CAJFF - Canon: The Next ASML?

2023-05-31 06:49:45 ET

Summary

- Canon's stock has been a terrible underperformer, with negative returns over the past decade.

- Despite that, the company has a good balance sheet, consistent profits, and a safe dividend.

- It has a safe leadership position in its markets, but more crucially, it could be about to take on ASML, which would propel its stock multiples higher.

Most articles on Seeking Alpha focus on discussing a given company's business and how it affects the stock. This article however will focus on a business Canon ( OTCPK:CAJPY ) doesn't have; EUV machines manufacturing.

Extreme Ultraviolet (or EUV for short) is a lithography technology pioneered by ASML ( ASML ). It took 17 years and 6 billion Euros of R&D to develop, and now it is the way to manufacture the most advanced chips in the world. As semiconductor chips became smaller and smaller, manufacturers found it more challenging to pattern the details of the chip. ASML's EUV allows semiconductor manufacturers to create those patterns accurately and at massive scale on tiny chips (less than 10 nanometers). There isn't really another way to manufacture 7 nanometer-chips right now and ASML is the only company capable of producing EUV machines, due to the technological know-how required and the unavailability of crucial inputs like the light source required for the machine to work anywhere else (ASML bought a company called Cymer in 2013 to secure that light source). Canon's own lithography business struggled, as did Intel's ( INTC ) whose competitive position seems to hinge on its ability to get EUV machines , as ASML completely dominated the market. But as capitalism taught us time and time again, if you develop a high margin business, competition is going to come. And Canon's management seem to suggest they might have found the answer to EUV.

Canon Nanotechnologies Inc.

Photolithography is the standard for manufacturing semiconductor chips. It essentially involves the use of light to create the patterns on a given chip. This is true for all kinds of chips, whether CPUs, GPUs, memory, or logic. And as those chips get smaller and smaller, fabs will have to rely on EUV machines as it's the only one capable of mass-producing the patterning of chips below 10 nanometers.

All legacy lithography manufacturers (like Canon and Nikon) have been looking for ways to catch up to ASML, and in some cases just be part of the EUV supply chain by selling components for the EUV machines .

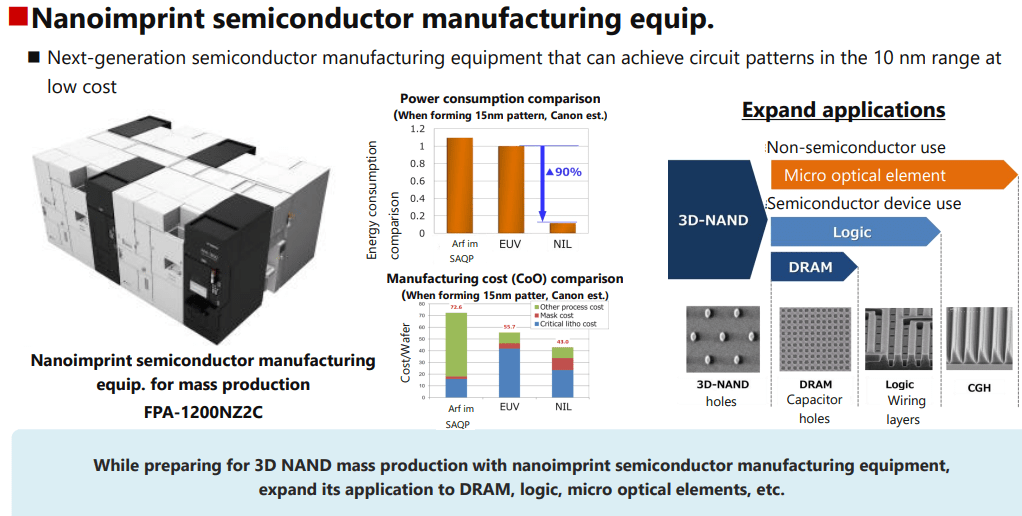

Nanoimprint lithography (NIL) has been a promising alternative to photolithography in general. Its real challenge was getting it to be fit for mass production. While it had the ability to create the patterns on really tiny chips (similar to EUV), it generated a lot of defects. One way to simplify the difference between EUV and nanoimprint lithography is that the former "drew" the pattern on the chip layer using light, while the latter stamps the pattern on the chip layer. That element of physically touching the layer with the stamp causes it to sometimes be misaligned. This is a gross oversimplification of the process but it is sufficient to highlight the difference between the two processes for investors. The real advantage nanoimprint lithography has over EUV is that it is much cheaper and consumes much less energy, almost a tenth of the cost. In addition to being a much simpler process to execute.

There were other challenges, but Canon recently announced that they will be able to ship NIL machines to customers for mass production by 2025.

We already have a product ready and are now making adjustments to address customer requests. Demand for this product is expected to be high as a large reduction in cost can be expected compared with conventional lithography equipment, and we expect to reach a certain level of sales volume in 2025.

That was from a Q&A session with analysts in July of last year.

You can read more about Canon's process and how it made the technology ready for mass production here .

Canon added a bit more details its recent corporate strategy conference two months ago on the features and plans for the unit.

Early signs suggest NIL will not be able to disrupt EUV, but it might stand a chance to disrupt DUV (which is a bigger market in terms of units) if Canon can show that to potential customers.

Canon to ship NIL machines 2025 (Canon)

{kind=link}

What Nano Imprint Lithography Could Mean for Canon's Business, Stock

The company's industrial business unit, which includes its semiconductor equipment sales, generated $2.5 billion in revenue in 2022. The dollar figure was obtained by dividing the yen figure by the 131.66 average exchange rate provided by management in this document . That is a small fraction of the company's total sales of approximately $31 billion in 2022. Management also projects $2.7 billion of sales for the industrial unit in 2023.

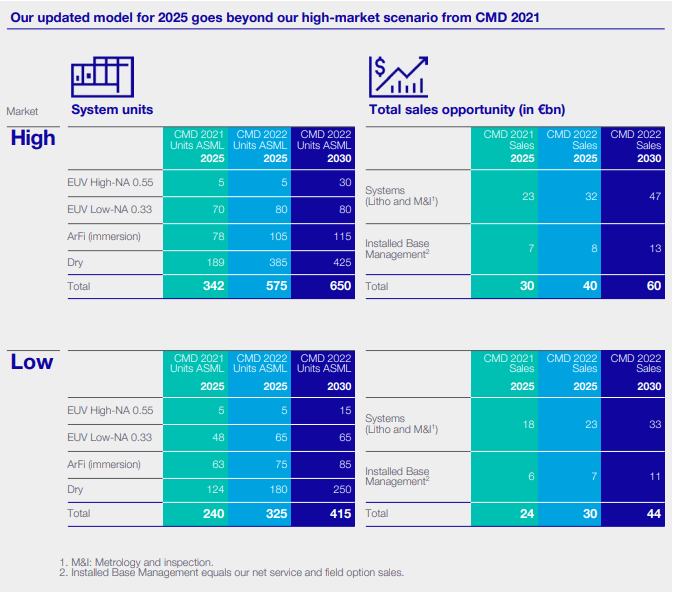

That is a fraction of what ASML generated in 2022 at 21.2 billion Euros in sales (roughly 22.7 billion in USD ). By 2025, ASML's management expects to generate 30-40 billion Euros in sales.

ASML's 2025, 2030 projections (ASML)

{kind=link}

They are also expanding their production of semiconductor machines like Canon. Here is a quote from ASML's annual report :

Cranes stand across the skylines of our sites as our investment to increase our manufacturing capacity to 90 EUV 0.33 NA and 600 DUV systems by 2025-2026 begins to take shape, while we are also ramping our EUV 0.55 NA (High-NA) capacity to 20 systems by 2027-2028. And key partners such as Carl Zeiss are also busy adding capacity, doing everything they can to free the logjam in the supply chain.

There are two takeaways from this quote: 1) ASML is in a much stronger competitive position than Canon, and is unlikely to let up. 2) ASML management expects the demand for its products and the shortage in chips to continue in the medium to long-term.

And so an investor might ask, why invest in Canon at all? The answer is that Canon is a business that offers investors option value. Author of Expectations Investing: Reading Stock Prices for Better Returns Michael Mauboussin believes such businesses offer a lot of upside for investors :

There are certain businesses that have option value. An option is the right but not the obligation to do that. If there are market leaders in uncertain markets with smart management teams and access to capital, they may be able to see opportunities as they present themselves and take advantage of them... from an investor's point of view, you want to have that potential for option value without paying for it.

This is the case with Canon. NIL represent an opportunity that is not appreciated by investors. But luckily it doesn't matter that much as they are a leader in their imaging and printing businesses that are quite stable and continue to grow steadily. There was fear that work from home would mean less office equipment sales for the company, which ended up being true, but they benefited from work from home because it turned out people needed to upgrade the home office to fit their new work needs. Their medical business is also growing double digits. Add to that renewed focus on shareholder return, and investors buying the stock can receive a dividend of 3.5% a year, plus the embedded option of their nanoimprint lithography business taking share from ASML or more likely Nikon.

Here is a quote about financial returns from the management's corporate strategy event :

We plan to increase free cash flow to repay debt, return to debt-free management, and actively invest for growth while maintaining disciplined. Accordingly, over the next 3 years, we plan to invest about 240 billion yen every year. We will not only make capital investments in growth areas such as semiconductor production equipment and Medical, and the new businesses of Imaging, but also in other areas like IT services. And together with R&D, we plan to strengthen and expand each business group. Additionally, we will engage in M&A activity when there is a good candidate that complements and strengthens our business portfolio.

So the company will continue to focus on growing all business units and 2022 results showed that growth, meaning investors don't have to fear the company is a melting ice cube. Management said they plan to keep the dividend payout ratio to as much as 50%, meaning dividends can grow over time.

The company's balance sheet is also strong and highly liquid, with $17 billion in current assets and $14.4 billion in total liabilities.

Then comes the potential bonus from the nanoimprint lithography business. It does not really compete with ASML's EUV machines, but Canon's management believe it offers an upside to using DUV. If the shortage persists like ASML management seem to suggest in their annual report, desperate customers might look to try this new technology, which could lead to Canon taking at least some of that 40 billion Euros of additional revenue ASML expects to generate by 2030. If they can't, 3.5% dividend yield that grows wouldn't be the worst thing in the world.

Just to highlight the opportunity for Canon if they take any sort of share in the DUV market. Even though the Japanese company's revenue is about a third higher than that of ASML for the year ending Dec. 31 of 2022, it has a market cap of $25 billion, compared to ASML's $285 billion as of the close of May 26. So each dollar of revenue that Canon can take in the lithography machines market can have huge implications for its market cap. Canon's stock had negative returns over the past decade, but the recent investments the company has made, particularly in the semiconductor business, could be a precursor for change

Risks

Almost 64% of the company's current assets are inventories and receivables. This could leave the company in a bit of a tight spot in the case of a recession, as its current liabilities would significantly larger than its current assets and will require management to manage their working capital efficiently. They might not be able to pay a dividend during a potentially severe recession.

Additionally, while Canon is investing to improve its position in the DUV business, so is ASML. The latter has better resources and is already technologically ahead of Canon. The more likely scenario, barring some regulatory or political intervention, is that ASML would extend its technological lead over Canon. That would undermine the attractiveness of the option value embedded in Canon's semiconductor business.

Summary

Canon's commercialization of the Nanoimprint Technology is currently underappreciated by the market. While it seems unlikely to disrupt EUV machines, it could replace some DUV machines if they continue to be in short supply in the medium to long-term. Canon's solid competitive position in its main businesses like printing, imaging, and medical devices, means any share they take in semiconductor machines could rocket the stock higher. The company has a decent balance sheet with a nice dividend yield of 3.5% that could grow. However a sharp recession might put the company's balance sheet under pressure.

For growth investors, ASML is probably a better option. But for value investors who prefer the lack of stability, Canon will offer decent returns with potential for blockbuster ones if NIL takes off.

For further details see:

Canon: The Next ASML?