CARG - CarGurus: Fairly Priced But A Poor Hold

2023-12-14 06:25:17 ET

Summary

- CarGurus' share prices have declined since its IPO, raising questions about whether it is currently trading at a discount.

- It has experienced significant growth through acquisitions and expansion into different revenue segments, including wholesale and product segments.

- The company has a capital-light and synergistic business model, but uncertainties may impact its long-term returns.

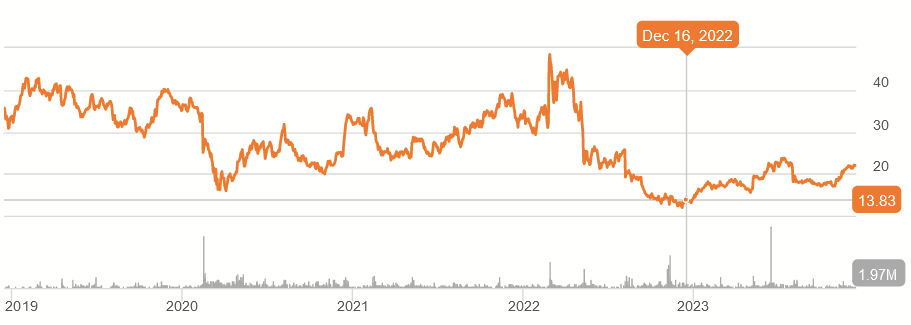

Founded in 2006, CarGurus (CARG) is an online research platform and marketplace that allows consumers to look up vehicles available for sale at local dealers. With over six years since its IPO at around $29 per share in 2017, share prices currently trade around $22. Already priced for growth well before it occurred (and it did occur), shares of this company have seldom ever traded at anything that could be considered a discount. Yet, with that long-term decline, folks might be wondering if $22 is in that discount range.

The company has a lot going for it, being capital-light and enjoying a synergistic model for which some growth opportunities exist. Yet, I will make the case the CARG is a SELL, given how the price relates to that upside and future developments remain unclear for folks who want a long-term investment.

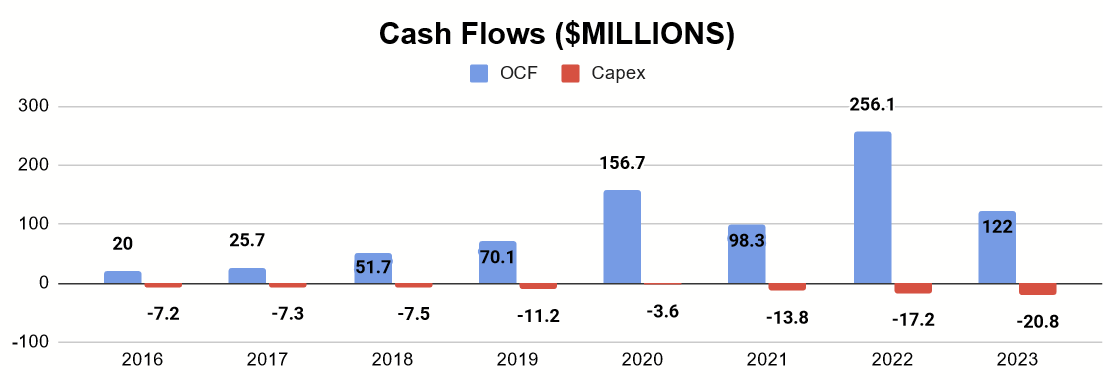

Cash Flows Since IPO

Let's a look at the cash flow situation as reported since the IPO. I've included the YTD data for 2023.

{kind=link}

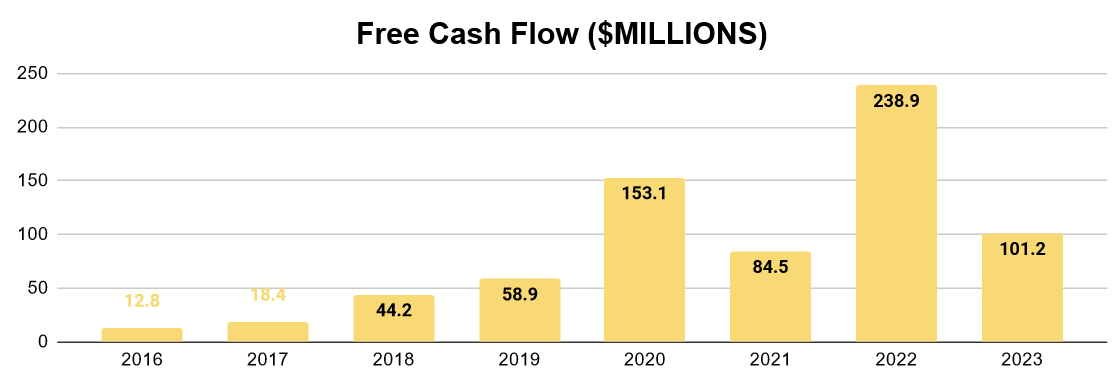

As we can see, capex has remained fairly low, not hiking nearly as much as operating cash flows as the business grew. Thus we can see that free cash flow has worked out to be the following:

{kind=link}

The growth here seems meteoric. What drove it? Well, the company made a series of acquisitions from 2019 to 2021. This included PistonHeads (a UK-based automobile marketplace), Autolist (a similar company and site to CarGurus), and a 51% stake in CarOffer , a platform to assist in wholesale of car to dealers. Just this month, they announced acquiring the remaining stake in CarOffer.

Understanding That Cash Flow

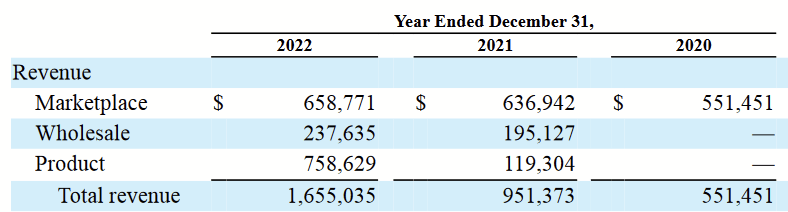

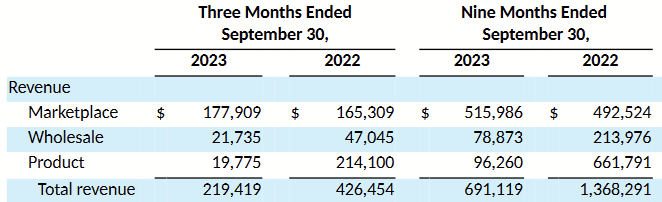

Over the last few years, the company's revenue sources have expanded from its marketplace model to its wholesale and product segments.

{kind=link}

While revenues have grown quite a bit, it's worth noting that these segments operate on very different margins.

{kind=link}

The marketplace revenue primarily derives from subscription fees that dealers pay to use the platform and advertising fees to list their inventory. In addition to putting their product before customers, the platform comes with various tools to assist dealers in customer engagement that are unlocked by the subscription. The marketplace's value is therefore in its ability to increase a dealer's sales and/or reduce their cost of sales.

{kind=link}

The wholesale segment was made possible with the acquisition of CarOffer. It is an adjacent platform to the marketplace (whose focus is retail), and its revenues derive primarily from transaction-related fees on the platform. It allows for dealer-to-dealer sales of cars, allowing dealers to manage their inventory more flexibly on that platform. Similarly, its value is in its ability to increase a dealer's sales and/or reduce their cost of sales (albeit on the wholesale side now).

The product segment was also made possible by CarOffer. Its revenues derive from proceeds it realizes from cars acquired by customers and sold to dealers or through arbitration. As this segment's cost of sales and revenues are roughly equal, its value is less a matter of its cash flow and more a matter of how it enhances the bigger ecosystem of its retail and wholesale segments.

{kind=link}

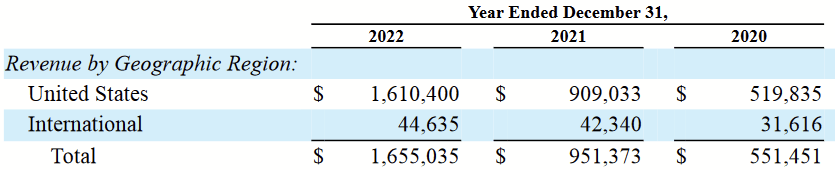

Additionally, revenues derive almost entirely from the United States.

{kind=link}

A Look to the Future

Before attempting a valuation, let's try to get an idea of reasonable expectations about this company.

Product Segment

The product line is where I think we see some potential risk, and I want to address that first. Quoting their 2022 Form 10K :

For example, if retail prices for used vehicles rise relative to retail prices for new vehicles, it could make buying a new vehicle more attractive to consumers than buying a used vehicle, which could result in reduced used vehicle wholesale sales on the CarOffer platform. Used vehicle dealers may also decide to retail more of their vehicles on their own, which could adversely impact the volume of vehicles offered for sale on the CarOffer platform. We also face inventory risk in connection with vehicles acquired by CarOffer via arbitration , including the risk of inventory obsolescence, a decline in values, and significant inventory write-downs or write-offs. Such inventory risk would be higher if arbitrations increase, which is more likely to occur in connection with declining wholesale market conditions

They aren't simply printing profits with a low-cost website anymore. By taking on inventory, they do face some potential risk that the proceeds will be substantially less than what they paid for cars. Revenue from the product line was $738.6m in 2022, with cost of sales being $765m. That's already a loss (perhaps an acceptable one), but just a 5% decrease in proceeds would have been an additional loss of $38m, a significant chunk of any year's free cash flow.

Thankfully, the company seems to have a selective appetite for taking on inventory, as its latest 10Q shows substantially less activity in the Product space:

{kind=link}

Since this is a new component of CarGurus through its acquisition of CarOffer, investors should be watchful of what kind of patterns then company will follow going forward.

Marketplace

The marketplace is the big winner, the bread and butter, of this company, accounting for the lion's share of its cash flows. I'll quote their 2022 Form 10K again:

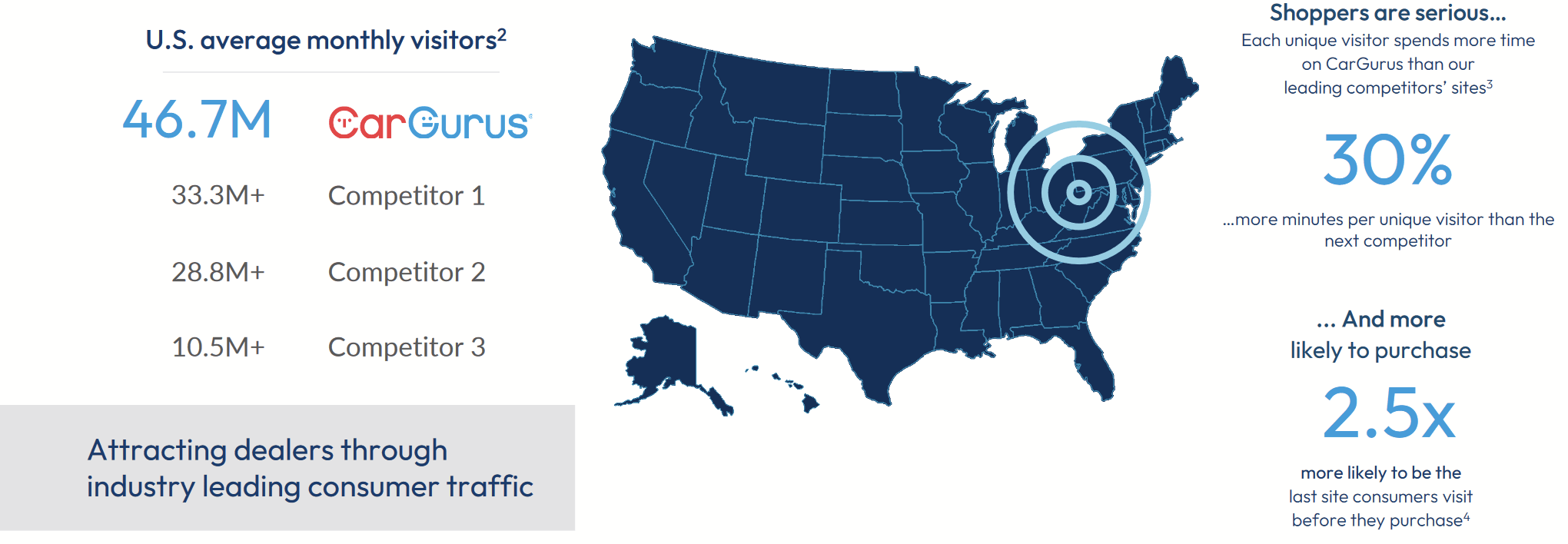

With the majority of dealers in the United States listing inventory on our platform and our consumer-friendly deal ratings, we have built the most visited online automotive marketplace in the United States (Source: SimilarWeb, Traffic Report, Q4 2022, USA) and we believe that our scale creates powerful network effects that reinforce the competitive strength of our business model.

I believe that this is an important feature because it makes it reasonably likely that positive cash flows will persist, even if the product segment lags. I don't think the company quite has a moat, as Cars.com and AutoTrader.com offer very similar marketplace platforms, but does it does mean the company has cast a wide net and enjoys diverse cash flows from dealers. In its Q3 earnings release, it did boast the advantages it has over competitors such as these:

{kind=link}

These are all assuring, but with a majority of dealer's already on their platform, this means there will be less room for growth in this segment like we saw over recent years. Instead, it will be steady and incremental at best.

Wholesale

The wholesale segment of CarOffer will likewise see incremental growth as the marketplace brings dealers into the ecosystem, but since its revenues are based on transaction-based fees, this also means it will be exposed to the cyclicality of the automobile industry. Ultimately, I think it will be positive but that the cash it generates will fluctuate.

Buybacks and Share-Based Compensation

One way in which the company may grow shareholder value is through opportunistic buybacks. These began in 2022, accounting for about $14m in cash spent:

{kind=link}

The company also reported an average repurchase price of $13.84, representing some of the lowest the stock has ever traded.

{kind=link}

It was, therefore, reassuring that buybacks did not start when the stock was at all-time highs, as many in tech are known to do. YTD for 2023 , the company has spent much, much more on buybacks.

{kind=link}

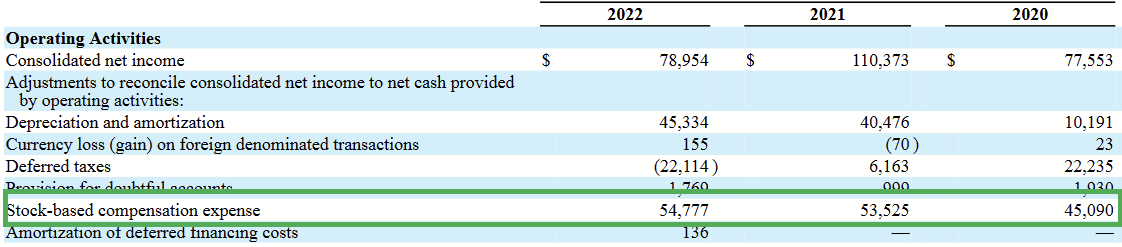

That's over $100m in cash spent. For the first three quarters, it reported an average price of $16.66 per share. Again, this is on the low side of the shares historically, which is good. It's worth noting that share-based compensation is still a part of the picture here, with around $50m in SBC given out the last three years:

{kind=link}

As such, the company is showing odd signals. It remains to be seen if buybacks will persist, even if the share price were to rise significantly and in excess of company's own growth. Right now, buybacks and SBC seem to balance out. Shareholders should be mindful of how either could change and thus affect their long-term returns.

Disruption?

With any tech company, the question in my mind is: What will come to disrupt it, just as it came in and disrupted older business models? The existence of similar (if weaker) competitors is one issue. Recent strides in the development of AI could materialize in ways that hurt the company's bottom line in way that we cannot currently expect. Anything that causes dealers to believe that they will capture more value through other means will reduce the earnings from subscriptions and advertising fees on the marketplace.

Since subscriptions are often done on a per-dealer basis, any data-driven models that improve a dealer's logistics could allow them to scale down their locations and thus reduce their number of subscriptions. In their Risk Factors of their 2022 Form 10K, the company writes:

When dealers consolidate, the services they previously purchased separately are often purchased by the combined entity in a lesser quantity or for a lower aggregate price than before, leading to volume compression and loss of revenue. Further dealership consolidations or closures could reduce the aggregate demand for our products and services.

This risk is mentioned in the context of harder times for dealers, but that doesn't mean dealers can't find reasons to consolidate and minimize this cost during more prosperous times. Long-term owners of CARG should be mindful of this.

Valuation

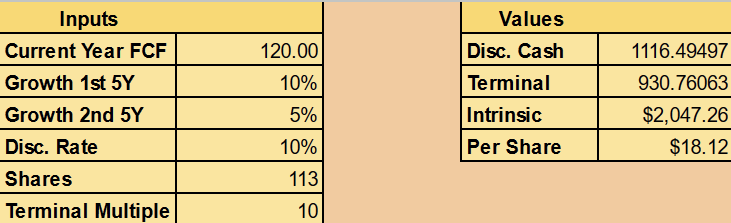

With the historical financial data, a review of the revenue sources, and the various factors to consider for the future, I can attempt a valuation with Discounted Cash Flow. I'll make the following assumptions:

- Baseline of $120m in annual free cash to reflect its newfound size

- 10% average growth the first five years as it continues gaining dealers and realizing synergies

- 5% growth the next five years as ability to acquire new dealers slows down

- Terminal multiple of 10 to reflect market attitudes on new growth in the future

{kind=link}

That brings us an intrinsic value per share of $18.12. With $355.3m in cash on its balance sheet and no debt, that also gives shareholders about $3.14 in net cash per share. With current share prices between around $22, some may interpret this company as fairly valued.

My valuation and its assumptions are conservative, given the nature of tech businesses, even one as straightforward and value-adding as CarGurus. I believe shareholders should demand a more attractive discount before buying and, since they aren't getting a dividend and no longer see an ocean of growth ahead, shouldn't feel any problems with selling and moving into a more attractively priced investment.

Conclusion

CarGurus is a financially healthy business, generating strong cash flows with almost no debt. Yet, for much of CARG's life on public markets, it has traded at or above its intrinsic value. It enjoys a leading position in its dealer marketplace for new and used cars, and owners can likely expect steady cash flows for the foreseeable future.

Yet, much of their growth seems to be behind them. The company seems to realize this with the launch of a buyback campaign that has, so far, picked up shares at good prices. With most American dealers already on their platform, growth at this point is likely to be more steady than stellar. Its product segment also exposes it to risk of occasional losses on inventory that did not exist in years prior.

At the moment, I would say the business is only fairly priced and not attractive enough to hold. Prudent investors who search can find more attractively priced investments elsewhere, which is why CARG is, in my book, a sell .

For further details see:

CarGurus: Fairly Priced But A Poor Hold