CAJFF - Canon Isn't Picture-Perfect

2023-11-04 00:12:43 ET

Summary

- Canon has operational advantages in its printing segment and has a strong global presence in various markets.

- However, the company's financial metrics, including revenue and net margin, are lacking compared to its peers.

- Based on my valuation measures, Canon is currently fairly valued, but my discounted cash flow analysis does not support an investment at its current price.

Canon ( CAJPY ) is a strong company, but it is far from an ideal investment at current valuations and considering past financial performance. There are some significant advantages to Canon that make it a compelling purchase based on operations. However, the company is lacking in competitive growth metrics and falls short on valuation. My analysis outlines why after consideration, I will not be buying shares but would continue to hold them if I already owned them.

Operational Advantages

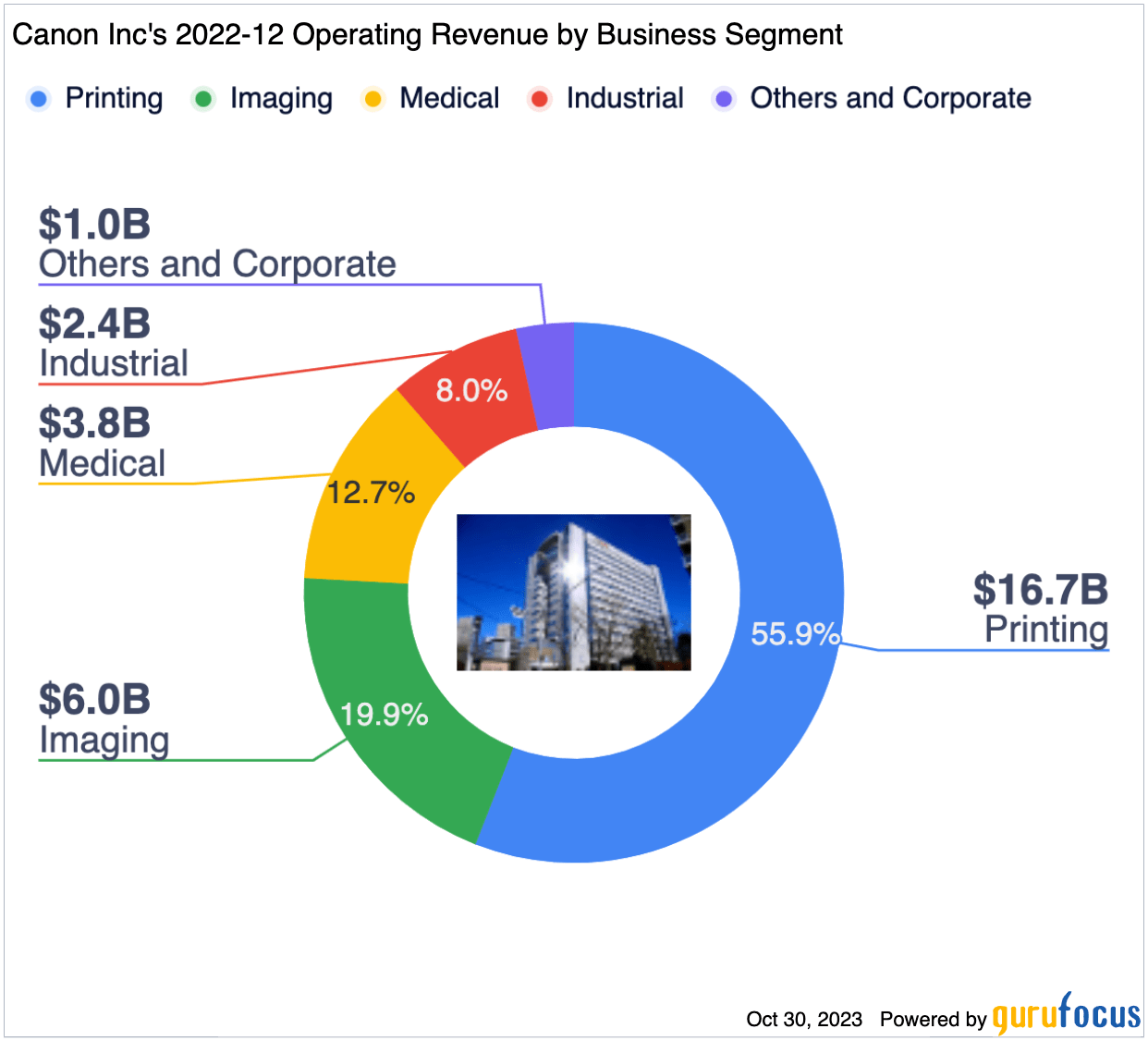

The majority of Canon's revenue comes from printing, but the company also has revenue streams from imaging, medical, industrial, and other segments:

{kind=link}

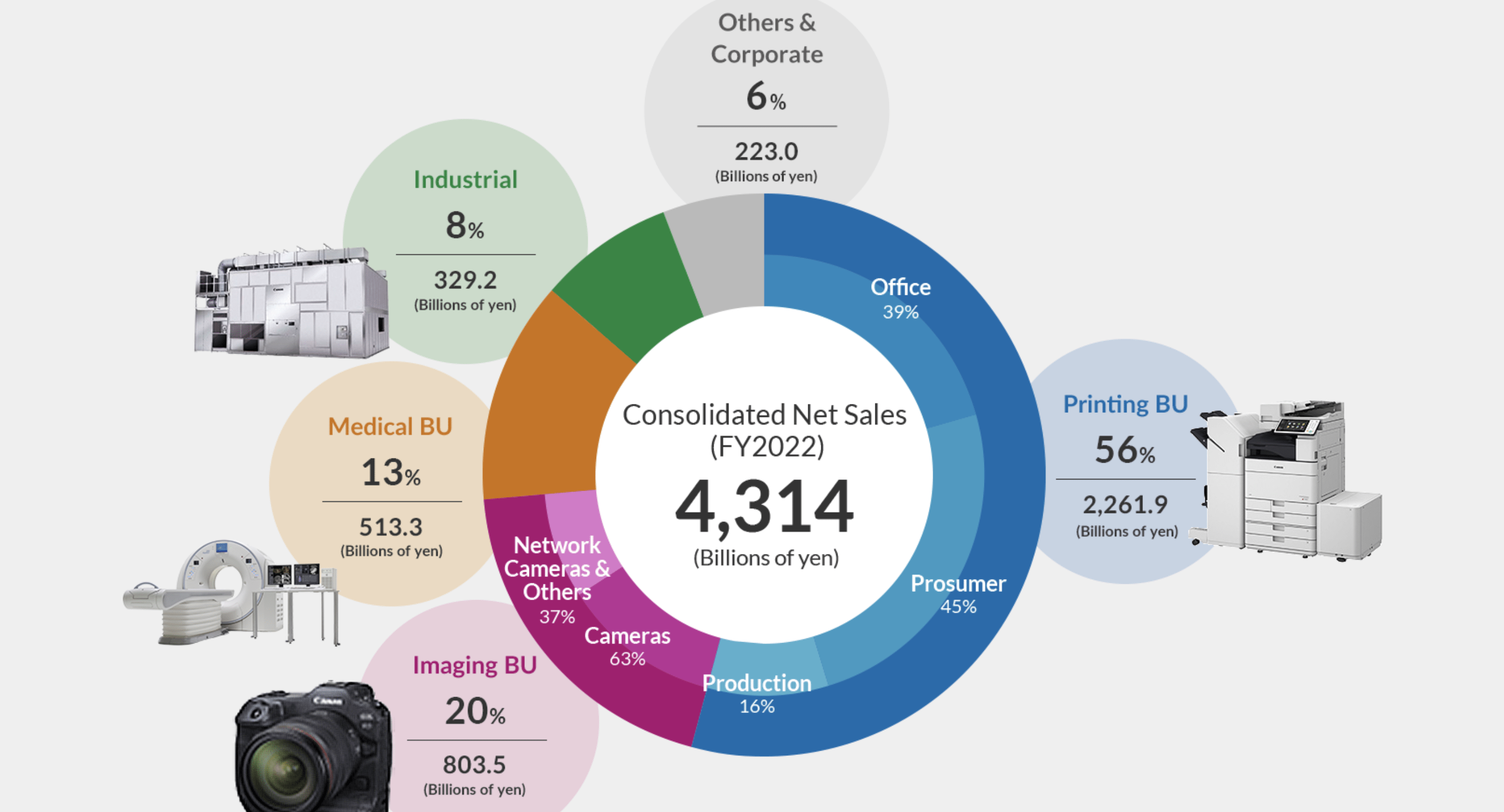

A further breakdown taken from Canon's direct investor relations shows what these business segments consist of on a micro level:

{kind=link}

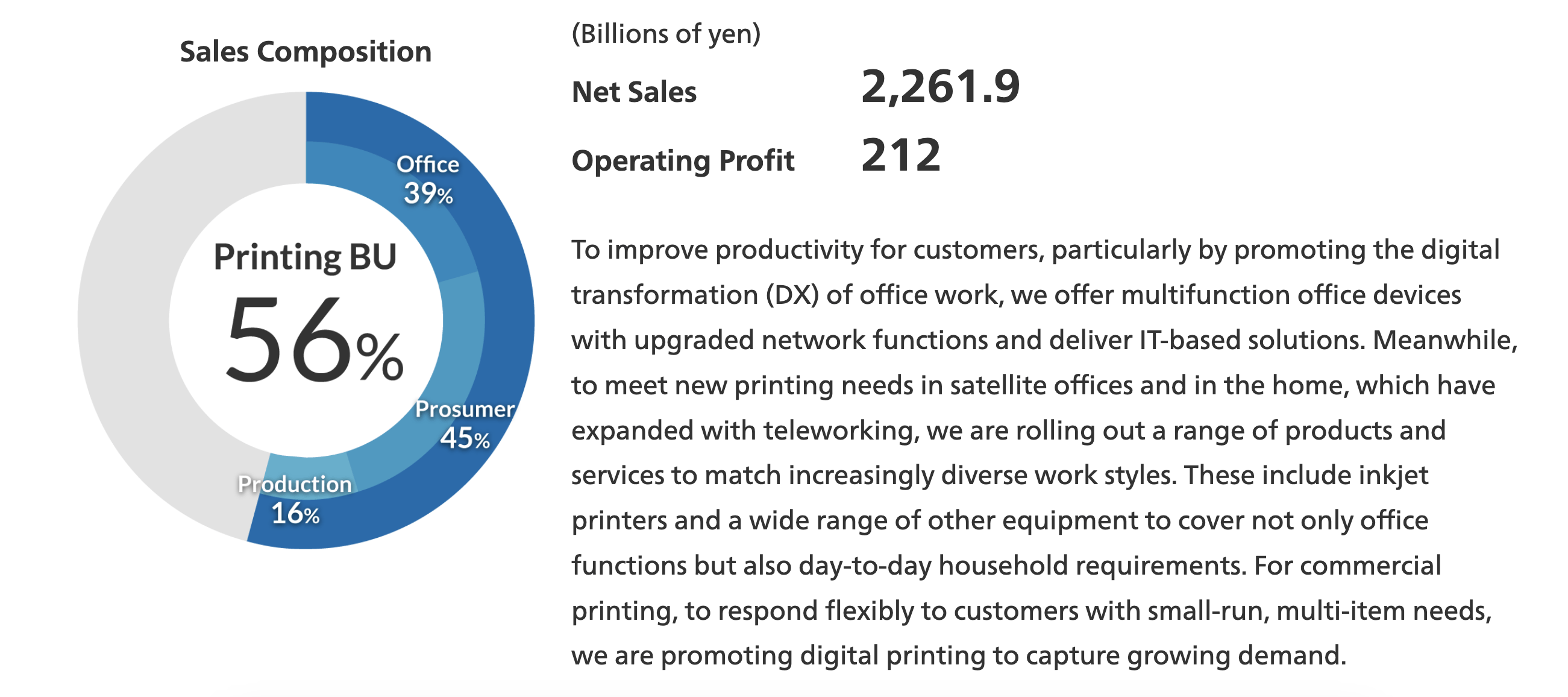

I find it prudent to have a comprehensive understanding of at least a business's largest segment of revenue's mission statement and operational profile, to get a more tangible outlook on what I'm investing in. In the case of Canon's printing segment, what I like is that the products are not 'fads', and in that sense, my investment is hinged on products of real utility.

{kind=link}

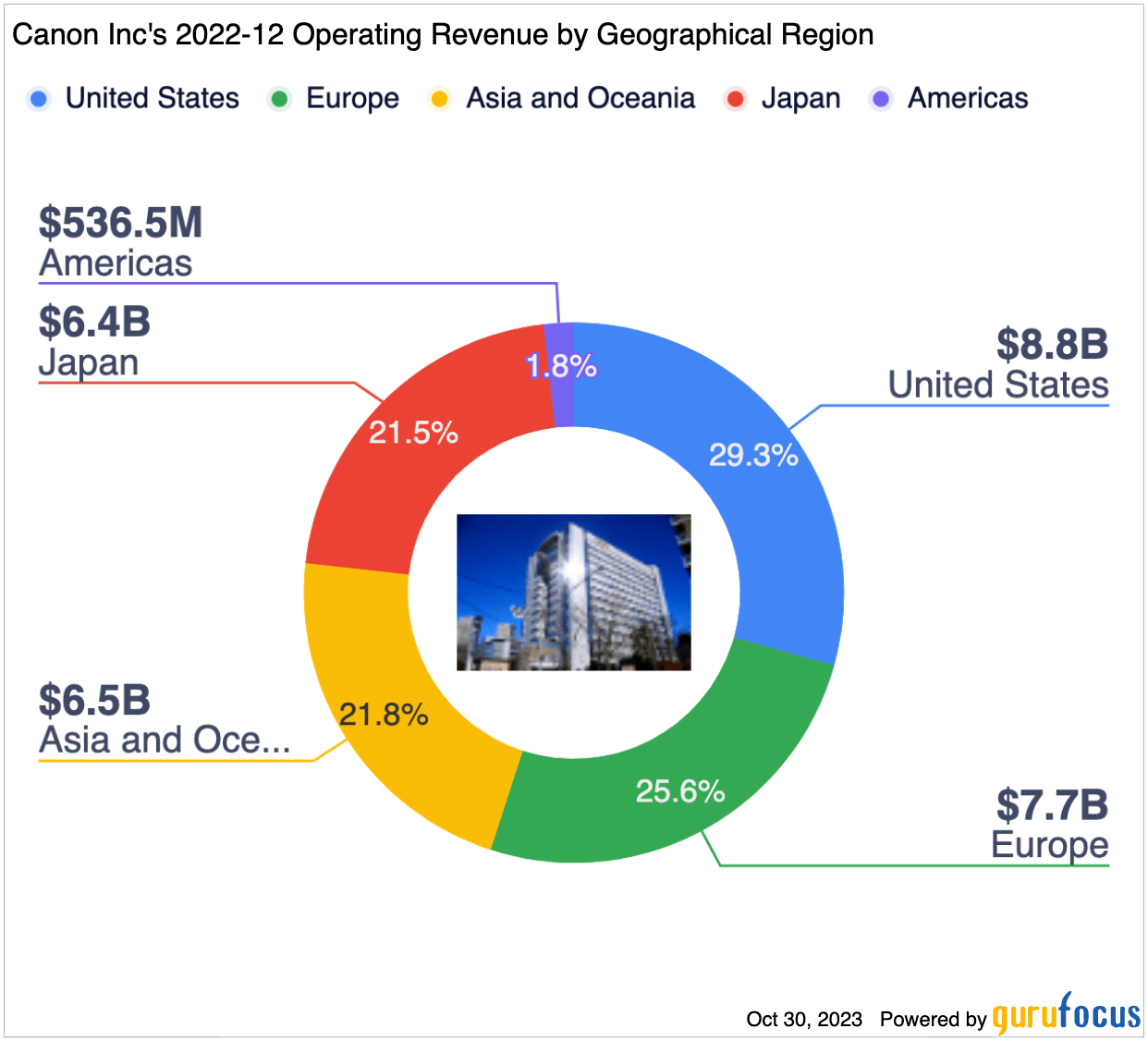

Operating revenue based on geography is also strong, with an entrenched global portfolio of markets:

{kind=link}

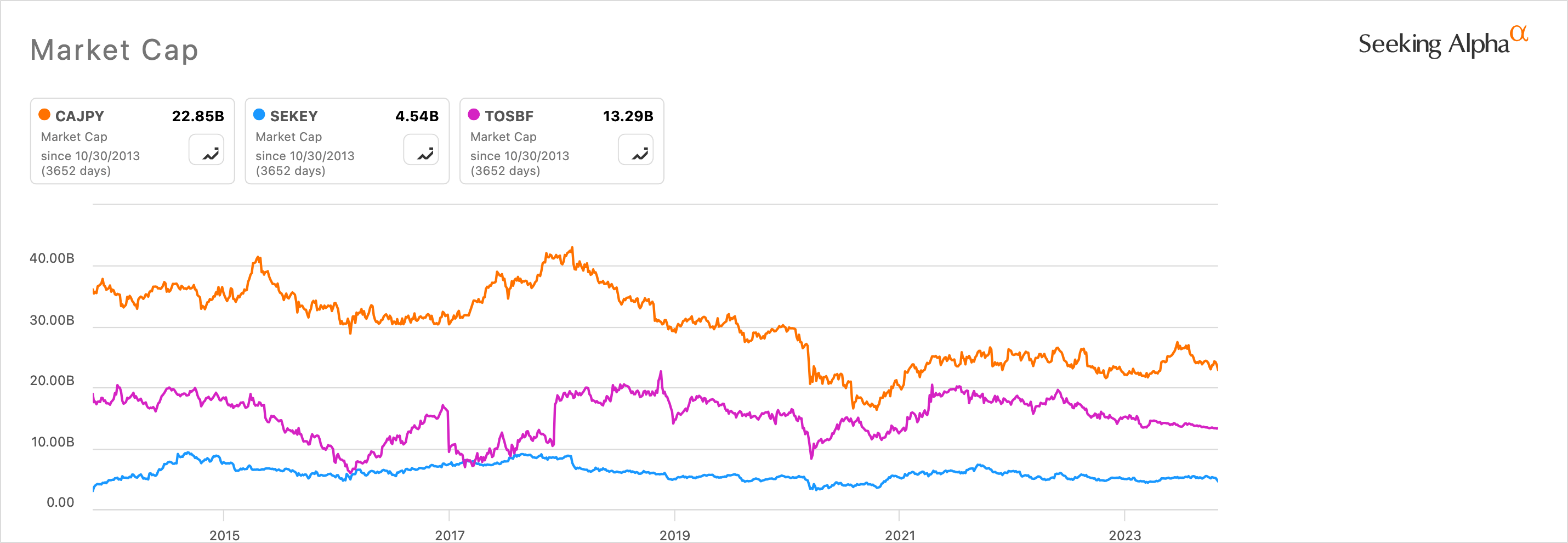

For market dominance analysis purposes, comparing Canon to peers in Japan on market cap presents a favorable competitive profile for Canon:

{kind=link}

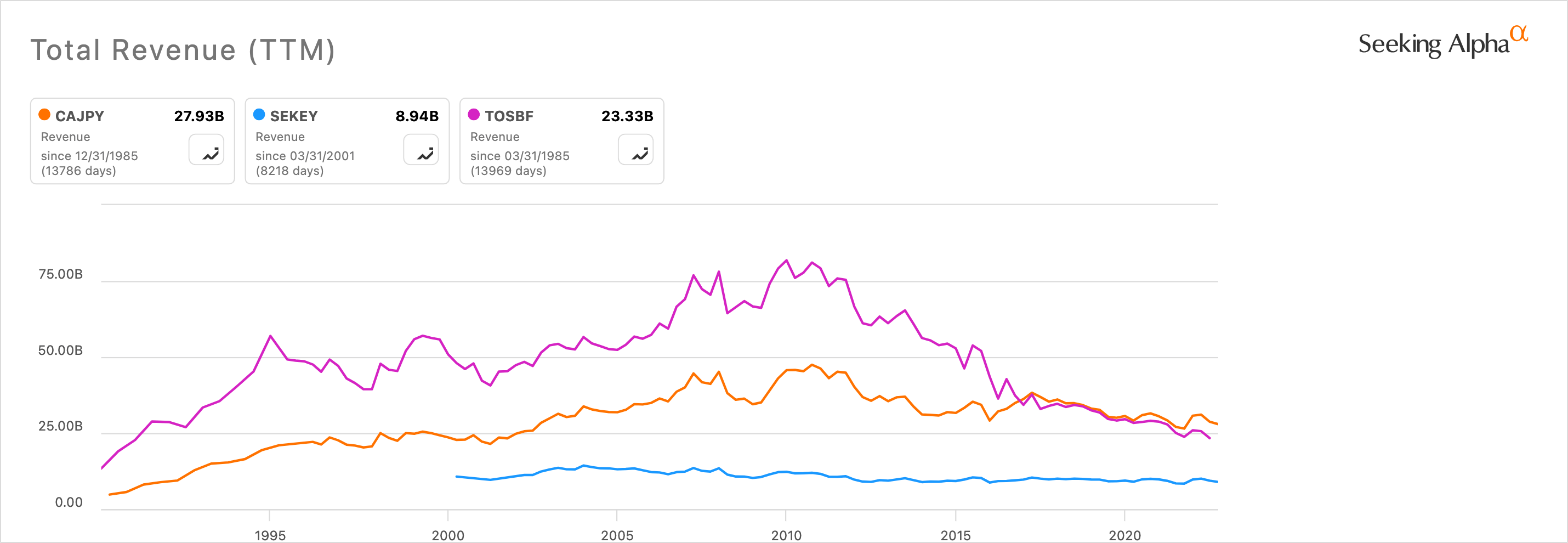

However, to gain a clearer understanding of the current growth prospects of each of the three companies, I've compared them on all-time revenue growth:

{kind=link}

As we can see, the growth story for Canon is not that competitive, which brings me onto a deeper financial analysis concerning Canon's weakest financial components, before discussing key strengths of what is still, generally, a very strong Japanese business.

Growth & Value Concerns

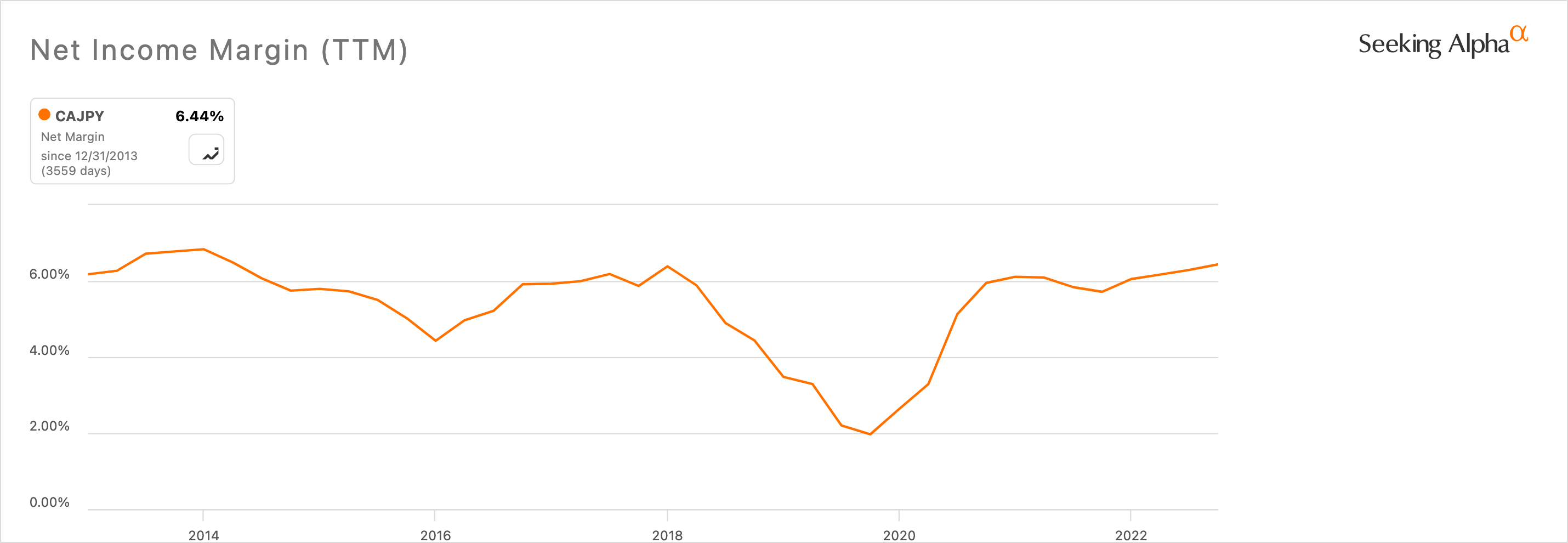

Extrapolating further on Canon's lackluster revenue growth, I'm also stressing margin slowdown. The company does have better net margin historical readings than revenue and gross margins, and I'm going to compare all of them to give Seeking Alpha readers a visual understanding of the slowdown in growth we're looking at across the board.

Using Seeking Alpha's powerful Y Charts tool, here's the 10-year net margin picture:

{kind=link}

As we can see, Canon's net margin situation is less than favorable, with a notable uptick since 2020, but all-over stagnant for 10 years and counting.

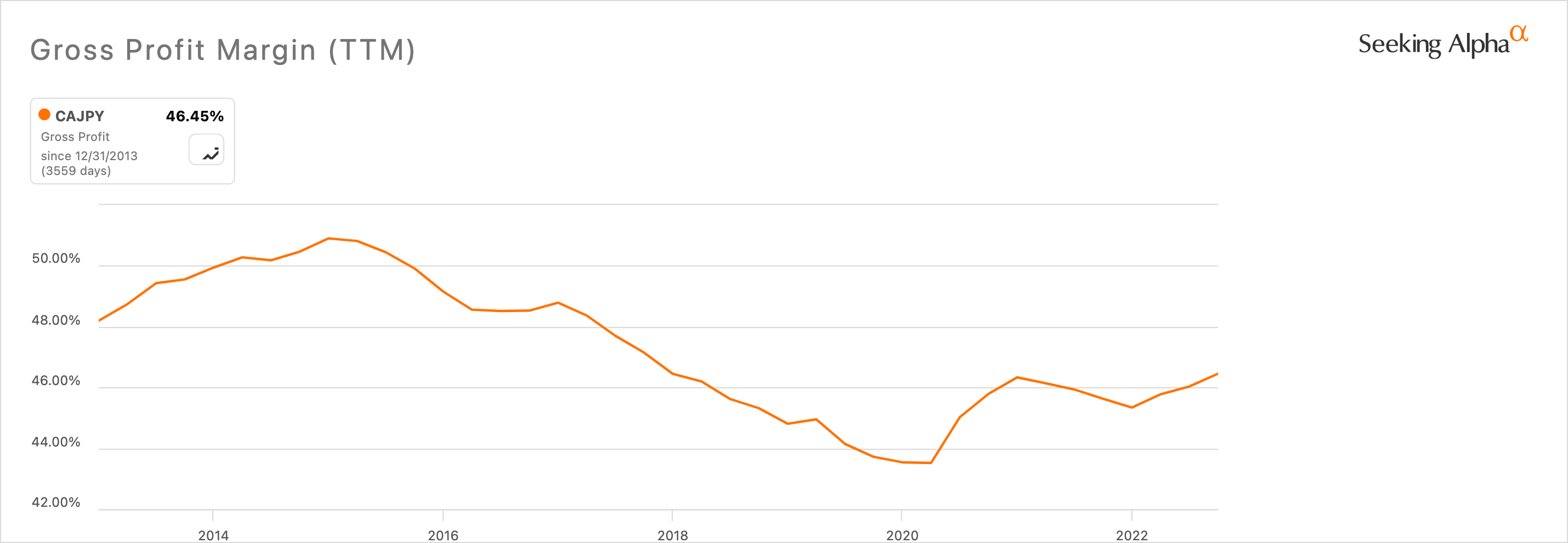

The gross profit margin situation is much worse. That's good news in terms of Canon's internal efficiencies with stress on net margin maintenance even during down-trending gross margins but still paints a negative picture for Canon's growth prospects overall.

{kind=link}

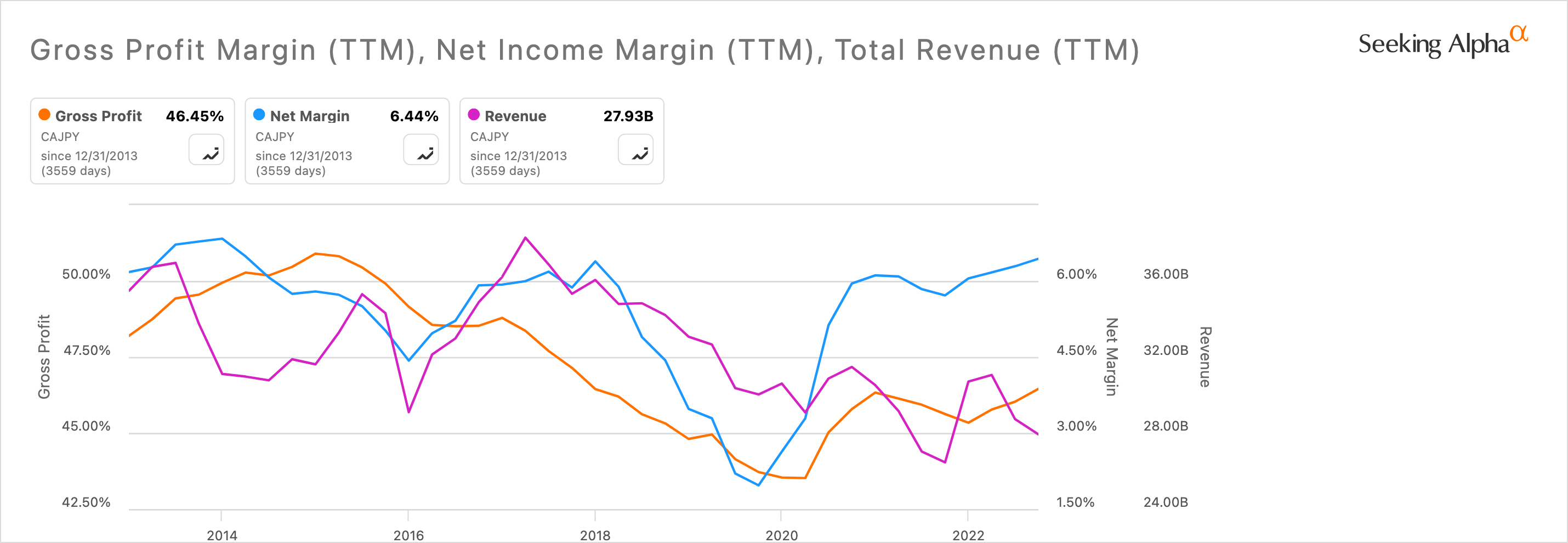

If we compare all three metrics (revenue, net margin, and gross margin) we can get a visual aid to a tripoint growth downtrend.

{kind=link}

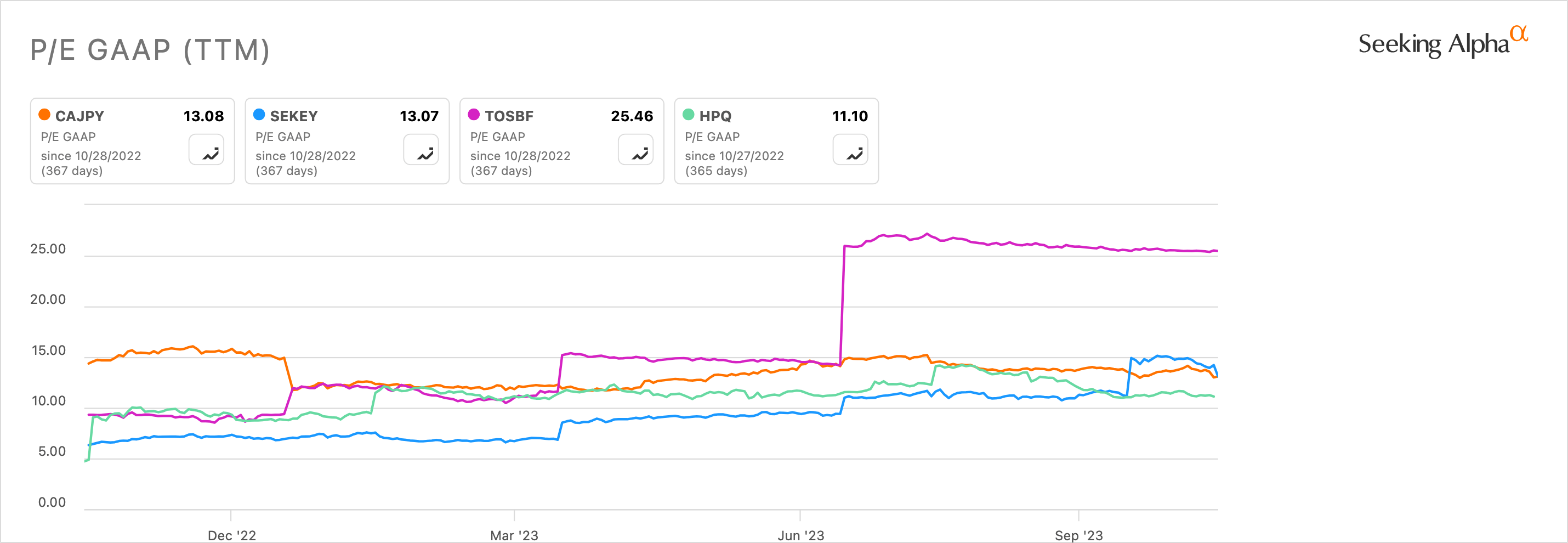

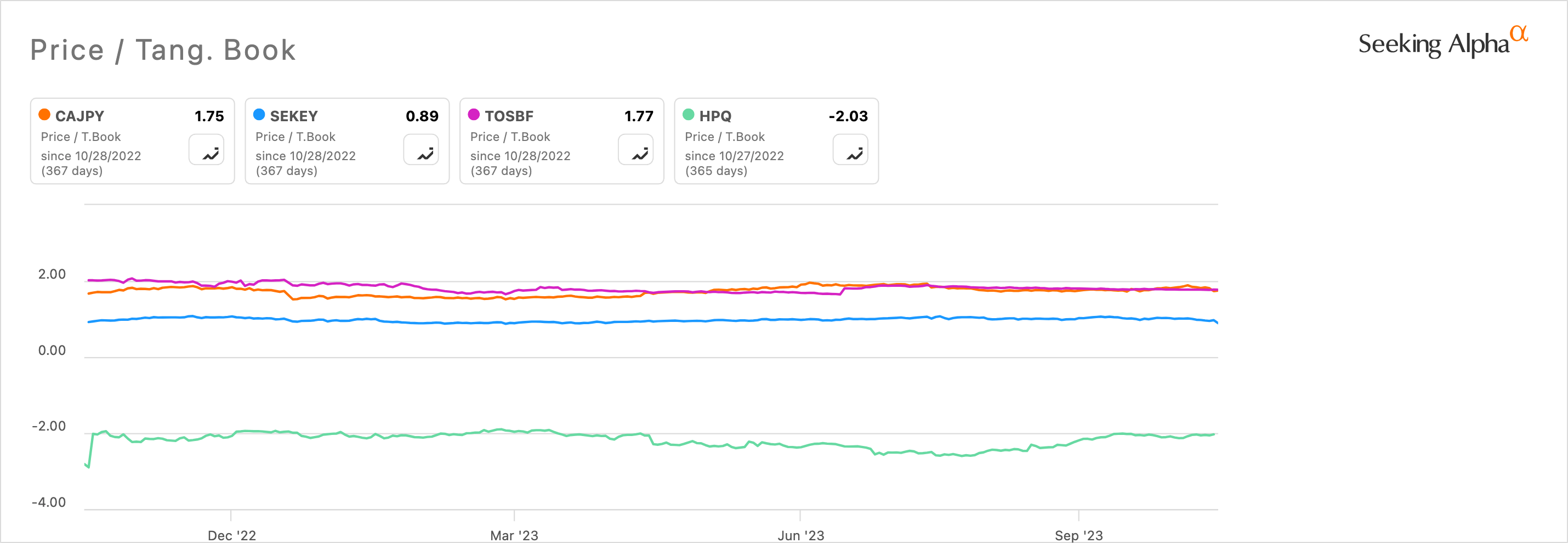

If we look at Canon based on its valuation measures, starting with the price-to-earnings and price-to-tangible-book profile, we can see an average profile for the company when related to peers, now including HP ( HPQ ) for a Western comparison:

{kind=link}

{kind=link}

Given Canon's liability, asset, and cash flow profile, the price-to-tangible-book value provides me with a nice measure of how much I'm paying above intrinsic asset value for the shares. Since Canon doesn't have a strong balance sheet in relation to its industry, I want to make sure I'm not paying too heavily for a company with a low book value, which acts as a nice buffer against any operational deficiencies. In this instance, the price isn't too high. In my opinion, the company seems fairly valued on many measures.

That being said, given Canon's current price, I can't warrant an investment given the discounted cash flow analysis I have computed with a generous 5% 10-year growth stage and a 4% terminal stage, with an 11% discount rate. From my calculation, the generous fair value is $22.11, and the current share price is $23.34, leaving a -5.56% margin of safety on the stock at its current valuation. To me, that isn't compelling enough of a value opportunity to warrant an allocation in my portfolio.

Cash Flow & Balance Sheet Perspectives

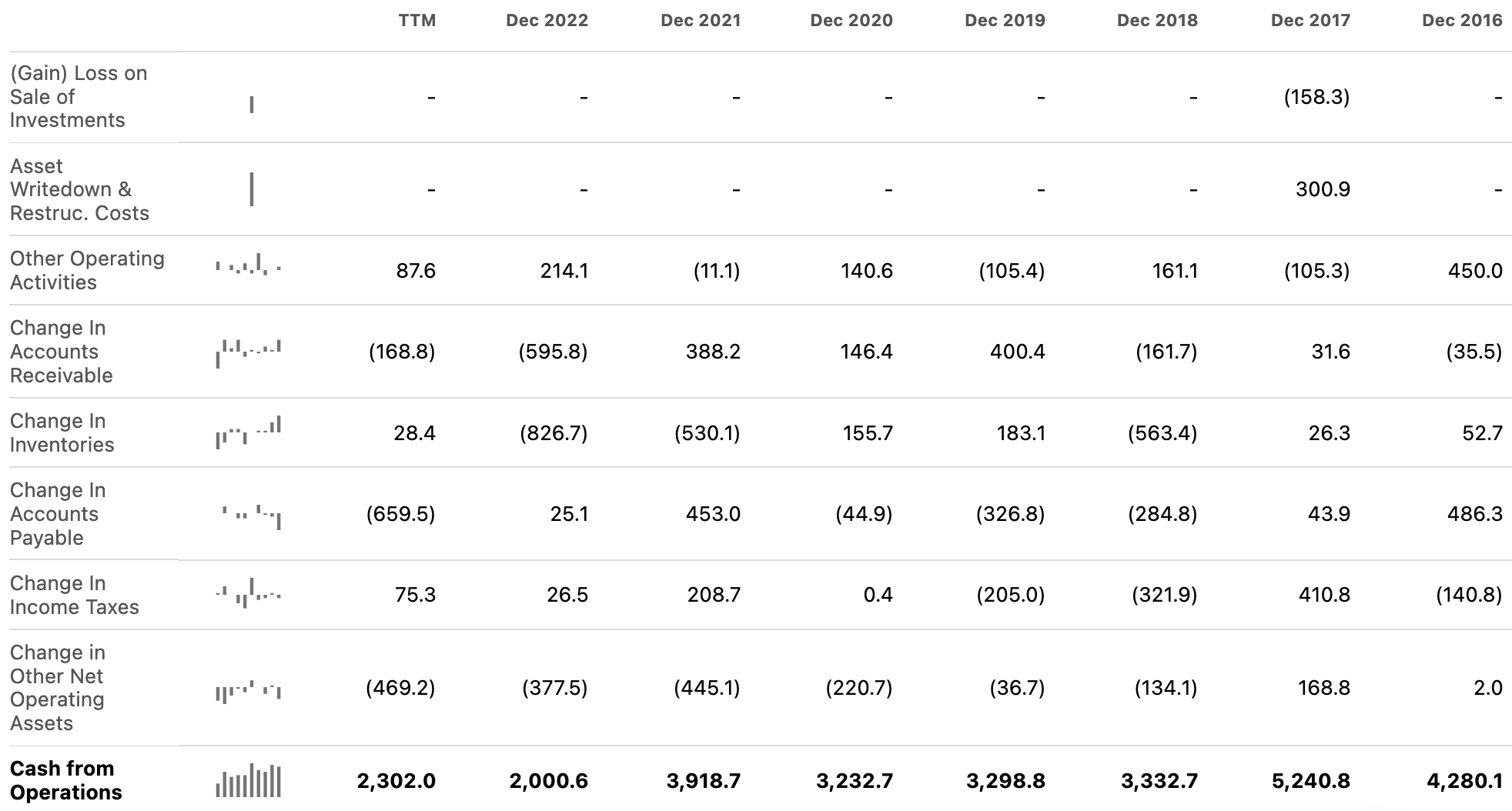

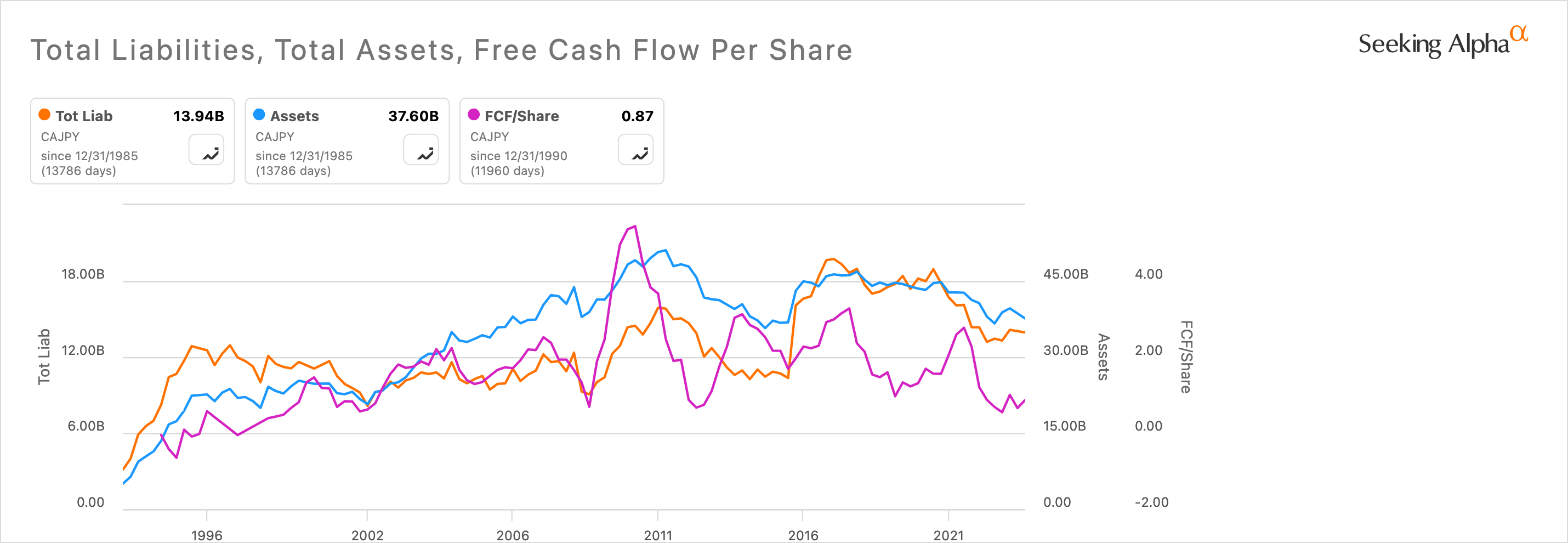

Canon's cash flow from operations has been in significant decline since 2016:

{kind=link}

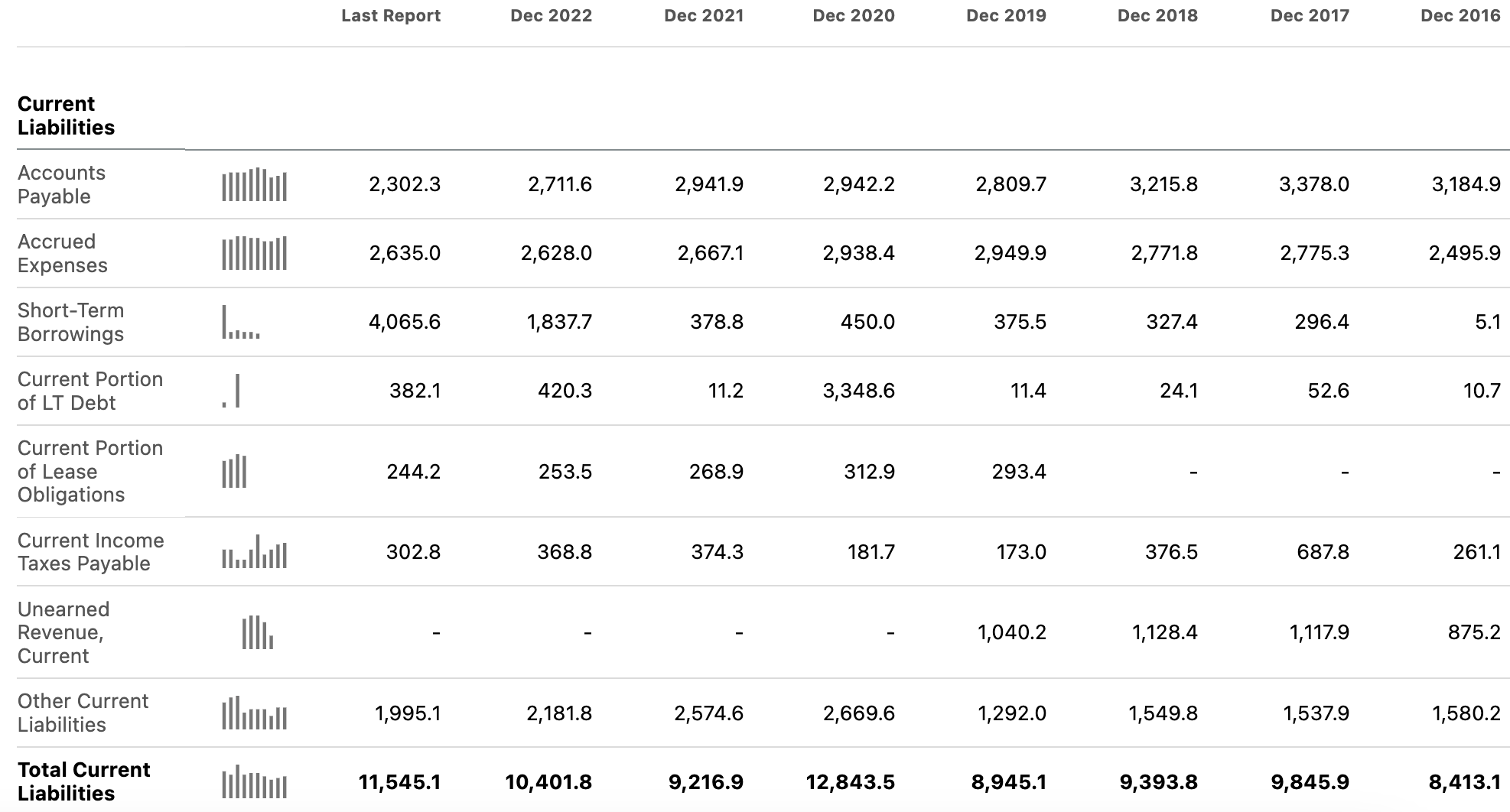

Considering the company's total current liabilities are up significantly over the long term, this presents an additional area of weakness.

{kind=link}

Total assets have seen almost no growth during the same period. As a potential investor in the company, I am concerned by the lack of growth of assets versus total liabilities, especially when compared to the free cash flow per share. Seeking Alpha's Y Charts tool has strengthened my visual understanding of the current cash flow vs. balance sheet situation:

{kind=link}

Overall it isn't bad, but there is certainly room for improvement. My analysis of these parts of Canon's overall financial health continues to reinforce my estimate that an investment in CAJPY would give me relatively stable, but moderate returns.

Let's back up a bit and look at the strengths, because they do exist, and even given the financial shortcomings, I love Canon as a business and believe it has an exceptional portfolio of highly useful products.

Analyst Rating: Hold

I'm making my rating for Canon 'Hold', primarily because although there are better investments out there, the company has seen significant short-term momentum on margins, and that provides me with enough hope to warrant at least a small allocation of a portfolio to a Japanese company like Canon. The investment not only diversifies a heavily Western-weighted portfolio but also creates exposure to a company with strong operations.

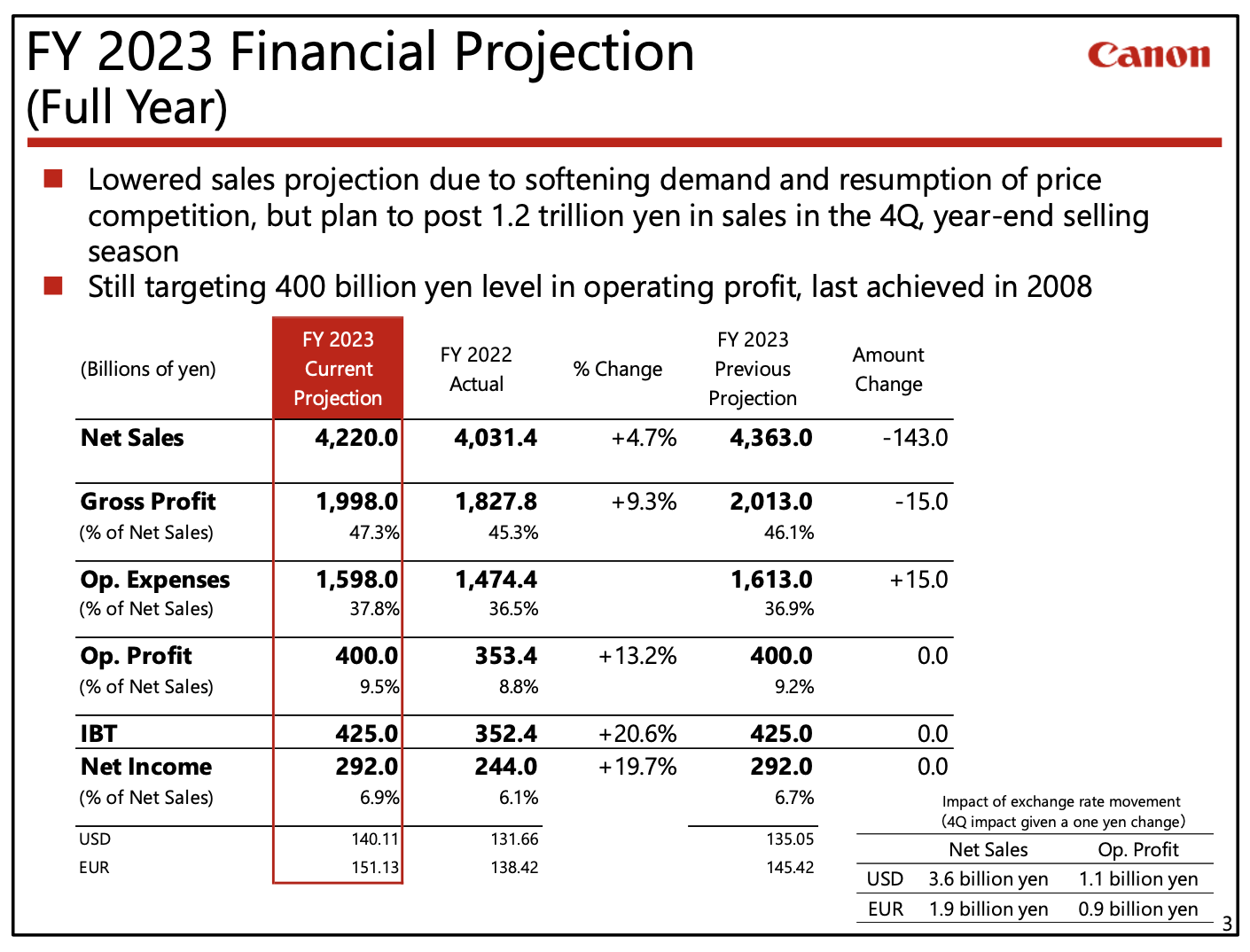

A strong financial projection for the year ahead also bodes well for current investors:

{kind=link}

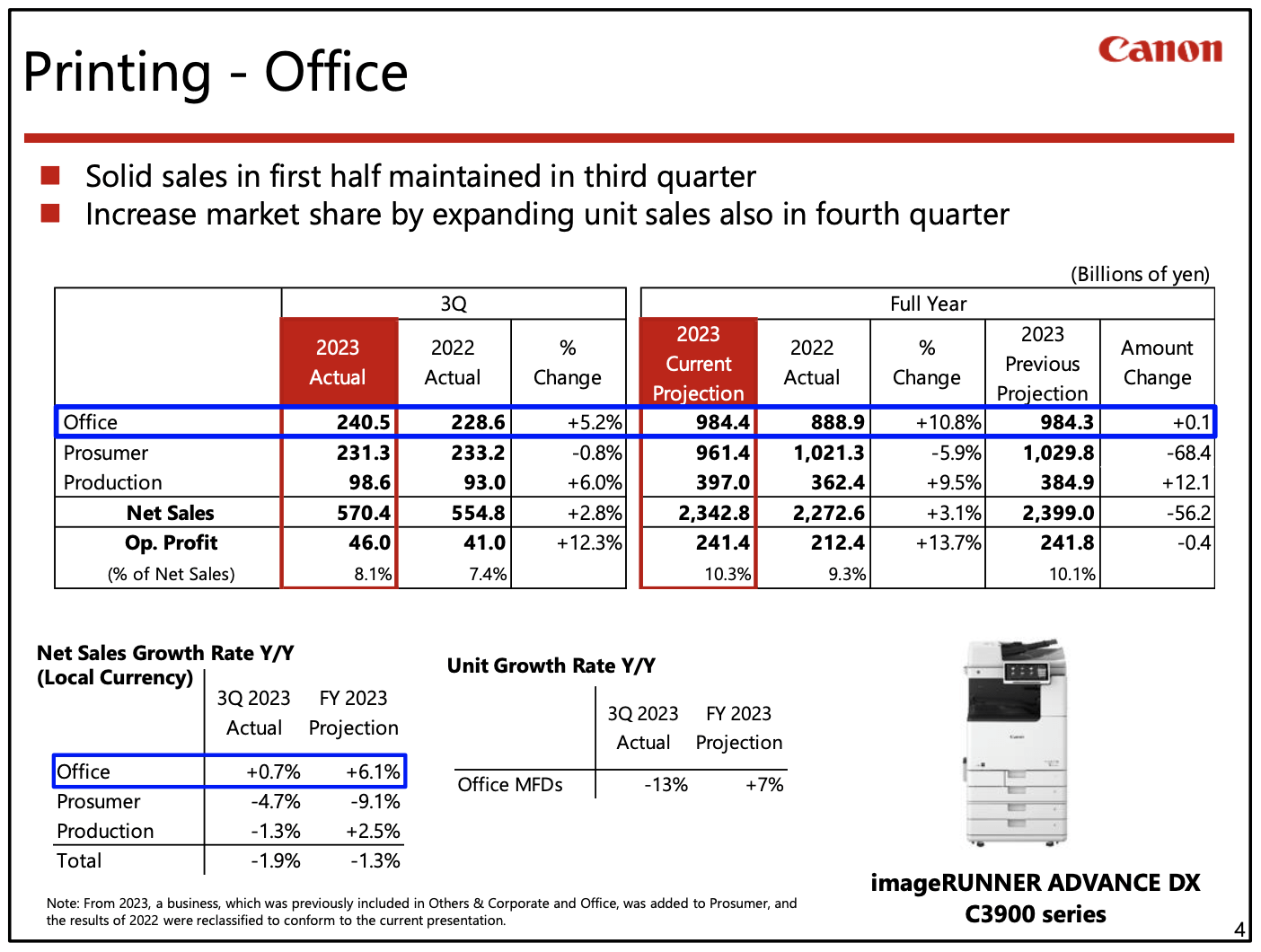

And, again, looking at printing as our core source of revenue and analyzing it on a micro level, here's the recent uptick in printing profits:

{kind=link}

It's worth noting the 'Net Sales Growth Rate Y/Y' in the bottom left corner, which again signifies a slowdown in growth rates for Canon.

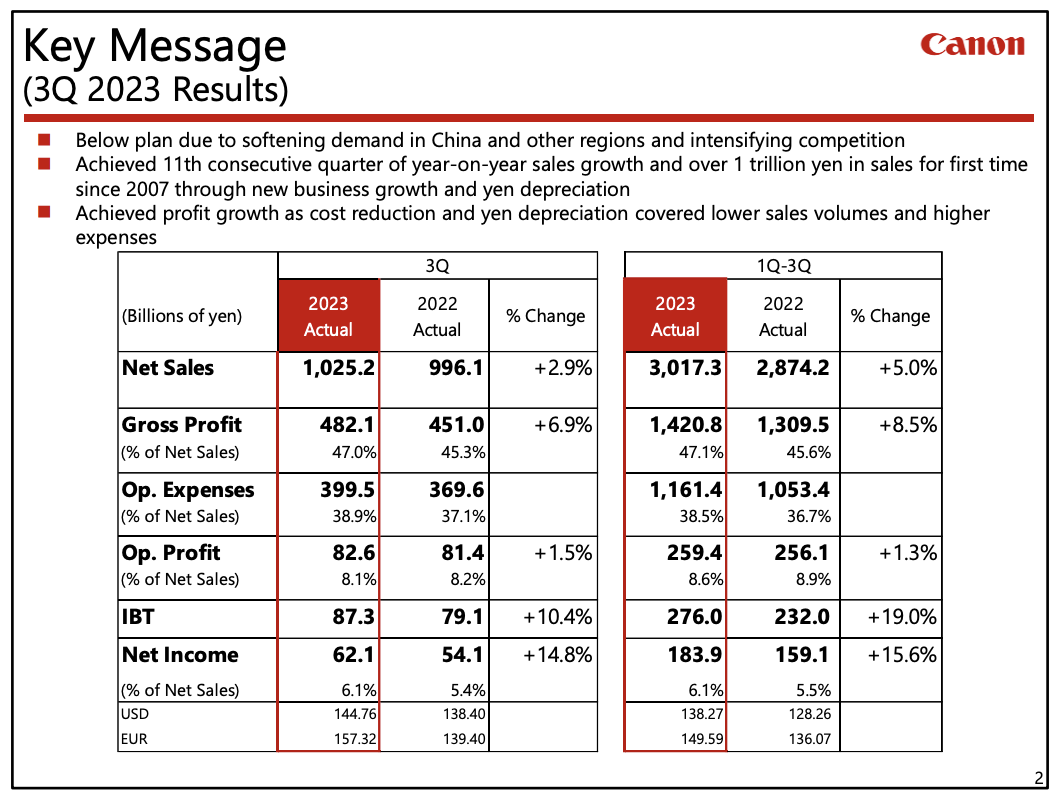

The overall Q3 Results Message from Canon is significantly positive and reminds me that, as mentioned previously, there is hope for a further continued advance of Canon to increase its growth metrics and create higher shareholder returns.

{kind=link}

At present, however, I do not see an investment in Canon as prudently seeking alpha directly. Alternatively, if I were a shareholder, similar to my investment in Mitsui (which I prefer due to its wider industry and global diversification), the investment would act as a hedge against Western downside risk by exposing me more heavily to Asian economies with Japanese headquarters. In essence, that achieves alpha over the index in a very nuanced and carefully weighted manner.

Conclusion

Canon has a strong portfolio of revenue streams both by business segment and geographically. Although I have significant growth concerns for the company and I am not compelled by the current valuation, I posit that there is hope considering recent financial results. A strong argument can be made for holding Canon as a geographic hedge against Western downside risk. However, I still believe my investment in Mitsui is a stronger way to achieve this.

For further details see:

Canon Isn't Picture-Perfect