CPLP - Capital Product Partners: It's Cheap But Maybe For A Good Reason

2023-11-10 10:16:33 ET

Summary

- Capital Product Partners is a marine transportation company with a fleet of ships that transport LNG and other goods.

- The company faces challenges such as rising debt, dilution, and fixed-rate contracts that limit its ability to benefit from price increases.

- Despite its cheap valuation and strong growth, the company's issues and the overall underperformance of the marine transportation industry make it a risky investment.

Capital Product Partners L.P. ( CPLP ) is a marine transportation company headquartered in Greece and listed on Nasdaq. The company operates a fleet of ships to mostly serve medium- to long-term fixed charter contracts transporting mainly energy products such as LNG (liquefied natural gas). The company seems to offer strong growth at a cheap price but its chronic problems such as rising debt, dilution, and some other sector-specific concerns make it difficult for me to recommend this stock as a buy right now.

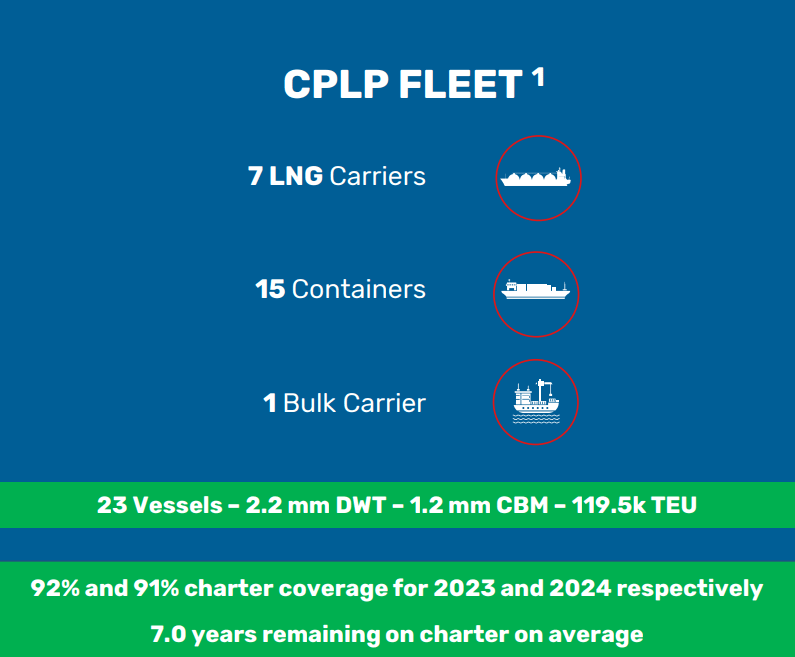

The company operates a fleet of 23 vessels 7 of which are LNG carriers, 15 are containers, and 1 bulk carrier.

CPLP Fleet Info (CPLP)

{kind=link}

Transportation of LNG became a big deal a couple of years ago with the war in Ukraine. European nations used to buy large amounts of natural gas from Russia delivered via pipelines but now they had to look for new sources of natural gas including the US. Since there isn't another way to deliver natural gas to long distances in a reliable way, the demand for ship fleets that are able to transport LNP suddenly became valuable. Also, energy costs rose along with the rising inflation which also increased the cost of transporting energy. These were beneficial to the company in the last couple of years.

On the other hand, there were also some challenges faced by the company. Since the company mainly makes long-term contracts at fixed cost, it wasn't able to benefit fully from some of the price increases and it may not benefit from some future price increases either. Having long-term contracts at a fixed rate allows the company to have good visibility and predictability to its future revenues but it also makes it difficult for the company to benefit from a rise in prices or pass its rising costs to customers.

Another challenge with the company has been its debt load. A good chunk of the company's debt is at variable rate and rising interest rates in recent years made it increasingly more expensive for the company to service and roll its debt. This is one of the biggest cost factors for the company and when we couple rising interest costs with its inability to raise prices in a meaningful way due to most of its contracts being at fixed rate, this puts the company's future earning potential at risk.

A couple of years ago, the company took on a large debt which increased its long-term debt load to $1.29 billion and its annual debt servicing costs to $83 million. This couldn't have happened at a worse time because interest rates jumped pretty sharply soon after this and the company might end up paying even more for debt servicing next year if this continues. The company doesn't exactly specify how much of its new debt is on fixed-rate as compared to variable rate. We know that about $250 million of this new debt is on fixed rate as the company discloses in its latest annual report but we don't know the rest. A good portion of the company's debt is to shipbuilders which provide credit to the company after it pays a 10-20% down payment for the building of the ship and each debt contract might come with different conditions which the company doesn't exactly specify.

{kind=link}

To put things into perspective, the company's total operating cash flow is $173 million, which means its debt servicing of $83 million eats into almost half of its total operating cash flow, which will limit the amount available to distribute to investors.

In recent years, in addition to rising debt, the company's investors also faced dilution. The company's share count is up more than 500% in the last 12 years even though the rate of dilution seems to be slowing down in recent years.

Historically speaking, marine transportation hasn't been a great industry to invest in for the majority of investors. While there are exceptions, most marine transportation companies fail to create much value for investors as many of them eventually either take too much debt, dilute their investors to death, or a combination of the two. When things are good, these companies can make a lot of money, get overly confident, over-invest, and when things are bad, they post large losses because they were overleveraged. There are brief periods where trading companies in this industry seem to result in good returns but those periods are rare. If you invested into this company 10 years ago you'd be down 78% in share price and -48% in total returns even after reinvesting dividends.

Speaking of dividends, the company's dividend distribution history has a lot of ups and downs but mostly downs. In fact, the company's distribution is down by more than 90% in the last decade (down from $1.64 to $0.15).

Marine transportation is a very cyclical industry and it's showing signs of cracking lately. One of the world's biggest marine transporters Maersk recently shocked the world by announcing mass lay-offs totaling 10k employees as freight rates started falling. Since most of CPLP's contracts are long-term fixed-rate contracts, it might not feel the full effects of falling freight rates but this could affect any future contracts made by the company.

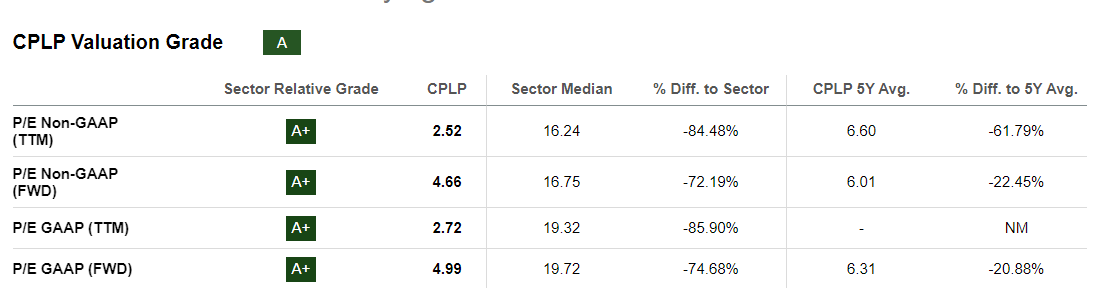

To be fair, the company's valuation is at compellingly cheap levels. It appears that the market is already aware of many of the issues I mentioned above and at least tried to price them in appropriately. The company trades at a trailing P/E of 2.5 and a forward P/E of 4.6 on a non-GAAP basis and a trailing P/E of 2.7 and a forward P/E of 5 on a GAAP basis as compared to mid to high teens P/E ratios in the transportation industry. The valuation is cheap and it will attract a lot of value-oriented investors but sometimes a company (or a sector) is cheap for a good reason and "cheap things" have a tendency to remain cheap for a long time. When it comes to CPLP, the issue is not exactly valuation. I will admit that the stock is fundamentally cheap and this is why I am rating it a "Hold" instead of "Sell". If I had to pick a "fair value" for the stock based on just current fundamentals, I'd probably pick a value significantly higher than the current value but then it wouldn't be fair because this is a chronically struggling industry where cheap fundamentals might not be enough to warrant a buy.

CPLP Valuation (Seeking Alpha)

{kind=link}

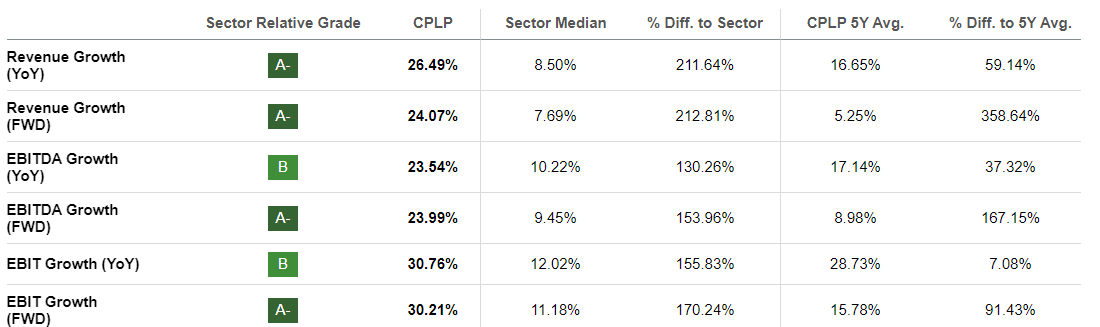

In recent years the company also posted some strong growth figures in mid 20s range and most of this growth came from the company's recent investments in transporting LNG and its new fleet additions (and some price increases). Time will tell us if these growth rates are going to be sustainable or just a one-time thing.

{kind=link}

Moving forward I can see the company benefiting from its LNG transportation business for quite a while even if the war in Ukraine ends. Europeans are likely to keep buying LNG from overseas for the foreseeable future since there is no easy way to build transatlantic pipelines. The company's dry cargo business is highly dependent on the health of global trades. Currently, marine transportation is facing some challenges as we've seen with Maersk but these challenges will probably clear once the global economy returns to growth in a few years. The business itself will likely be fine in the future but this may not be reflected in the stock because there may be additional debt and dilution considering the company's history of relying on these mechanisms in the past.

One thing to keep in mind is this company is categorized as a limited partnership and it is obligated to distribute practically all of its positive cash flow to investors in the shape of dividends. This makes the company dependent on external funding for any capital expenditures or paying debt off which could put a limit on the company's growth. The below paragraph is from the company's latest annual report:

"Because we distribute all of our available cash (a contractually defined term, generally referring to cash on hand at the end of each quarter after provision for reserves), we generally rely upon external financing sources, including bank borrowings and equity and debt securities offerings, to fund replacement, expansion and investment capital expenditures, and to refinance or repay outstanding indebtedness."

So the company enjoys a cheap valuation and strong growth but I am still not rating it as a buy because there are many challenges and issues faced by the company (not to mention the entire marine transportation industry). There are heavy debt levels, debt servicing eating into almost half of operating cash flow, rising interest rates making debt servicing even more expensive, high dilution rates, declining dividends over the years, and chronic underperformance of marine stocks in general. Some of these issues might be solved but many of them have been with us for a very long time and I would be skeptical about many of them being solved anytime soon.

For further details see:

Capital Product Partners: It's Cheap But Maybe For A Good Reason