CAH - Cardinal Health Is Setting Up For A Great 2024

2023-12-21 02:53:22 ET

Summary

- Cardinal Health is a global healthcare company that operates in over 40 countries and covers pharmaceutical distribution and medical products.

- Based on strong Q1 earnings, the Company is growing on multiple fronts. In addition, cost mitigation is starting to drive results in widening margins.

- With a price target of $115 and mitigated risks, CAH is a buy.

Cardinal Health (CAH), a global healthcare services and products company, operates with a diversified business model that covers pharmaceutical distribution and medical products. With operations in over 40 countries, it sources, purchases, warehouses, and distributes pharmaceutical products to pharmacies, hospitals, clinics, and other healthcare facilities. Additionally, it manufactures and distributes medical and laboratory products globally. Cardinal Health generates revenue through the sale of these pharmaceutical and medical products, as well as the provision of related services.

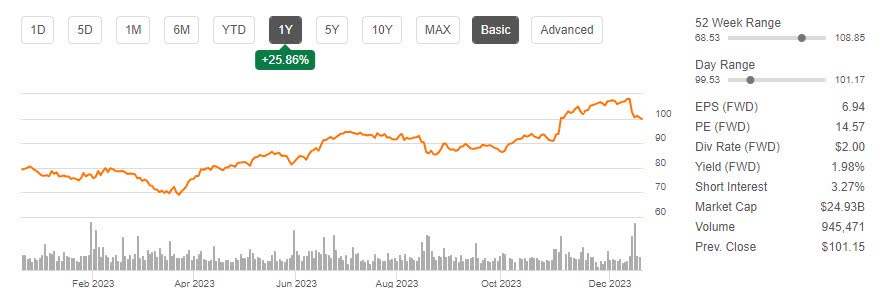

Cardinal Health has had a strong run over the past year, up 26%, leading many analysts to speculate that the stock is now at fair value.

CAH Stock Price Trend (Seeking Alpha)

{kind=link}

Based on strong Q1 earnings , Cardinal Health is growing on multiple fronts. In addition, cost mitigation is starting to drive results in widening margins. Not to mention a strong management focus on driving shareholder returns, and improving cash flow to support that goal.

Despite the run-up, I still see additional upside with a DCF-generated price target of $115, 16% up from today's pricing, and rate Cardinal Health a buy.

Growing On Multiple Fronts

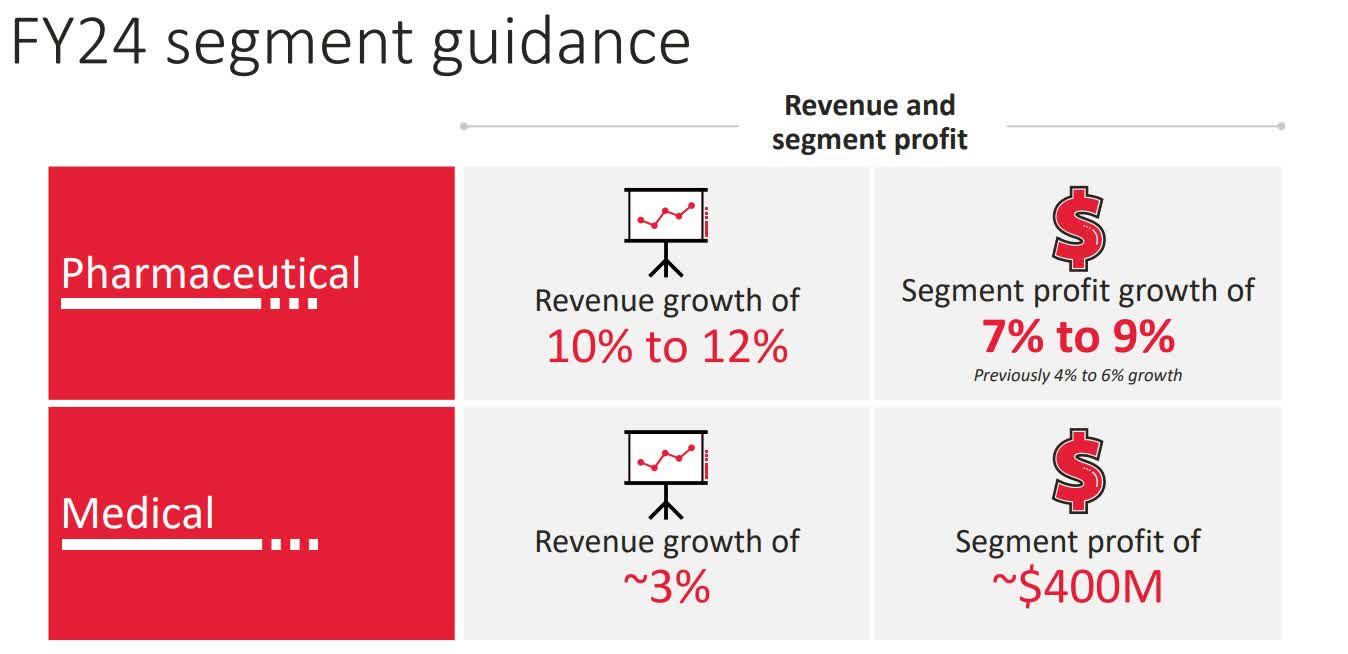

In August, Cardinal Health put forward aggressive guidance to not only deliver strong revenue growth but also restore profitability growth in both of its businesses.

Growth Guidance (CAH Investor Relations)

{kind=link}

My first question was, is this even sustainable in the market? Pharmaceuticals are expected to grow 6% from 2023-2028, so in the early days, this requires taking market share. That said, Cardinal Health over indexes on products like vaccines, which are growing at higher rates. They also have the benefit of being a distributor and riding on their customers' growth. On the other hand, the branded medical space is expected to grow by 3-4%, so businesses just need to keep up with the market.

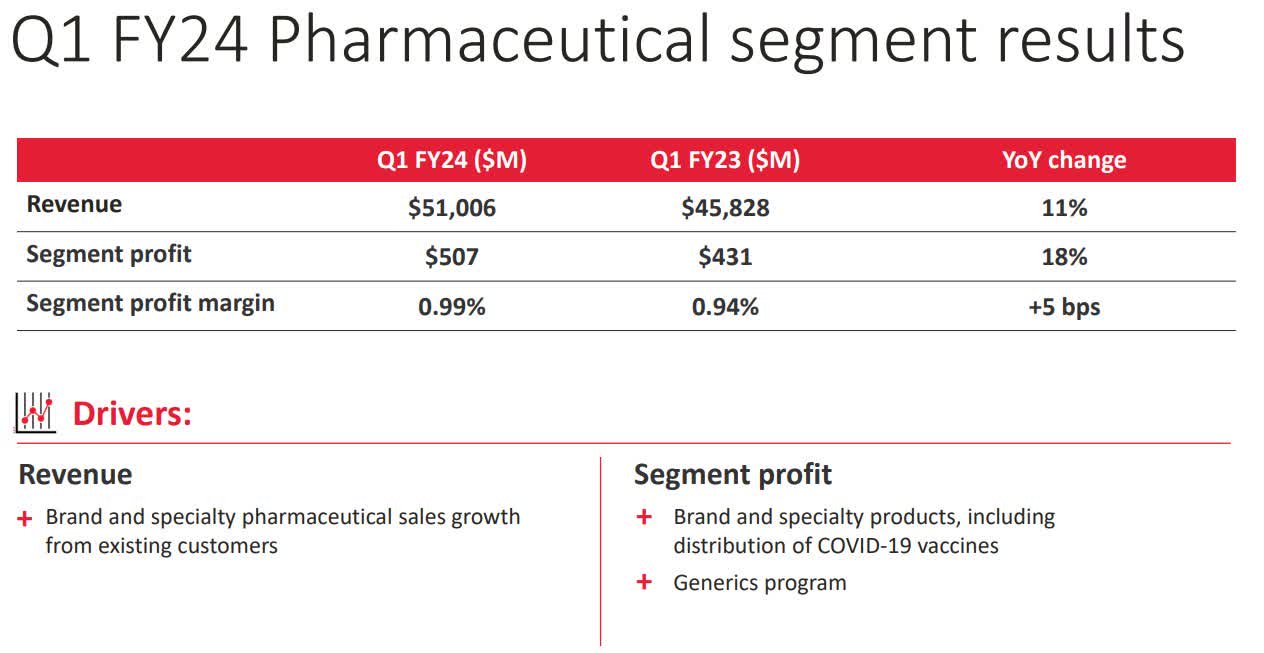

The next question was, can the business deliver on this growth? Looking at Q1 results, they are well on the way.

Starting with the pharmaceutical business, revenue was up 11%, in line with expectations, and profit was up 18% well ahead of expectations. Management discussed in the earnings call that the covid-19 vaccine and the expanding generics program drove some of the margin benefit.

Q1 Pharmaceuticals (CAH Investor Relations)

{kind=link}

Looking at the medical business, revenue was essentially flat, falling short of expectations; however, the profit margin increased by 210bps, much faster than expected. This benefit was driven by cost mitigation, which we will discuss below. Revenue is also expected to lift going forward as PPE impact roll-over.

Cost Mitigation Is Starting To Drive Results

In 2023, Cardinal Health was struggling with margin as inflationary impacts and volatile input prices drove up costs. That trend has started to reverse in 2024 allowing margins to widen.

Starting with SG&A at the enterprise level, costs were flat year-over-year despite high-inflation over 3%, with increased selling costs offset by lower support costs.

SG&A (CAH Investor Relations)

At the business level, management took a " ruthless " approach to mitigating inflation and streamlining costs. Here are a couple of highlights from the earnings call :

- Significantly reduced volatility in inputs like oil and freight

- Margin improvement from cost mitigation in medical group is expected to continue forward

- Inflation impacts will be offset exiting 2024

Overall, the business grew revenue and margin at the same rate and has the opportunity to further expand margin in its businesses based on 2024 trends.

Guidance Suggests Double-Digit Upside

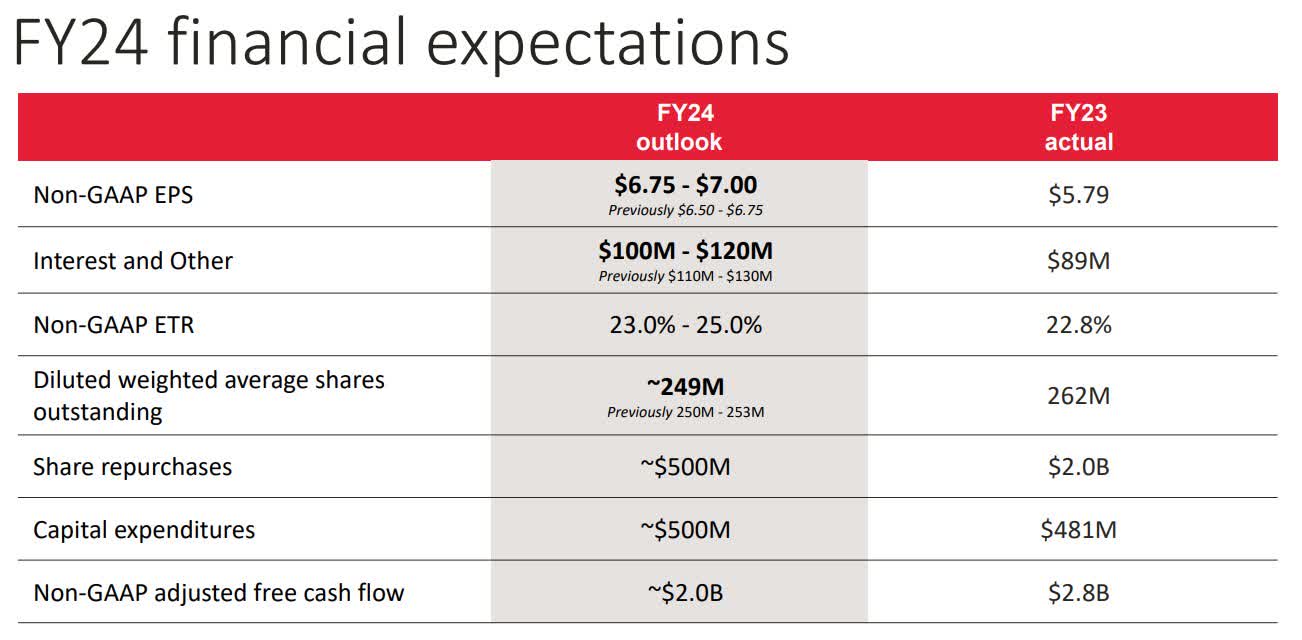

In the earnings presentation, management provided the following guidance on the heels of the improved revenue and cost performance.

Q1 Guidance (CAH Investor Relations)

{kind=link}

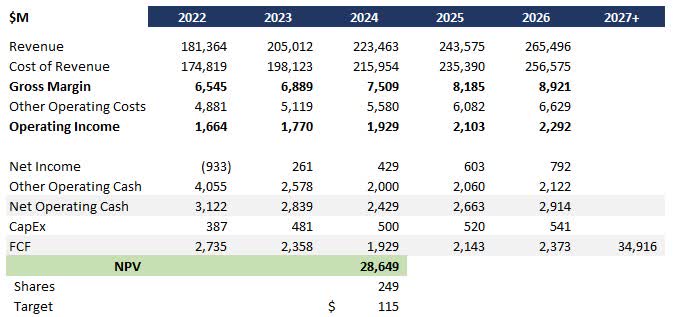

I flowed this guidance through a DCF model along with the following assumptions:

- Margins do not expand after 2024; I kept 2025-2027 with revenue and cost matched

- Discount rate of 10% driven by high-debt and low risk premium as a large, high-cash flow company

- 3% long-run growth rate based on historical inflation

With the above in mind, I generated a price target of $115.

CAH DCF (Data: SA; Analysis: Mike Dion)

{kind=link}

Wall Street Analysts have an average hold rating with a price target of $104, still up from today's pricing but without a margin of safety. My target at $115 is still within their overall range of $78-126.

CAH Wall Street (Seeking Alpha)

{kind=link}

The quant rating is especially bullish at a strong buy, driven by low valuation multiples as well as profitability and momentum in the price. Growth is the only weight on the rating, which should shake out as 2024 moves along.

Downside Risk

The biggest risk for Cardinal Health is execution risk on their growth and cost mitigation strategy. I believe there is upside as long as costs stay at or below revenue growth and maintaining this balance will be critical.

As a company with negative equity , Cardinal Health is also heavily exposed to interest rates. With upcoming maturity in debt this will be something to keep an eye on, although they have the cash on hand to mitigate this exposure partially.

Verdict

In conclusion, Cardinal Health exhibits promising potential based on its improved revenue and cost performance. The first quarter guidance influenced a DCF model outcome, resulting in a price target of $115. Although Wall Street analysts average a hold rating with a price target of $104, this figure remains within their overall range of $78-126. The company's quant rating is particularly bullish, driven by low valuation multiples, profitability, and momentum in price, although growth is a slight concern. Key risks include execution of growth and cost mitigation strategy, and exposure to interest rates due to negative equity.

I rate Cardinal Health a buy with upside potential and price target outweighing downside risks.

For further details see:

Cardinal Health Is Setting Up For A Great 2024