CAJFF - Canon: Why It Might Be Time To Leave It Behind (Rating Downgrade)

2024-01-17 07:58:03 ET

Summary

- Canon's market outperformance has been limited, and its valuation is no longer sustainable.

- The company has achieved consecutive quarters of top-line growth and cost reduction, but its profitability is not as strong as it once was.

- Canon's debt ratio is low, but its gross and operating margins have declined. The company's valuation is stretched, and its upside is limited.

Dear readers/followers,

The time has come to update Canon (CAJPY), one of my more successful Japanese investments over the past few years. I invested in the company when it was undervalued, and my returns on this investment have been positive. In fact, in a funny coincidence in terms of timing, I managed to almost perfectly pick out the period of time when the company was at its lowest with my last article. Take a look at the RoR since.

Seeking Alpha RoR (Seeking Alpha)

As you can see, market outperformance for this company has not been a thing, unfortunately. But we have a higher valuation at this time, and given that it's been almost 3 months since I covered Canon, and we have a different valuation, it's time to update this company's thesis.

You can find the article on this company here, in terms of my latest work. My thesis at the time was expecting outperformance based on further profit increases but with more and more headwinds from softening demand and markets, as well as increased competition for some of its products.

Canon is a great investment at a certain price - though not at any price, and I believe we're reaching price levels where this is no longer sustainable.

Let's look at an update for Canon.

Canon - Looking at the upside after a double-digit performance

So, this isn't a sign that I'm going to sell my shares straight away. Despite these ongoing challenges, the company expects a growing operating profit level with continued growth.

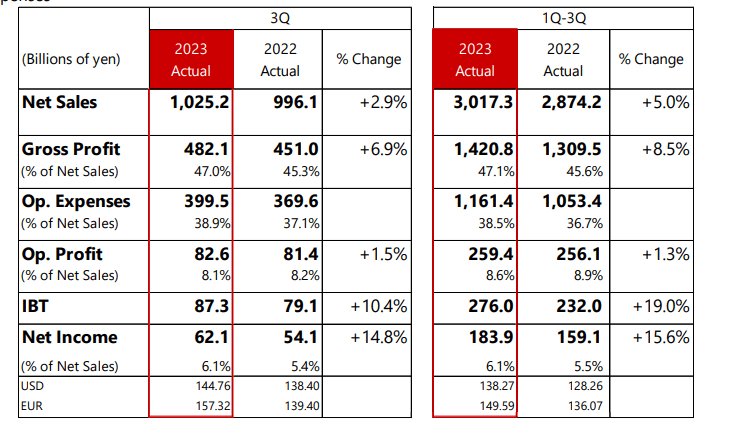

However, it seems that there are a bit more headwinds here. The company achieved the 11th consecutive quarter of top-line growth, through both new business growth and some depreciation in the Yen - positive Japanese FX. The company also managed a fair bit of overall cost reduction, further enhancing returns here.

At this point, it's a good thing to remember why Canon is a good investment. I'm talking about above-average sector margins in terms of gross margins, as well as above-average on both operating and net margin levels. Overall profitability KPIs are still well above the average, in this case, the hardware industry sector (Source: GuruFocus).

Where the company really shines is debt. Like most Japanese businesses, Canon operates with an extremely low amount of leverage. This leaves the company with an interest coverage of 200x and a debt/EBITDA ratio of 1.16x.

The main problem that the company has been facing for the past 10 or so years is a decline in both the gross and operating margins - so while the company retains above-average profitability, it's not as solid or as above-average as it once was. Also, once we look at current prices for the company, we also see that the company is seeing above-average price levels in terms of P/E, as well as an above-average sales multiple. Some of these multiples, such as sales, are not the best way to value Canon - but as with all companies, if every single measurable KPI would present an attractive value, I would say you could take that to the bank.

For this, though, the picture is more complicated.

The recent set of quarterly results is solid - even if they're not as good as they might have been before in terms of growth.

{kind=link}

But let's not underestimate Canon. The company really troughed during COVID-19, but has reversed with a sort of vengeance typically reserved for other businesses. Fundamentally speaking, Canon is one of the most impressive companies on the Japanese market that you can invest your money in. I'm talking about a sub-3% debt ratio for an A-rated, 3.6T yen company. That alone, not even mentioning the 3%+ yield, should be enough for the more conservative investors of you to stop and pay attention to this business.

Now, granted, that yield is no longer as great as it once was, and the value upside - more on that later - also isn't as great as it once was.

Still, if you want an upside case on Canon, you can still see it here. The company retains market leadership in several crucial fields, and every single risk that the company has is pretty much macro-related, things that the company has very little control over.

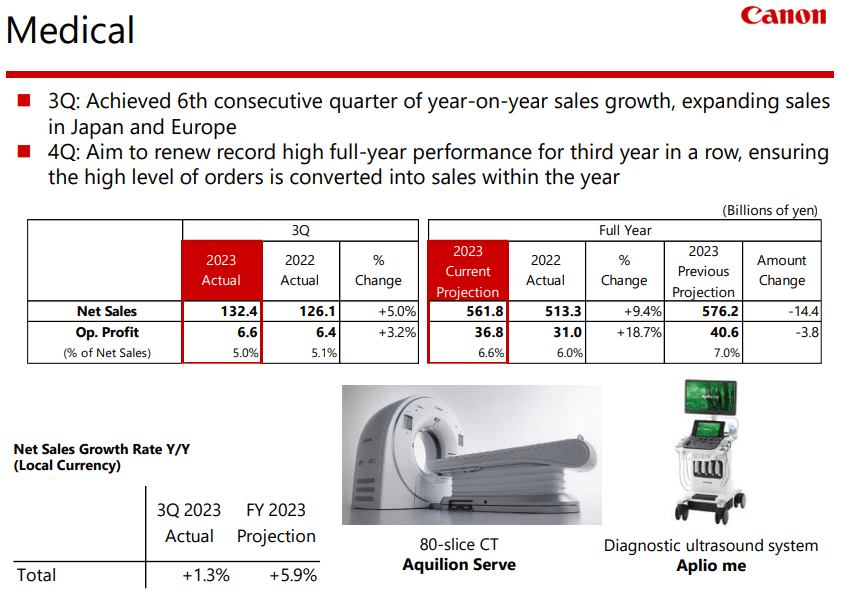

The downturn in demand was primarily in the printer segment and related - with continued growth in network cameras, medical products and other smaller business segments. It's important to remember that Canon does quite a bit of advanced products in a few, innovative segments, and while medtech usually isn't the focus for Canon, it's certainly a segment that deserves some attention.

{kind=link}

So is the company's segment which focuses on optical and industrial equipment, such as semiconductor lithography. The company also has significant inventories still on hand - 16B Yen higher than it was at the end of 2Q23, but this is mainly a build-up of goods that's expected to normalize at the end of December, and where we'll see what 4Q23 brings.

Overall, Canon has achieved the third consecutive year of sales and profit growth after COVID-19, and a strong link to its 2025 targets. On the longer-term timeframe, this is a step in the right direction according to the company's Phase VI plan, which is ongoing. The company posted more than three trillion Yen of net profit in 9M23 alone, which is the first time in fifteen years the company has managed this.

However, the company has also lowered sales estimates due to changed market conditions. The company still aims to bring a strong close to the year, but estimated earnings growth for the foreseeable future, the next few years, is lower than previously.

How low?

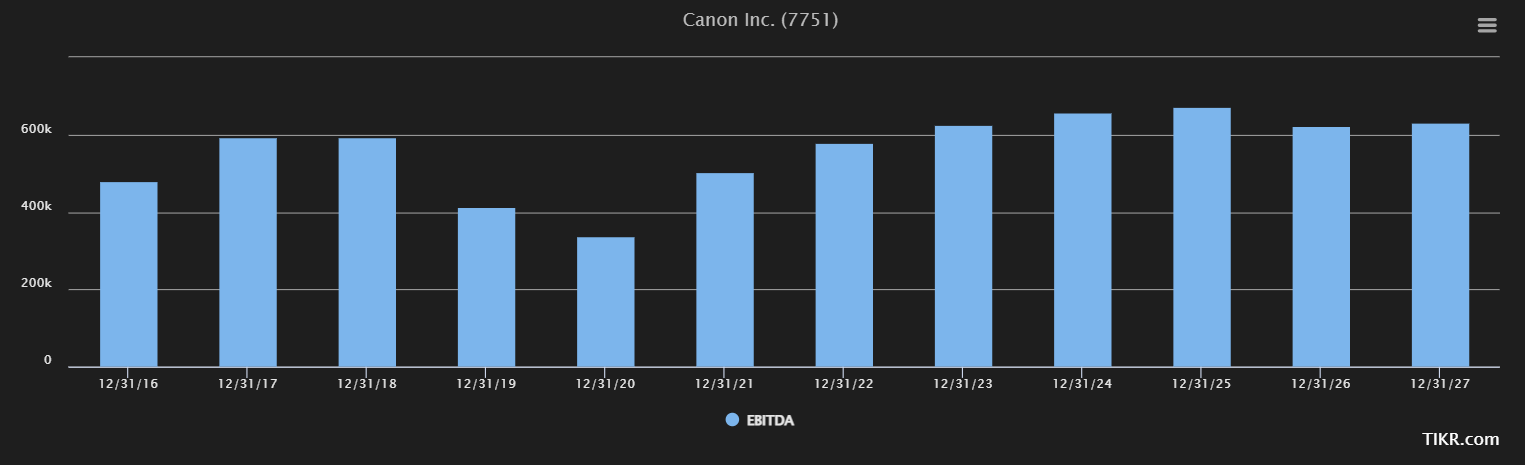

Here's the thing. I forecast the company's SCM and other initiatives and demand in some of the sectors will result in a growing company EBITDA - at least in 2024. However, beyond that, I believe there will be a normalization for the company. Much of 2020 was creating pent-up demand which we're seeing realize now, and which we've seen realized for the past two years.

S&P Global analysts tend to mostly agree with these estimates but put peak EBITDA at 2025E.

{kind=link}

Let's look at what we have in terms of valuation.

Canon - The Valuation here is no longer as good

When I last reviewed Canon, the company was still at what I considered to be an undervaluation. I gave the company a PT for the ADR CAJPY of $24.5/share. The company now is at $25.89, as I am writing this article.

What this means is that I am changing my rating. The company's upside is now less than 15% per year inclusive of the dividend, and I would say the valuation is somewhat stretched.

For the native share, the company's P/E is now over 13.3x. While the company has a historical premium of around 18, I don't view that as likely, even with an A-rating, a 3.66% yield, and a 4-5% EPS growth rate. I would forecast the company at no higher than 15x P/E, based on current EPS growth estimates, and this means that we're looking at no more than a 13.3% annualized upside.

While this may sound good, remember that the last few years have seen the company trade at 13-15x P/E, no higher than that. If the company normalizes around 13, then that's less than 7% annualized - and that's with the company dividend.

This highlights the importance once again, of company valuation when investing in a business. Even the S&P Global analysts following the native ticker 7751 don't consider the company a "BUY" any longer. With 9 out of 11 analysts either at a "HOLD" or "SELL" recommendation, I believe the overwhelmingly correct choice, if you believe in the valuation, is to at the very least "HOLD" here.

You could also realize some profits here. Including the dividend and FX, I could realize about 20% worth of profit here on my investment - and I may do so yet - even if I am not doing so at this particular time.

For 2024, I don't see a whole lot of catalysts for market-beating RoR, given the macro pressures related to lower demand for the company's core segments of printing.

Macro-wise, I continue to hold a pessimistic stance about the realistic prospect of a so-called soft landing. This is also why I've included far more defensive investments and also hold a 10%+ cash allocation at this time, which is very unusual for my approach. I'm usually more than 95% invested at all times.

I will characterize Canon as a successful investment, but with the valuation now significantly changed and the appeal less than 15%, I'm changing my stance and moving to a "HOLD".

Here is my 2024 update for the company, and what I expect for Canon.

Thesis

- Canon is one of the premier imaging, camera, and printing companies on the planet. It has a solid foundation as well as excellent growth prospects. At the right valuation, this company goes from being a possible buy to being a very compelling prospect for long-term investing.

- At a conservative 14-15x normalized P/E, I now only consider the company somewhat attractive and no longer a "BUY". My position, since establishing it, has grown to an impressive half-percent of my portfolio, and I'm looking to potentially either divest it, or wait until it becomes attractive again here.

- I follow Canon with a $24.5 ADR price target or 3,500Y for the native Tokyo ticker. It doesn't matter if you follow the native or the ADR, the company is no longer buyable here, as I see it.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company no longer fulfills my valuation criteria, which makes it a "HOLD" here, and no longer a "BUY".

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Canon: Why It Might Be Time To Leave It Behind (Rating Downgrade)