CARG - CarGurus: Still Attractive After Earnings But I'll Hold Off For Now

2023-05-11 09:15:18 ET

Summary

- After the earnings, the company’s share price skyrocketed.

- I wanted to delve deeper into the company's financials mainly while touching on the sector and business outlook briefly.

- The company has a very strong balance sheet, but with a couple of financial metrics trending down is slightly worrisome.

- An intrinsic value calculation suggests that even after the earnings, the company still has some room to the upside, however, I will hold for now due to macroeconomic headwinds.

Investment Thesis

After beating Q1 ’23 estimates by a decent margin and jumping over 16% on the day, I wanted to dig deeper into CarGurus, Inc. ( CARG ) financials, and a bit into the sector outlook to see if, after such a melt-up in stock price, the company is still a good investment.

With improvements to the CarOffer segment and used car prices picking back up, which leads to more dealer transactions, I can see that even with somewhat conservative estimates, the company is a buy at these levels, however, the stock price may come back down slightly due to the volatility of the sector and overall macroeconomic headwinds.

Briefly on Q1 Results

As expected, y-o-y revenues were down substantially, however, revenue of $232m beat consensus estimates by $17.65m, and non-GAAP EPS of $0.26 beat estimates by $0.10. GAAP and non-GAAP gross margins improved by 25% each. Operating and sales and marketing expenses were down 1% and 13% y-o-y respectively.

Sector Outlook

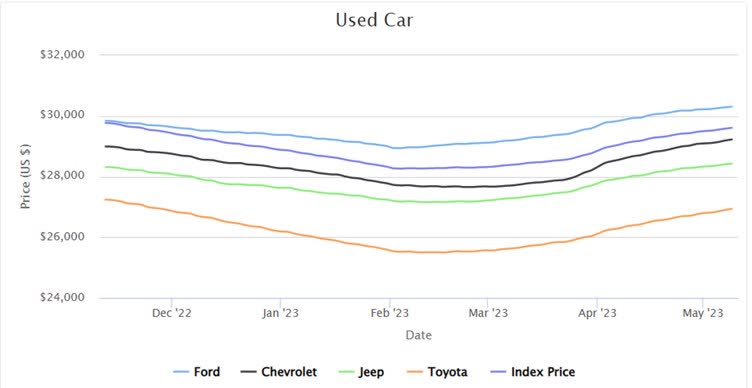

I believe that the company is prepared for anything that the auto sector has in store for it. When it comes to the dealers’ side of things, if prices have been going down for a while, the dealers are less likely to advertise their cars in hopes that the prices will pick back up. That is what’s been happening in the first months of ’23.According to CarGurus themselves, used car prices have started to pick back up, which will be a positive catalyst in the next quarter.

{kind=link}

In terms of new cars, I believe that the emergence of subsidies by governments all around the world to produce more electric vehicles will present an opportunity for the company also. The chip shortages are still prevalent all around the world, the prices are still on a climb as you can see from the graph below.

{kind=link}

As cars depreciate in value, the way that CarGurus can make money from the dealers who are looking to get rid of a depreciating asset quickly is to help them advertise the vehicles more effectively so they can sell them off.

CarOffer Headaches Improving

This has been quite a headache for the company for a while now. I was pleasantly surprised that the fixing of this segment has been well on its way this past quarter and the management seems very excited about the progress they made in reducing inefficiencies. The team has been working hard on improving the inspection process in the last quarter and this resulted in a 70% reduction in arbitration cases from the peak we saw in the fourth quarter. This segment in the long run will offer really good profit margins if everything is going to get fixed and it starts operating as intended.

Financials

Most of the graphs I will be displaying will be up to the end of FY22, as I believe they represent the company better than looking at quarterly figures which may fluctuate wildly. I will mention some figures from the latest report if needed for some extra color.

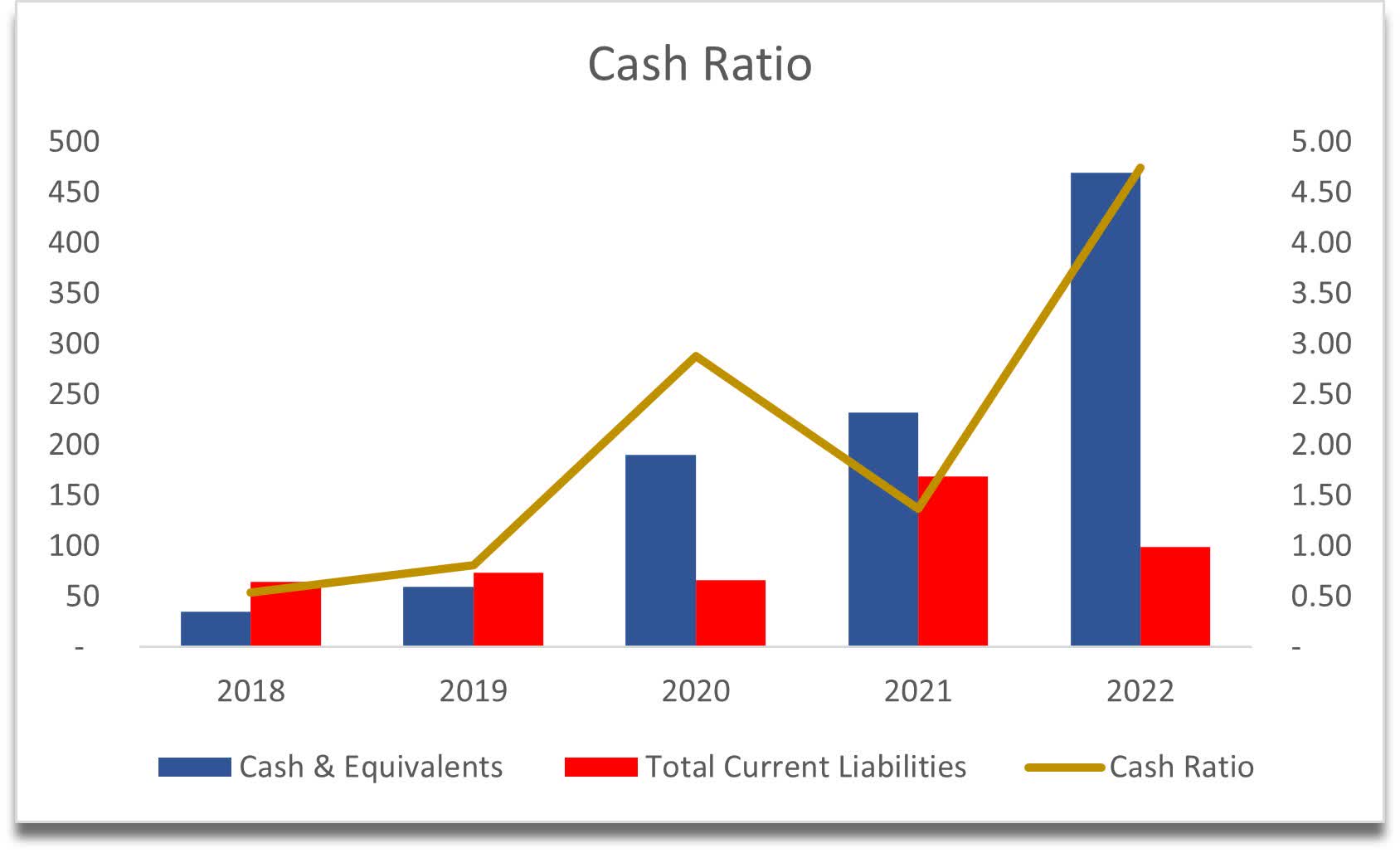

At the end of FY22, the company had around $470m in cash and zero debt, which is great. In the latest quarter, the cash position is relatively similar at $457m. The company hasn't needed to get into debt for any reason which presents a very strong financial health that will be able to weather any upcoming recession in my opinion, especially if the recession is meant to be a mild one.

Furthermore, the company's cash ratio, which is a more stringent measure of liquidity that takes into account only cash available and short-term investments to pay off its short-term obligations, is at almost 5, which means that the company can pay off its short-term obligation 5 times over with only the cash available. As of the latest quarter, the ratio went down slightly to 3.68x, however, that is still a very healthy position to be in. The company has no liquidity issues at all. Naturally, the company's current ratio is also well above my minimum of 1.5 to 2.0, standing at 4.37x as of Q1 '23.

{kind=link}

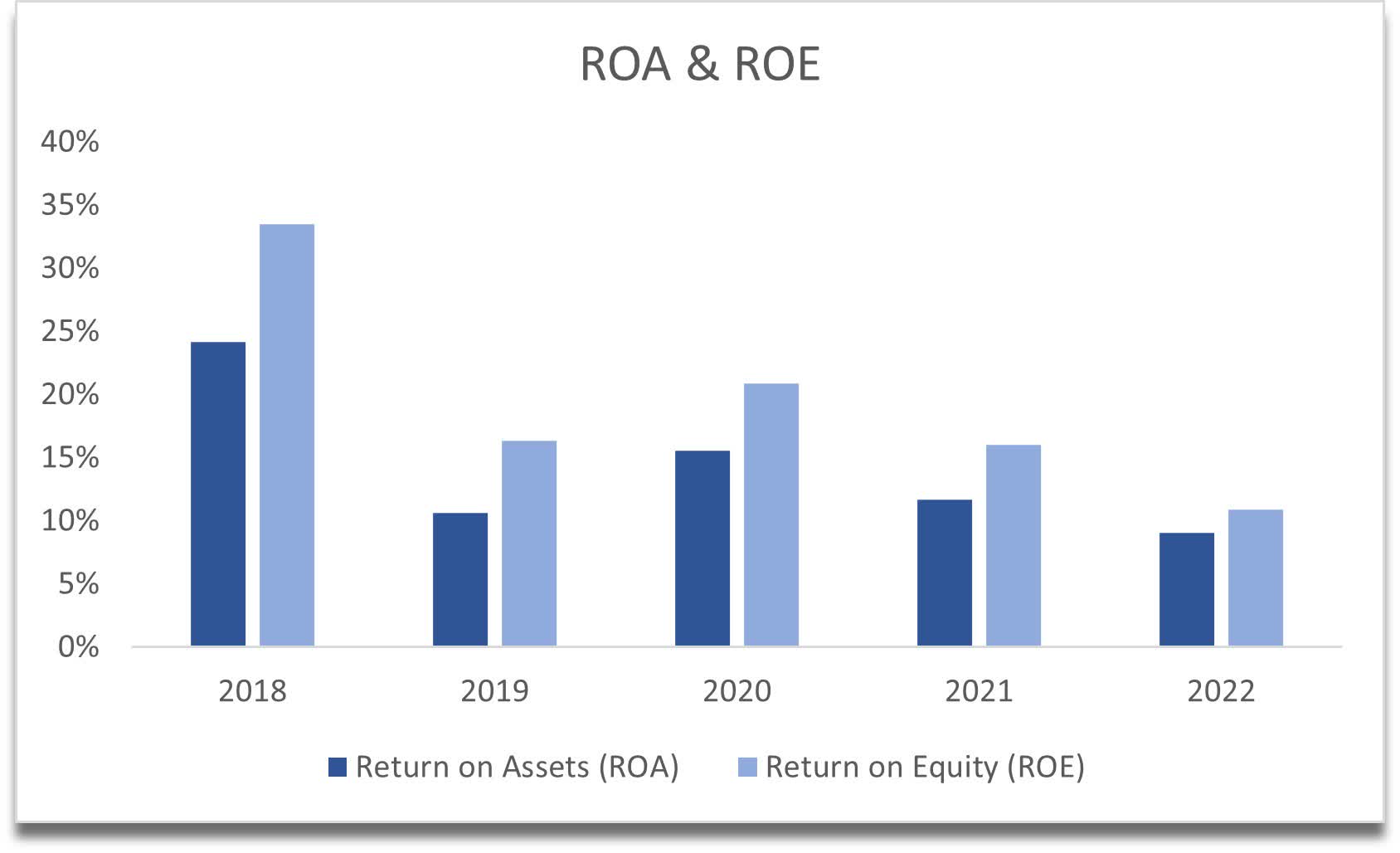

In terms of profitability and efficiency, the company’s ROA and ROE metrics are also decent, however, when looking at the past, these have been better before. I would like to see these trending up in the future and not keep going down. With more efficiency measures and further digitization initiatives in the future, I could easily see these coming back up or at least stabilizing.

{kind=link}

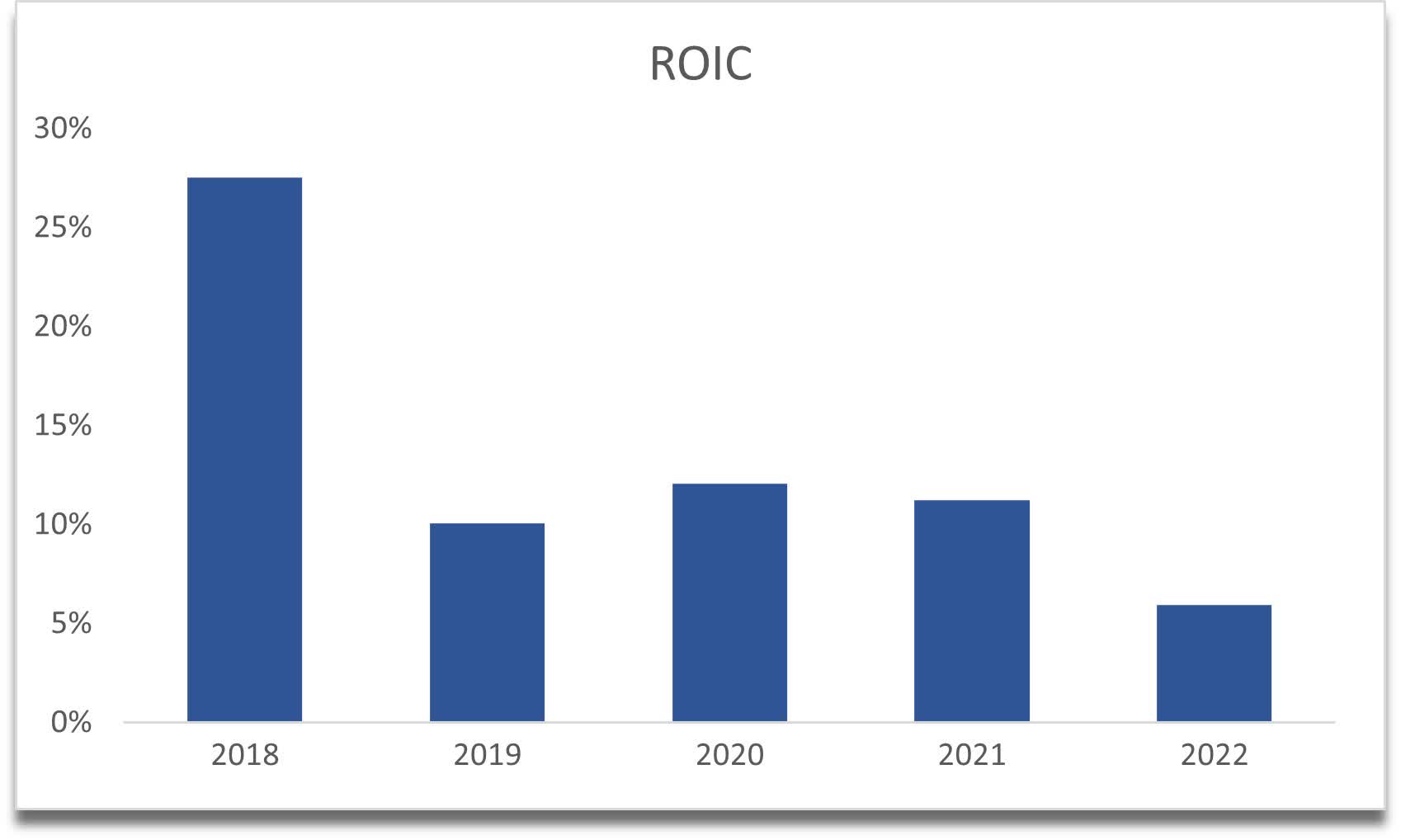

The company's ROIC has also seen a similar trend which is slightly worrying also. The company is losing its competitive edge and moat. With further economic headwinds in the short term, I could see this trending further down if the management is not able to invest the capital in positive NPV over time. I'd like to see ROIC coming back up above 10%, this would indicate a very healthy and strong company in my opinion that is creating value for shareholders.

{kind=link}

Overall, even with the metrics showing a downtrend, I believe the strength of the balance sheet suggests the company is in a good position to weather economic downturns in the near term.

Valuation

The company has seen stellar revenue growth in the last couple of years fueled by rising car prices. The trend as I showed for the new cars is still intact, while for the used cars, although returned to an uptrend, however, I would expect much more volatility there. Car prices are not going to climb forever, especially with the Fed tightening still, which will bring down demand in the short run, I cannot be too overly optimistic about the company’s future growth. For the base case, average revenue growth will be 11% for the next decade, for the optimistic case, 13%, while for the conservative case, 9%.

In terms of margins, these have been varying wildly over time with different mixes over the last 2 years. I will argue that with further improvements in the digital space, efficiencies will arise, and the company will find a stable mix of profitability over the next 10 years. I will assume the company manages to improve gross margins and operating margins by 200bps by 32, which I think is very conservative. Net profit margins will go from 5.1% in FY22 to 11% by ’32. Just last year in FY21 the company’s net margins were at 11%, so I think it is manageable.

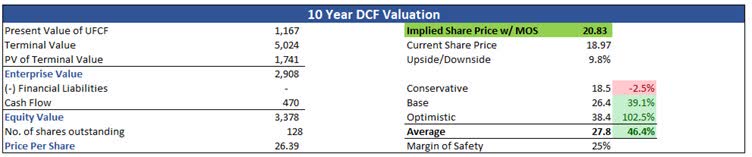

To keep it even more conservative, I will add a 25% margin of safety to the intrinsic value calculation, which is the minimum I give to companies that present a very healthy balance sheet.

With that said, the company's intrinsic value is $20.83, which still implies around a 10% upside from current valuations, even after the melt-up of the Q1 announcement.

{kind=link}

Closing Comments

The reason for this article was to look into the company itself rather than focusing on the sector and the company’s prospects too much, because if I can find a company that is already making good money and has a strong balance sheet, the company may be a good investment in the long run, however, we may end up paying too much if the company already saw a huge run-up recently. According to my calculations, the company is still quite attractive in the long run, however, the results caused the share price to skyrocket very quickly and I'm not a big fan of that because I'm looking for a steady price appreciation. The company is quite volatile, and I believe the price will come back down over the next few months, mainly due to the macroeconomic headwinds and the negative sentiment in the markets overall, which may present a better entry point with a better risk/reward ratio.

CarGurus is a decent company with great financials. If it can manage to iron out the problems with a couple of its segments, mainly CarOffer, it is a good long-term investment. For now, I will wait a little longer to see if the share price will come down slightly as usually happens.

For further details see:

CarGurus: Still Attractive After Earnings, But I'll Hold Off For Now