CRLFF - Cardinal Energy: Worth Going Long But The 11% Dividend Is At Risk

2023-07-05 10:30:00 ET

Summary

- Cardinal Energy is an oil producer in Canada, but the majority of its oil production consists of medium and heavy oil, which is sold at lower prices.

- The Q1 free cash flow was not sufficient to cover the dividend.

- This means that unless oil prices increase soon, the dividend is definitely at risk.

- I am still planning to go long in Cardinal Energy, I'm just not counting on the dividend to be sustainable.

Introduction

I have been following Cardinal Energy ( CRLFF ) ( CJ:CA ) for multiple years now and my best investment decision was to purchase the convertible debentures of the company in the first half of 2020 when it started to look like the world was coming to an end. The debentures were fully repaid (in cash and on time) resulting in a triple digit return, but the company’s common shares have performed even better as the current share price in the mid C$6 range is more than 10 times higher than the lows during the COVID crisis. But that definitely doesn’t mean the company is overvalued as it has done an excellent job in cleaning up the balance sheet.

A look under the hood based on the Q1 results

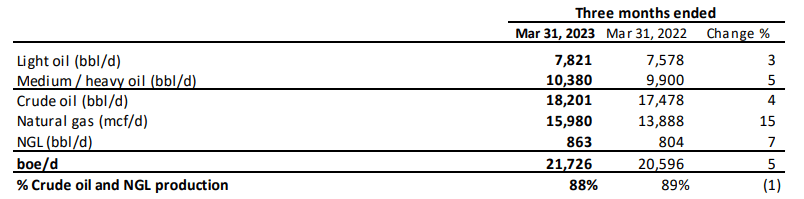

Cardinal Energy has been focusing on balance sheet strength in the past few years and this means production growth has not been a priority for a while. In the first quarter of the current financial year, Cardinal Energy produced a total of just over 21,700 barrels of oil-equivalent per day . As you can see below, about 88% of the oil-equivalent output comes from oil and NGLs, but only about 36% of the total oil-equivalent production qualifies as light oil.

{kind=link}

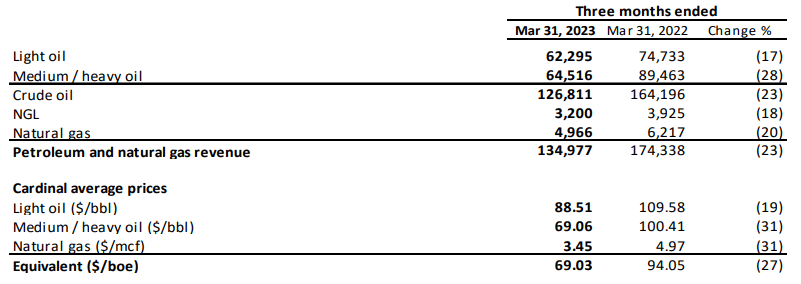

That distinction is important as light oil obviously fetches a higher price on the markets than medium and heavy oil. That was also clearly visible in the company’s first quarter as Cardinal Energy received about C$88.5 per barrel of light oil but just C$69 per barrel of medium and heavy oil.

{kind=link}

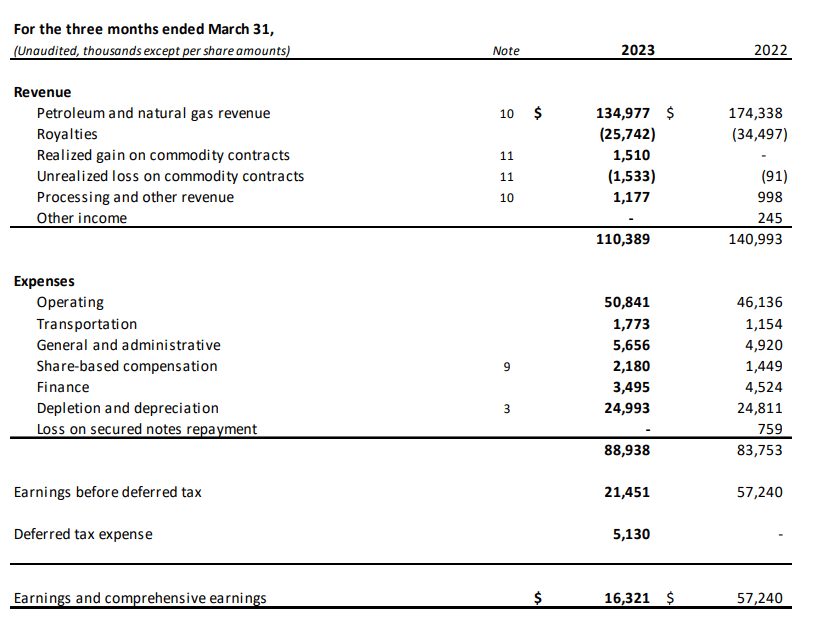

As you can see above, Cardinal was still able to fetch a price of C$3.45 per Mcf of natural gas, and although natural gas only contributed a few million dollars to the total revenue (which came in at C$135M), every dollar obviously helps to improve the dividend coverage level.

The net revenue after deducting the royalties payable on the oil revenue was C$110.3M and this resulted in a pre-tax income of C$21.5M . As you can see below, Cardinal Energy is still very lucky to take advantage of the very low transportation expenses, but the pure operating expenses are increasing (which makes sense given the inflationary pressure and the slightly higher production rate compared to the first quarter of last year).

{kind=link}

The main takeaway is the reported net income of C$16.3M or C$0.10 per share. So the company remained profitable in an era of US$75 WTI and c$3.45 natural gas. Of course, on an annualized basis, the C$0.40 EPS is not really impressive for a stock trading at around C$6.50, but thanks to Cardinal’s low decline rate, the sustaining capex tends to be pretty low.

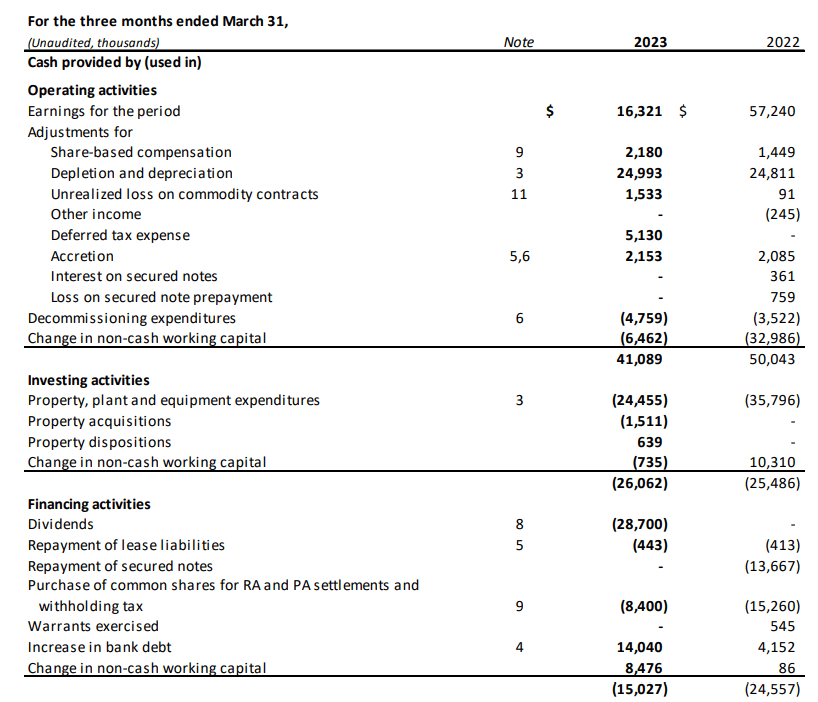

Looking at the company’s operating cash flow, it reported a total of C$41.1M in operating cash flow, and after taking changes in the working capital and the lease payments into consideration, the adjusted operating cash flow was approximately C$47M. This already includes almost C$5M in decommissioning expenditures but it also does not take any cash taxes into account as the entire Q1 income tax was a deferred tax. Based on the forward curve at the end of 2022, Cardinal Energy expected it would not have to pay any cash taxes until 2026. As the oil price has decreased since that measuring point, it is now likely the date of the first cash tax payment will be pushed back even further.

{kind=link}

As the company spent C$24.5M in capex (C$26M including the property acquisition), the underlying free cash flow was approximately C$21M. Divided over 157.1M shares, the free cash flow per share was C$0.13.

What does this mean for the dividend?

This wasn’t sufficient to cover the dividend as the monthly dividend of C$0.06 per share is costing the company approximately C$9.5M per month or C$28.5M per quarter and the net free cash flow fell short of that result in the first quarter of this year.

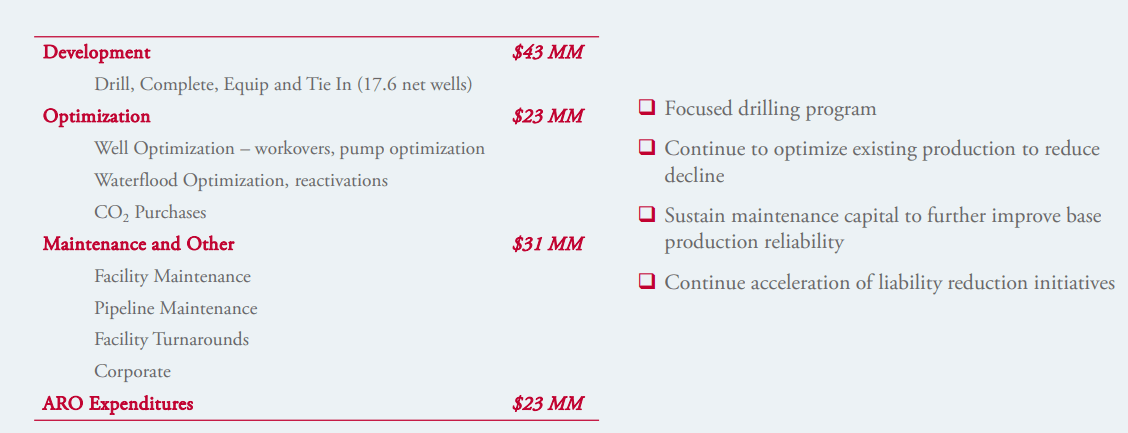

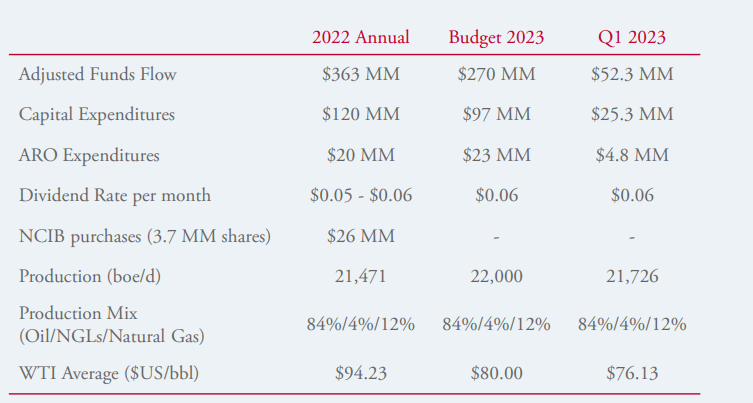

On an adjusted basis (adjusted for the decommissioning liabilities), the Q1 operating cash flow was approximately C$52M which would represent about C$208M on an annualized basis. According to the full-year guidance, Cardinal Energy plans to spend C$97M on capex and complete C$23M in decommissioning expenditures (‘ARO’, Asset Retirement Obligations).

{kind=link}

This means that based on the average prices in the first quarter of this year, Cardinal Energy will generate approximately C$88M in free cash flow. That’s approximately C$0.56 per share and clearly not sufficient to cover the annualized dividend of C$0.72 per share.

That being said, Cardinal Energy’s average production rate for this financial year is estimated at 22,000 boe/day. And considering the Q1 output was lower, the average daily production rate will likely be 3-5% higher in the next few quarters and that will help the total cash flow as well. But a higher oil price will still be needed to cover the dividend.

{kind=link}

Investment thesis

At the current oil price, Cardinal’s dividend is unfortunately not covered and that explains the weak share price performance. The company’s official full-year guidance with a C$270M adjusted funds flow is based on an oil price of US$80 WTI and in that scenario the dividend would be fully covered. Investors bullish on the oil price may just hold onto their position in Cardinal Energy, but if the oil price remains at the current levels for a few more quarters, I think a dividend cut is unavoidable.

This doesn’t mean Cardinal is a sell. I think it is still a buy (and I have been writing put options to establish a long position), but if the oil price doesn’t increase, the dividend will have to be cut.

For further details see:

Cardinal Energy: Worth Going Long But The 11% Dividend Is At Risk