CARG - CarGurus: Not Worth Sticking Around For A Comeback

Summary

- Shares of CarGurus have dropped more than 60% this year on weakening performance.

- Investors are also rightly unnerved over the company's expanding Instant Max Cash Offer program, which is still operating at negative margins.

- The company's profitability margins have dramatically declined since the prior year.

- Without a substantial valuation discount to the broader market, there isn't sufficient incentive to stay invested in CarGurus.

Right now, in my view, investors have a broad opportunity to invest in a lot of high-quality tech stocks at a very low price. It is time for us to be choosy in our stock-picking: I see 2023 as a rebound year in which taking on risk and buying strong small/mid-cap names is going to generate plenty of alpha versus the broader market.

At the same time, there are many underwater names that we should avoid, and I think CarGurus ( CARG ) is one of them. This used-car marketplace has fallen far from its pre-pandemic days, and though the stock is down more than 60% this year I see very few catalysts that are capable of lifting CarGurus beyond its current doldrums.

I am finally downgrading my view on CarGurus to bearish. In my view, this stock has too much added fundamental risk without much safety buffer in its valuation.

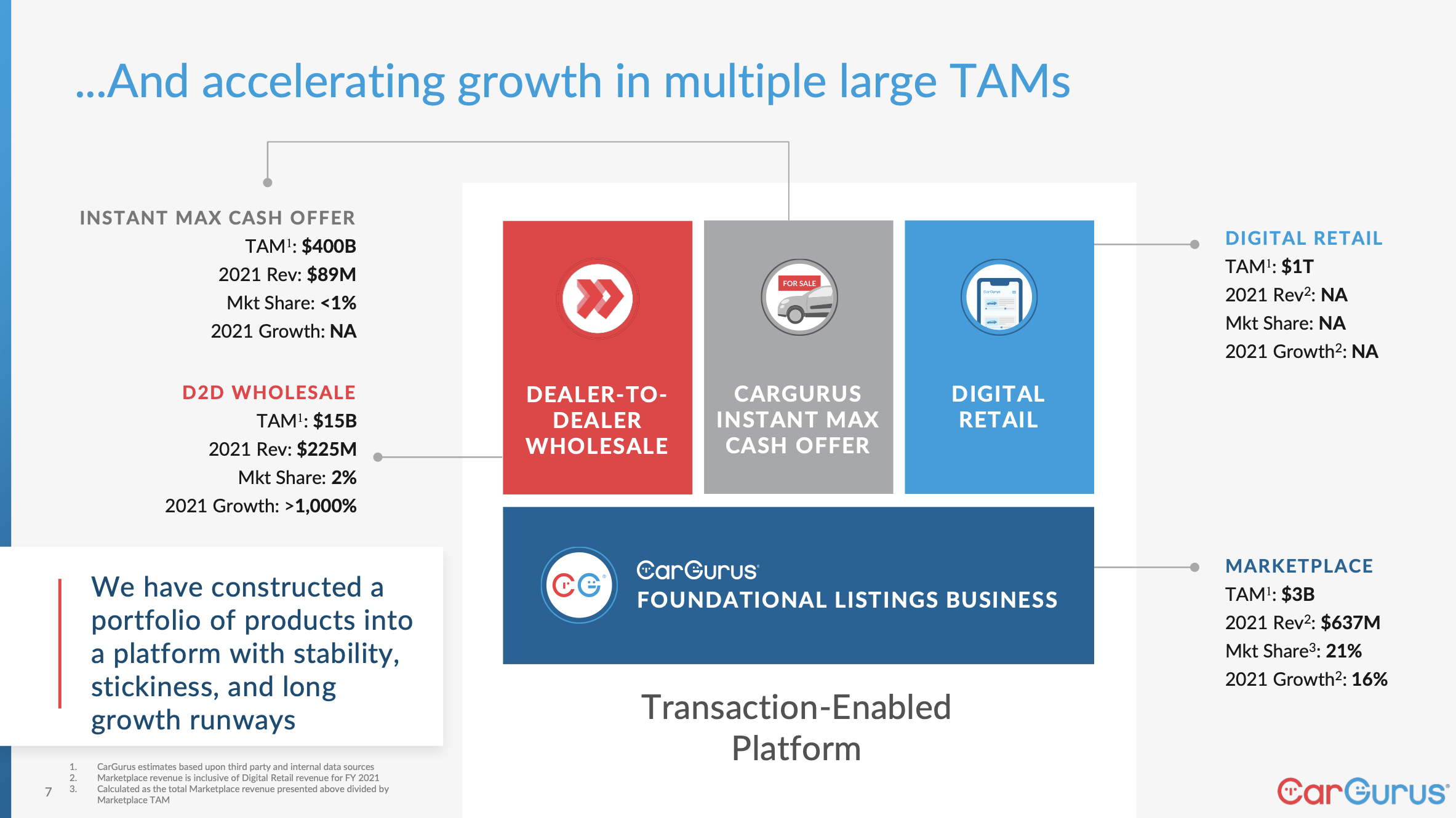

At its root, the core issue with CarGurus is its ability to scale its new business segments. In 2021, the company acquired CarOffer to facilitate used car sales between dealerships, and also launched Instant Max Cash Offer to directly connect dealers to CarGurus site visitors and place offers on their cars.

The idea, as shown in the chart below, is to create a more verticalized experience where CarGurus has more control over the entire used car-buying process:

{kind=link}

The issue, of course, is margins. CarGurus' appeal used to lay in the fact that dealers paid the company a reliable and high-margin subscription revenue fee (this model got tested during the pandemic, when many dealerships folded and CarGurus ended up effectively discounting rates to its dealerships in order to keep them on the platform and help them stay afloat). CarGurus' new revenue streams, while certainly providing a kick of growth, are coming in at low or negative margins - dragging the bottom line at just the exact moment that the market has taken on a risk-averse stance and is avoiding unprofitable names. Meanwhile, the company's core marketplace business is seeing rather flat performance.

We don't have much of a valuation incentive to compensate for this added risk, either. Given CarGurus' margin erosion with its new revenue streams, we have to look at its valuation from an earnings standpoint. Consensus is pegging FY23 pro forma EPS at $0.74 (data from Yahoo Finance ) - meaning CarGurus is now trading at an 18.3x forward P/E multiple.

With CarGurus management itself citing unpredicted volatility in the wholesale segment that the company is attempting to get off the ground, I don't see a near-term fix for CarGurus here. Without any meaningful catalysts for a turnaround, I'm content to move to the sidelines here and invest elsewhere.

Q3 download

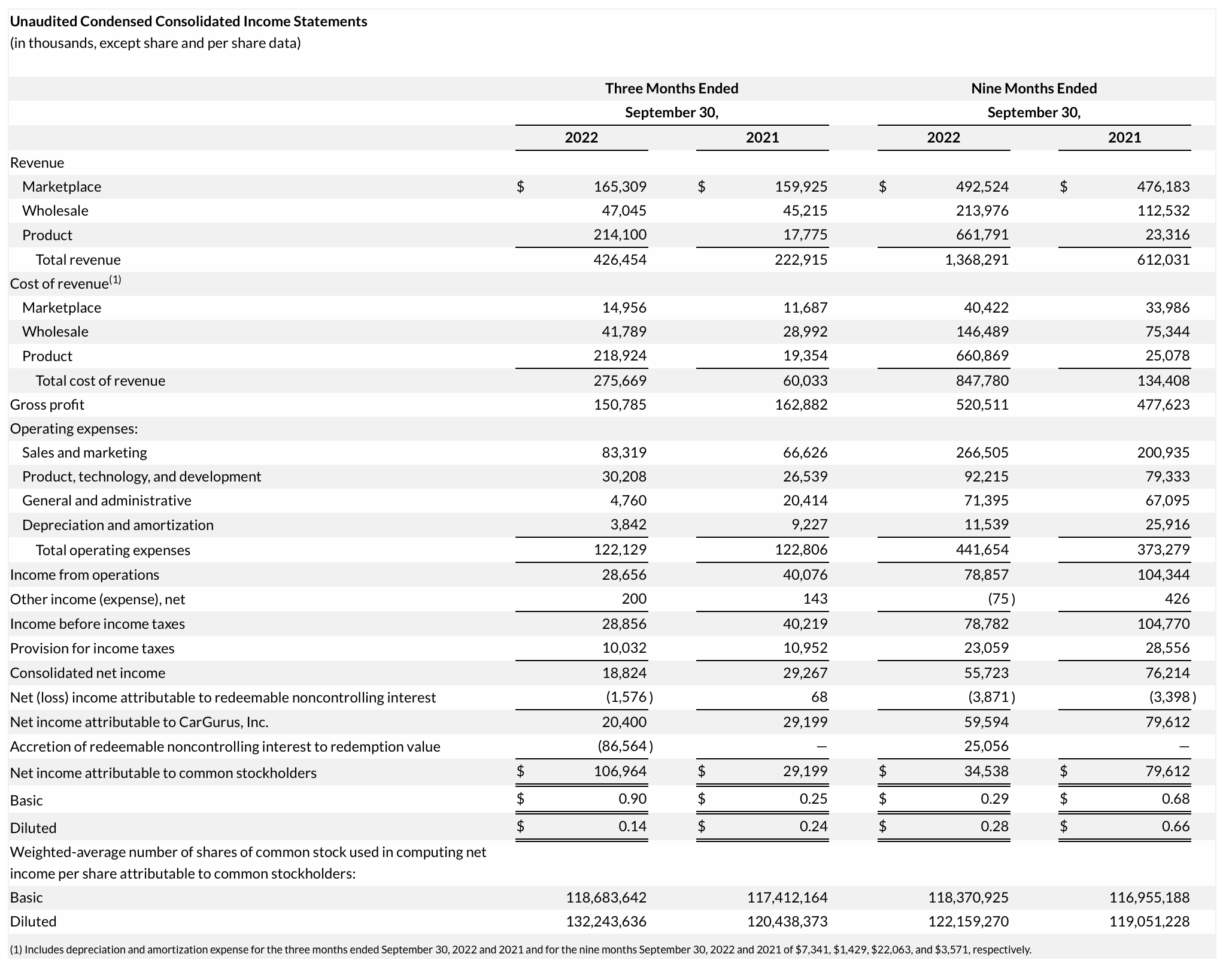

CarGurus stock faced additional pressure after the company reported disappointing Q3 results. Take a look at the earnings summary below:

{kind=link}

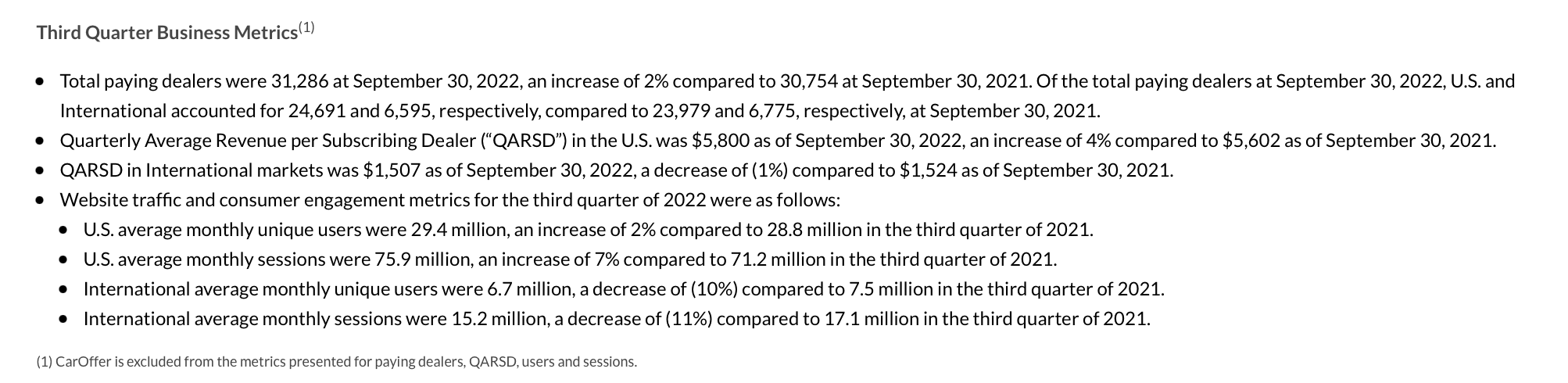

Let's start first with the marketplace business, which is CarGurus' original core revenue stream of taking in subscription fees from paying dealers. Revenue from this business was relatively flat, growing 3% y/y to $165.5 million. The good news here is that traffic metrics returned to slight growth: with U.S. monthly users and sessions up 2% y/y and 7% y/y, respectively. This compares to a decline of -15% y/y in users and -6% y/y in sessions in Q2. Declines in the international arm, meanwhile, kept on pace with Q2.

{kind=link}

As can be seen above, CarGurus' marketplace business basically finances the other segments. Product revenue, as seen above, is running at a -2% GAAP gross margin. This drag is pulling down overall company gross margins to 35%, or 37% on a pro forma basis - down from 73% in the prior year, and down 100bps from Q2.

Management noted that challenges in the wholesale business were due to macro conditions (transaction volumes declined, along with used car ASPs), but also due to operational issues in which CarGurus was forced to take brief possession of automobile inventory in a depreciating environment. Per CEO Jason Trevisan's prepared remarks on the Q3 earnings call :

Similarly, combined wholesale and product non-GAAP gross margin was not only challenged by a reduction in transactions and declining average selling prices, but also due to operational challenges.

In a declining market, dealers are more likely to arbitrate a vehicle and our operating systems and controls related to inspection, arbitration and transportation, which were built and scaled in a rising price market were not sufficient to operating an efficient business.

For example, in a transaction where a vehicle is unwound and we take brief possession, we are holding a depreciating asset in a declining wholesale price environment, which further magnifies the issue.

Unfortunately, we did not have rigorous processes in place to manage arbitration and loss effectively this quarter. So we saw increased losses on arbitration in the number of vehicles and per vehicle, as well as greater expenses related to transportation for multiple vehicle unwinds and rematches [...]

Clearly, the wholesale market trends this quarter caught us by surprise and exposed weaknesses in our offering and operations and we are maniacally focused on fixing those issues and serving our wholesale customers well, but we don’t believe that this quarter’s results should alter our longer term strategic view or our ability to realize it."

Even though Trevisan expressed continued confidence in the long term, he also noted that "it will take time to work through our Digital Wholesale operational challenges."

Pro forma operating margins in Q3 sank to 7%, down 21 points from the year-ago quarter, while in nominal dollars pro forma operating income sliced in more than half to $29.4 million.

{kind=link}

Key takeaways

In my view, there is too much risk in CarGurus to make the stock - especially at a ~18x forward P/E multiple - worth taking on. With CarGurus' issues likely to take several quarters to work through, it's best to stay on the sidelines here.

For further details see:

CarGurus: Not Worth Sticking Around For A Comeback