CAH - Cardinal Health: A Revenue Growth Gem Plagued By Symptoms Of Negative Equity

2023-10-13 18:12:41 ET

Summary

- Cardinal Health gets a Hold rating today, in line with the Wall Street consensus.

- Its strengths include revenue growth beating its peer group, and low P/E valuation.

- Some headwinds faced are YoY profitability declines, debt load, and a share price getting too high vs the long-term moving average.

- The downside risk of negative equity and the upside potential of FY24 positive revenue forecasts have been discussed.

Research Note Summary

Today's note will focus on Cardinal Health ( CAH ), a large player in the health care distribution space, but one that is often under-covered on this portal.

I gave it a hold rating today based on several positive factors including revenue YoY growth beating its peers, undervalued on price-to-earnings, and outperforming the S&P500 index.

Its offsetting factors include a share price getting too expensive in relation to the long-term moving average, negative shareholder equity, and YoY drops in profitability and cashflow per share.

The downside risk of its heavy debt load was discussed, as well as the upside risk of its positive FY24 outlook on revenue.

Methodology Used

I will utilize my WholeScore Rating methodology which looks at this stock holistically across 6 categories including potential downside risks, and assigns a rating score. Most recent quarterly performance data comes from fiscal year 2023, Q4 which ended Jun 30th and reported August 15th.

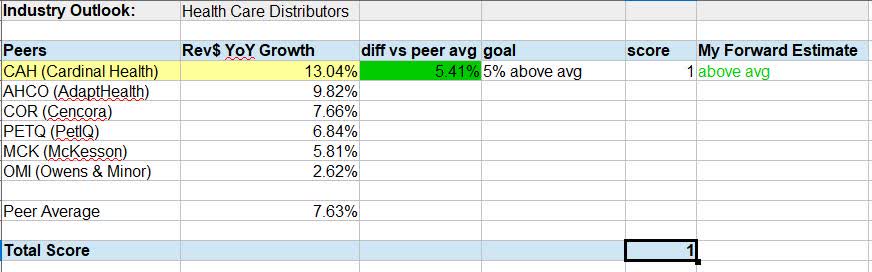

Industry Outlook

This stock sits in the sector of health care distributors , and is a leading player in this space.

One can see from the table I created that this stock leads its peer group in terms of YoY revenue growth, and is over 5% above the peer average.

{kind=link}

This is a typically a highly regulated industry subject to continually changing laws and oversight, but also one that is capital-intensive since producing medical products and solutions at large scale often requires multiple facilities and a robust supply-chain, not to mention thousands of people. In periods of high inflation, it can also be subjected to higher material costs throughout its supply-chain.

Also, if the company funds itself heavily from debt, periods of elevated interest rates may have a business impact on costs such as interest expense.

For readers less familiar with Cardinal, what I can see beyond just a cursory view of their homepage is that they make a lot of the supplies that work behind the scenes and you as a patient may not even take notice of them.

For example, around 2 million PET-Scans are done annually in the US, often in nuclear medicine to detect malignancy, and to make that possible practitioners must inject certain radiopharmaceuticals to help with the imaging. Well, turns out that Cardinal Health happens to be a leading producer of the Gallium-68 that is used for this purpose.

For any readers who have ever had this procedure done, had a relative who has, or simply had a discussion about it with your doctor, according to the Mayo Clinic the Gallium is used as a radioactive tracer to help locate malignancies during a Pet-scan.

You can imagine, then, the amount of federal regulation involved before having gotten products like that approved, and also the amount to time and resources that goes into testing, as well as cost.

The fact that Cardinal has outperformed its peers on revenue, in a peer group with average YoY revenue growth of less than 10%, it is already a positive factor for this company, I think.

In this category, I gave it a score of 1.

Financial Statements

The financial statements for this company show a positive in YoY revenue growth beating my target of 5% by a lot, coming in at 13.4% YoY growth.

However, where they came in below my goal was on profitability, cashflow per share, and equity which remains negative.

{kind=link}

Based on the company's own positive FY24 outlook for revenue in its two business segments, I am estimating positive revenue growth going forward. I think cashflow should remain similar, profitability could improve somewhat and the negative equity on the balance sheet will remain as long as the debt load is so high, even though they are working towards paying it down.

I gave the stock a score of 1 in this category.

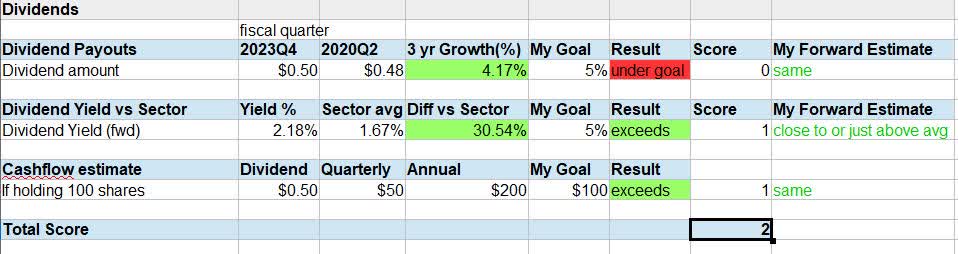

Dividends

Let's talk about making some cashflow from this stock rather than just holding on to shares. I usually say I don't invest in stocks, or companies, but existing cashflow streams .

In looking at the dividends for this stock, the 3 year dividend growth is slightly below my target goal of 5%, according to the table below I made.

{kind=link}

What is notable to call out is the yield which exceeds the sector average by almost 31%, beating my own goal of 5% above average.

Also, my goal of making at least $100 a year in dividend income from holding 100 shares also is met, which means I look for stocks paying at least $0.25 per share in quarterly dividends. These I consider "serious" companies with the capacity to return capital back to shareholders.

My forward estimates for this stock are expecting a similar dividend rate in the next quarter and a yield close to or just above average, as I don't expect a major share price dip which could cause the yield to spike. This could occur if the next quarterly earnings in November has a major earnings miss, however, but I think strong top-line revenue will provide enough of a tailwind to offset losses.

In this category, I confidently give this stock a score of 2.

Share Price

When it comes to the current share price, this stock is trading above its 200-day moving average for a while now, a long-term price trend indicator I prefer to follow due to its smoothing out of price movements.

In fact, you can see the crossover above the average occurred back in spring and the market has been rather bullish on this stock ever since.

However, in my analysis I am looking for no more than 5% above the long term moving average, as I think above that is overpriced, considering the firm has negative equity and YoY decreases in profitability lately.

According to my table below, my 1-year price estimate is 10% above the current SMA, or $92.02.

{kind=link}

In this scenario, buying at the current share price would only give me a $0.14 price gain per share, which is meager. On 100 shares, for example, that is just a $14 unrealized capital gain after a year.

Though I don't think there is a "perfect" buy or sell price, and cannot for certainty predict the future, I think what we can do is limit our downside risk and increase upside potential, by tracking the moving average.

In this case, the downside risk seems higher than upside potential so in this category I gave it a score of 0.

Performance vs S&P500

In terms of the 1-year price performance vs the S&P500 index, I am looking for the stock to outperform the index by at least 5%, and in this case it did, outperforming by almost 64%

This is a sign of strong market momentum for this stock, I would say, especially coupled with the previous price chart I discussed.

{kind=link}

My sentiment is that the market loves the strong revenue growth it has seen against its overall sector, and this focus on top-line growth is bringing out the bulls, despite the company having negative equity and profitability issues. Because of this, I expect the next quarter to continue to be near or above average vs the index.

Hence, in this category I gave it a score of 1.

Valuation

In terms of valuation , I can really just go by the forward price to earnings in this case since Seeking Alpha has not included a P/B ratio on this stock. Likely it is due to the negative equity on the balance sheet.

In terms of the P/E ratio, this stock meets my goal of being no more than 5% above the sector average. In fact, it is almost 35% below the average and so I am calling it undervalued.

{kind=link}

The why behind this undervaluation, in my opinion, is driven by concerns over profitability going forward, rather than revenue growth. In the last 6 reported fiscal quarters, three of them posted net losses, including the most recent one. This is evident from the income statement .

However, keep in mind a debt-ridden company could have significant interest-expenses but also during this current inflationary period the supply-chain costs could be high. Both the cost of revenues and total operating expenses grew on a YoY basis, for example.

A positive call-out, however, is that interest expenses are on the decline.

As for the book value, it remains negative and although there are many companies in a similar boat due to excessive liabilities exceeding assets I think that the fact that this company has posted negative equity since March 2022 also makes valuing the price-to-book (P/B ratio) highly problematic.

{kind=link}

In this category, I gave the score of 1.

Forward-Looking Risks

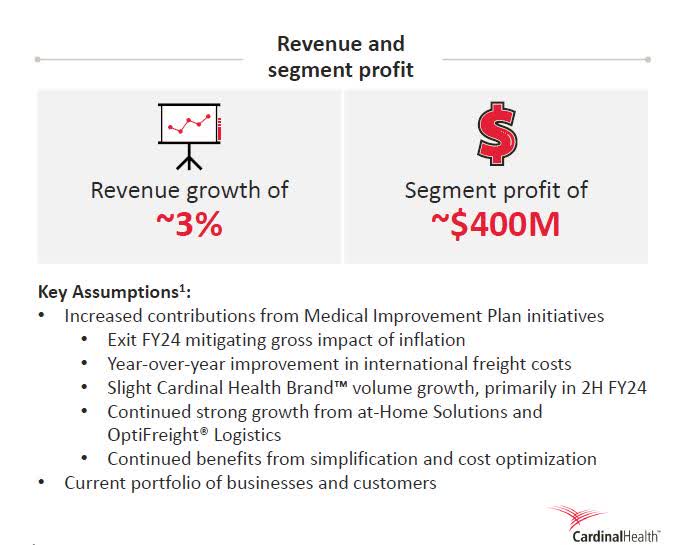

A neutral rating on this stock could have upside risks. One upside risk I can point to is that for fiscal 2024 the company has a very bullish outlook for revenue in its two key segments, as you can see from their own data below.

As their fiscal 2024 is already underway and about to report its first earnings in early November, they have forecasted 3% revenue growth in their medical supply segment for this fiscal year.

Cardinal - outlook on medical supply segment (company presentation - fiscal Q4)

{kind=link}

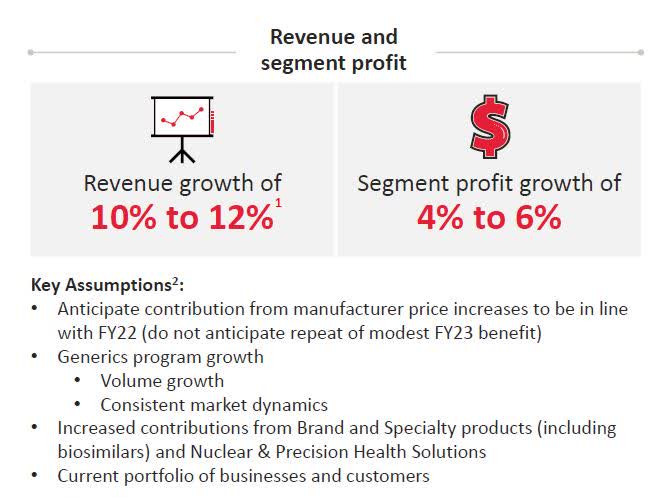

Further, they are even more positive this fiscal year about their pharma segment, forecasting a 10 to 12% revenue growth:

Cardinal - outlook on pharma segment (company presentation - fiscal Q4)

{kind=link}

I think those positive forecasts could keep many bulls loyal to this stock, however it is not without downside risks too.

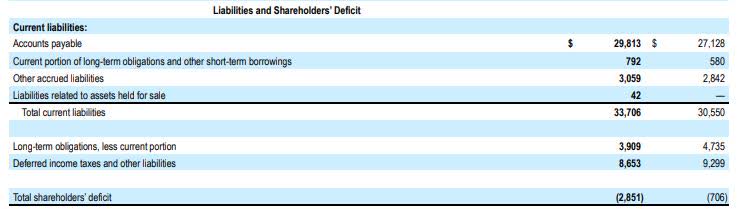

The primary downside risk I see with this company is the negative equity, which I think is driven by liabilities being too high, particularly long-term debt.

Cardinal - liabilities and negative equity (company fiscal Q4 release)

{kind=link}

A mitigating factor, however, is that the long-term debt has come down on a YoY basis, and also according to the following graphic the company has already paid down nearly half a billion dollars in long-term debt in the last fiscal year.

Cardinal - debt paydown (company quarterly results)

Here is how this stock fared in my risk scoring.

The negative equity and debt load resulted in a risk score of 10, which exceeded my risk target and so I consider it a negative factor.

At the same time, though, cancelling it out is the positive factor of a robust FY24 revenue forecast as mentioned earlier.

{kind=link}

Essentially, in this category the stock scored 0, as the downside and upside risks offset each other in my opinion.

WholeScore Rating

In today's rating the stock earned a WholeScore of 6, giving it a hold rating.

Cardinal - WholeScore rating (author analysis)

Though I am being more neutral than the consensus from SA analysts and the quant system, this time around I am essentially agreeing with the Wall Street consensus which I think is spot on for this stock and I have shown why:

Cardinal - consensus rating (Seeking Alpha)

Be sure to keep an eye on this stock's upcoming fiscal 2024 Q1 earnings release due out on November 3rd.

For further details see:

Cardinal Health: A Revenue Growth Gem Plagued By Symptoms Of Negative Equity