CARG - CarGurus: Stabilizing But Not Yet Out Of The Woods

2023-07-27 00:54:10 ET

Summary

- CarGurus has seen its stock price rise by over 50% this year, despite facing fundamental issues such as breaking into the wholesale business and slower traffic growth.

- The company has focused on its core marketplace business, which involves advertising dealers' used-car inventory on its website, and has managed to return it to low single-digit growth.

- However, overall profit is declining and hinges on the company's ability to get CarOffer back on track after fixing a multitude of operational drags.

- At a >20x forward P/E, CarGurus' valuation isn't attractive enough to warrant an immediate investment.

It's an incredible thing what lower interest rate expectations have done to the mood in the markets: investors are suddenly far more willing to bet on more speculative small-cap names. As we head through the remainder of this year, stock selection remains critical: don't assume a rising tide will lift all boats.

One rebound that has been particularly surprising to me this year is CarGurus ( CARG ). The used-car research website has seen its stock price rise by more than 50% this year after battling a slew of fundamental issues, ranging from issues breaking into the wholesale business as well as slower traffic growth. Responding to these challenges, CarGurus has opted to focus on its core marketplace business, which it has resurrected to low single-digit growth; as well as padding the overall company bottom line by shedding expenses. Pleased with this progress, the markets have sent CarGurus into an upward tilt since the start of May:

After CarGurus' recent rally, it's difficult to believe much upside is left

I am now neutral on CarGurus, but nor do I think this rally is particularly safe. I think CarGurus is a relatively balanced set of positive and negative drivers.

The upside case for CarGurus is if the company can continue to expand its marketplace business. As a reminder, CarGurus' core business comprises of advertising dealers' used-car inventory on its website, while dealers pay subscription fees to CarGurus for the exposure. As with other internet advertising-based businesses, this revenue stream comes at a very high gross margin and is the source of all of CarGurus' profits. At the moment, CarGurus remains one of the leading used-car sites in the U.S., so its brand image among consumers does provide it with a substantial moat. There's additional opportunity for CarGurus to extend its presence internationally, where traffic is still at one-quarter of U.S. levels but growing at a faster pace.

The bear case for CarGurus, however, is if the company fails to scale its other subsidiaries. The company has purposely slowed down wholesale transactions (which is the main drag to the company's most recent quarterly results) because of operational challenges ranging from the company's inspection capabilities to logistics challenges. In addition, the company has noted that many dealers are choosing to prioritize margin and minimize advertising in this tough macro environment. Dealers withdrawing from the CarGurus platform creates a vicious cycle for the company - if less inventory and shrunken geographic coverage starts to plague CarGurus' platform, consumers will also start leaning on the website as a primary landing spot for finding a new car, which will in turn reduce CarGurus' appeal to other dealers.

From a valuation front, I don't think CarGurus at current levels appropriately compensates for these risks. At current share prices near $22, CarGurus trades at a market cap of $2.55 billion. After we net off the $456.7 million of cash on the company's most recent balance sheet, the company's resulting enterprise value is $2.09 billion.

Meanwhile, for the next fiscal year FY24, Wall Street analysts are expecting CarGurus to generate $1.07 billion in revenue (+14% y/y) and $1.10 in pro forma EPS (data from Yahoo Finance ). And if we assume CarGurus holds its current 18% adjusted EBITDA margin on its revenue next year, its adjusted EBITDA would be $192.6 million. This would put CarGurus' valuation multiples at:

- 1.9x EV/FY24 revenue

- 10.8x EV/FY24 adjusted EBITDA

- 20.4x forward P/E

In my view, I don't see enough appeal in these valuation multiples - especially for a business that is handling so many fundamental snags - to entice an investment at current levels. I'd recommend staying on the sidelines here and adopting a watch-and-wait approach.

Q1 showcases a stabilizing marketplace business

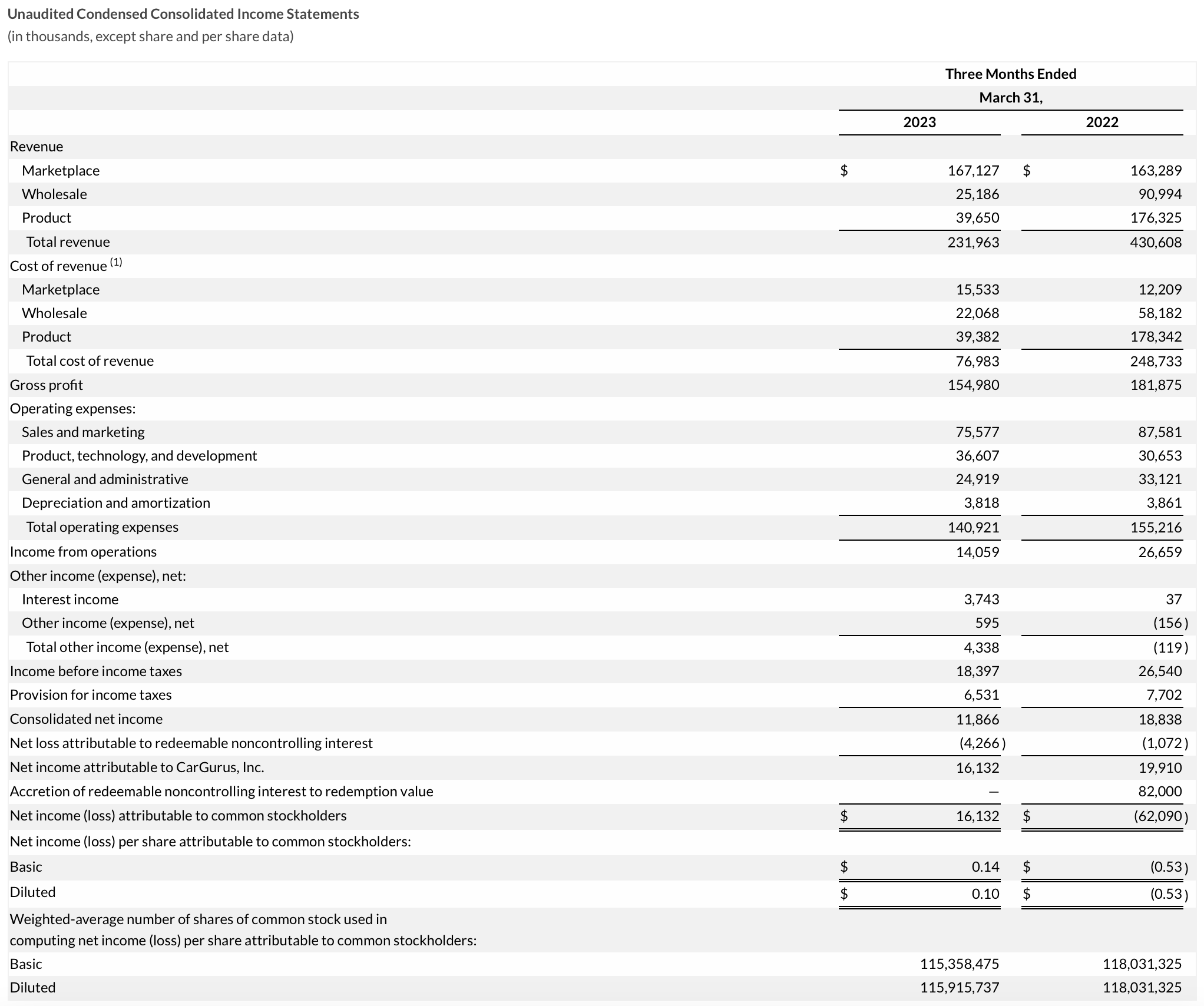

This being said, we should acknowledge the positives that CarGurus has demonstrated that allowed the stock to rally in the first place. Take a look at the company's Q1 results in the table below:

{kind=link}

Revenue declined -46% y/y at a total company level to $232.0 million, but that's largely due to the company's intentional decision to slow down CarOffer (wholesale and product revenue) while it fixed operational challenges. The core marketplace business, meanwhile, saw revenue growth of 2% y/y to $167.1 million.

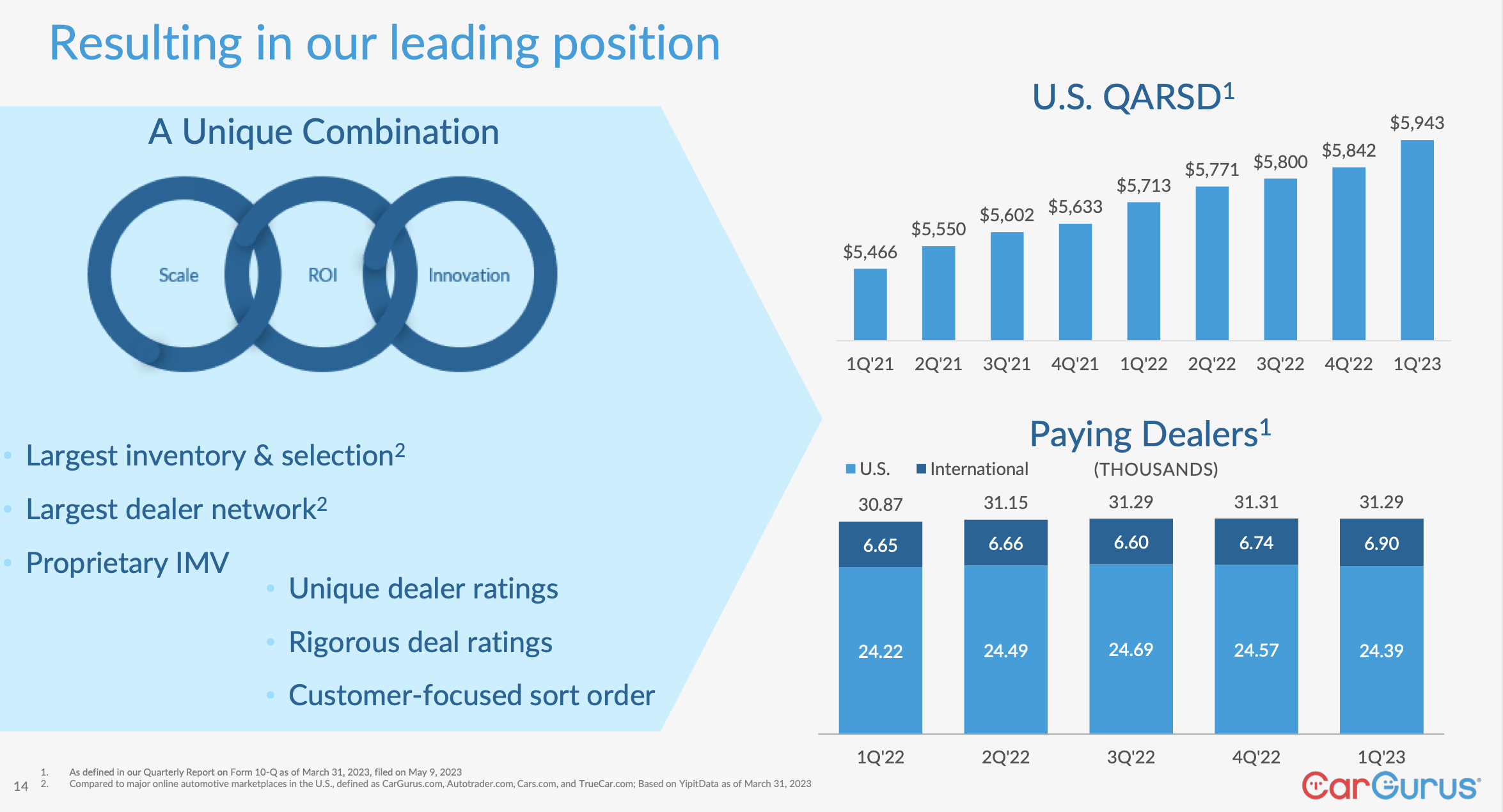

The slide below shows the key metrics for the marketplace segment. The one red flag is that paying dealers saw a slight sequential reduction to 31.29k, but did grow 1% y/y.

{kind=link}

While CarGurus notes that smaller dealers did churn, the company has signed on larger dealers that move greater volumes - which allowed U.S. quarterly average revenue per subscribing dealer (QARSD) to grow 4% y/y to $5,943.

Here is some commentary from CEO Jason Trevisan on dealer dynamics within the quarter, made during his prepared remarks on the Q1 earnings call:

I'm pleased to share we exceeded our forecasted Marketplace revenue for the quarter. One key driver of our Marketplace results this quarter was the scaling and overperformance of monthly recurring revenue, resulting from annual business reviews or ABRs.

Through the ABR process, we are renewing a cohort of meaningfully underpriced dealers each quarter, and we have made significant improvements to our renewal process by streamlining our packaging and enhancing the value proposition for our dealers through the addition of new features and benefits to our listings tiers that best support our dealers' needs.

Even during a period of historically low inventory, our improved ABR process demonstrated the strength of our platform to effectively scale and recognize more appropriate value delivered while simultaneously enabling us to be more consultative in introducing cross-product adoption opportunities that best support our customers' business needs. In fact, in Q1, the ABR process was 2.5x more successful in converting Area Boost dealers into a new offering known as Digital Deal with geographic expansion."

The company's new feature, Digital Deal, allows customers to do more of their transaction online (from receiving trade-in estimates to getting prequalified for financing). These new capabilities have been adopted by ~2.2k of CarGurus' dealers (roughly 7% of its base), which has contributed to QARSD growth.

Traffic has also remained healthy, with monthly unique users up 3% y/y to 32.0 million in the U.S. International unique users, meanwhile, grew 5% y/y to 7.2 million.

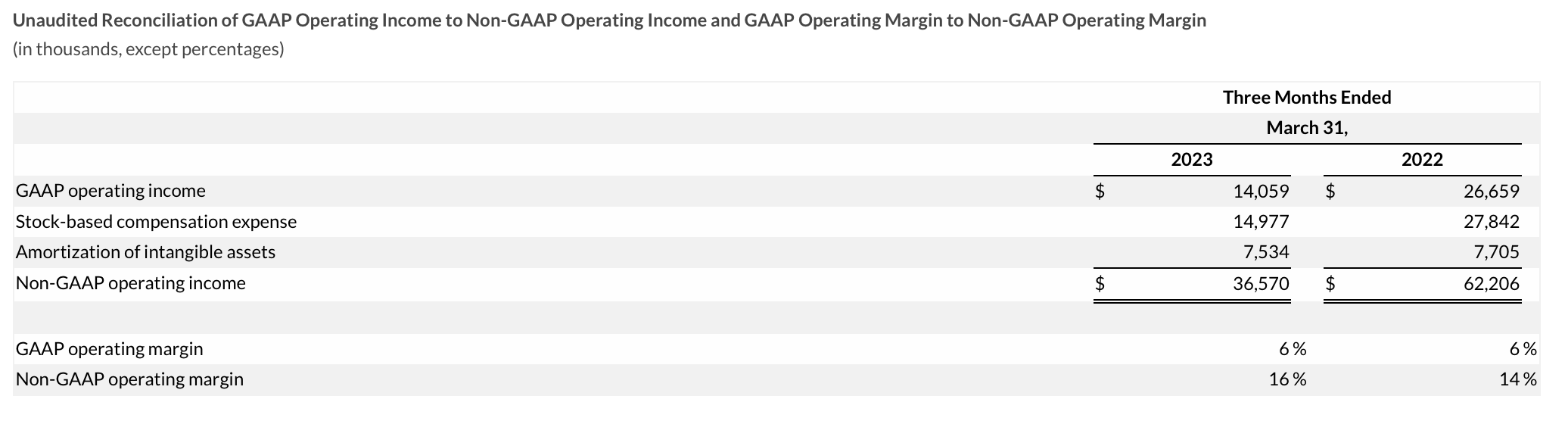

CarGurus' favorable revenue mix shift toward its higher-margin marketplace business has helped the company bring up its pro forma operating margins to 16%, up two points from the year-ago quarter. The company has also reduced its sales and marketing spend to boost profitability.

{kind=link}

On a nominal dollar basis, however, it's worth noting that pro forma operating income did decline -41% y/y to $36.6 million.

Key takeaways

If you've held onto CarGurus shares since the start of the year, in my view, it's a good time to lock in gains and move to the sidelines. Though healthy marketplace metrics are encouraging, it remains to be seen if CarGurus can both maintain traffic and dealer engagement while getting its wholesale business back on track.

For further details see:

CarGurus: Stabilizing, But Not Yet Out Of The Woods