CFFN - Capitol Federal Financial: Cheap And Worth Considering

2023-09-14 13:00:00 ET

Summary

- Capitol Federal Financial has shown no significant recovery in the banking sector and is still down 36% compared to February.

- The bank has a low exposure to uninsured deposits, making it a potentially attractive prospect.

- The institution has experienced growth in net interest income and non-interest income, but has seen a decline in net profits due to higher interest expenses.

- But it still is cheap enough to be worth consideration.

Even though the stock market is up quite a bit so far this year, not every sector is performing well. The banking sector, for instance, has shown some signs of weakness. This is largely the result of the banking crisis that began in March and that only ended after the collapse of multiple regional banks. Since then, many of the banks that did survive have posted sizable partial recoveries. But there have been a select few that have shown no significant recovery. A great example of this latter category would be Capitol Federal Financial ( CFFN ).

Driven by high amounts of debt, declining profits, and continued weakness when it comes to deposits, Capitol Federal Financial is still down 36% compared to where the stock ended in February of this year. For context, at its low point after February, shares were down as much as 37.4%. So we are very near to the bottom still. Normally, the continued decline in deposits would cause me to be concerned. But when you consider how little exposure the bank has to uninsured deposits, which were the same kind of deposits that created the banking crisis, I would argue that the company could make for an attractive prospect at this time.

A cheap bank

As a small commercial bank, Capitol Federal Financial provides all the primary services that many other banks of its size due. Examples here include offering deposit services, not only for the general public, but also for businesses. The company gives out loans, including commercial loans, mortgages, and more. It also makes investments in various securities, including mortgage-backed securities. As of the end of its most recent fiscal year, the institution had 54 different branches spread between nine counties in Kansas and three counties in Missouri. 45 of these branches are traditional in nature, while the remaining nine are in store branches. Although this may not seem like the institution is all that large, as of the end of its 2022 fiscal year, it handled about 6.4% of all banking deposits in the state of Kansas, making it the second-largest by market share in the state.

{kind=link}

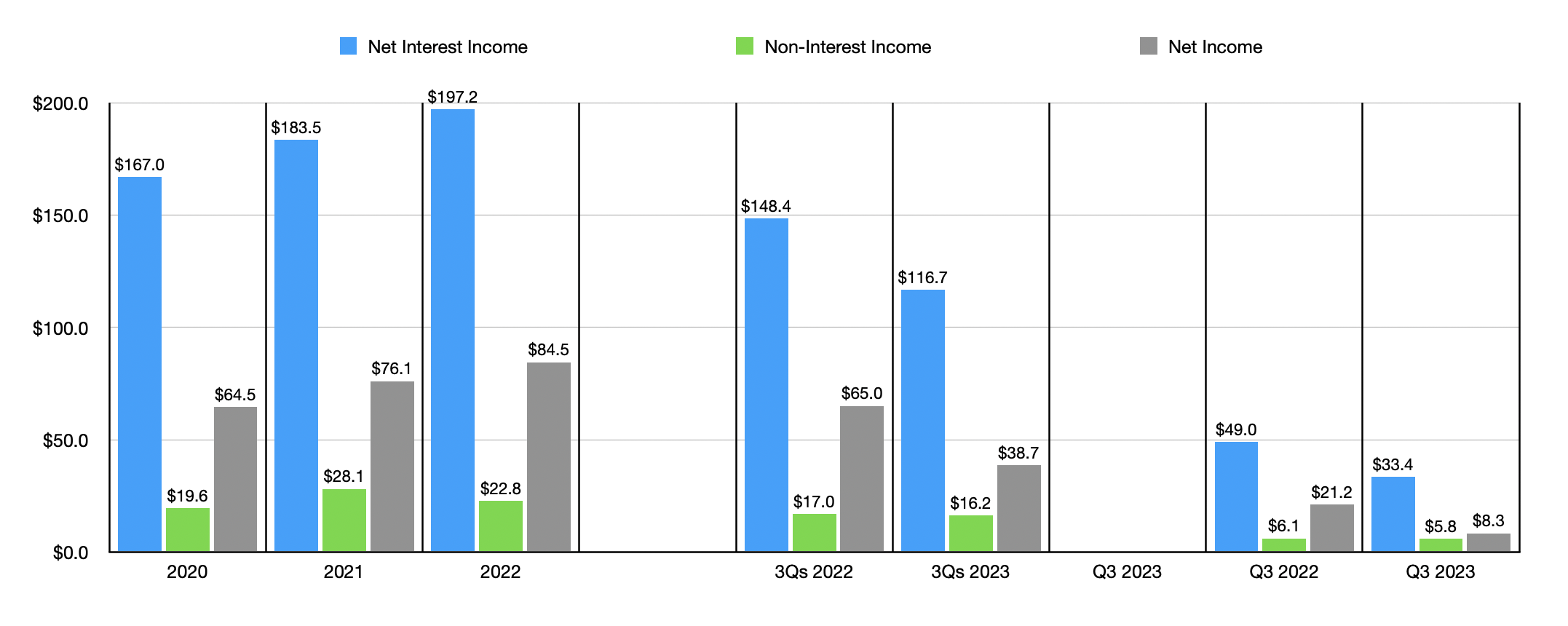

Over the past few fiscal years, Capitol Federal Financial has done quite well to grow both its top and bottom lines. Net interest income, for instance, managed to rise from $167 million in 2020 to $197.2 million in 2022. Over this window of time, non-interest income inched up from $19.6 million to $22.8 million. Both of these, combined, caused net income to grow from $64.5 million to $84.5 million. This is not to say that everything has gone fantastic from a revenue and profit perspective. The sad truth is that this year is looking to be a bit painful. In the first three quarters of 2023 , net interest income for the bank came in at $116.7 million. That's down from the $148.4 million achieved one year earlier. As the chart above illustrates, both non-interest income and net profits also declined on a year-over-year basis, with the latter dropping by almost half from $65 million to $38.7 million.

A lot of this pain recently has come from higher interest expense that the company has had to cover. For the first nine months of 2023, for instance, interest paid on deposits totaled $52.5 million. This was more than double the $25.4 million reported one year earlier. Higher amounts that had to be paid on certificates of deposit and money market accounts, both of which have become far more popular over the past couple of years because of higher interest rates, were responsible for this. But the real pain came from a surge in the interest expense paid on borrowings. This jumped from $28 million last year to $96.5 million this year. That, according to management, was driven by two things. First, borrowings have increased for the bank. At the end of 2022, for instance, the bank had $2.13 billion of debt on its books. As of the end of the third quarter, this number had grown to $2.99 billion. On top of this, a general increase in interest rates caused by Federal Reserve policy aimed at combating inflation has also proven to be problematic for the bank.

{kind=link}

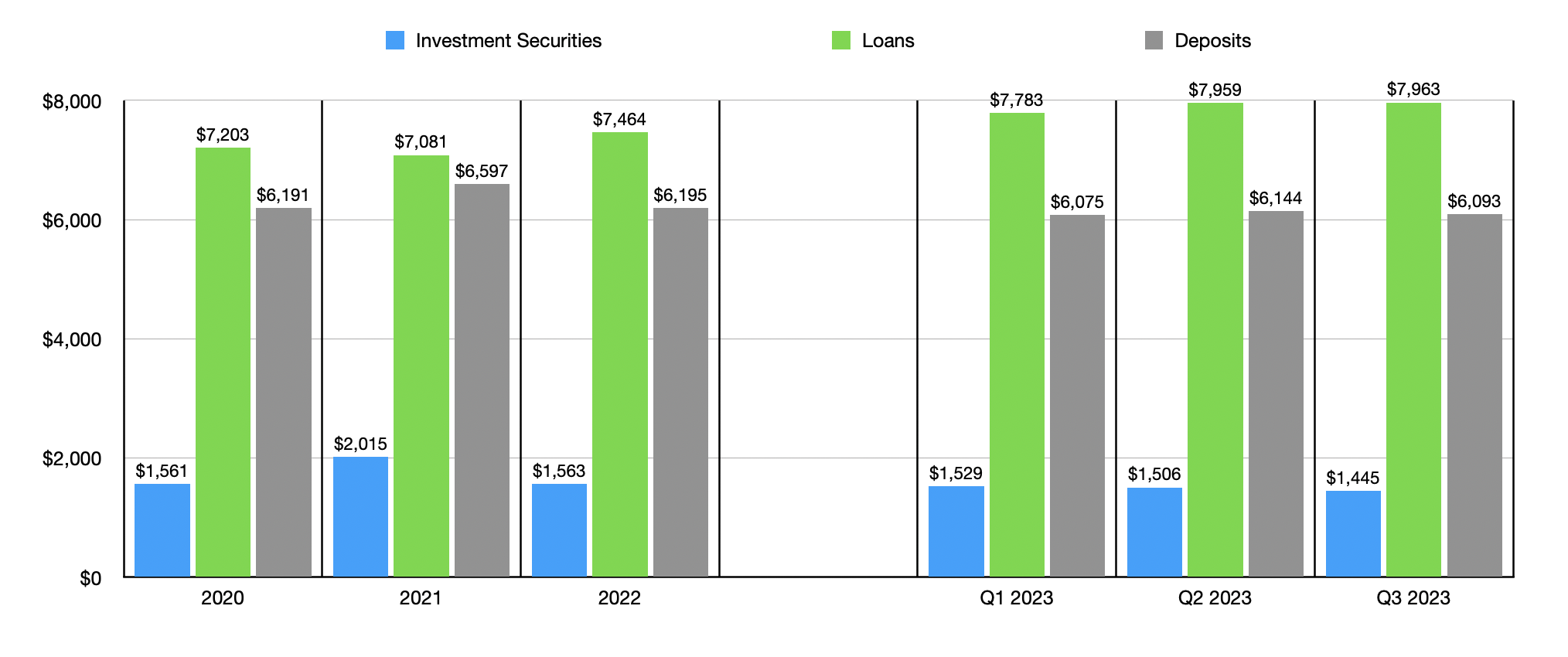

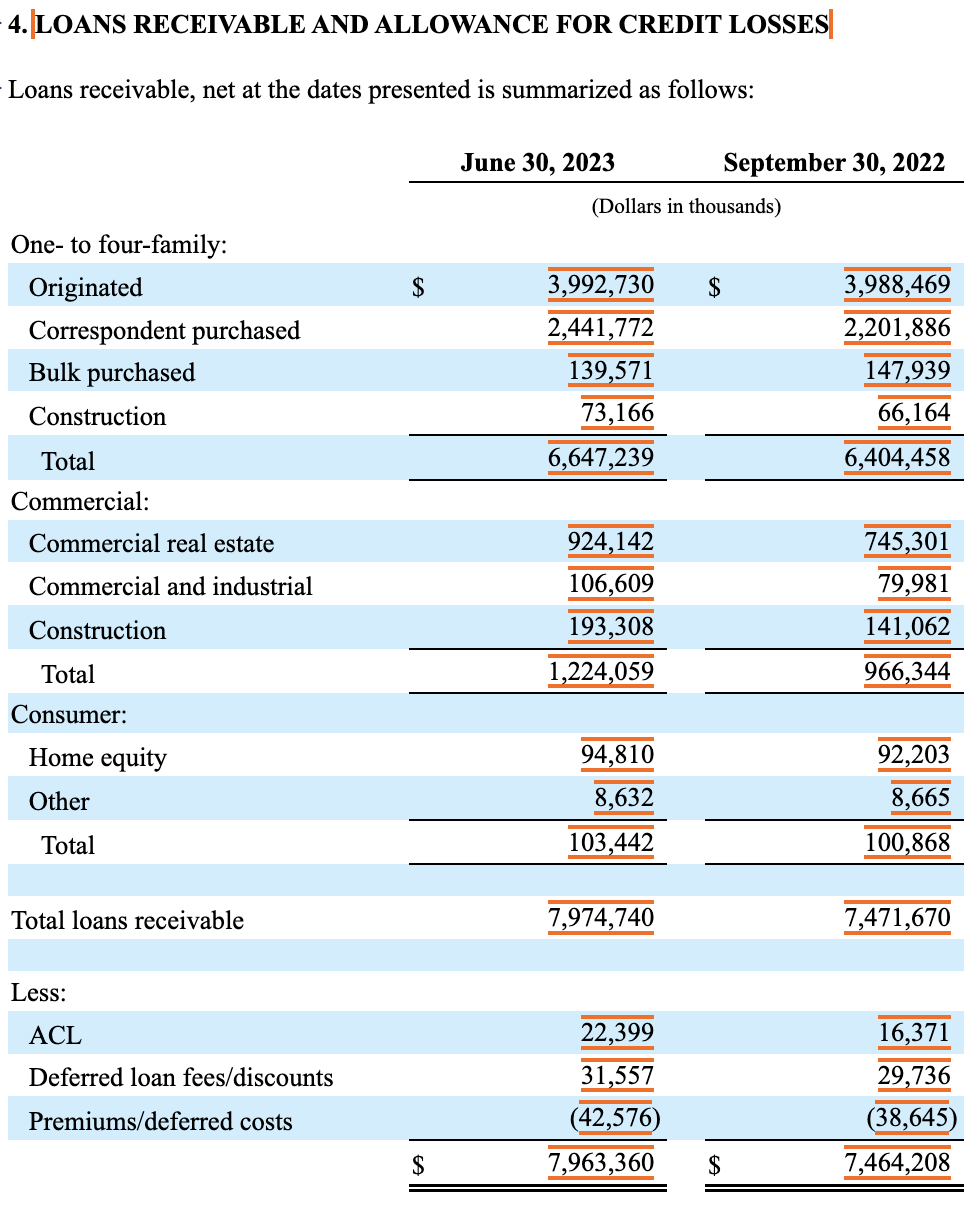

The growth that the institution saw between 2020 and 2022 was made possible by continued investments made in the form of loans and various securities. Available for sale securities remained more or less flat at around $1.56 billion during that three-year window, though there was a spike to $2.01 billion in 2021. Meanwhile, the value of loans increased from $7.20 billion to $7.46 billion. We have seen that increase continue this year, with a total reading as of the end of the most recent quarter of $7.96 billion even as available for sale securities dropped to $1.44 billion. It is worth mentioning the composition of the loans that the bank has. As of the end of the most recent quarter, 83.4% of all loans outstanding we're in the form of one to four family properties. About $2.58 billion of this amount was in the form of loans that the bank purchased, with about $3.99 billion involving loans that it originated. The second-largest concentration of loans involved commercial properties, at about $1.22 billion. That works out to roughly 15.3% of all loans today.

{kind=link}

Unlike most banks, which happen to fuel loan growth largely with deposit growth, Capitol Federal Financial has actually taking on a strategy of accepting higher amounts of debt and reinvesting that capital for the purpose of generating returns. Meanwhile, deposits have remained largely unchanged. At the end of 2022, they were $6.19 billion. We saw a slight drop to $6.07 billion in the first quarter of this year before experiencing a slight rebound to $6.14 billion during the second quarter. However, in the third quarter, which was the first full quarter for which the effects of the banking crisis played out, deposits fell again, totaling $6.09 billion. Though that is not a large drop, it is still discouraging to see during these uncertain times. The really good thing about the deposit picture, however, is that, as of the end of the most recent quarter, only 11.1% of deposits were classified as uninsured. This is some of the lowest exposure that I have seen in a bank this year. That certainly makes the picture better from a risk perspective.

{kind=link}

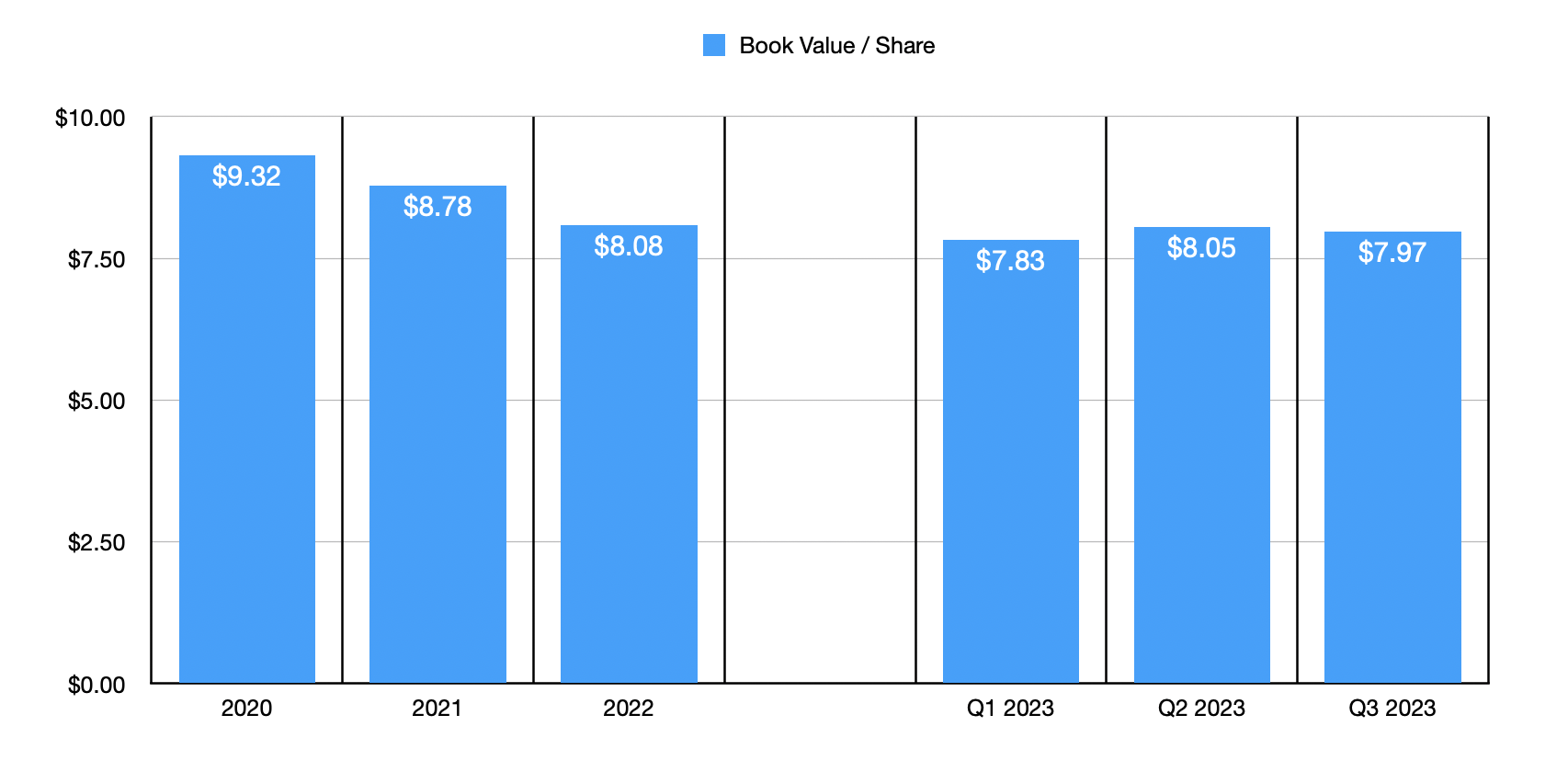

Other than the high amount of leverage and the recent drop in deposits, the only negative that I see with Capitol Federal Financial is that its book value per share has a history of declining from year to year. From 2020 to 2022, it dropped from $9.32 to $8.08. As of the end of the most recent quarter, it totaled $7.97. Even though this is a negative, it is worth mentioning that shares are currently trading at only 67.4% of the company's book value. And, using results from 2022, the stock is trading at a price-to-earnings multiple of 8.7. This is quite attractive, though not the cheapest that I have seen by any means.

Takeaway

All things considered, I must say that I am fairly pleased with Capitol Federal Financial. It's a bit more complicated to digest its fundamental picture because it deviates in multiple ways, some positive, and some negative, from many of the other banks that I have looked at. Uninsured deposit exposure is lower, but overall deposits have really failed to grow. Debt is high while the book value per share has continued to drop. Prior to this year, the bank had done quite well in terms of growing its top and bottom lines. But we have seen some weakness this year because of higher interest rates. This is most certainly a mixed bag when all is put together. But on the whole, I feel as though the bank is attractive enough to rate a soft 'buy' at this time.

For further details see:

Capitol Federal Financial: Cheap And Worth Considering