CPWPF - Capital Power: Risk/Reward Turns Increasingly Favorable Following Midland Cogen Acquisition

- Capital Power recently disclosed the net C$581m acquisition of a cogeneration facility in Michigan.

- The deal is set to turn immediately accretive while also strategically diversifying the overall business.

- At the current relative discount, the stock offers investors compelling upside from here.

Capital Power ( OTCPK:CPXWF ), along with its 50/50 joint venture partner Manulife Investment Management, recently announced an agreement to acquire the 1.6GW Midland Cogeneration facility in Michigan for a net enterprise value of C$581m. While this equates to a modest % of the company's pre-deal valuation on a net basis, the acquisition represents a positive extension of the company's mid-life gas-fired M&A strategy. Meanwhile, the favorable financial terms of the acquisition will drive the annual dividend growth guidance to ~6% through 2025 (up from ~5% previously) while also adding a front-end-loaded cash flow profile - an appealing prospect given the current inflationary backdrop. Given the long-term renewables-led growth runway and that the plan to clean up its natural gas assets remains intact as well, the discounted relative valuation seems unwarranted at this juncture.

M&A-Led Diversification Continues with Midland Cogen Acquisition

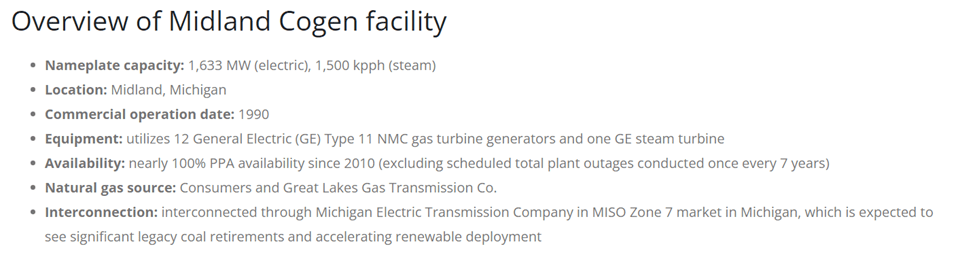

For its latest acquisition of a 100% interest in the 1,633MW Midland natural gas combined-cycle Cogeneration facility in Michigan, Capital Power has entered into a joint venture with Manulife Investment Management to fund the gross $894m (~C$1,150m) purchase price. For context, Midland Cogen is the largest US-based Cogen facility and has sustained an impressive ~100% uptime under its power purchase agreements (PPAs) over the last decade or so. Per the deal terms, Capital Power will run the asset, including the operations, maintenance, and asset management duties, and in return, will be compensated with an annual management fee.

Most of the capacity has already been dedicated to investment-grade counterparties - ~80% of revenues (or ~1,240MW of capacity) with Consumers Energy (a subsidiary of CMS Energy ( CMS ) and the remaining ~10% of revenues from steam and electricity purchase agreements with Corteva Agriscience and Dow Silicones through 2035. This leaves ~243MW of uncontracted capacity through which the company generates revenues via merchant sales on the Midcontinent Independent System Operator's (MISO) market in Michigan.

{kind=link}

More broadly, the acquisition represents a continuation of CPX's diversification strategy - the company has long utilized its strong balance sheet to strategically diversify beyond the Alberta region. With Midland Cogen, the company will have the added benefit of an increased contribution of contracted cash flows from its asset base as well (including gas-fired and renewable power). Financing the transaction should not be an issue - the company has more than enough liquidity given its ~C$329m cash balance as well as ~$1bn available from undrawn credit facilities. That said, at a ~C$581m net enterprise value (including attributable debt), this transaction alone will exceed the ~C$500m targeted annual committed capital for growth, so any additional major M&A seems unlikely for the rest of the year.

Financially Accretive Deal Terms Support Dividend Upside

Per management estimates, the deal will add C$59m of average annual EBITDA over the five years post-acquisition, although the cash flow profile is front-loaded - from an initial ~C$85m in 2023 - the asset's cash generation will decline to ~C$45m in 2027. Thus, the asset is being acquired at an implied ~5x upfront EV/ EBITDA multiple, or ~8x the annual average EBITDA. Of note, this doesn't factor in post-acquisition synergies from the company tapping into additional cost efficiencies and cash flow opportunities from the asset, so I suspect the valuation multiple could move meaningfully lower over time.

Still, a ~8x EBITDA multiple is solid relative to Capital Power's prior 7.5-8.7x natural gas asset acquisition range. Plus, the front-end-loaded cash flows are a net benefit given the inflationary backdrop. All in all, the accretive nature of the deal validates management's decision to boost its annual dividend growth guidance, in my view (now up to ~6% through 2025 vs. the prior ~5%/year). With the company also noting it was tracking at or above the upper end of its full-year guidance (adj EBITDA of C$1.11bn-C$1.16bn) on its Q1 2022 call , I wouldn't rule out more upward revisions in the coming quarters.

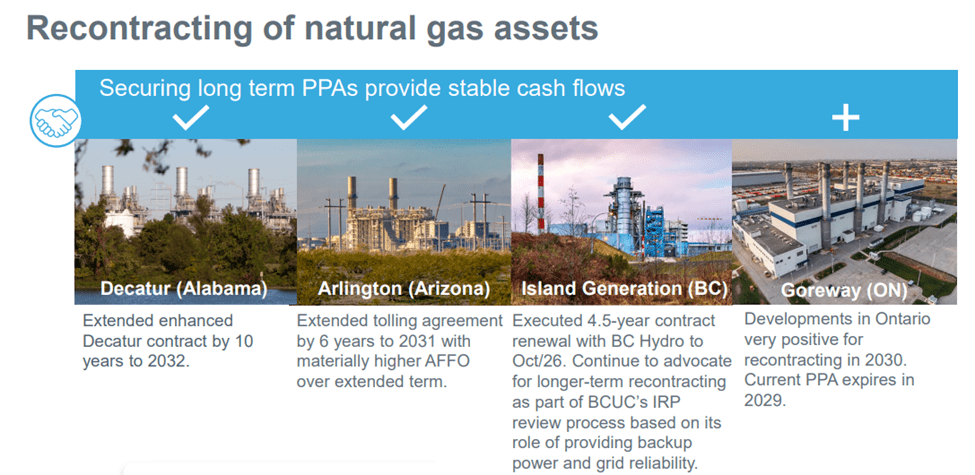

Building on Successful Track Record of Re-Contracting Mid-Life Gas-Fired Acquisitions

Thus far, Capital Power's track record in re-contracting mid-life gas-fired acquisitions has been impressive, having successfully re-contracted Decatur and Arlington Valley. Midland Cogen looks to be more of the same, with the asset well-positioned for re-contracting beyond 2030, given it is strategically located to support grid reliability. The timing coincides with a period when additional renewables are set to be added to the system as well - per management, MISO Zone 7 is set for significant retirements of legacy coal-fired generation as well as an acceleration in renewable power-generating capacity deployments in the coming years.

{kind=link}

That said, there is more re-contracting risk here, as this acquisition involves an asset expected to be >40 years of age once its existing contracts expire, likely making it more difficult to re-contract without incurring incremental capex. On the other hand, the 1.2k acres of land Midland Cogen has leased from Consumers Energy also allows for additional turbines and battery installations, presenting compelling long-term growth optionality.

Risk/Reward Turns Increasingly Favorable Following Midland Cogen Acquisition

On balance, Capital Power remains a great way to capitalize on the strong power pricing environment in Alberta. The pipeline looks robust, with the company on track to complete its natural-gas repowering strategy for Genesee 1+2 in 2024 and an investment-grade balance sheet leaving it well-positioned to add more accretive renewable power development projects in Alberta and the US to its fleet. In the meantime, the acquisition of the Midland facility validates Capital Power's proven strategy of surfacing value from mid-life, contracted gas assets and should, thus, be well received by investors. Coupled with the P&L accretion and planned dividend increase post-acquisition, the stock's ~7x fwd EV/EBITDA valuation seems cheap, particularly given the discount to its peers in the pure-play renewables space.

For further details see:

Capital Power: Risk/Reward Turns Increasingly Favorable Following Midland Cogen Acquisition