BOAT - Capital Product Partners: Higher Distributions Coming But Higher Risks Too

- Capital Product Partners ended 2021 by acquiring six LNG vessels, which has transformed their partnership.

- They subsequently increased their distributions by 50% in early 2022 with plans to continue growing them higher in tandem with their earnings.

- This points to higher distributions coming, especially given the very strong outlook for LNG demand from Europe, but disappointingly, this has also imposed a heavy cost upon their financial position.

- Their leverage is now in very high territory and appears poised to jump even higher as their net debt grows another circa 50% to acquire a further four LNG vessels.

- This leaves them particularly vulnerable, which offsets the desirability of their growth, and as a result, I believe that maintaining my hold rating is appropriate.

Introduction

A little over a year after the Covid-19 pandemic saw Capital Product Partners L.P. ( CPLP ) reduce their distributions, it seemed that higher distributions could be coming, although these were already risky after acquiring six LNG vessels, as my previous article discussed. Thankfully, management subsequently provided their unitholders with a solid 50% distribution increase, which now sees a moderate yield of 4.03%. Even though their outlook sees higher distributions coming, quite disappointingly, these are accompanied by higher risks too, as discussed within this follow-up analysis that also reviews their subsequently released financial results as well as the implications of the Russia- Ukraine war.

Executive Summary & Ratings

Since many readers are likely short on time, the table below provides a very brief executive summary and ratings for the primary criteria that were assessed. This Google Document provides a list of all my equivalent ratings as well as more information regarding my rating system. The following section provides a detailed analysis for those readers who are wishing to dig deeper into their situation.

Author

*Instead of simply assessing distribution coverage through distributable cash flow, I prefer to utilize free cash flow since it provides the toughest criteria and also best captures the true impact upon their financial position.

Detailed Analysis

{kind=link}

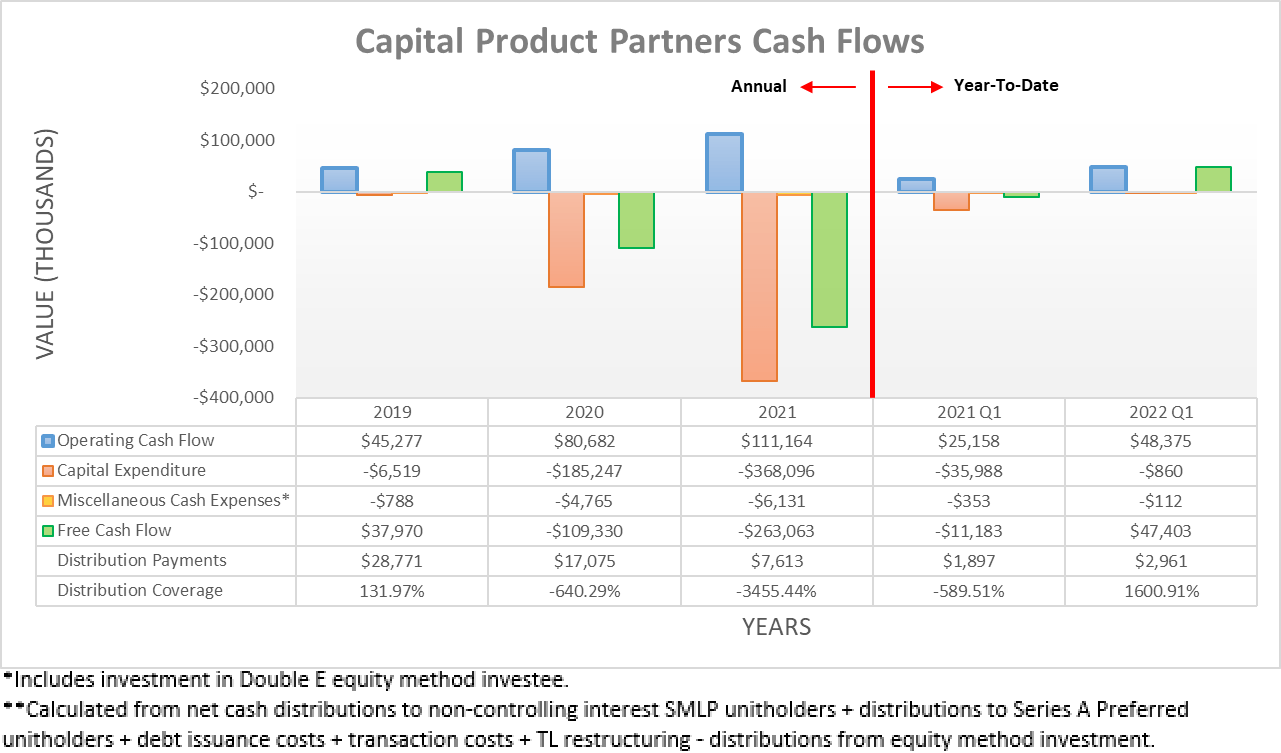

Following a solid end to 2021 with the fourth quarter seeing operating cash flow of $36.2m, they have enjoyed further strength into the first quarter of 2022 with their operating cash flow climbing higher to $48.4m. Apart from this strong consecutive increase, this also represents a very large improvement of 92.28% year-on-year versus their previous result of $25.2m during the first quarter of 2021, which was not materially impacted by their temporary working capital movements. This is not too surprising considering their now larger fleet includes six new LNG vessels, plus the continued strong operating conditions for container ships that comprise the vast majority of their remaining fleet .

Since they abstained from acquiring any new vessels during the first quarter of 2022, their barebones capital expenditure saw almost all of their operating cash flow translated into free cash flow of $47.4m, which provides ample scope to fund unitholder returns. When conducting the previous analysis, management had recently flagged higher distributions were forthcoming and thankfully, they followed through with a 50% increase in early 2022 with prospects to see even higher distributions coming, as per the commentary from management included below.

“I think as we complete more dropdowns and we increase our disable cash flow, you should also expect that we'll continue to increase the capital return to unit holders that is through unit buybacks and quarterly distributions.”

-Capital Products Partners Q1 2022 Conference Call.

It can be seen that management intends to continue scaling their unitholder returns higher as they grow their fleet larger with further dropdowns from their parent company, which phrased another way means further vessel acquisitions. Even though management had no way of knowing back during 2021 when acquiring their new LNG vessels, their outlook is very strong following the subsequent Russian invasion of Ukraine in early 2022, which stands to boost their financial performance, despite the otherwise tragic loss of life.

When looking further ahead into the medium to long-term, the outbreak of war in Eastern Europe is creating a surge in demand for LNG vessels as Europe now expedites sourcing their gas supplies from outside of Russia. This geopolitical event is highly uncertain and still evolving but it remains certain that Europe will reduce their vulnerability to Russia from a national security perspective, especially with the latter recently reducing their own gas exports in suspected retaliation to sanctions in support of Ukraine. This even saw the International Energy Agency warning that Europe should brace for Russian gas imports to completely cease, which creates the scary possibility that Europe could run out of gas during the coming Winter or more likely, see them forced to ration supply.

Even though they cannot simply flick a switch to completely transition their gas supply away from Russia seamlessly, this pivotal geopolitical moment should nevertheless still create additional LNG demand and thus by extension, additional demand for their LNG vessels for transportation to Europe during the coming years. Whilst this helps make their outlook for continued fleet and distribution growth more desirable, thus far the former has imposed a heavy cost upon their financial position that sees their higher distributions accompanied by higher risks too.

{kind=link}

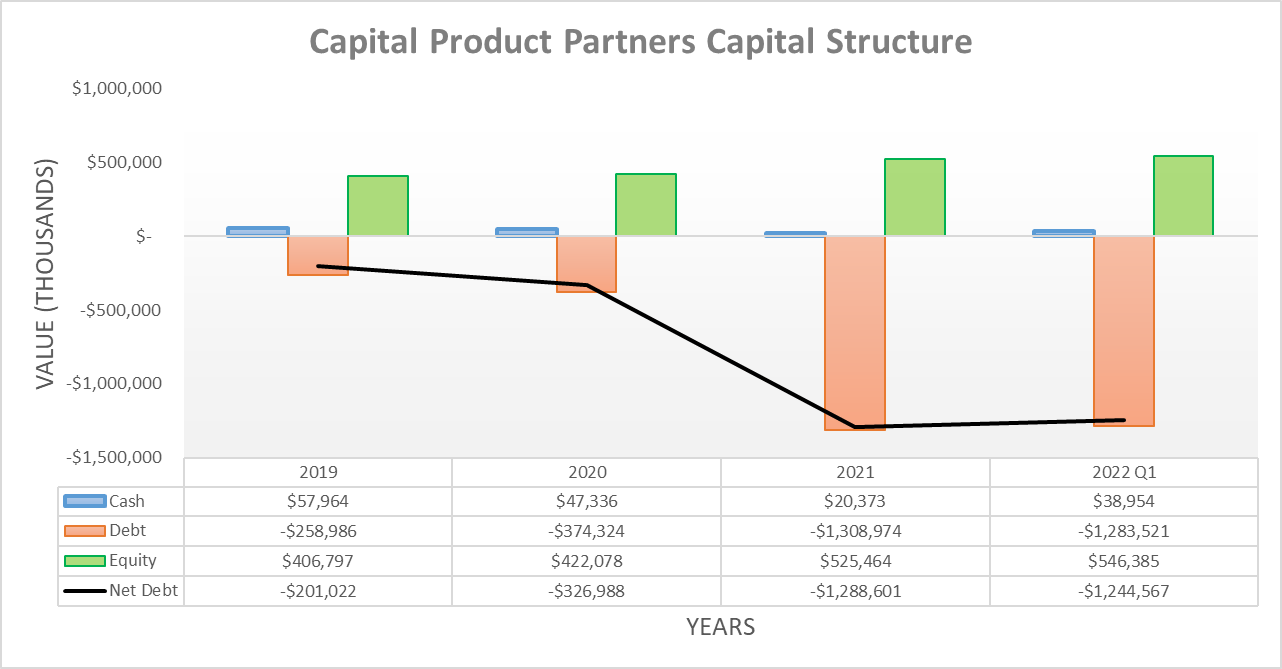

Their LNG vessels acquisition saw their net debt explode higher following 2021 to $1.289b and thus cross the $1b level for the first time, thereby sitting almost 300% higher year-on-year versus its previous level of $327m at the end of 2020, which was expected when conducting the previous analysis. Unsurprisingly, this transformed their capital structure in a lasting manner, as despite their solid cash flow performance during the first quarter of 2022 that was accompanied by almost no capital expenditure, they still saw their net debt barely move with only a small decrease to $1.245b.

When looking ahead, they are planning to double down on building out their fleet by acquiring another four LNG vessels for $597.5m later in 2022, which guarantees their net debt will continue climbing even higher to circa $1.85b and thus quickly push closer towards the $2b level. This represents another increase of almost 50%, which is concerning given where their leverage already resides and sees it far surpassing their market capitalization of only around $292m, thereby ruling out any ability to issue equity to deleverage and leaving them completely reliant upon their internally generated cash inflows.

{kind=link}

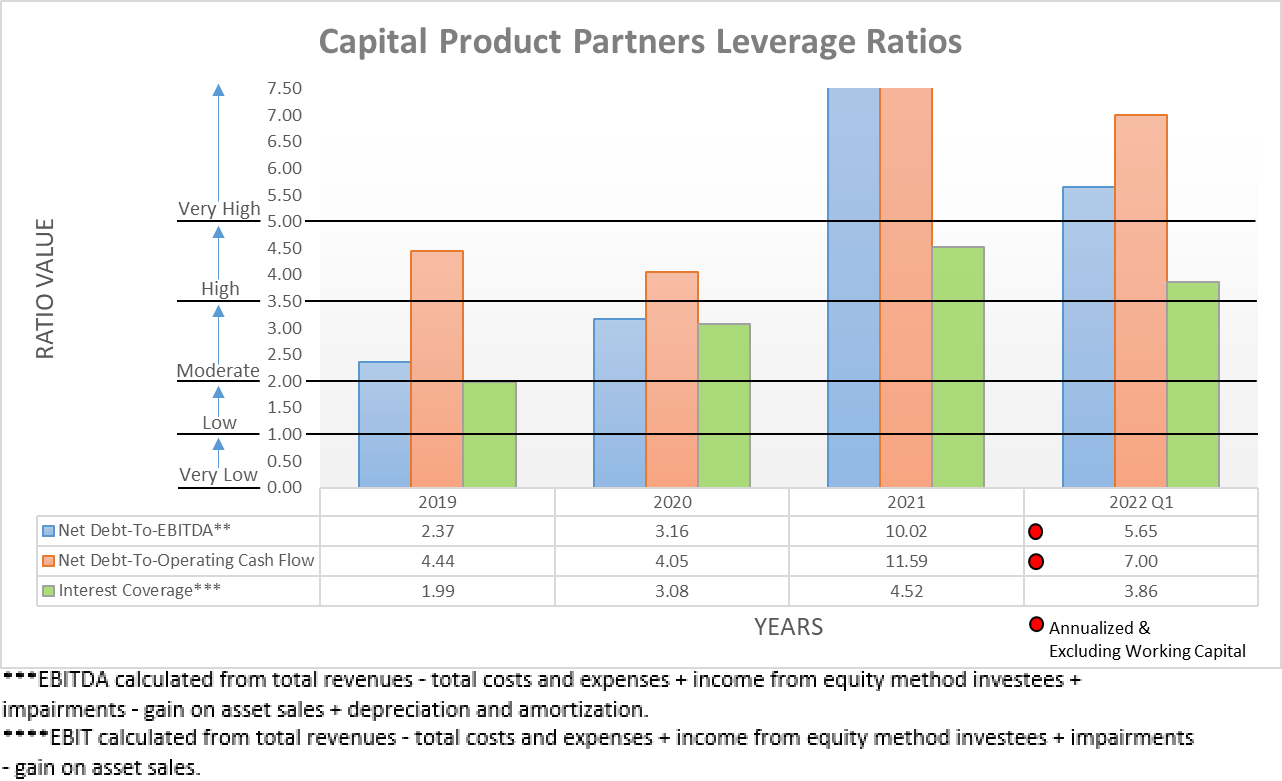

Despite their significantly stronger financial performance throughout the first quarter of 2022, it was nowhere near sufficient to offset their dramatically higher net debt and thus as a result, their net debt-to-EBITDA now sits at 5.65, whilst their net debt-to-operating cash flow sits at 7.00. Apart from both now being well above their previous respective results of 3.16 and 4.05 at the end of 2020 before embarking upon the acquisition spree of 2021, they are also both now well above the threshold for the very high territory of 5.01, which confirms my fears when conducting the previous analysis.

Since their latest leverage ratios annualize their first quarter of 2022 results, they see full contributions from their new LNG vessels, as per slide six of their fourth quarter of 2021 results presentation . Apart from the usual fluctuations of the inherently volatile broader shipping industry that can see its fortunes turn on a dime, this means that there is not a simple answer to their very high leverage on the horizon. Even though the outlook for their new LNG vessels appears very strong, it should be remembered that more than half of their fleet are containerships, which could see their earnings suffer if the recent fears of a recession come to fruition, thereby offsetting the strength of their new LNG vessels.

Whilst not necessarily a dire situation, this nevertheless increases the probability of their leverage remaining very high, which hinders the appeal of their units. It also calls into question how they are going to fare after pushing their net debt even higher to acquire the next four LNG vessels later in 2022, especially since adding four new vessels to an existing fleet of twenty-one vessels cannot possibly see their financial performance increase by the same circa 50% as their net debt stands to increase.

{kind=link}

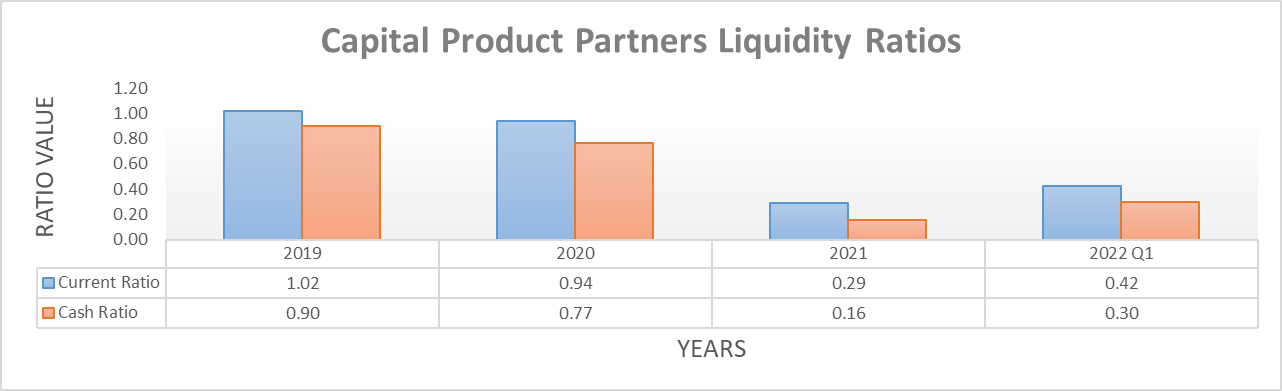

When turning to their liquidity, normally a current ratio of 0.42 would be concerning and point to weak liquidity but thankfully, their relatively high cash ratio of 0.30 largely negates this risk because when it comes to liquidity, cash is king and thus their liquidity remains strong. Their oddly low current ratio stems from 2022 seeing a total of $100.1m of debt maturities, as the table included below displays. Since central banks are tightening monetary policy, thereby pulling liquidity out of the system, this will be something to watch but realistically, they should be capable of refinancing as required given their ability to produce free cash flow outside of making large acquisitions, such as during the first quarter of 2022. Whilst they see further debt maturities every year, thankfully the majority is not until 2026 and thereafter, which also helps provide breathing room by keeping their refinancing requirements relatively modest in the medium-term.

Capital Product Partners 2021 20-F

Conclusion

On one hand, the prospects to see higher distributions coming as they grow their fleet larger and capitalize on the very strong outlook for LNG demand out of Europe are obviously desirable. Whereas on the other hand, when a partnership carries so much debt, their fortunes can change any moment with them increasingly vulnerable to sudden shocks and black-swan events, thereby seeing higher risks too with their leverage already very high and poised to increase as they tap debt markets to grow their fleet larger. Following this contrasting outlook, it should not be surprising that I continue to believe that maintaining my hold rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from Capital Product Partners’ SEC filings , all calculated figures were performed by the author.

For further details see:

Capital Product Partners: Higher Distributions Coming, But Higher Risks, Too