and when comparing to its competitors like HP Inc ( HPQ ) and Epson ( OTCPK:SEKEF ), Canon is a leader.

Gross Margin of Canon against comps (Seeking Alpha)

EBITDA margins are also quite healthy, and the company is leading against its competitors also.

EBITDA of Canon vs Comps (Seeking Alpha)

{kind=link}

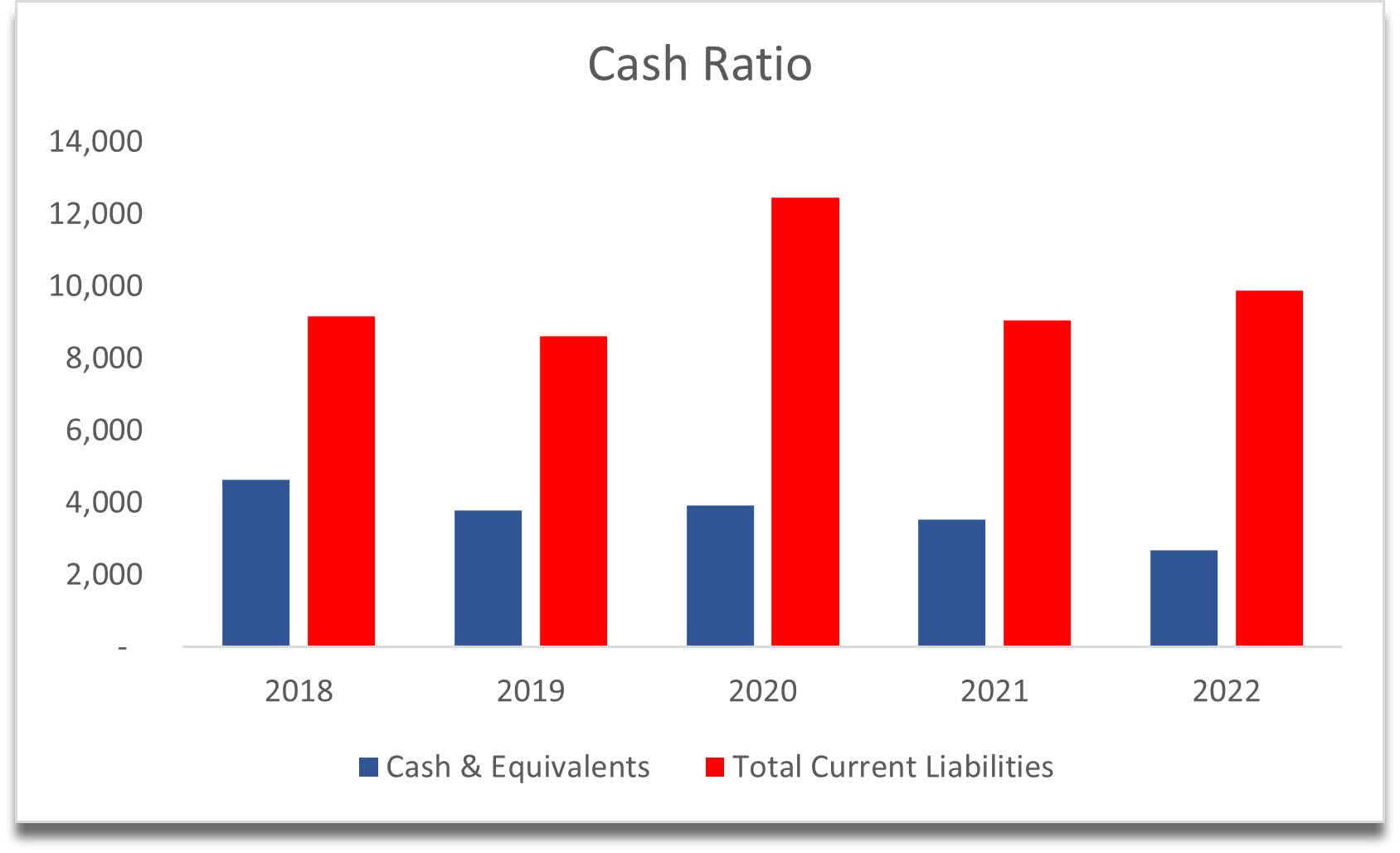

The next thing that is important for my investment is the cash ratio. Here the company gets an X because it cannot cover its current liabilities with cash on hand. That does not mean they would have liquidity problems, but just to be more scrutinizing I always like companies that have plenty of cash on hand to cover their short-term obligations.

{kind=link}

The company's current ratio is acceptable but on the lower end. Companies with a current ratio of 2 are what I like to see, however, Canon's is still sufficient. From the graph below, we can see that the ratio is going down slightly, but let's hope that it is not a trend and that things start to turn around. The company is averaging 1.76 over the last 5 years.

{kind=link}

The debt levels are pretty much non-existent on the latest report. Sitting barely at around 2.4B yen, which amounts to around $18m. I like companies that don't take on excessive debt to run their day-to-day business, but also, I'm not saying that debt is bad, I just prefer companies that have little debt. For example, I did an article on Crocs Inc. ( CROX ) recently and they have quite a bit of debt, however, this kind of debt is not worrisome to me because they are actively paying it down and the acquisition was a smart move.

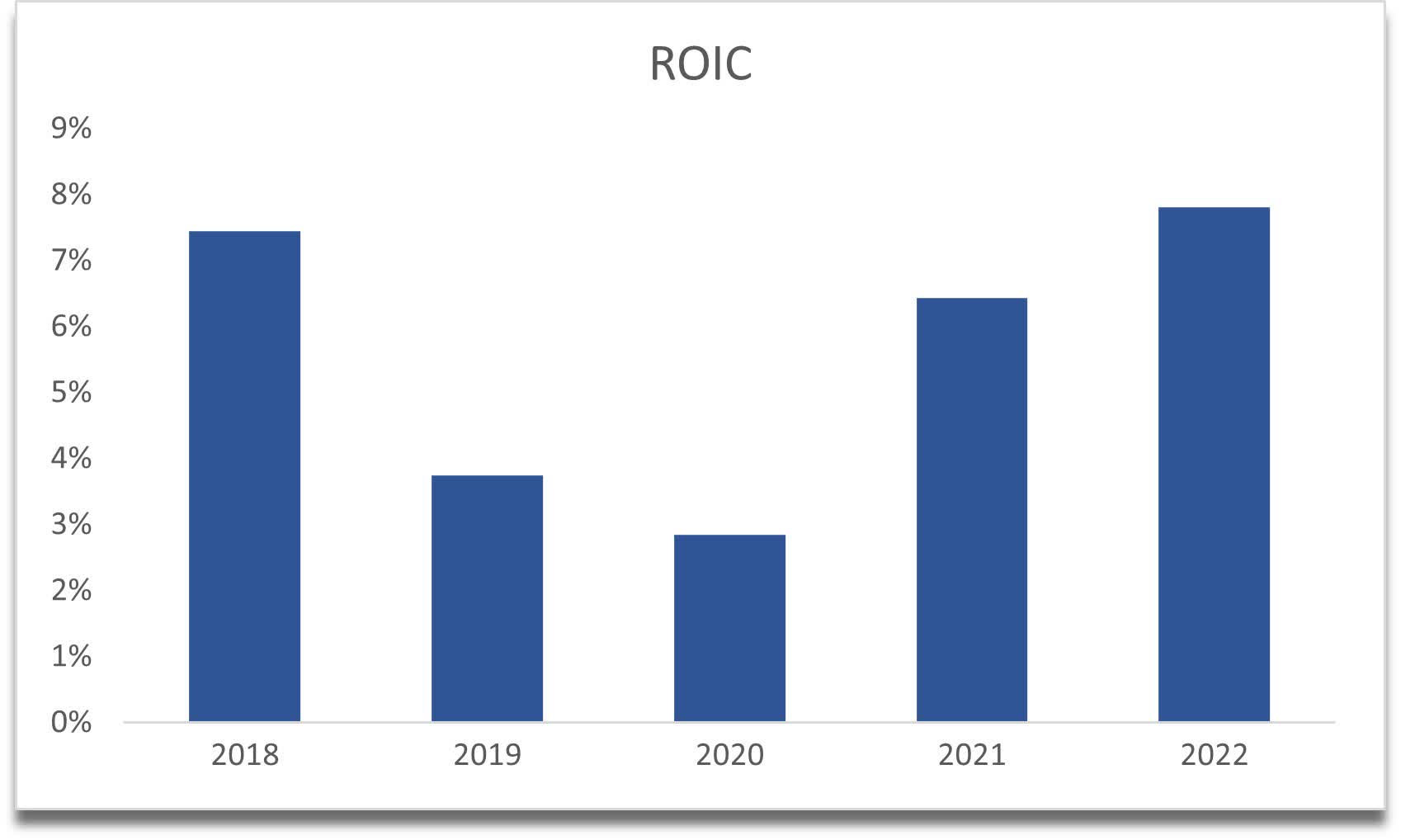

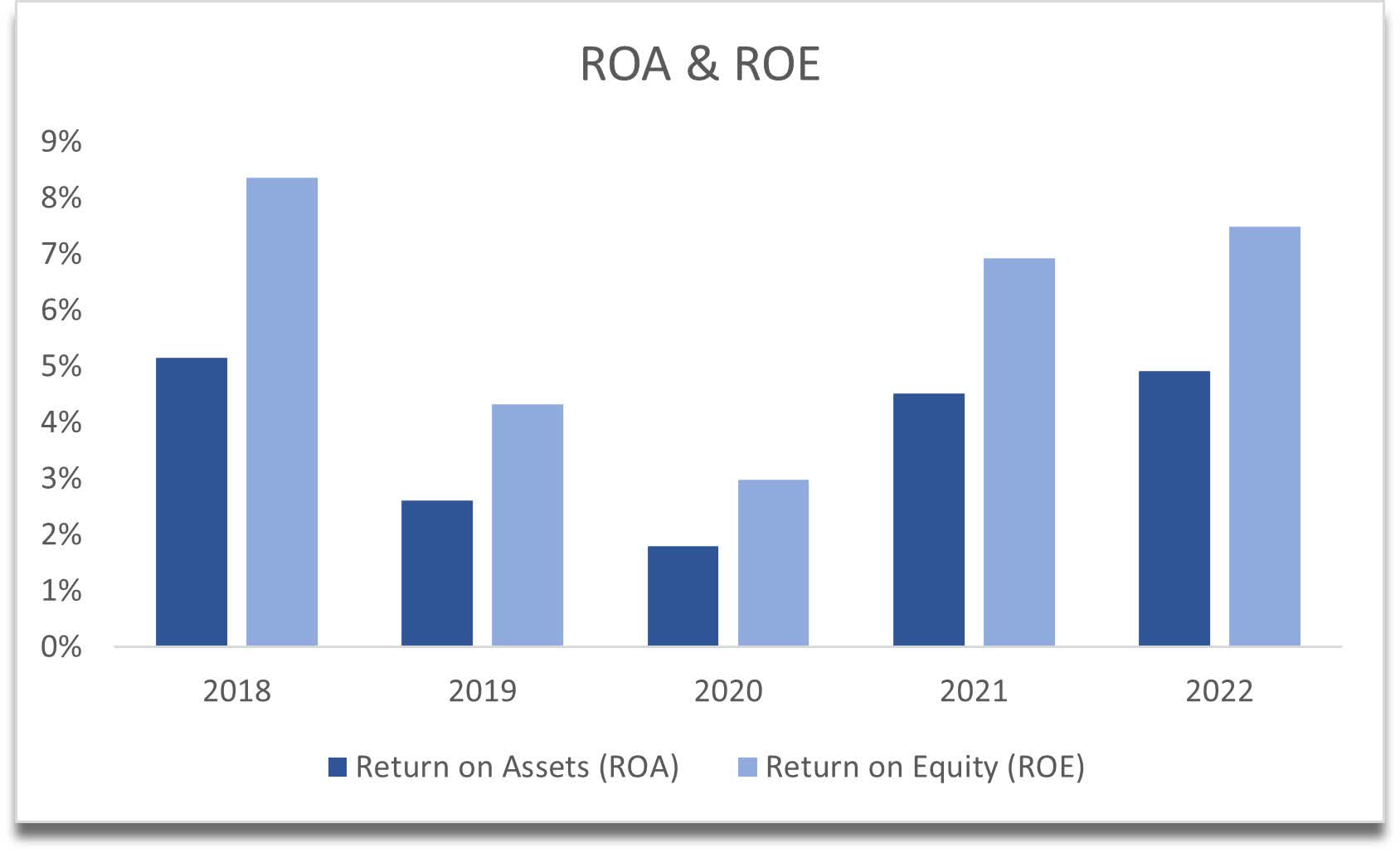

Return on invested capital is a bit of a mixed bag and is a bit lower than what I would normally consider, however, it can be much worse. The same goes for ROA and ROE. With time I would like these metrics to improve as the trends for the last years suggest below.

{kind=link}

{kind=link}

From looking at the above metrics and the whole balance sheet, the company is not doing badly, however, it could perform much better. With increasing growth prospects, I would expect these numbers to improve in the next 5 years.

Valuation

Considering the potential growth prospects, overall great financial results in 2022, and positive outlook, I do not want to be too influenced by all of these and would stick to my conservative growth assumptions. I have gathered all the financial info for the last 10 years in USD instead of JPY as most of the investors here would be trading in this currency. The US Dollar over the last while has appreciated quite a bit against the JPY so revenue growth y-o-y does not translate to the same number in USD. At the beginning of 2022, JPY was worth around 115 per USD, since then USD appreciated by around 15%, which means that those great revenue numbers in JPY (around 15% for the year), basically end up being 0% in USD. USD reached 150 at one point but retreated recently. I assume 2% growth over the next 10 years in USD for revenue growth as I believe since the dollar has already retreated 15% from its peak it may continue and settle down back to where it was a few years back, around the 105 to 110 range.

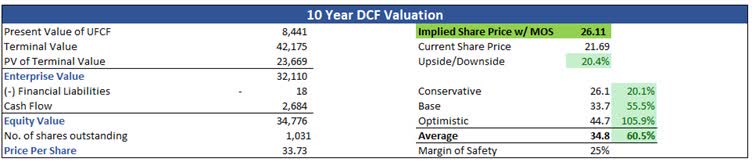

On a more conservative case, I have growth sitting at 1%, and on a more optimistic case, at 3%. I believe these are very conservative numbers, furthermore, to have even security, I added a 25% margin of safety to the final DCF valuation.

After inputting my assumptions into the model and getting a price range for the company, I can conclude that at these levels the company has a 21% upside with an implied share price of 26.11.

{kind=link}

Closing Remarks

With the above financials, growth prospects, and DCF valuation, the company looks attractive at the levels, however, does that mean they are going to reward their shareholders in the future? It is hard to tell, but what the analysis tells me is that it is reasonable to assume that it could. On the other hand, if we go and look at how it has rewarded its shareholders in the past, we can see that there have been better companies to invest in over the same period. With the recent announcement that the company intends to delist its ADR from the NYSE, it could become a bit more cumbersome to trade the stock, however, ADR will still be available on the OTC markets or investors can trade it straight off the Japanese exchange with ticker JP7751.

Returns compared to SPY (Seeking Alpha)

Take the above analysis with a grain of salt, and make sure to do your due diligence when looking into whether you would like to add the company to your portfolio. In my opinion, it is a buy right now from what I can see, and am considering starting a position within the next half a year.

For further details see:

Canon: A Diamond In The Rough Or A Cautionary Tale? A DCF Analysis