CSWC - Capital Southwest: High Yield Low Leverage And Expenses Make It A Buy

2024-01-05 11:00:52 ET

Summary

- Capital Southwest has seen strong price appreciation over the past year, but remains attractive with a high and well-covered dividend yield.

- CSWC targets investments in the lower middle market, with a diverse portfolio and a focus on first-lien debt investments.

- It has shown strong performance, generating growth in NII and operating cost efficiencies, making it an appealing investment option.

BDCs have come a long way over the past 18 months, from being sold off by the market despite the obvious benefits to them from a rising rate environment to the market finally coming to its senses and pricing them appropriately higher.

This has indeed created plenty of buying opportunities along the way, this brings me to Capital Southwest ( CSWC ), which I last covered here with a 'Strong Buy' rating back in December of 2022, highlighting its improving operating leverage, value proposition, and discounted valuation.

It appears that my investment thesis has paid off, as CSWC has given investors a 54% total return since then, far surpassing the 16% rise in the S&P 500 ( SPY ) over the same timeframe. In this article, I provide an update and discuss why CSWC remains an appealing pick at present for its big yield, so let’s get started!

Why CSWC?

Capital Southwest is an internally managed BDC that, like peer Main Street Capital ( MAIN ), targets investments in the lower middle market, where deals are more fragmented resulting in less competition. These companies are also smaller in size compared to the middle market, thereby leading to more capital appreciation potential for CSWC as the investor.

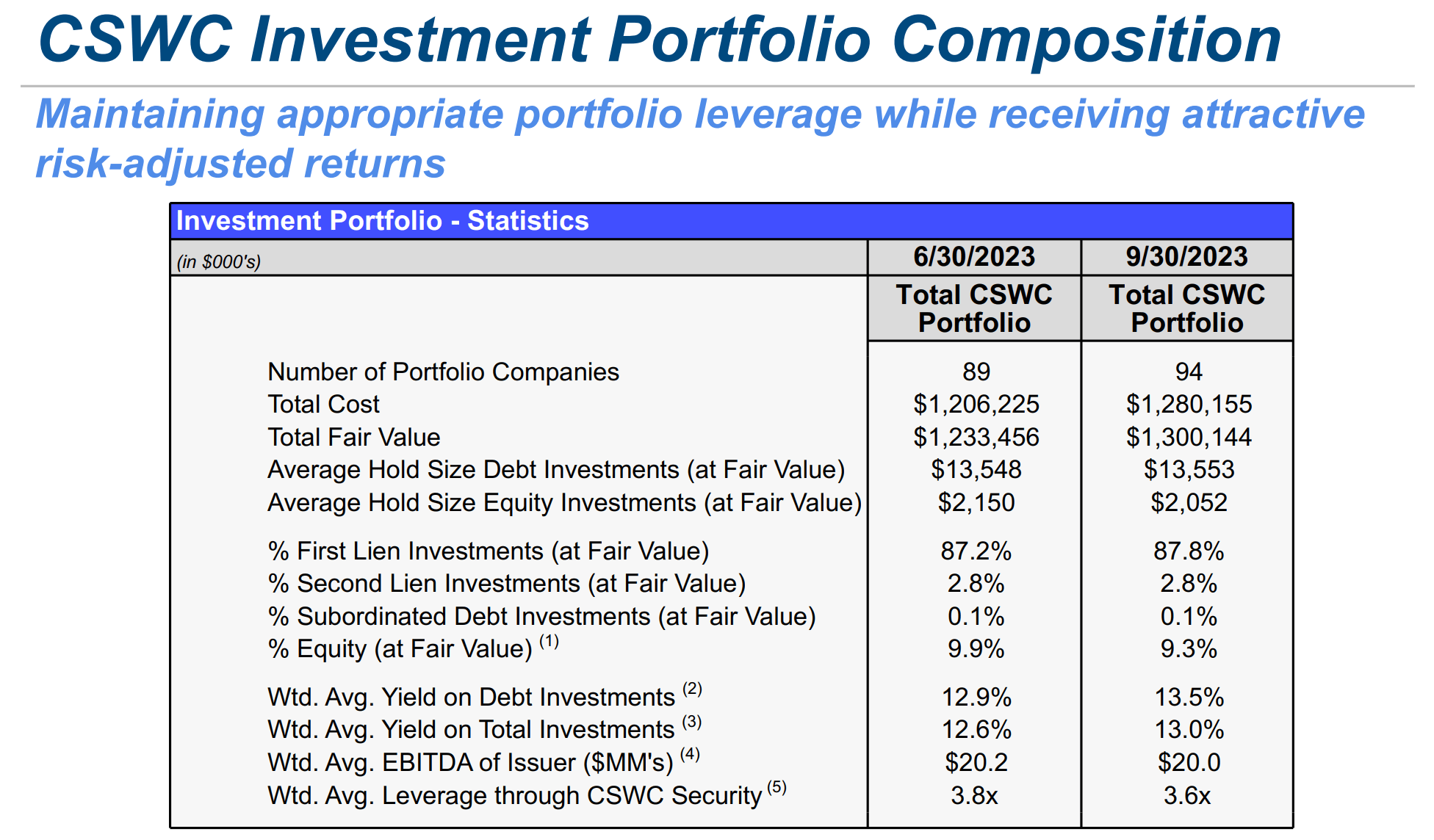

At present, CSWC has an investment portfolio worth $1.3 billion at fair value, covering 94 portfolio companies. It also has a fair amount of equity in its portfolio companies, giving it one of multiple avenues to grow its net asset value. As shown below, 88% of CSWC’s investments are in the form of first lien debt investments, which carry the least risk compared to other investment tranches. Another 3% is in second lien secured debt and 9.3% is invested in equity of its portfolio companies.

{kind=link}

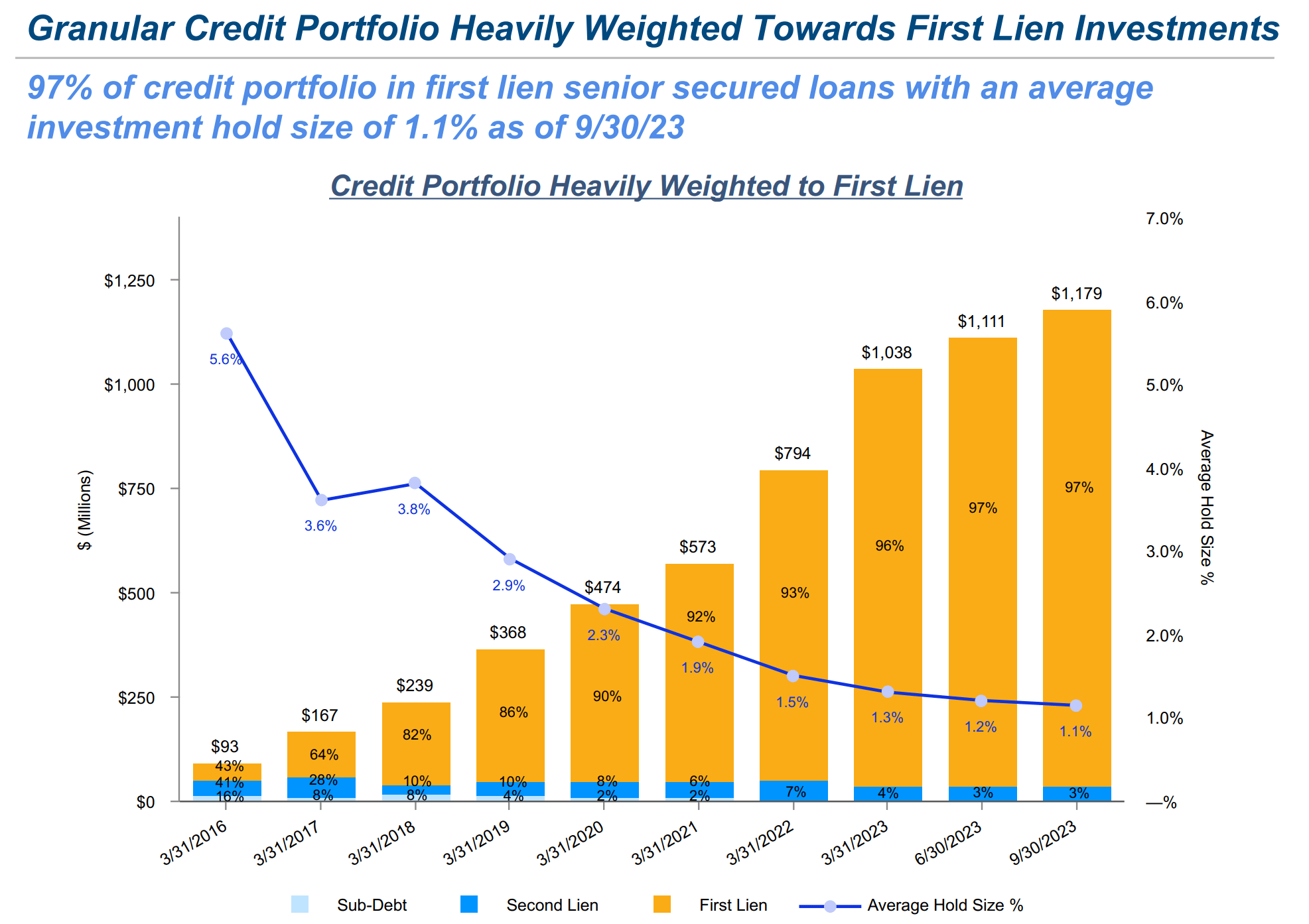

Importantly, CSWC has de-risked its portfolio in recent years through diversification. This has resulted in the average portfolio holding declining from over 5% of the portfolio in 2016 to just 1.1% as of the last reported quarter. Additionally, CSWC has heavily increased its exposure to safer first lien debt investments, which now represent 97% of the debt portfolio, up substantially from 43% in 2016.

{kind=link}

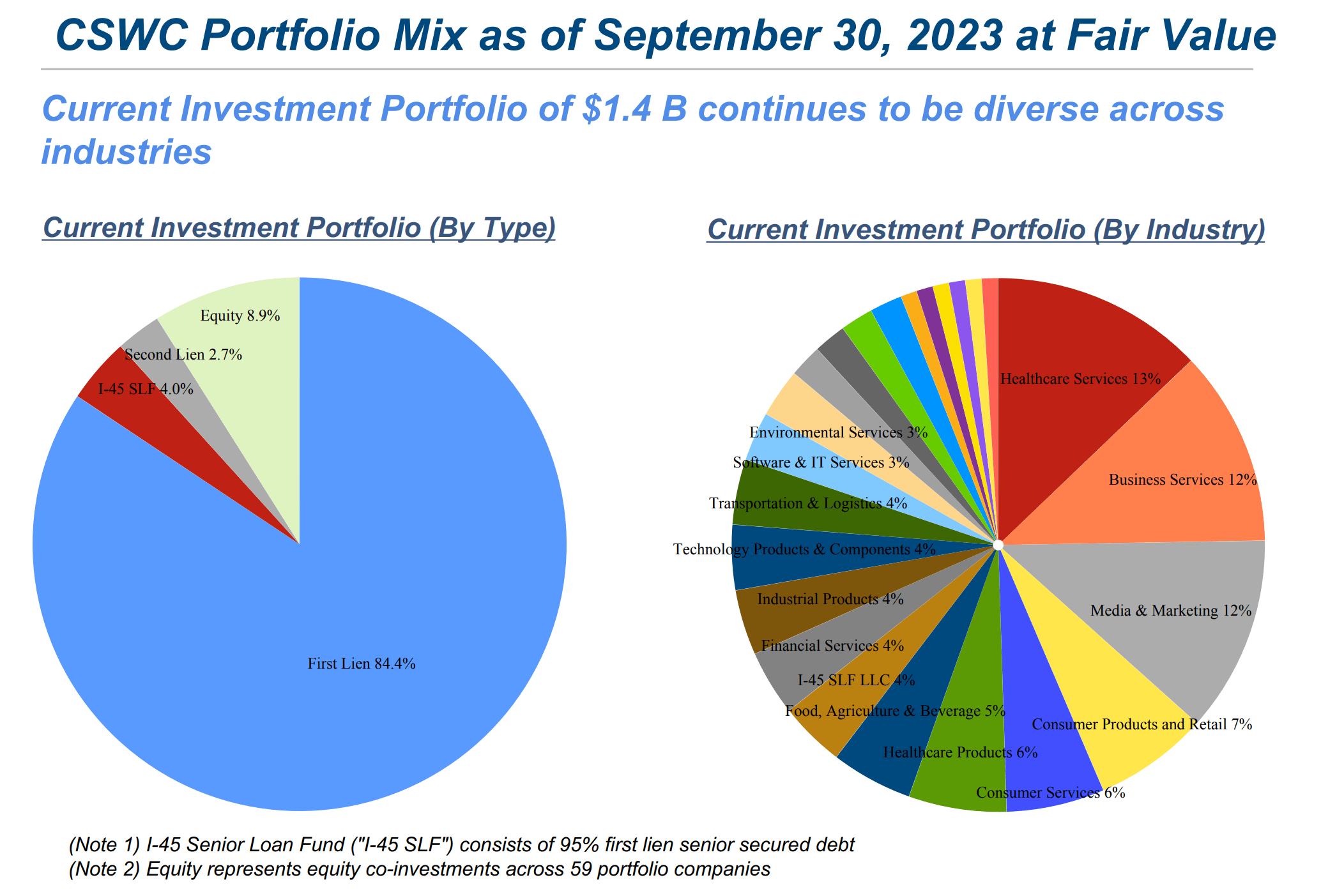

Unlike internally managed peers Hercules Capital ( HTGC ) and Trinity Capital ( TRIN ), CSWC is not heavily involved in the technology segment, as its investments are concentrated around companies that are easy to understand and serve as the bread-and-butter of the economy. As shown below, Healthcare Services, Business Services, Media & Marketing, Consumer Products and Services comprise half of its portfolio.

{kind=link}

Meanwhile, CSWC’s portfolio continues to perform well in the current interest rate environment, generating NII per share of $0.67 during the fiscal second quarter (ended September 30 th ), representing 24% growth from $0.54 in the prior year period. This was driven by higher interest rates, given that most of CSWC’s debt investments are carried at floating rate.

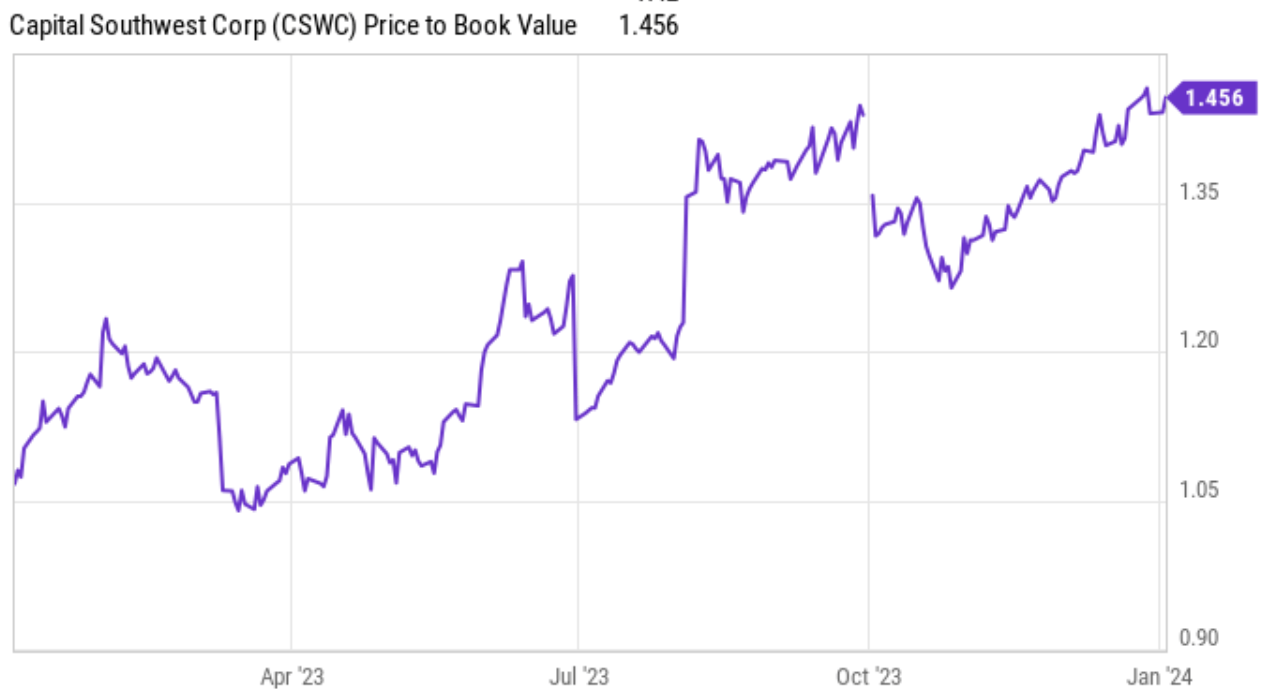

Growth in NII was also driven by CSWC’s ability to raise capital at an appealing premium to net asset value, enabling CSWC to grow its total assets by $214 million in the first nine months of 2023. This was driven by the fact that CSWC has traded at a price-to NAV ranging from 1.05x to 1.46x, as shown below.

{kind=link}

This compares favorably to many externally-managed BDCs, which are trading at a comparatively smaller premium to NAV and, in some cases, even a discount to NAV. As one can imagine, it doesn’t take as many new shares to raise fresh capital when the price is at a substantial premium to NAV compared to when the price is at just a slight premium to NAV.

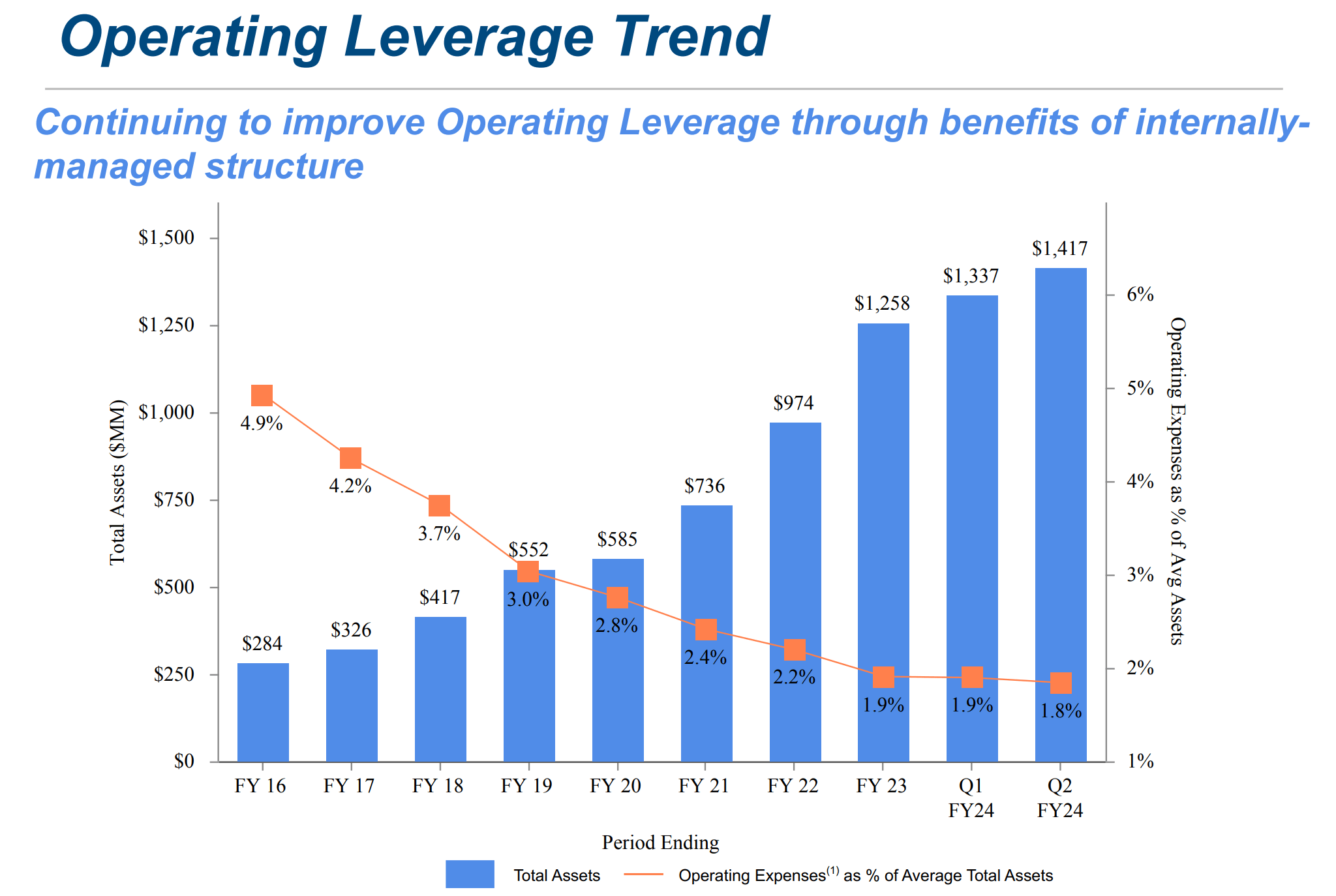

Importantly, CSWC continues to flex its muscle as operating expense as a percentage of average total assets continues to decline, from 3.0% in FY19 to 1.8% in the last reported quarter. While CSWC still has room for improvement as compared to the 1.3% expense ratio of Main Street Capital ((MAIN)), it could continue to see improvement as it benefits from increased scale. For reference, many externally-managed BDCs like Ares Capital ( ARCC ) charge a base management fee of 1.5% and additional fees beyond a certain hurdle rate, which could drive the total fee to well above 2%.

{kind=link}

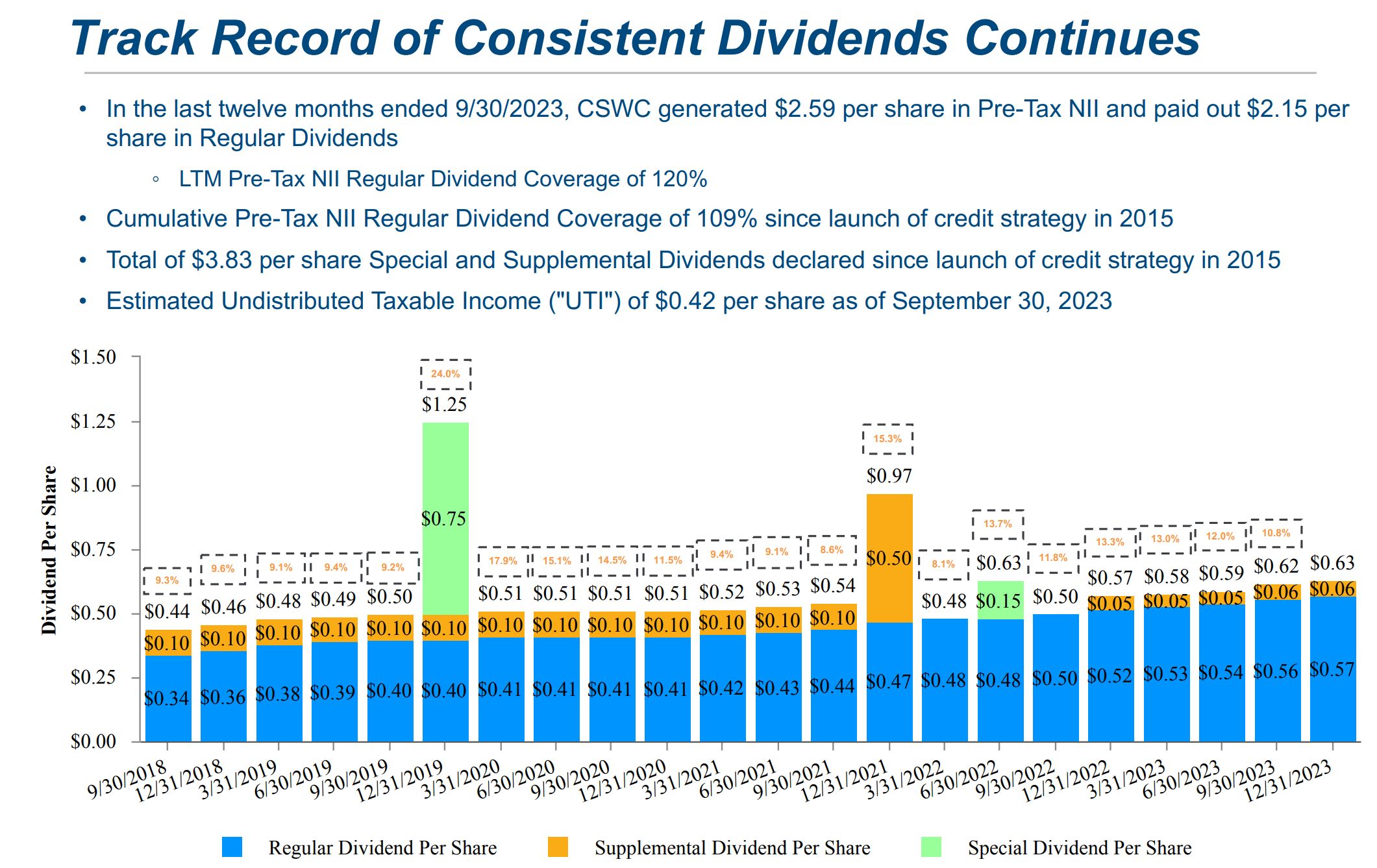

Having an efficient cost structure enables CSWC to return more of its earnings to shareholders. As shown below, CSWC has a steady track record of raising its regular dividend payout while paying special dividends along the way. Speaking of which, the current regular dividend rate is well-covered (by BDC standards) by NII at an 85% payout ratio.

{kind=link}

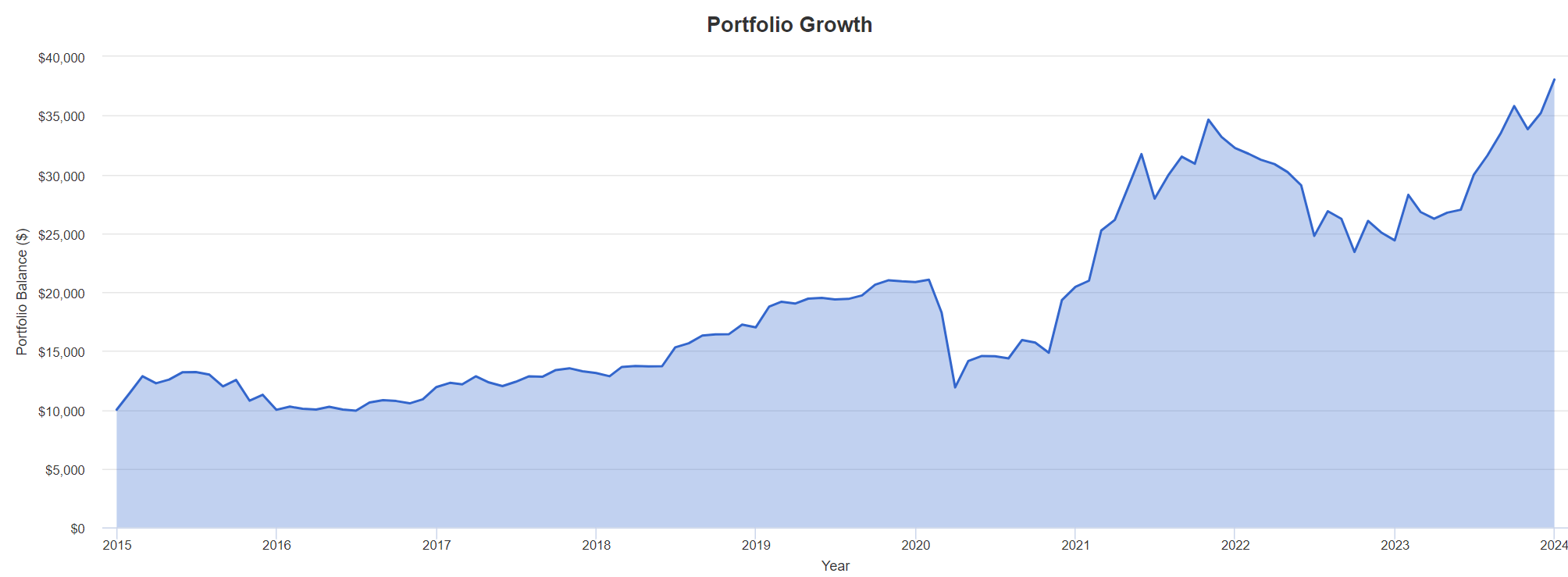

As shown below, thanks to the power of compounding dividends, an investor who made a $10,000 investment in CSWC in 2015 would see their investment balance grow to $38,000 after reinvesting dividends along the way.

{kind=link}

Looking ahead, CSWC is well-positioned to grow its portfolio in an accretive manner through equity issuances, considering that it currently trades at a 1.46 premium to NAV at the current price of $23.98. It also has strong balance sheet capacity, as it carries a regulatory debt-to-equity ratio of 0.92x, sitting well below the 2.0x statutory limit. CSWC also carried $207 million cash and undrawn leverage as of the last reported quarter, giving it flexibility to make opportunistic investments.

Risks to CSWC include potential for lower interest rates, which may lead to lower yields for CSWC’s investments. However, the market expects just three quarter point rate cuts this year, which would leave the benchmark rate at around a still elevated 4.5% rate.

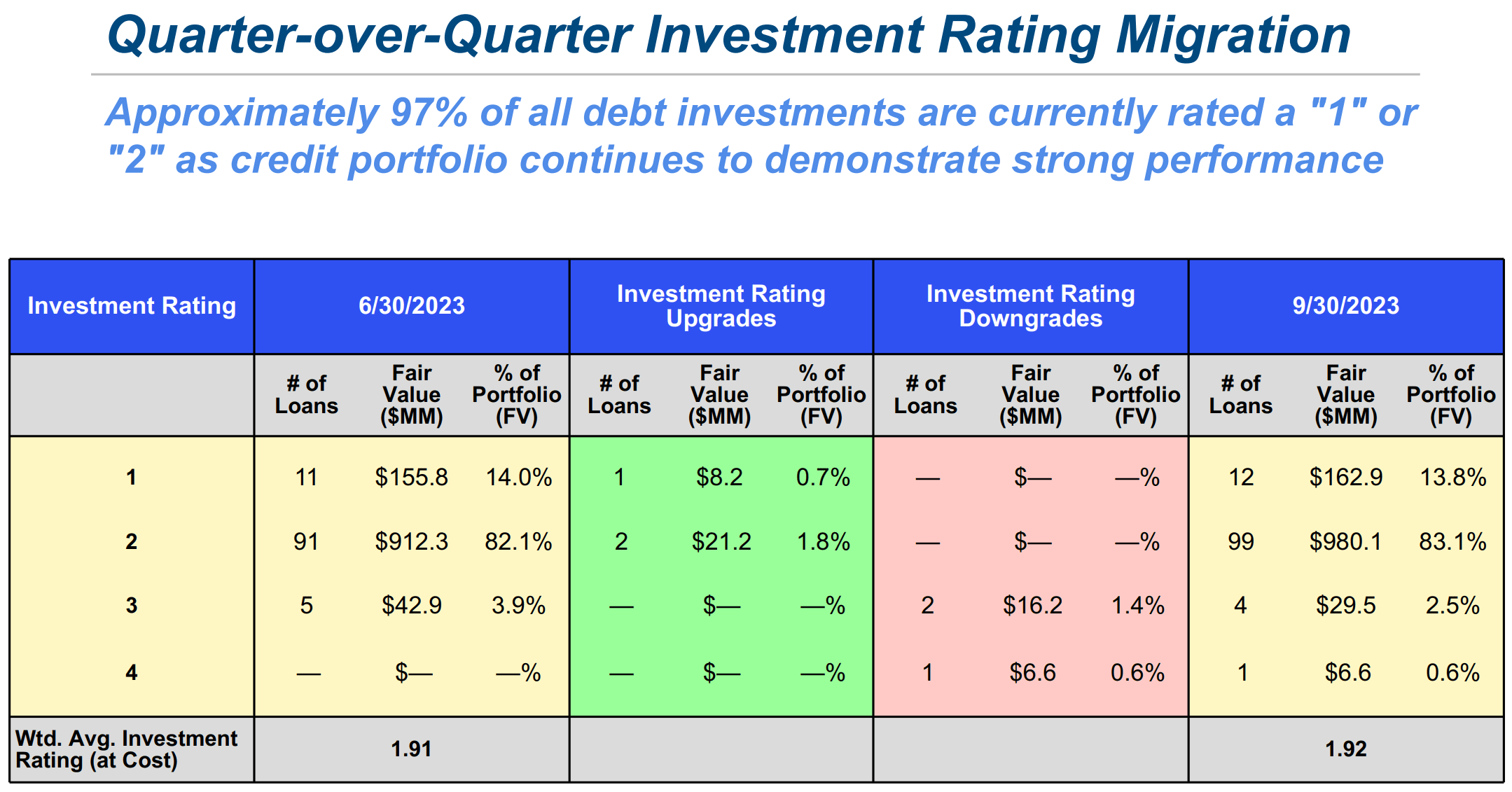

Other risks include potential for economic volatility and uncertainty, which could pressure borrowers. Nonetheless, CSWC’s portfolio health has remained stable with more investments sitting in the top 2 ratings on a sequential basis, and just 1 investment representing 0.6% of the portfolio fair value sitting in the lowest rating, as shown below.

{kind=link}

Admittedly, CSWC is no longer cheap at the current price of $23.98 with a Price-To-NAV ratio of 1.46x. While some investors may dislike paying a substantial premium to NAV, I continue to believe that well-run internally managed BDCs deserve to be valued based on Price-To-Earnings due to their efficient cost structures, and that’s how CSWC is able to pay a high and well-covered 9.5% dividend yield while trading at a substantial premium.

From a forward PE standpoint of 9.0x, CSWC does not appear to be prohibitively expensive. Even in a no-growth scenario, investors can collect the 9.5% yield plus a boost from special dividends, and with potential for portfolio and dividend growth down the line as CSWC can raise equity capital in an accretive manner at the current price.

Investor Takeaway

Overall, CSWC continues to be a solid investment option for investors seeking income and growth potential. Its diversification strategy and focus on safer first lien debt investments have proven to be successful in generating strong returns in the current interest rate environment. With a strong track record of dividend growth and efficient cost structure, CSWC has been able to provide attractive dividends while also growing its portfolio.

While CSWC is no longer the deep value that it was last year, I continue to see merits in owning this growing player for the aforementioned reasons at the current price and high and well-covered yield. Considering that CSWC is not deeply undervalued anymore, I'm downgrading it from a 'Strong Buy' to a 'Buy' at present.

For further details see:

Capital Southwest: High Yield, Low Leverage And Expenses Make It A Buy