CGRN - Capstone Green Energy: Equity Holders To Retain Majority Ownership Following Emergence From Bankruptcy

2023-09-29 11:30:13 ET

Summary

- Ailing microturbine manufacturer files for bankruptcy protection to implement a prepackaged plan of reorganization agreed on with its sole secured lender Goldman Sachs.

- The restructured company is expected to emerge within 42 days with improved liquidity and substantially lower debt levels.

- Surprisingly, common equity holders will retain a majority stake in the restructured business.

- The all-new Capstone Green Energy Corporation is projected to achieve substantial profitability within the next few quarters.

- Existing equity holders should abstain from selling their shares near all-time lows and rather wait for the restructured company to deliver upon management's projections.

Note:

I have covered Capstone Green Energy Corporation ( CGRN ) previously, so investors should view this as an update to my earlier articles on the company.

On Thursday, ailing microturbine manufacturer Capstone Green Energy Corporation, or "Capstone" filed for Chapter 11 bankruptcy protection after entering into a transaction support agreement with affiliates of Goldman Sachs ( GS ), the company's sole secured lender (emphasis added by author):

Capstone Green Energy Corporation (...) has entered into a transaction support agreement ("TSA") with Goldman Sachs Specialty Lending Group, L.P., in its capacity as collateral agent (the "Collateral Agent") under that certain Amended and Restated Note Purchase Agreement, dated as of October 1, 2020 (as amended, the Note Purchase Agreement), and Broad Street Credit Holdings LLC, an affiliate of the Collateral Agent, in its capacity as purchaser (Consenting Lender) under the Note Purchase Agreement, and in connection therewith has initiated a prepackaged restructuring. This is a significant step towards expediting the Company's corporate restructuring efforts, with the primary objectives of significantly reducing Capstone's debt burden, injecting additional liquidity into its operations, and ultimately paving the way for the sustained and prosperous future of its business .

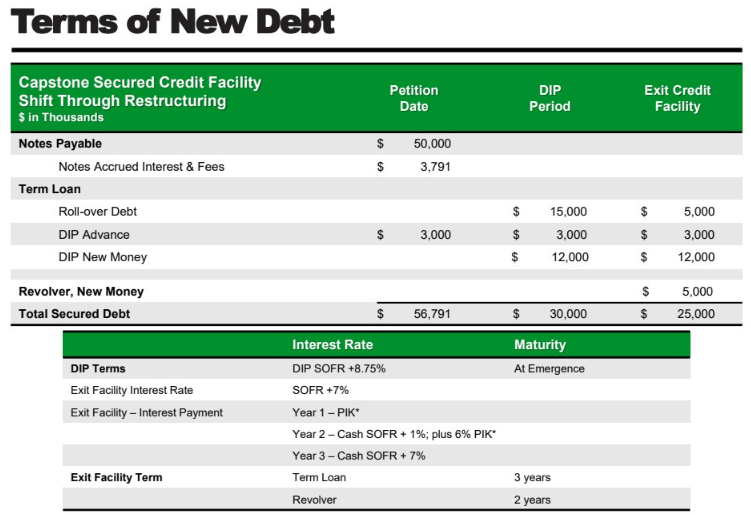

"The transactions contemplated by the TSA have been carefully designed to preserve and enhance value for all our stakeholders," said Robert C. Flexon, Interim President and Chief Executive Officer. " The new financings provide much-needed liquidity to ensure near-term stable operations and, importantly, upon emergence, our pre-petition debt and accrued interest of more than $56.0 million will decrease to $25.0 million resulting in significantly improved financial health and longer-term financial stability ."

Perhaps most importantly, common equity holders will retain a majority stake in the restructured business (emphasis added by author):

To implement Capstone's prepackaged restructuring, Capstone and certain of its subsidiaries (the Debtors) filed voluntary Chapter 11 petitions for relief in the U.S. Bankruptcy Court for the District of Delaware (the Bankruptcy Court). The TSA and the joint prepackaged Chapter 11 plan of reorganization (the Plan) contemplate the Debtors effectuating certain transactions pursuant to which the Company will become a private company (Reorganized PrivateCo) that will continue to own assets consisting of (i) right, title, and interest in and to the certain trademarks of Capstone and (ii) all assets relating to distributor support services (the Retained Assets). Capstone Turbine International, Inc., a subsidiary of the Company, will be renamed Capstone Green Energy Corporation (Reorganized PublicCo), which expects to be the successor to Capstone for purposes of Securities and Exchange Commission reporting and will be the successor to Capstone with respect to certain of its business, assets, and liabilities through its ownership interest in a new operating subsidiary.

Under the Plan, all holders of Allowed General Unsecured Claims will receive payment in full in cash in the ordinary course or such other treatment so as to render such claim unimpaired under the Bankruptcy Code. Existing stockholders of the Company will receive their pro rata share of 100% of the equity in Reorganized PublicCo, subject to dilution from any stock that may be issued as equity incentive compensation to employees. All existing warrants and restricted stock units will be canceled and will not receive any distribution. Other than the Retained Assets described above, the existing operating assets and liabilities of the Company will be transferred to a "New Subsidiary" (with certain limited exceptions), the common shares of which will be 100% held by Reorganized PublicCo, and 100% of its non-dilutable preferred shares will be held by Reorganized PrivateCo. On a fully diluted basis, Reorganized PublicCo will own 62.5% of New Subsidiary, and Reorganized PrivateCo will own 37.5%.

In layman's terms:

Goldman Sachs will own 100% of a private company that holds the rights to Capstone's trademarks and all assets relating to the company's distributor support services. In addition, this company will be allocated new preferred shares, which will be convertible into a 37.5% stake in the restructured business.

Capstone's current equity holders will be allocated 100% of the restructured business (subject to dilution from a new equity incentive program), a public entity expected to trade on the OTC markets:

{kind=link}

Assuming full conversion of Goldman Sachs' preferred shares, Capstone's current equity holders will retain a respectable 62.5% of the restructured business.

In addition, Goldman Sachs has agreed to provide $30 million in debtor-in-possession ("DIP") financing, which consists of $12 million in new money and the roll-up of $18 million in existing claims.

Exit financing is expected to total $25 million plus accrued DIP interest, consisting of $20 million in DIP claims and a $5 million committed revolving credit facility:

{kind=link}

In addition, the exit financing credit documents will provide for a $10.0 million uncommitted incremental facility and up to a $10.0 million asset-based revolver debt basket, with the latter requiring the repayment of the $5 million exit revolving credit facility.

In contrast to its current iteration, the restructured Capstone business is expected to be quite profitable with decent gross margins and substantial EBITDA generation:

{kind=link}

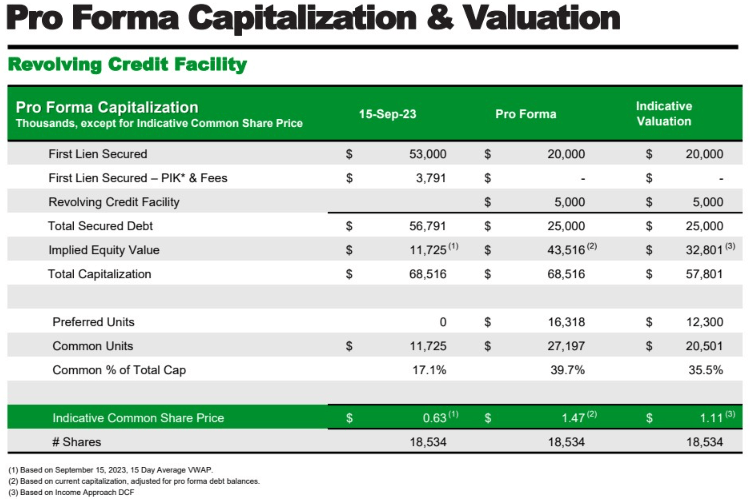

Based on a discounted cash flow valuation, the indicative common share price is stated at $1.11:

{kind=link}

However, the company hasn't provided sufficient details of its revised business approach to fully assess management's financial projections which, at least in my opinion, appear quite ambitious.

So, what is going to happen next?

I would expect Nasdaq to delist the company's common shares next week, but trading is likely to continue on the OTC until the restructured company emerges from bankruptcy.

According to the prepackaged plan of reorganization , the company is expected to emerge within 42 days. At this time, all existing equity interests in the current exchange-listed company will be cancelled and shareholders will be allocated newly-issued shares of the successor company, which should commence trading on the OTC soon following the emergence from bankruptcy.

Investors will likely have to prepare for some initial volatility amid very light trading volume.

Bottom line

While Capstone Green Energy Corporation has filed for bankruptcy protection, the company's badly stricken shareholders will retain a majority stake in the restructured business.

With the next iteration of the company benefiting from substantially lower debt levels and improved liquidity, existing equity holders should abstain from selling their shares near all-time lows and rather wait for the all-new Capstone Green Energy Corporation to deliver upon management's projections.

Should the company indeed achieve substantial profitability within the next few quarters, there would be considerable upside, but even if progress will be taking somewhat longer, the restructured company's vastly improved financial condition should provide ample support at current share price levels.

Personally, I am likely to take the gamble and keep my position acquired during Thursday's early selloff throughout bankruptcy.

Risks

Investors should note that, at least in theory, the bankruptcy court can deny confirmation of the prepackaged plan of reorganization and require changes to the detriment of common shareholders. Under a worst-case scenario, Capstone might end up in liquidation, with a recovery for common shareholders being highly unlikely.

However, with the company's sole secured creditor supporting the plan, I would consider the risk as very low.

In addition, reduced volume might result in some erratic trading on the OTC.

Investors looking to keep their shares should make sure that their broker provides access to OTC trading.

Lastly, should the restructured business not achieve the improvements projected by management, a second bankruptcy might be in the cards, albeit this is unlikely to happen anytime soon.

For further details see:

Capstone Green Energy: Equity Holders To Retain Majority Ownership Following Emergence From Bankruptcy