CPXWF - Capital Power: A Long-Term Utility Growth Play At A Bargain Basement Price

2023-04-20 03:38:48 ET

Summary

- Capital Power has transformed its portfolio to focus on natural gas and renewables.

- It is diversifying away from its home province and across North America.

- Shares are undervalued and have significant upside when compared to peer group valuations.

- The stock currently yields 5.5% and is expected to grow the payout by 6% annually through 2025.

Capital Power Corporation ( CPX:CA ) is an undervalued and overlooked independent power producer trading at a significant discount to peers. It offers excellent total return potential as more investors discover the company.

(All figures in CAD unless stated otherwise)

Introduction

Capital Power is an independent power generation company headquartered in Edmonton, Alberta. The company's history dates back all the way to 1891, when it was incorporated as the Edmonton Electric Lightning and Power Company.

In 1995 the City of Edmonton -- which still owned the local electric utility -- allowed the company to operate at arm's length with the city as a 100% shareholder. Freed from limiting itself to its local market EPCOR (Edmonton Power Corporation) started diversifying away from the city, buying power plants in other markets like British Columbia, Ontario, and into the United States.

Finally, in 2009, the Edmonton made the decision to spin-out EPCOR's power generation assets while keeping the local utility assets. The power generation assets became Capital Power and started trading on the Toronto Stock Exchange.

In its first few years as a publicly-traded company with inherited assets, the company grew by adding new generating facilities in Canada. It also sold three gas-fired power plants to Emera in 2013 for US$541M to, in part, focus on the Alberta merchant power market.

In 2015, Alberta's then-newly elected provincial government dropped a bombshell. The government announced it would ban coal-fired power production in the province by 2030, ordering producers to replace it with a combination of natural gas and renewable sources. A big portion of Capital Power's assets in Alberta at the time were coal-fired power plants, and the market sent the stock reeling in response.

After about a year of uncertainty, the Alberta government announced it would compensate Capital Power (and several of its peers) for unexpectedly putting an end to coal. Capital Power was the largest beneficiary of these payments, receiving $52.4 million per year from 2016 to 2029, for a total of $734M.

The company used its new cash source to really juice its diversification program. Prominent acquisitions from 2016 to today include:

- A 294MW acquisition of two natural gas-fired power plants in Ontario and B.C. for $225 million

- A 795MW natural gas-fired plant in Illinois for US$441 million

- Internally developing a 178MW wind project in Kansas

- A 580MW natural gas facility in Arizona for US$300 million

- Internally developing a 99MW wind project in North Dakota

- An 875MW natural gas-fired power plant in Ontario for $977 million

- 250MW of assorted wind projects , including the internally developed Cardinal Point project

- Acquiring 50% (along with Manulife) of Midland Cogeneration Venture , a 1,633 MW gas-fired power plant in Michigan

Additionally, the company has almost entirely converted its remaining Alberta plants to natural gas. Genesee plants 1 and 2 are currently being converted, with the last facility slated to convert in the later part of 2023 after the on-site coal mine closes. The company also plans to expand Genesee with additional gas-fired facilities, projects covered by The Investment Doctor in his recent piece on the company.

Put it all together and Capital Power has a diverse set of assets spread across North America, with 7,500MW of generation capacity spread across 29 different operating facilities. Below is a map of the company's assets.

Investor Presentation March 2023

The opportunity

CEO Brian Grasso and his team have done a masterful job completely transforming Capital Power from a mostly-Alberta power producer to one with diverse operations across North America.

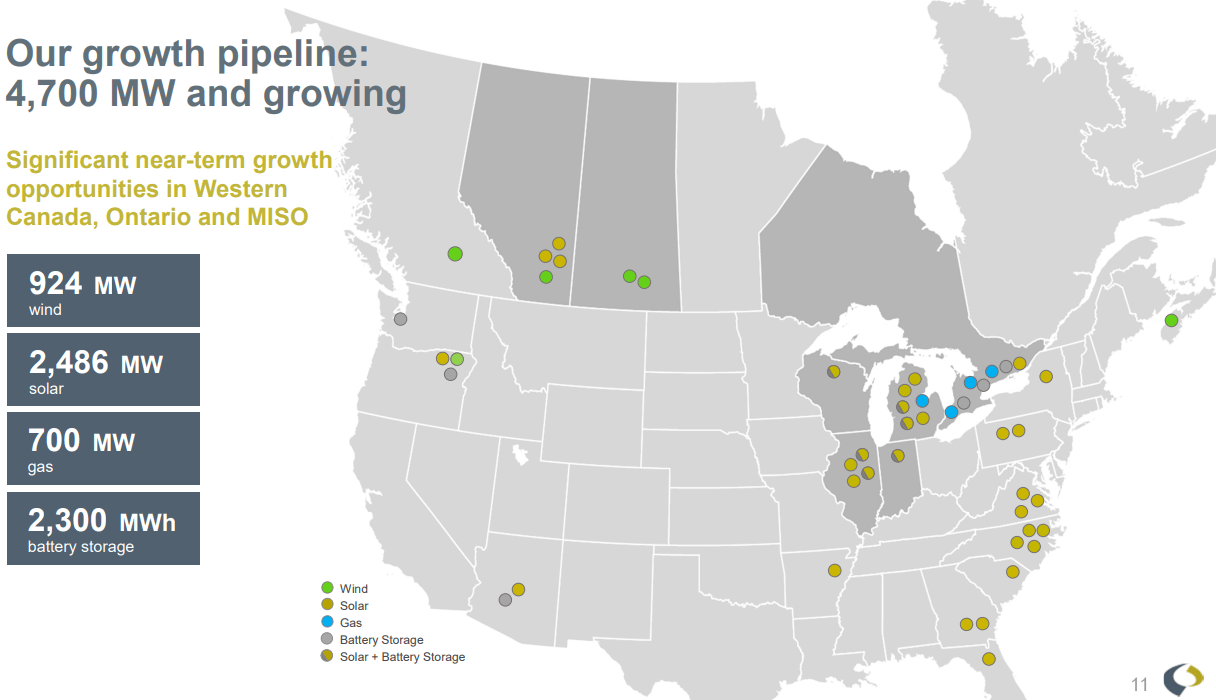

The company still thinks there's plenty of growth potential going forward too, identifying some 4,700MW of near-term growth opportunities across North America. Some are bolt-on deals to compliment current assets. Others have been identified with the future in mind, with a strong emphasis on battery storage.

Here's a map of upcoming growth opportunities, as identified in a recent investor presentation.

{kind=link}

The company has identified Ontario and Alberta as key growth areas, as well as the Eastern seaboard in the United States. Three projects submitted for approval in Ontario could add a further 250+MW to the portfolio, at a cost of more than $600M. Decisions on these Ontario projects are expected in May. The company has also bid on three solar projects (totaling 160MW), working with Duke Energy to modify the existing PPA, which was signed in 2020 and hasn't been adjusted for inflation.

There's always execution risk in a growth-by-acquisition story, and two recent failures from Capital Power's competitors highlight that risk in the power generation sector. TransAlta Renewables was forced to replace 50 faulty wind turbine foundations at its Kent Hills project in New Brunswick, at a cost projected to be $120M. And Algonquin Power recently cut its dividend after operational issues and higher interest rates impacted its earnings.

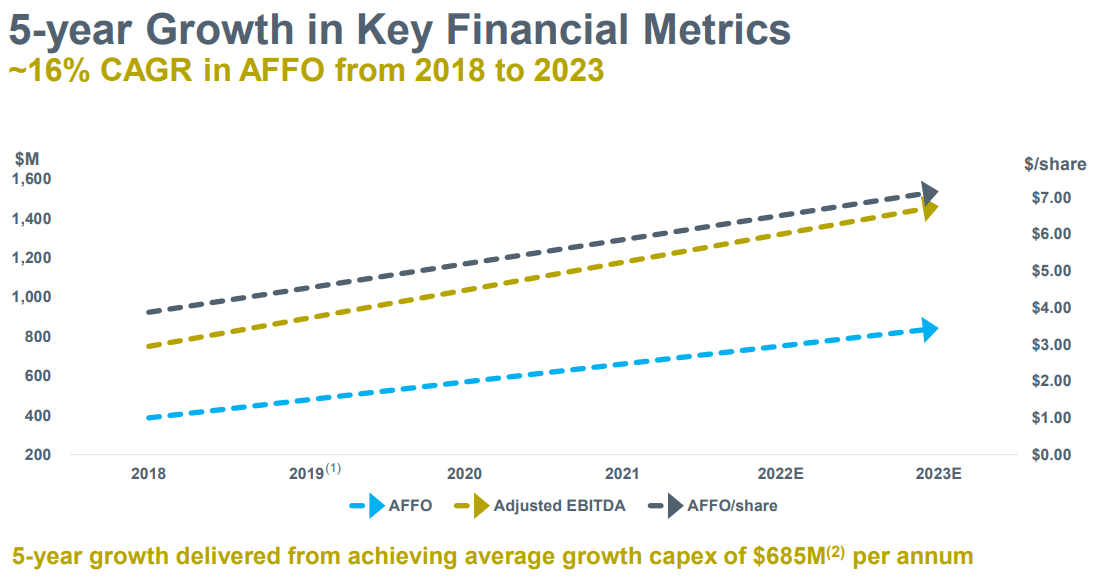

These risks are certainly real, but this analyst thinks they're mitigated by a couple of factors. Firstly, Capital Power has been expanding by purchasing assets for at least a decade now, and have shown investors a history of good execution on that front. Here's a chart that highlights EBITDA and AFFO growth since 2018. Capital Power has delivered sustainable earnings growth through its expansion program.

{kind=link}

And secondly, Capital Power is so cheap on an AFFO (adjusted funds from operations) basis that investors are already pricing in some pretty significant risks.

Valuation

Capital Power trades at a significant discount to its peers and is one of the cheapest stocks on the entire Toronto Stock Exchange, at least when looking at price-to-AFFO.

Capital Power earned $848M in AFFO in 2022, a 40% increase from 2021's levels. Much of this increase was from higher power prices in Alberta, but was also helped by lower finance expenses. The company expects 2023 to be largely the same as 2022, with AFFO in the range of $805M to $865M.

Capital Power currently has a current market cap of $4.99B. We'll round up to $5B for easier figuring. Meaning, shares trade at 5.9x trailing AFFO and a range of 5.8x to 6.2x 2023's expected AFFO.

Compare that to some of Capital Power's peers. Northland Power projects it'll earn between $1.70 and $1.90 in adjusted free cash flow per share in 2023. Shares trade hands at $33.43 each on the TSX after falling more than 16% over the last year. On the high end of the valuation shares trade at 17.6x forward adjusted free cash flow.

TransAlta Renewables projects it'll earn between $230M and $270M in cash flow available for distribution in 2023, which translates into a range of $0.86 to $1.01 per share based on 267M shares outstanding. On the high end that puts the stock at 12.3x forward cash flow available for distribution.

Finally, let's look at Brookfield Renewable Partners. The company didn't issue 2023 guidance, but we can look at consensus analyst FFO estimates on the company's earnings page. The company is projected to earn $2.37 per share in FFO in 2023, putting shares at 17.5x forward valuation.

(Note that each of these companies uses slightly different metrics to measure cash flow, but they do end up being fairly comparable to free cash flow)

Based on comparable companies, Capital Power trades at anywhere from a 50% to a 66% discount to its peers. This analyst thinks that discount slowly shrinks over time as the expansion plan continues to show solid results.

Giving back to shareholders

Capital Power has quietly become a dividend growth stock widely held by retail investors. In fact, according to a recent piece on its website , some 50% of Capital Power shareholders are regular investors who are looking for the company to provide stable dividends and predictable dividend growth.

The company has certainly delivered on that front, and is poised to continue growing its dividend going forward.

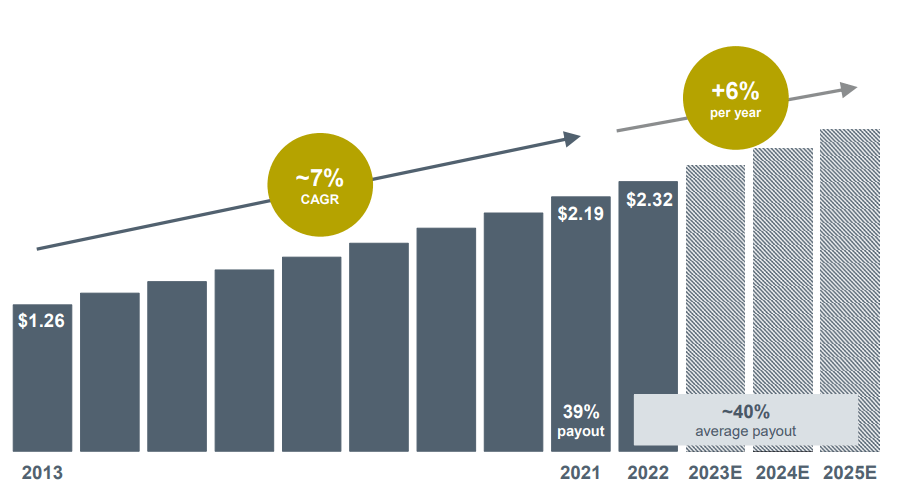

First, a little history. Capital Power has raised its common share dividend each and every year since 2014 by approximately 7% per year. It has already told investors they can expect 6% annual raises through 2025, with a payout ratio of approximately 40% of AFFO.

{kind=link}

If you combine that with Capital Power's high current yield -- which currently stands at 5.5% -- it combines to make the stock an intriguing income play as well. The yield alone is attractive. The potential growth makes it even more so.

And perhaps most importantly, the dividend gives an investor ample reason to wait while the valuation catches up to peers.

Share repurchases are another important source of shareholder returns. Capital Power hasn't delivered as well on that front. The company regularly announces share repurchase programs, but they're more than offset by using shares to pay for a portion of recent acquisitions. According to recent income statements , diluted shares outstanding have increased from 101.1M at the end of 2017 to 117.2M at the end of 2022.

Risks

There are three risks in this stock I'd like to highlight.

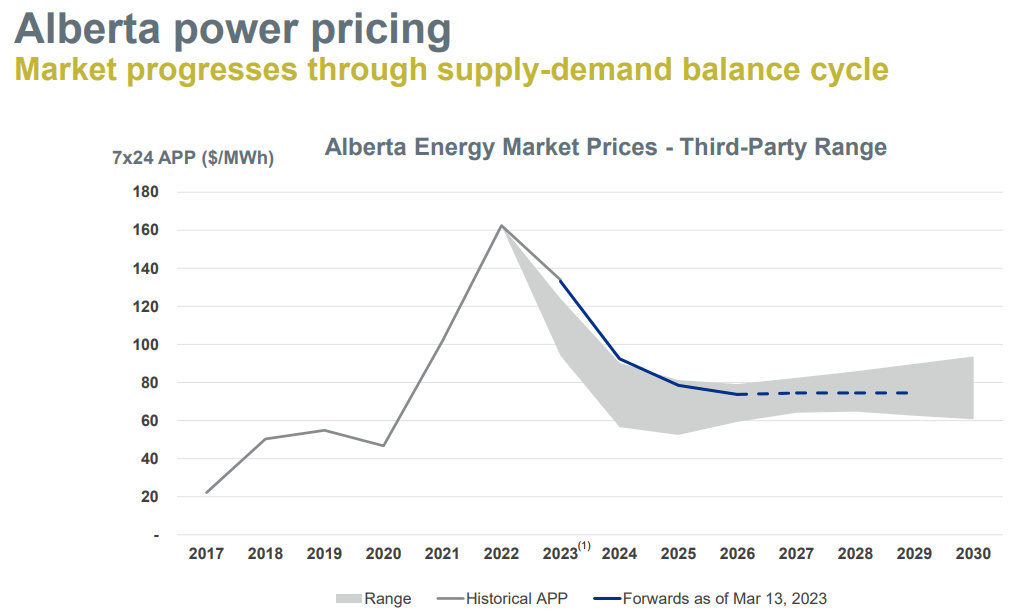

The first is the Alberta power market, one of the few markets left in North America where market prices are solely based on supply and demand. This floating rate has helped the bottom line of late as prices have been strong, with prices expected to stay relatively strong for the next few years.

{kind=link}

Capital Power can also mitigate the risk of lower prices by signing long-term supply contracts with certain key customers. This is an effective hedge for big power users, but many households and smaller businesses choose a floating rate option since those rates have historically been cheaper.

If Alberta sees a nasty recession its likely power prices in the province will head lower, a move that will impact Capital Power's bottom line.

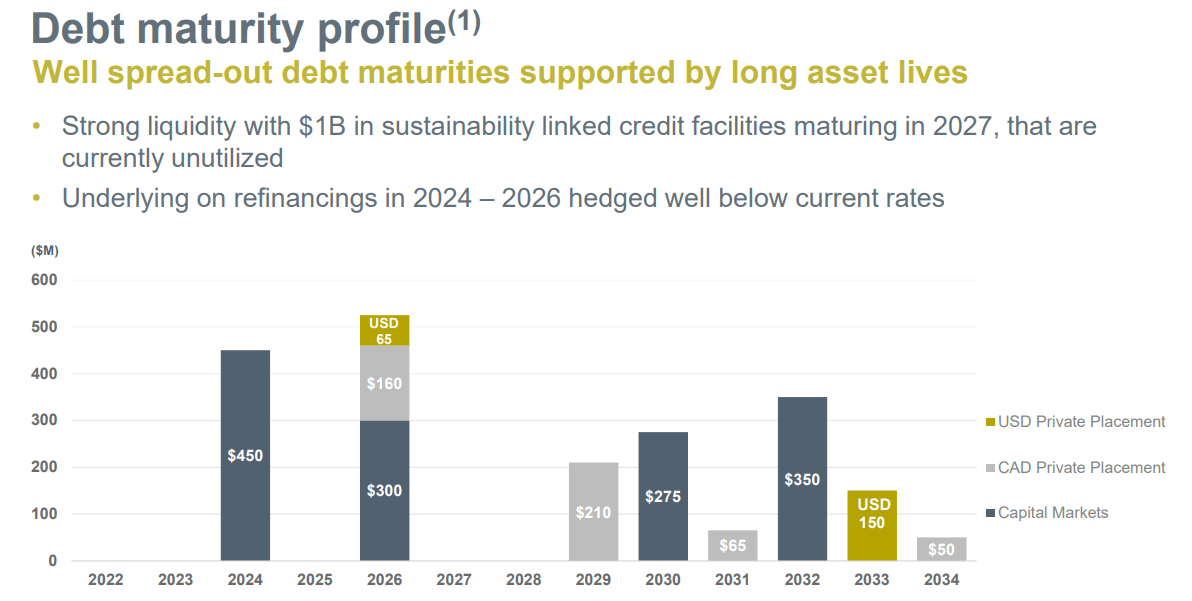

The second risk is higher interest rates. As of December 31st, 2022, the company had $3.9B worth of debt, offset by about $300M in cash. Higher interest rates mean lower profitability as debt gets refinanced.

The good news is the company has only about $1B worth of debt maturities from now until 2026, and then no debt coming due after that until 2029. It's a very manageable problem.

{kind=link}

The third risk is, as mentioned, execution risk. Although Capital Power does have a demonstrated history acquiring, developing, and managing power plants effectively, just one screw up can undo many years of meticulous work.

Additionally, the architect of the current expansion plan, CEO Brian Grasso, has recently announced his retirement. He will be replaced by Avik Dey, an unknown entity. The new CEO has an impressive resume, but investors will likely need a little bit of time to judge his performance before coming to any conclusions.

Conclusion

Capital Power has delivered excellent growth since its 2009 IPO, especially after 2015 as the company intensified its efforts to diversify away from Alberta. Despite solid execution and significant growth over time, the stock trades at one of the lowest free cash flow multiples on the entire Toronto Stock Exchange, and much cheaper than its competitors.

Some may argue Capital Power has traded at a discount for years, suggesting a rerating on the stock's valuation isn't coming anytime soon. But with a 10-year return of nearly 100% (plus dividends) and plenty of growth opportunities going forward, investors don't need the multiple to expand significantly for the stock to work out. It should generate enough growth for an adequate return even if the multiple stays low.

The company's excellent dividend also makes it easier for impatient investors to wait. A 5.5% yield today combined with 6% growth through 2025 means shares can stagnate and the investment still delivers steadily growing cash flow. I'm an early retiree dependent on dividends to pay the bills, so cash flow reigns supreme in my house. That cash flow helps many, including myself, be patient as long-term growth plans get executed.

Capital Power is a stock I plan to tuck away and hold for a very long time, patiently waiting until the market gives this name the higher valuation it has already earned.

For further details see:

Capital Power: A Long-Term Utility Growth Play At A Bargain Basement Price