HTGC - Capital Southwest: This 10.6% Yielding BDC Is Now Overvalued (Downgrade)

2023-10-12 03:03:17 ET

Summary

- Capital Southwest has good dividend coverage and recently raised its dividend.

- Despite payments of supplemental dividends and regular dividend growth, the risk/reward ratio is no longer attractive.

- CSWC trades at a premium valuation, and passive income investors can buy better-priced BDCs with comparable yields and higher margins of safety.

Capital Southwest Corporation ( CSWC ) is a well-managed business development company that has a history of raising its dividend payout and paying supplemental dividends in order to distribute excess portfolio income.

The BDC has a first-lien-centered investment portfolio, and Capital Southwest recently increased its regular dividend by 3.7% QoQ.

Capital Southwest also consistently covered its dividend payout and supplemental dividend with net investment income in the last year. While the 10.6% yield is covered by net investment income, the BDC's stock is now trading at a substantial premium to net asset value, which is indicative of a potential overvaluation.

My Rating History

I presented Capital Southwest as an intriguing passive income investment opportunity Capital Southwest : A Quality 11.4% Yield With A Reasonable Valuation in December 2022, primarily because the BDC was selling at only a small premium (10%) to net asset value.

This has profoundly changed in the last ten months, and CSWC is now trading at a 40% premium to net asset value, which to me indicates that other BDCs are now offering passive income investors better value.

Because I consider CSWC to be overvalued at a 1.4x NAV multiple, particularly because lower-priced BDC alternatives are available that pay similar yields, my stock classification changes to Sell. I will provide investment alternatives in this article as well.

Capital Southwest's Well-Diversified Investment Portfolio And First Lien-Focus

Capital Southwest is a BDC whose portfolio was valued at $1.2 billion at the end of the second quarter and included mostly highly-ranked first-lien debt. Approximately 87% of the company's investments were made in the highest rates forms of debt, while the remainder has been invested in other debt investments (Second Lien and Subordinated) as well as Equity.

Investment Portfolio Overview (Capital Southwest Corp)

Capital Southwest's portfolio is well-diversified and largely includes business sectors that are set to perform well during recessions. The sectors include the likes of business, healthcare, and media services, which are recession-resistant and expose Capital Southwest to fewer investment risks than more cyclical sectors such as transportation, energy, airlines, or hotels.

Current Investment Portfolio By Industry (Capital Southwest Corp)

Consistent Dividend Coverage

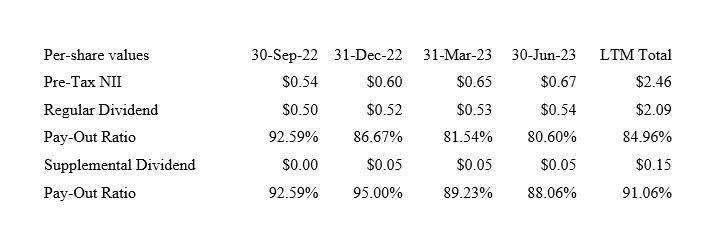

Capital Southwest provided passive income investors with decent dividend coverage of approximately 85-91% in the last year, depending on whether or not you include supplemental dividends. In the most recent quarter, Capital Southwest earned $0.67 per share in net investment income (pre-tax) and paid out a total of $0.59 per share (made up of a $0.54 per share regular dividend plus a $0.05 per share supplemental dividend).

Both the regular and supplemental dividends have been covered by net investment income and the BDC earned its dividend in each of the last four quarters.

Given the history of paying supplemental dividends, I think that passive income investors can continue to expect the payment of ~$0.05 per share per quarter moving forward.

Dividend (Author Created Table Using BDC Information)

{kind=link}

History Of Aggressive Dividend Growth

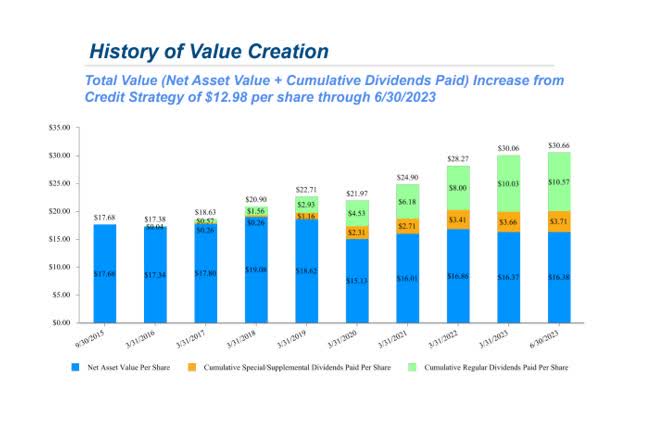

Capital Southwest has returned a lot of cash to passive income investors over time, particularly in the last five years, when the payment of supplemental dividends accelerated. The BDC increased its regular dividend to $0.56 per share in the September quarter, reflecting a 3.7% increase over the prior quarter.

Dividend Growth (Capital Southwest Corp)

{kind=link}

Other Investment Options

This article would not be complete without at least mentioning a number of BDCs that I believe provide better value for passive income investors.

One of my all-time favorite BDCs is Oaktree Specialty Lending Corp. ( OCSL ) which offers investors strong credit management performance over time. The BDC also occasionally paid special dividends to supplement the regular dividend and distribute excess portfolio income.

Another BDC I value highly is Hercules Capital Inc. ( HTGC ) which is a niche-focused BDC with very strong dividend coverage metrics and consistent portfolio growth . Hercules Capital also has excellent portfolio quality.

Passive income investors that like a little bit more risk and seek an opportunistic recovery play in the BDC sector may want to take a look at 15% yielding TriplePoint Venture Growth ( TPVG ) .

40% Premium To Net Asset Value

In the quarter ended June 30, 2023, Capital Southwest reported a net asset value of $16.38 per share. Since CSWC is now selling for $22.90, the BDC is valued at a 40% premium to net asset value.

Other BDCs, like OCSL, are selling at much lower net asset value multiples, so passive income investors don't need to pay a 40% premium to access healthily covered double-digit dividend yields.

Oaktree Specialty Lending and Ares Capital ( ARCC ) also offer yields in excess of 10%, and they are trading at valuations that improve investors' margin of safety. Particularly now that valuations in the BDC market have dropped, I think passive income investors can choose many better-priced BDCs.

CSWC is valued at 9.0x LTM net investment income, while OSCL costs 8.0x LTM net investment income and ARCC requires passive income investors to pay 8.3x LTM net investment income. Put simply, other BDCs offer better net investment income yields as well as comparable dividend yields.

Reasons For Premium Valuation

Capital Southwest is trading at a premium valuation because the BDC has seen strong growth in its net investment income in the last year, which is related to the company's 97% floating-rate positioning that has paid dividends for CSWC.

Capital Southwest grew its net investment income to $0.67 per share in 2Q-23, reflecting growth of 34% YoY, primarily because the BDC's floating-rate investments paid stronger income in a rising-rate world.

With that said, though, I think that the present trajectory of inflation limits the BDC's net interest income growth. Inflation has moderated to just 3.7% , compared against 8.3% in the year-ago period. With the central bank having less reason to increase interest rates, these net interest income tailwinds should be less substantial moving forward.

While this is also true for other BDCs, Capital Southwest's premium valuation reflects no margin of safety, in my view, and I see the stock as more vulnerable to a correction if the central bank embarks on a rate-lowering cycle.

Taking into account that other BDCs trade at less inflated valuation multiples, I would prefer BDCs such as ARCC or OSCL.

Capital Southwest And Investment Risks

Passive income investors that are selling into the strengths now are running the risk of losing out on incremental upside, though I think that this risk is rather negligible when taking into account how strong of a run Capital Southwest's stock has already had.

Since CSWC is selling for a whopping 40% premium to net asset value, I think the risk/reward ratio is not favorable enough to justify establishing a new position.

A deterioration in dividend coverage would indicate that CSWC could drop its supplemental dividend, which may impact valuation. My biggest concern, however, remains Capital Southwest's premium valuation and lack of a substantial margin of safety.

My Conclusion

Capital Southwest is a well-managed BDC with a strong focus on high-quality first lien debt and the BDC has a good record in growing its dividend as well as supplemental dividends.

The payout overall has been consistently covered by net investment income in the last year, and passive income investors will likely continue to receive a $0.05 per share supplemental dividend moving forward.

With that said, Capital Southwest has performed extremely well, resulting in a premium valuation. I think that the risk/reward profile is presently not favorable, and I would recommend the other BDCs mentioned in this article as a potential substitute for CSWC, depending on risk tolerance. Sell.

For further details see:

Capital Southwest: This 10.6% Yielding BDC Is Now Overvalued (Downgrade)