CPLP - Capital Product Partners: Skating On Thin Ice In A Warm Winter

Summary

- Capital Product Partners enjoyed strong financial performance during 2022.

- Towards the end of the year, they were saved by record-setting LNG vessel charter rates that offset rapidly plunging container vessel charter rates.

- Worryingly, LNG vessel charter rates are normalizing due to a warm winter and container vessel charter rates remain under pressure.

- This opens the door for impairments, which could see a debt covenant breached or if not, left with no margin of safety.

- This is a risky situation with them skating on thin ice and thus, I believe that maintaining my hold rating is appropriate whilst awaiting to see how they traverse 2023.

Introduction

When last reviewing Capital Product Partners ( CPLP ) back around the middle of 2022, their unitholders were enjoying the expectation of higher distributions coming but as my previous article warned, these were accompanied by higher risks too. As we now take a look ahead into 2023, it worryingly sees them skating on thin ice in a warm winter that could possibly even see debt covenant problems later in the year.

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

After enjoying solid cash flow performance during 2021 that further strengthened during 2022, it ultimately made for a record-setting operating cash flow of $172.6m during the latter that was up significantly versus their previous result of $111.2m during the former. Due to management easing back on their vessel acquisitions during 2022, they finally generated free cash flow, albeit fairly narrowly relative to their operating cash flow with a result of only $27m.

{kind=link}

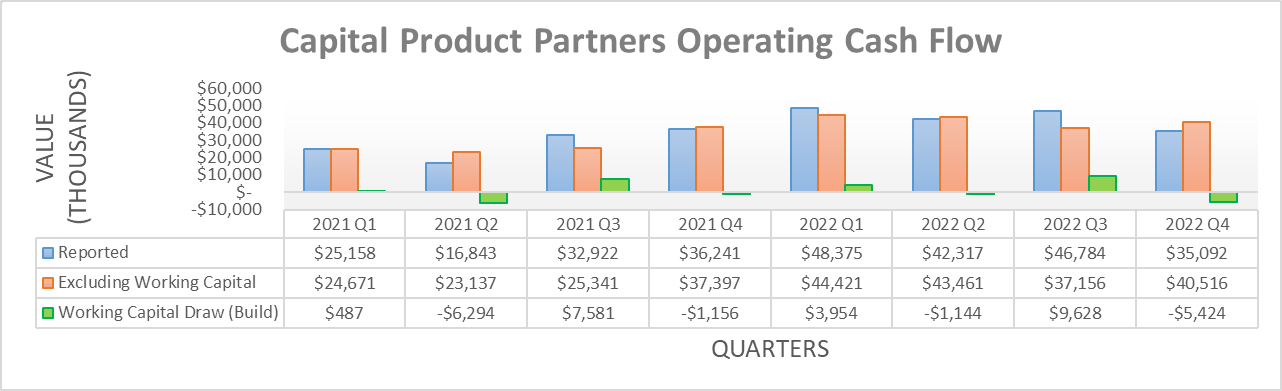

When turning to their quarterly operating cash flow, it becomes clear their record-setting results were weighted towards the start of 2022, as passing quarters saw results weakening. To this point, their reported operating cash flow during the fourth quarter dropped to $35.1m versus its previous result of $48.4m during the first quarter. At least if excluding their working capital movements, their underlying operating cash flow weakened to a less painful extent given its accompanying respective results of $40.5m and $44.4m, largely thanks to the strength of LNG vessels helping offset the weakness of their container vessels.

Capital Product Partners Fourth Quarter Of 2022 Results Presentation

{kind=link}

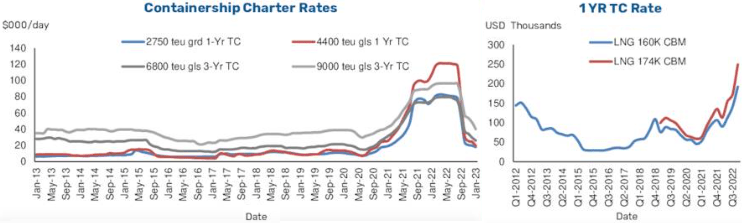

If reviewing these two graphs courtesy of management, it is easy to see how rapidly their charter rates for container vessels collapsed as 2022 progressed and weaker economic conditions started taking their toll, along with overstocked inventories and an easing of port congestion in the United States and elsewhere. Thankfully, they were saved by their LNG vessel charter rates that exploded to never-before-seen levels, as Europe scrambled to replace Russian gas supplies with LNG in the fallout from the Russia-Ukraine war.

Whilst positive, if not for what is effectively good fortunes following an otherwise tragic war, their financial performance would be suffering immensely right now, instead of merely weakening. Well herein lies the beginning of the problems because LNG vessel charter rates have already started normalizing during 2023 , thereby falling below $100,000 per day versus their crazy peak of above $400,000 a day back in October 2022. Quite unsurprisingly, this is driven by natural gas prices plunging dramatically on the back of hotter-than-expected weather that limited demand. As a result, this paints a concerning picture for even weaker financial performance heading into 2023 as container vessel charter rates remain under pressure and thus leave them skating on thin ice given their very high leverage.

{kind=link}

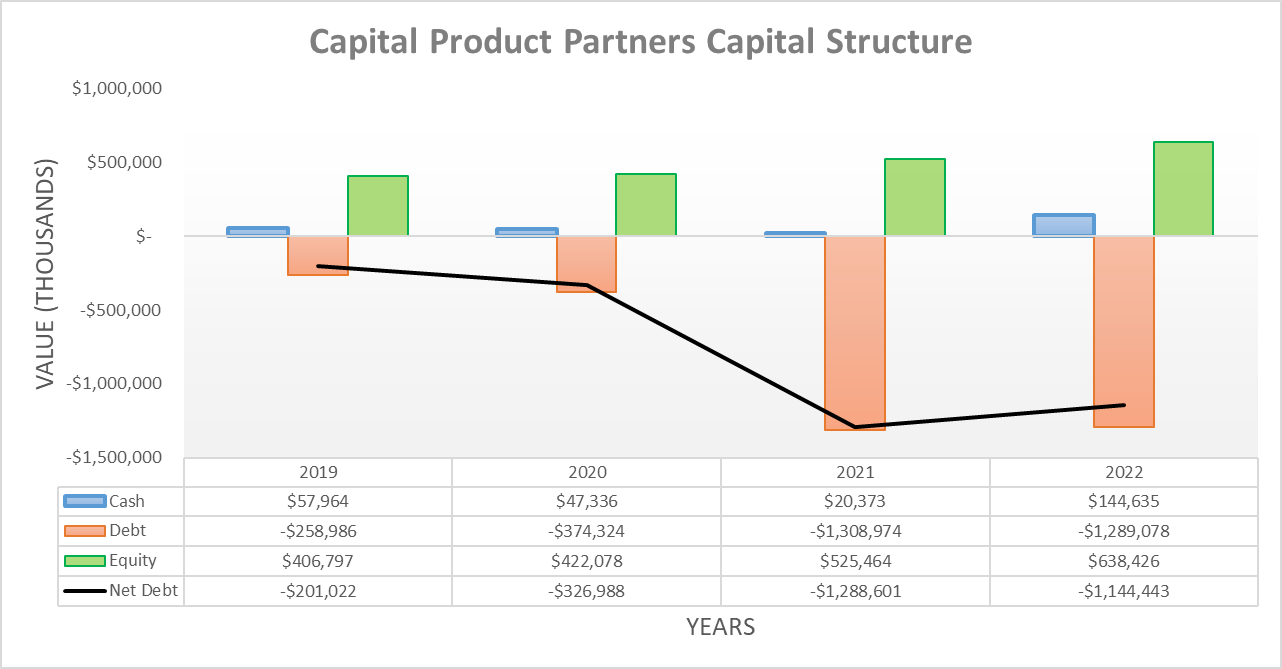

Thanks to easing back on their vessel acquisitions during 2022, their net debt actually decreased but admittedly, only to a modest extent and was helped along by $127.1m of divestitures. Still, any decrease is positive and now sees their net debt at $1.144b versus its previous level of $1.289b at the end of 2021. Unfortunately, this appears likely to be short-lived because 2023 is slated to see the final three of their four vessel acquisitions that were flagged when conducting my previous analysis, as per slide seven of their fourth quarter of 2022 results presentation .

Whilst their volatile cash flow performance makes it impossible to ascertain their future results to a set dollar amount, further vessel acquisitions make higher debt all but certain given the total cost of $597.5m for the four vessels. The first of their four vessels was delivered during the fourth quarter of 2022, which saw an additional vessel acquisition cost of $114.7m recorded on their cash flow statement. If subtracted from the original total cost, it indicates a further $482.8m cost will be forthcoming during 2023 that is essentially impossible to be completely funded by their weakening operating cash flow and thus means another circa $400m boost to their net debt, give or take a little.

{kind=link}

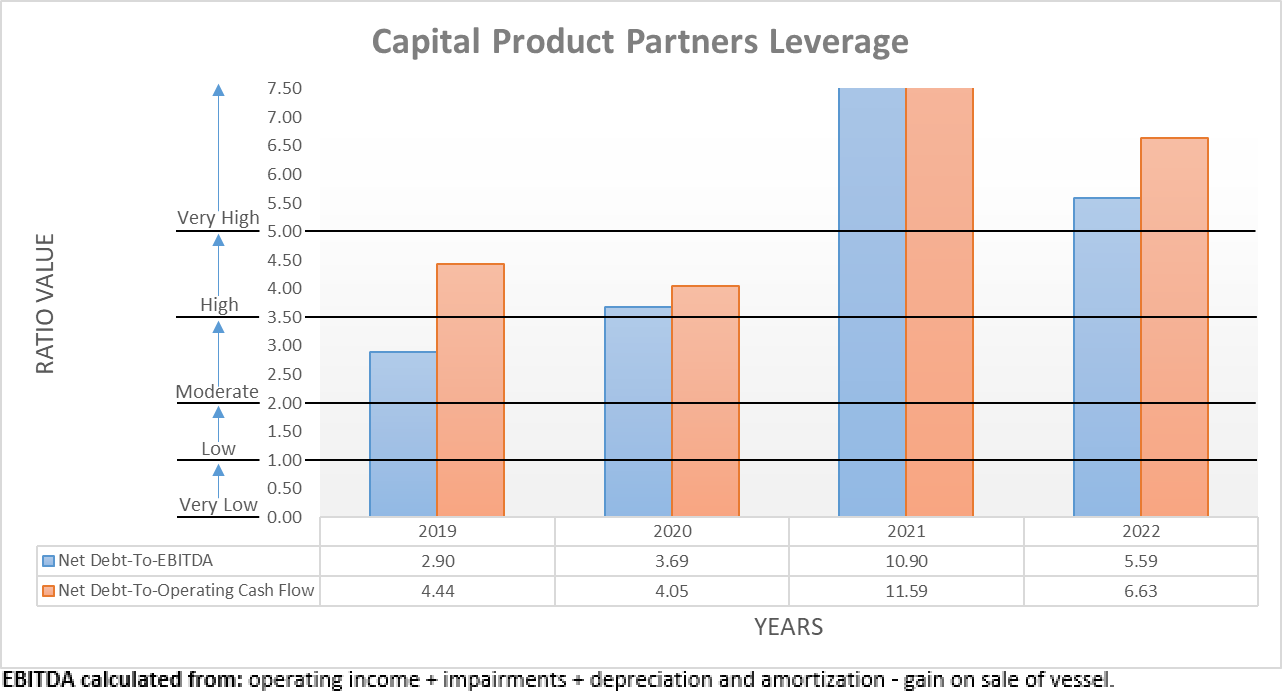

When turning to their leverage, it starts becoming easier to see why they are skating on thin ice heading into 2023. Quite unsurprisingly after seeing their net debt and weakening financial performance during 2022, their leverage is very high with a net debt-to-EBITDA of 5.59 and a net debt-to-operating cash flow of 6.63 that are both well above the applicable threshold of 5.01. Whilst their results at the end of 2021 were far worse at 10.90 and 11.59 respectively, even their latest results still leave them vulnerable.

Since the charter rates for LNG vessels are normalizing given this warm winter, they are likely to see their financial performance further weakening. By extension, their already very high leverage should surge even higher in tandem but that said, the bigger risk in this situation actually resides within their debt covenants that as subsequently discussed, I view as more of a liquidity issue.

{kind=link}

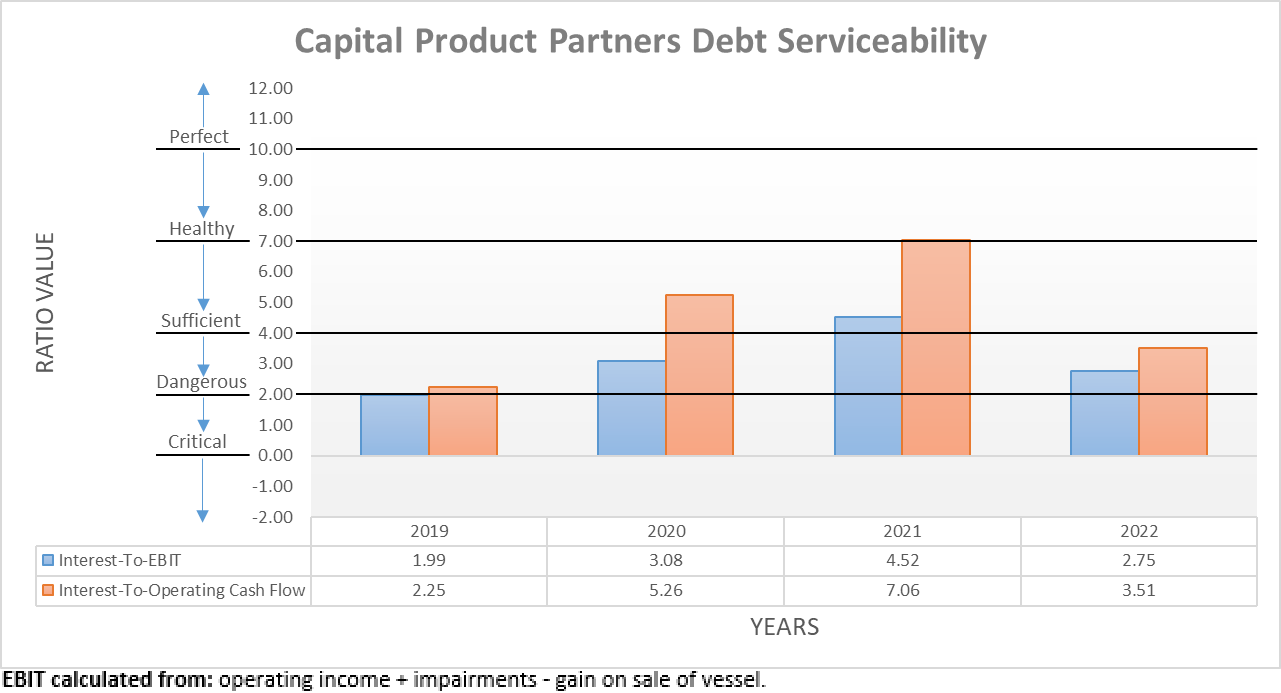

Despite their very high leverage, one slight area of reprieve is offered by their debt serviceability that somewhat surprisingly, actually remains sufficient. Regardless of whether their interest expense is compared against their EBIT or operating cash flow, their respective interest coverage of 2.75 and 3.51 is sufficient. That said, the margin of safety is not particularly high and thus weakening financial performance and higher net debt make this likely to deteriorate to dangerous levels in 2023, especially if charter rates for LNG vessels continue normalizing.

{kind=link}

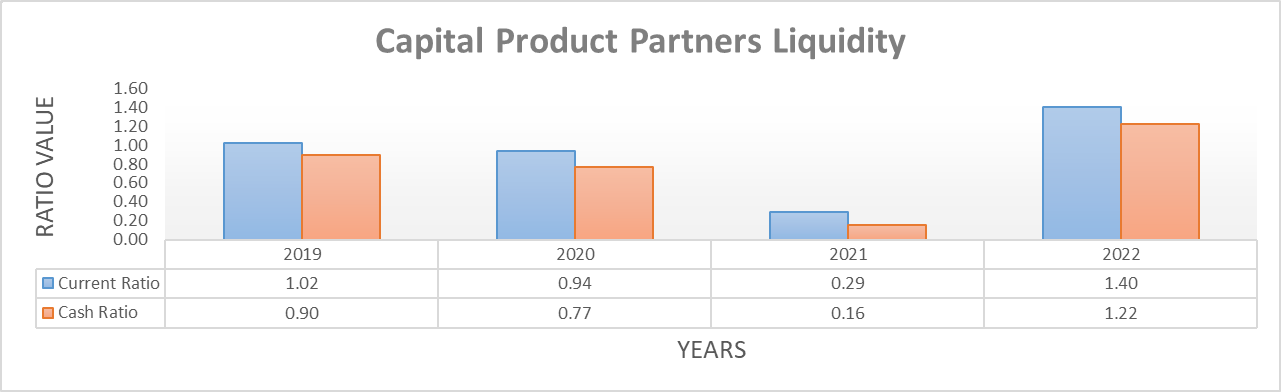

Whilst their leverage is already concerning, by far the biggest and most dangerous risks resides within their liquidity, as alluded to earlier. On the surface, this likely seems very strange because normally their current ratio of 1.40 and accompanying cash ratio of 1.22 would be considered a point of strength. It is true, these are strong results but alas, like many times in life there is far more lurking beneath the surface, namely, their debt covenants.

Capital Product Partners 2021 20-F

The most alarming debt covenant in my eyes is the first one, whereby they must retain a leverage ratio beneath 75%, which is later defined as the ratio between "financial indebtedness of the group net of any liquid assets" and their "market value adjusted total assets, as per their 2021 20-F . If phrased another way, it is essentially their net debt divided by total assets and following the end of 2022, their net debt of $1.144b and total assets of $1.997b give rise to a leverage ratio of circa 57%.

Despite being materially beneath their debt covenant, there are two very important moving parts to consider when looking ahead. The first being their aforementioned upcoming acquisitions of a further three vessels that will be primarily debt-funded, likely in the order of circa $400m. Whilst the aforementioned remaining overall $482.8m cost should be capitalized on their balance sheet, thereby boosting their total assets to circa $2.5b, the additional debt will also see their net debt pushed towards circa $1.55b. Since the latter increased relatively more than the former, it means their leverage ratio should increase to circa 62%. That said, their routine depreciation during 2023 will pull back on their total assets, which means the actual result would likely be slightly higher, possibly around circa 65%.

Unless their aforementioned weakening cash flow performance quickly turns a corner and helps reduce their net debt, this situation creates a narrowing gap beneath their debt covenant, which is already concerning. Meanwhile, the second moving part is potentially even more important and relates to how their total assets must be "adjusted to reflect the aggregate market value of all the fleet vessels", as per their previously linked 2021 20-F. During normal times, this is not problematic but these are not normal times as the container vessels that comprise most of their fleet are under pressure due to the aforementioned rapidly collapsing charter rates. If there is not a quick change of fortunes, this opens the door for potential impairments during 2023 that in turn, reduce their total assets and push their leverage ratio higher, possibly breaching their debt covenant.

If a debt covenant is breached, it is normally a death knell that foretells a trip to bankruptcy court as they obviously could not repay their entire debt balance at once and thus, it leaves their liquidity looking questionable. That said, I am not necessarily saying this dark future awaits unitholders, as management may negotiate with lenders ahead of time to avert such an outcome. Although this could still see their dividends cut, unit buybacks cease and possibly, a highly dilutive equity issuance that destroys unitholder value.

Conclusion

Even though the record-setting LNG vessel charter rates saved the day in late 2022, they are nevertheless skating on thin ice as a warm winter now sees the tide turning as natural gas prices plunge dramatically due to hotter-than-expected weather limiting demand. The majority of their fleet comprising container vessels remains under pressure and thus very worryingly, this opens the door to impairments that if forthcoming, could breach a debt covenant. Only time will tell and thus, I believe that maintaining my hold rating is appropriate whilst we await and see how they traverse 2023.

Notes: Unless specified otherwise, all figures in this article were taken from Capital Product Partners' SEC filings , all calculated figures were performed by the author.

For further details see:

Capital Product Partners: Skating On Thin Ice In A Warm Winter