NCBDY - Capcom: Quality Business With Leading IP Deserves To Trade At A Premium

2023-10-20 06:26:33 ET

Summary

- Capcom is a Japanese video game developer and publisher known for franchises like 'Resident Evil' and 'Monster Hunter.'

- We believe the company can generate stable growth with the strength of its back catalog and new game release pipeline.

- Demonstrating a business with sustainable growth and high returns, we believe the shares deserve to trade at a premium.

Investment thesis

Capcom (CCOEF) has the ability to generate sustainable growth, based on a strong back catalog and a steady pipeline of high-quality IP due for release in the medium term. We believe the shares therefore deserve to trade at a premium, and we reiterate our buy rating.

Quick primer

Capcom is a Japanese video game developer and publisher with core franchises such as 'Resident Evil', 'Monster Hunter' and 'Street Fighter'. It also develops arcade game machines, pachinko/pachislot (Japanese gambling machines), and operates 'Plaza Capcom' arcade centers. Its peers include BANDAI NAMCO (NCBDF), Sony (SONY), Kadokawa (KDKWF), and Sega Sammy (SGAMY).

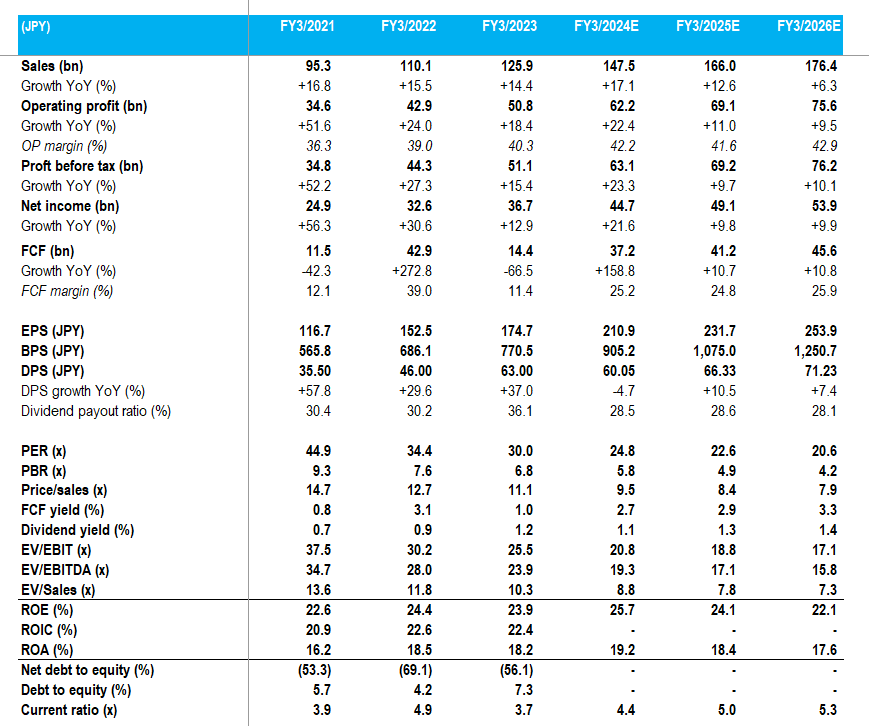

Key financials with consensus forecasts

Key financials with consensus forecasts (Company, Refinitiv)

{kind=link}

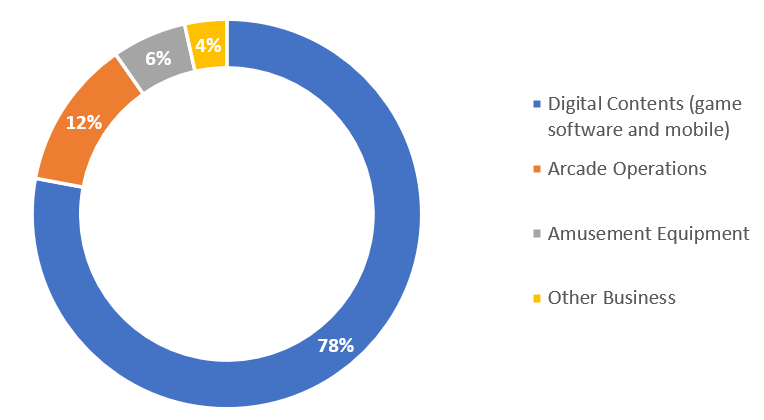

Sales split by segment - FY3/2023

Sales split by segment - FY3/2023 (Company)

{kind=link}

Updating our view

We are updating our view from March 2023 where we rated the shares as a buy, with the release of the 'Resident Evil 4' remake being a major success driving earnings strongly in Q4 FY3/2023.

Q1 FY3/2024 results have started strongly with the release of 'Street Fighter 6' and high repeat sales of 'Resident Evil 4'. The company's FY3/2024 guidance points to a steady 10% growth YoY at the operating profit level of JPY56 billion, but consensus (see key financial table above) is more optimistic at 22% YoY growth YoY.

The big question facing investors is the software release pipeline. An undisclosed major release is planned for H2 FY3/2023, and there is limited visibility for the medium-term. We want to assess whether 1) FY3/2024 will experience a strong second half, and 2) the outlook for the medium term for key releases to sustain earnings growth.

The strategic value of a strong back catalog

Capcom is aiming to sell 45 million units of game software in FY3/2024 ( page 7 ), equating to growth of 8% YoY. Whilst this may look like a relatively high hurdle YoY, the company is aiming to make up 79% of the total volume from previously released catalog games. This tells us two things: 1) Capcom has confidence in the strong shelf life of core franchise releases, as many of the top-tier titles continually sell over 1 million units per year, and 2) the dependence on new title releases is relatively low at approximately 9.5 million units. Dependence on the back catalog is positive for the sales mix, given the limited need for marketing activity.

With 'Street Fighter 6' already selling 2 million units and 'MegaMan Battle Network Legacy Collection' selling 1.3 million units during Q1 FY3/2024, the company has relatively low targets for new release volumes to make up in the rest of the year, but a million-seller is clearly required. With updates disclosed at the Tokyo Game Show in September 2023, we believe 'Dragon's Dogma 2' will be a core release for Q4 FY3/2024. The long-awaited release of the online team-based action game 'Exoprimal' in July 2023 was relatively muted, although the company seems to have confidence that it will generate long-term value.

Expectations are more of the same

Whilst FY3/2024 may appear to rely on back catalog sales, the company remains focused on incremental growth with its long-term target of selling 100 million units of software per year. Capcom has been working towards constructing a company that is capable of sustainable growth, focused on retaining staff and strengthening its key brands and IP.

Successfully recycling and reinventing IP is a core and fundamental practice in the game industry, and Capcom has a relatively successful track record. It has three major offerings - 'Resident Evil', 'Monster Hunter', and 'Street Fighter'. It would therefore appear prudent to think that 'Monster Hunter' and its sixth mainline release are being prepared for FY3/2025. Following on, 'Resident Evil 9' will be expected in FY3/2026, a rejuvenated franchise following the success of the remake of 'Resident Evil 7'.

We believe that the company will either need a new big-hitting franchise to boost sales volumes, or successfully bring back an old franchise (such as 'Devil May Cry') to double the current annual volume run-rate. This is a difficult undertaking and we believe that even Capcom will find this challenging. However, the company's track record combined with the continued secular growth in electronic entertainment are positive indications that the company can maintain a stable growth profile.

Valuation

On consensus forecasts, the shares are trading on PER FY3/2025 22.6x, and a free cash flow yield of 2.9%. Despite operating in what is a 'hit-driven' industry, Capcom displays characteristics of a quality business - operating margins at 40%, both ROE and ROIC above 20%, and EPS growth at 28% 10-year CAGR.

With a strong track record, strong IP, and quality fundamentals, we believe the shares should trade at a higher premium.

Thesis catalysts

A confirmed slate for H2 FY3/2024 software releases increases earnings visibility. Confirmation of 'Monster Hunter' for FY3/2025 will be a major event, given the large install base for the Switch.

Risks to the thesis

Title slippage results in a shortfall of unit sales volume in H2 FY3/2024. Major franchise releases are not ready in time to prevent earnings volatility for the medium term.

Conclusion

We believe that Capcom's focus on generating sustainable growth provides investors with an opportunity to invest in a quality business. With increasing volatility over the macro environment, we believe it will become more difficult for companies to generate stable growth; electronic entertainment remains a steady growth market, and companies equipped with skilled creators and strong IP have a competitive advantage. With an emphasis on multiple expansions, we reiterate our buy rating.

For further details see:

Capcom: Quality Business With Leading IP, Deserves To Trade At A Premium