ASOZF - Capgemini Shows Businesses Still Need Digital But It's Decelerating

Summary

- Digital transformation is a buzzword but it has substance, and companies are needing both the soft and the hard elements of the tech consulting services Capgemini offers.

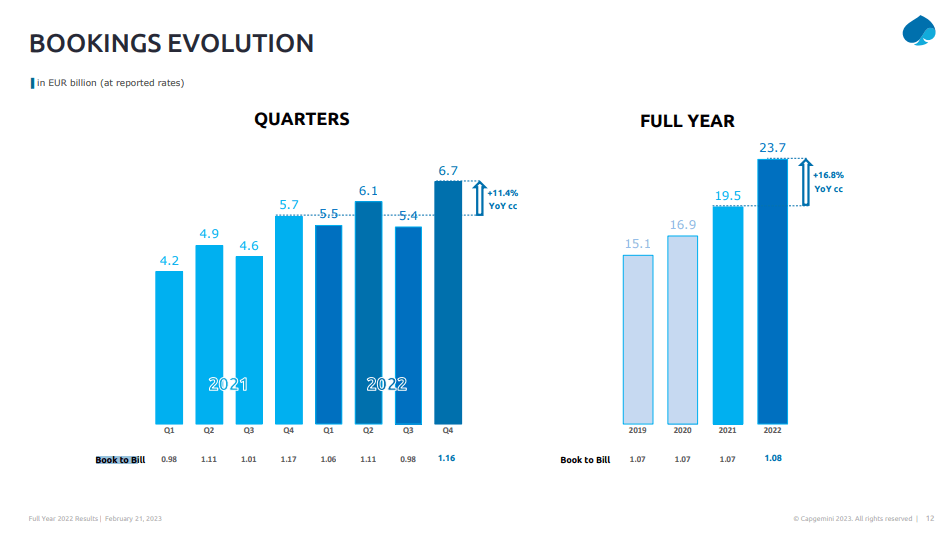

- Q4 growth is still good at double-digit rates in revenue, and book to bill revenues in Q4 are higher than they've been at any point in 2021 or 2022.

- Still, the growing headcount in a tight labour market was well executed, as margins managed to expand, but guidance shows substantial deceleration as discretionary spending declines.

- Mix effects also helped, with the greatest margin businesses gaining share. However, guidance shows substantial deceleration as would be expected with discretionary expenditure.

- Utilization rates should still rise as headcount becomes more productive, and FCF conversion is great, but deceleration means we prefer other ideas within the tech consulting space: Asseco Poland.

Capgemini ( CAPMF ) is a pretty straightforward tech consulting company. It does tech strategy consulting but also provides engineering solutions directly. Growth was good in 2022 unsurprisingly, but even in the Q4 momentum stayed rather well in line with the FY results. However, guidance is pointing to deceleration and the more discretionary segments are also the higher margin ones. Offsets are welcome such as new headcount that is still benefiting from learning economies and higher utilisation, and despite the headcount increases the margin profile did improve, but given the multiple and the growth outlook for the next year, we think there are better plays in the market like Asseco Poland ( ASOZF ), which goes for a much lower price.

Q4 and FY Notes

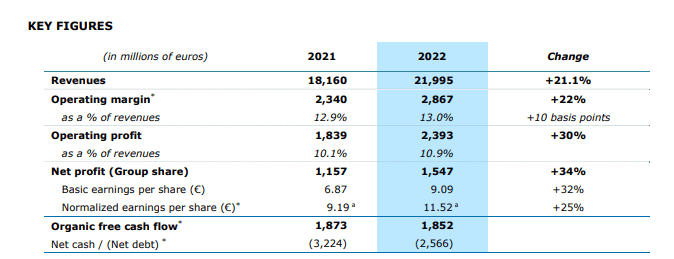

Organic growth was pretty good at 15.3% for the FY, and Q4's organic growth in revenue came at pretty similar levels at 12.8%. APAC acquisitions brought the headline revenue up to 21%, so the growth was mostly organic and it was being driven by their strategy consulting services related to digital transformations, which grew much faster than other segments. This contributed to mix effects as these services which are more discretionary, based on soft assets and are generally more transformative and value-added than cloud engineering services or other more commodified services like technology assessment.

Segments (Q4 2022 PR)

All segments still grew, and of course while momentum in cloud revenues had begun to show a little bit of lost momentum over the year as sales velocity declined, it was still a growth area together with applications and technology which supports digital transformations, a still pretty market agnostic force.

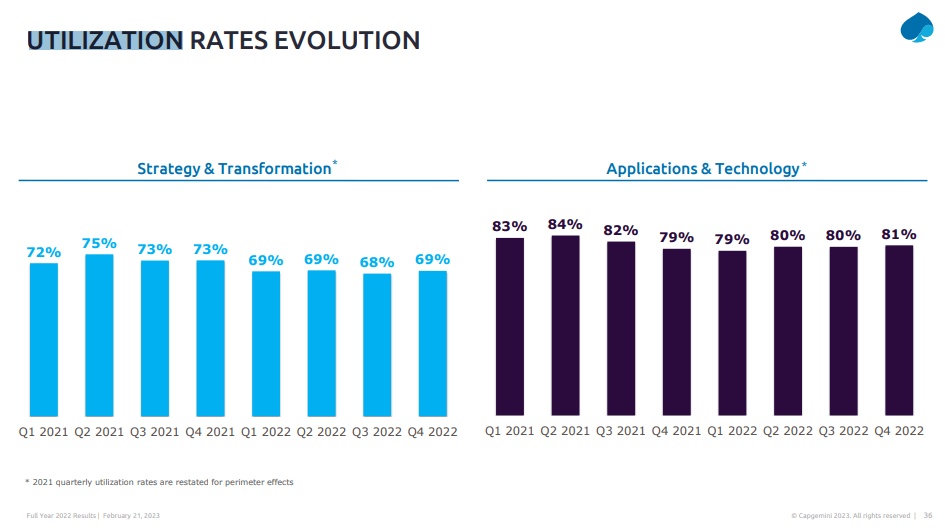

Labour tightness has been a common theme, and Capgemini has been adding headcount substantially, starting mainly in Q1, with utilisations falling concurrently but beginning to rise as the new talents get trained and benefit from learning economies. Headcount rose 11% YoY.

{kind=link}

Utilisation Rates (Q4 2022 Pres)

Still, we saw margin growth, which was partially due to mix effects but is still remarkable considering that labour inflation has been an important force. Offshoring helped too of more commodified work, but the returns there to GM accretion have also become increasingly limited.

{kind=link}

Key Figures (Q4 2022 PR)

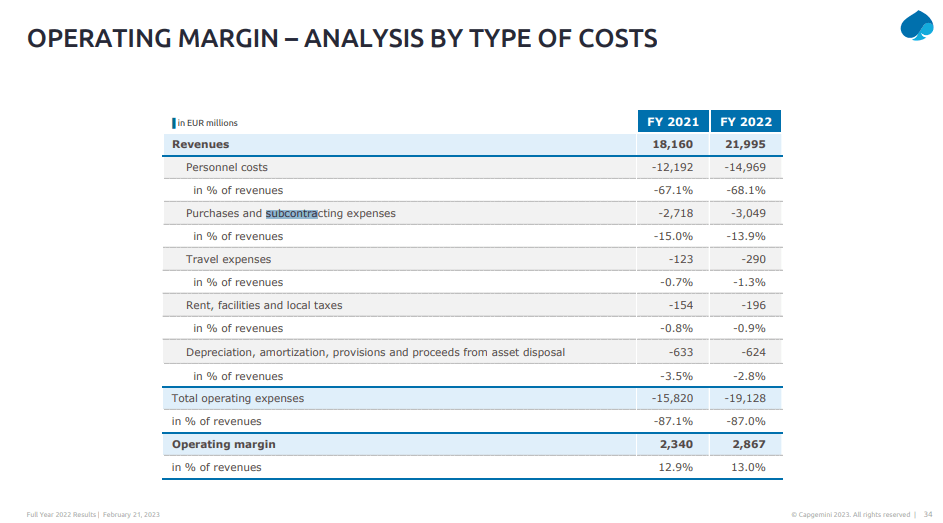

One of the reasons is that personnel costs increasing have taken away from the need to subcontract, at least as a portion of revenues, and this has led to margin accretion.

{kind=link}

Operating Margin (Q4 2022 Pres)

Management started adding headcount in Q1 2022 most aggressively, so it is unclear whether they believe this added headcount is ideal, especially as they guide cautiously in 2023 for a 4-7% growth in revenues, a substantial deceleration, but a believable and continued growth figure that comes from pretty resilient end-market exposures to the public sector, packaging as well as utilities and energy. Still learning economies are being developed and the J-curve for talent productivity after hiring should be overcome which should create further utilisation lift. The book to bill showing momentum more or less guarantees that headcount will be utilised for the next year by providing sales growth.

{kind=link}

Book to Bill (Q4 2022 Pres)

Bottom Line

Strategy and transformation may not be the more vigorous segments next year as these services are more discretionary. Still, higher margins are being forecast as possible for as much as a 20 bps increase. Growth is still expected which means utilisations should continue to rise with the added headcount and overcome the negative mix effects. Moreover, companies like this benefit from a decent degree of operating leverage, so earnings growth is in the cards for the next year and of course secularly given its markets.

However, the multiple is not very low at 20x. While common for tech consulting companies, especially one like Capgemini which returns more FCF than they make in net income, so a very cash generative business, we know of better deals in the market. Asseco Poland continues to be relatively cheap and provides superb growth . It also has about 15% exposure to solid tech exposures in Israel and in the US through its holding company structure. There's more to mine in researching it which means there is more likely to be opportunity. The downside is the Zloty exposure, and in this moment it's more volatile due to proximity to Ukraine and Russia, and also more severe inflation, but still we're talking about a developed market currency. At a third of the multiple it's a preferable option with much of the same exposures except to Eastern Europe especially as bond rates continue to rise and compete with earnings yields from public equities, increasingly pressured by macro on the demand side.

For further details see:

Capgemini Shows Businesses Still Need Digital, But It's Decelerating