CAH - Cardinal Health: Not A Long-Term Investment

2023-05-24 05:54:01 ET

Summary

- Cardinal Health reported solid third quarter results and raised full-year guidance.

- In the last twelve months, Cardinal Health's stock outperformed as the stock price saw a reversion to the mean from previously extreme undervaluation.

- And while the stock might still be a bit undervalued, Cardinal Health is not the long-term investment I would like to make.

Almost one year ago I published my last article about Cardinal Health ( CAH ) and only two months after I had published a bullish article about Cardinal Health in March 2022, I explained why my patience was getting thin with Cardinal Health and why I sold the stock. I also explained why I still saw the stock as undervalued but did not want to hold the stock anymore.

In retrospective this might have been a mistake as Cardinal Health performed great during the last twelve months and clearly outperformed the S&P 500 ( SPY ) and most other companies (Cardinal Health was among the top 20 best performing stocks in the S&P 500 during the last twelve months). In the following article we are looking at Cardinal Health once again and we start with the quarterly results.

Quarterly Results

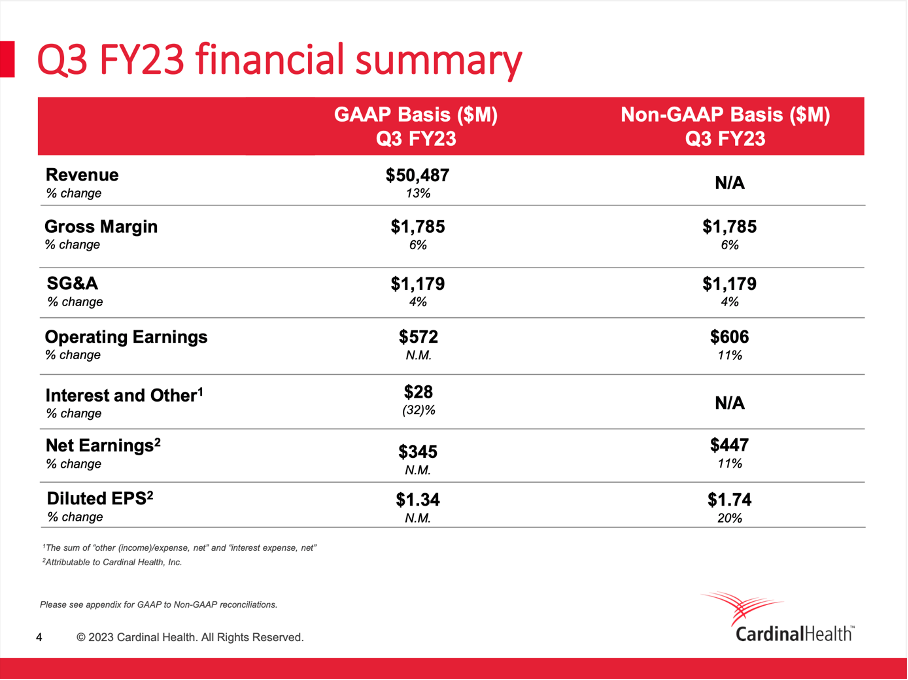

When looking at the third quarter, Cardinal Health reported solid results. Similar to previous years, Cardinal Health increased its revenue with a solid pace. Revenue increased from $44,836 million in Q3/22 to $50,487 million in Q3/23 - resulting in 12.6% year-over-year growth. Additionally, Cardinal Health also reported an operating income of $572 million in this quarters and compared to an operating loss of $97 million in the same quarter last year, this is an improvement. And diluted earnings per share also switched from a loss of $5.05 per share in Q3/22 to $1.34 in earnings per share in Q3/23.

Cardinal Health Q3/23 Presentation

{kind=link}

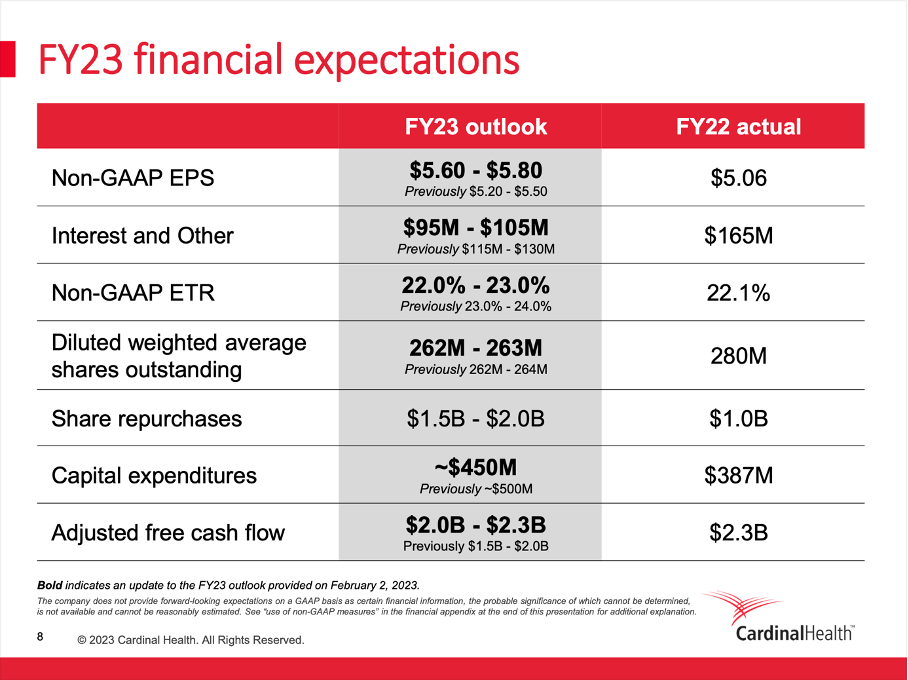

And we saw not only an improvement in quarterly results, but guidance for fiscal 2023 was also raised by management. Cardinal Health is now expecting $5.60 to $5.80 in non-GAAP EPS (compared to $5.20 to $5.50 previously). Adjusted free cash flow is now expected to be between $2.0 billion to $2.3 billion (compared to $1.5 billion to $2.0 billion in a previous guidance).

Cardinal Health Q3/23 Presentation

{kind=link}

Growth

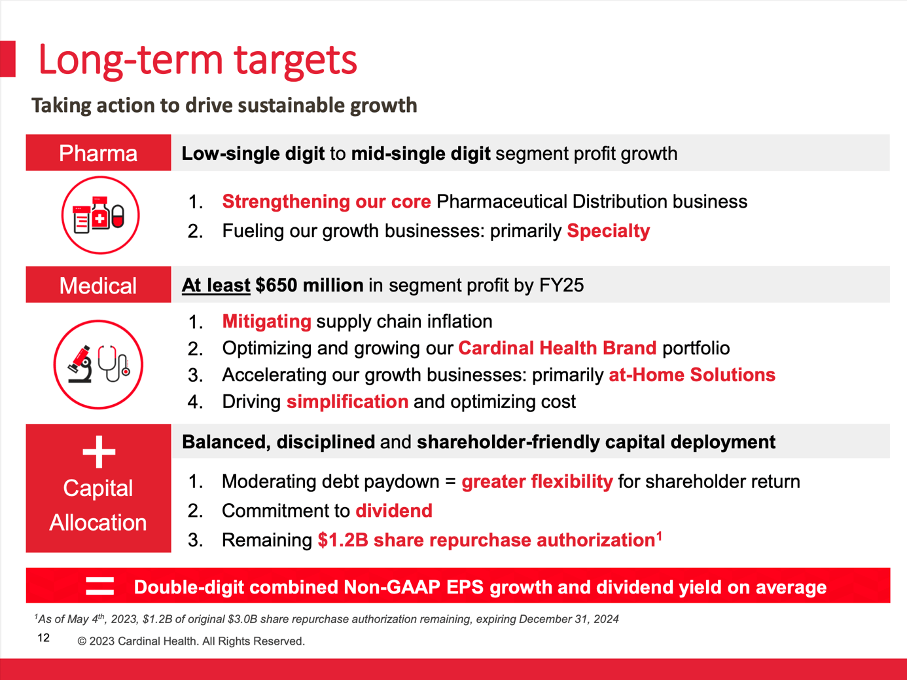

And management is not only optimistic for fiscal 2023, but also for the following years and is expecting double-digit EPS growth for the years to come (according to the company's own long-term targets).

Cardinal Health Q3/23 Presentation

{kind=link}

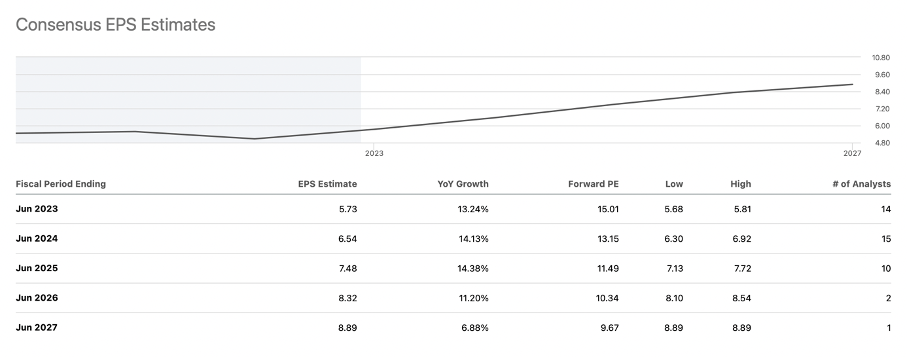

When looking at analysts' expectations for the years to come, we see a similar optimism and earnings per share are expected to grow with a CAGR of 12% until fiscal 2027.

Cardinal Health: EPS Estimates (Seeking Alpha)

{kind=link}

Problem: Declining Margins

And I don't have doubts that Cardinal Health will be able to grow its top line. In the last ten years, revenue increased with a CAGR of 5.36% and I remain optimistic that Cardinal Health can continue to increase its top line in the single digits. The problem for Cardinal Health was not the top line growth, but the company's margins. I already pointed out in my last article that margins were declining for several decades and since last year, the picture did not improve.

Cardinal Health is already operating in a low margin business with its operating margin being only 0.83% in the last four quarters. And the constantly declining margins are adding pressure and are not a great sign for Cardinal Health. Declining margins - especially a declining gross margin - are a sign for missing pricing power and a business that is being put under pressure by competitors.

Dividend and Share Buybacks

In the last few years, the biggest contributor to bottom line growth (or the reason for keeping earnings per share somewhat stable) were share buybacks. And Cardinal Health is continuing to buy back shares with a rather high pace. In the last twelve months the number of outstanding shares decreased from 275 million one year ago to 258 million right now - resulting in a decrease of 6.2% YoY. When looking at the last ten years, the company constantly decreased the number of outstanding shares.

Aside from share buybacks, Cardinal Health is also paying a quarterly dividend to distribute cash to its shareholders. And recently, Cardinal Health raised the dividend again - but only slightly from $0.4957 before to $0.5006 right now - resulting in 1% dividend growth. In the last few years, the picture was similar - over the last five years, Cardinal Health increased the dividend with a CAGR of 1.4%.

Other Investments

I also mentioned three other companies (and stocks) in my last article about Cardinal Health that might be a better investment than the pharmaceutical distribution company. I personally bought two other companies from the money previous invested in Cardinal Health - one of them was PayPal ( PYPL ). When looking at the performance since my last article was published, it certainly would have been the better idea to remain invested in Cardinal Health as PayPal declined 26% in the meantime.

Despite that performance, I remain confident that PayPal is a much better long-term investment than Cardinal Health and will clearly outperform. The same is true for Starbucks ( SBUX ) - the second company I invested in. And although Starbucks could not keep up with the performance of Cardinal Health in the last year, an investment in Starbucks was also a good idea and the stock gained 34%.

And finally, I mentioned McKesson ( MCK ) in my article and wrote that Cardinal Health's competitor would be a much better investment. And while McKesson gained 18% in value during the last year, it could not match the great performance of Cardinal Health. But in my opinion, all three are better long-term investments than Cardinal Health.

Reversion to the Mean

Although Cardinal Health outperformed in the last 12 months (and although it was a mistake not to hold on to Cardinal Health for the time being) I would still argue it is not a great long-term investment. To understand, we must look at the two main drivers for any stock price (in my opinion). On the one hand, stock prices are driven by the fundamental performance of the company. This is what Graham called the long-term weighing machine. And on the other hand, stock prices are driven by investor sentiment (and maybe news and stories). This is what Graham called the short-term voting machine.

And in the last twelve months, the stock performance was mostly driven by what Graham called his voting machine. In the previous years, investor sentiment drove Cardinal Health to unjustified low valuation multiples and as the stock was clearly undervalued a reversion to the mean was reasonable (and had to be expected at some point). Investor sentiment often reaches extremes - in this case: extreme pessimism - but at some point, investors will realize that the price for the stock is unjustified, and the stock will move towards a more reasonable price (or towards its true intrinsic value). Such price movements are sometimes taking only a few months or quarters and will lead to a clear outperformance of a stock in the short-term or mid-term.

And while betting on deeply undervalued stocks to return to its intrinsic value can work as short-term strategy, it is not enough as long-term strategy. In the short term, we can profit from investor sentiment reaching extreme levels, but in the long term, we must pick companies (and investments) growing its bottom line with a healthy pace. It is a deep conviction (and basis of my investment philosophy) that stock prices will move accordingly to the fundamental performance of a company - but only in the long term. And a company growing its bottom line only in the low single digits will see its stock price move accordingly.

In case of Cardinal Health, we saw an outperformance in the last few quarters due to a reversion to the intrinsic value of the stock (as the stock was clearly trading below its intrinsic value). But over the long run, I don't think Cardinal Health is the best investment as I expect the fundamental performance to be only mediocre and over the long run, the fundamental performance is driving the stock price. Once a stock has reached its intrinsic value, it can only gain in value when the fundamental business is growing. And when expecting Cardinal Health to grow 5% annually (for example), it is only reasonable to assume the stock to grow 5% annually as well. When hoping for the stock to grow 6% or 7% annually, that additional growth would stem from higher valuation multiples (and the stock therefore moving towards overvaluation) - and that is a bet that could work out (as markets are irrational) but is not a bet I am willing to make.

Intrinsic Value Calculation

While the performance of the last years was mostly due to a reversion to the mean, it does not mean this effect is already over. We still can make the case for Cardinal Health trading below its intrinsic value and still implying upside potential as the stock will move towards its intrinsic value.

We can start by looking at the two major simple valuation metrics - the price-earnings ratio as well as the price-free-cash-flow ratio. But both are rather misleading in case of Cardinal Health. When looking at the P/E ratio of 49.5, Cardinal Health would be overvalued and when looking at the price-free-cash-flow ratio of 5, we must assume that the stock is an extreme bargain at this point. But both conclusions would be false, and the high P/E ratio is based on a rather low EPS (GAAP numbers) and the low P/FCF ratio is based on an unreasonably high free cash flow in the last four quarters.

Instead, we rather use a discount cash flow calculation to determine an intrinsic value for the stock. And as basis for our calculation, we can use the midpoint of the company's guidance for fiscal 2023. Management is expecting free cash flow to be around $2.15 billion, and that number is also more or less in line with free cash flow in the last ten years.

When calculating with this number as well as 258 million outstanding shares (and a 10% discount rate) and also assume that Cardinal Health won't really grow in the coming years (a reasonable assumption based on the performance in the last few years) we get an intrinsic value of $83.33 making Cardinal Health fairly valued right now.

I still don't want to calculate with high growth rates as I still see no reason for the optimism and double-digit growth rates in the years to come. But assuming that Cardinal Health can grow at least 3% annually for the years to come is not unreasonable. This would already lead to an intrinsic value of $119.05 for Cardinal Health and is implying further upside potential for the stock.

Technical Picture

While an intrinsic value calculation based on fundamentals is still indicating that the stock might have room to run, the technical picture should make us more cautious. The stock is rather close to reaching its all-time highs around $92 again and this level could turn out to be a major resistance level and there is a rather high probability for the stock bouncing off and leading to a bigger correction. And I don't think it is a good idea to invest before the stock reaches a major resistance level.

Conclusion

Although I was wrong about Cardinal Health and should not have sold the stock last year, I still don't think Cardinal Health is a good long-term investment. The stock is continuing to trade for low valuation multiples and potentially remains undervalued. This is still implying potential upside for the stock as the reversion to the mean (and the reversion to reasonable valuation multiples) might continue. And this is leaving us with some short-to-mid-term potential upside for the stock, but over the long run we should expect a rather mediocre performance - or at best a performance in line with the overall market.

For further details see:

Cardinal Health: Not A Long-Term Investment