CZMWF - Carl Zeiss Meditec: One Of The Highest Premiums I'll Accept

2023-08-08 05:13:37 ET

Summary

- Carl Zeiss Meditech is a subsidiary of Carl Zeiss AG and manufactures tools for eye examination and medical lasers.

- The company has a strong financial performance with high gross and net margins.

- Despite being heavily focused on the German market, the company has shown solid growth and profitability. I say the company is a "Buy" Here.

Dear readers/followers,

in this article, I'm going to give you a glimpse and my introductory look at Carl Zeiss Meditech ( OTCPK:CZMWF ) ( OTCPK:CZMWY ). This company won't make you a dividend millionaire - it won't turn your investment into a 10,000% RoR in a short time. At least not how I see it.

However, what the company will do is offer you value, safety, and quality. A sleep-well-at-night sort of business that will keep growing for as long as the business does well. And based on the sort of trends we see for the business, I believe that this path of growth will be ongoing for some time.

In this article, I'm going to present you with Carl Zeiss Meditec and see what we can expect from the company in the medium to long term.

Also, of course, why this company is a "BUY".

Carl Zeiss Meditech - A storied company

So, first of all, Carl Zeiss Meditech is a subsidiary of the massive Carl Zeiss AG. What it does, specifically, is to manufacture tools for the examination of eyes, as well as medical lasers, solutions for neurosurgery, dentistry, gynecology, and oncology. As the name suggests, this makes it into a Meditech company.

It owns some of the most advanced tools on the entire market, including products like the CIRRUS 6000, the ReLEx Smile laser system, and other products. The company, with its head company Carl Zeiss AG, has a history of over 170 years. Carl Zeiss has multiple subsidiaries, but out of those subsidiaries, only the Meditech company is publically traded. Carl Zeiss AG, meanwhile, has a complex ownership structure where it's majority-owned by the Carl-Zeiss Foundation. Like many old German companies, Zeiss was founded by one or several families, and their descendants still maintain control of the company. Giving a majority of the shares to the market is something that for many companies, especially older ones is not done in Germany.

{kind=link}

Carl Zeiss Meditech, therefore, is part of one of the oldest still-existing optics manufacturers in the world. Its products, even outside of the Meditech segment, are being used across the world in cameras, in technology, and in various devices.

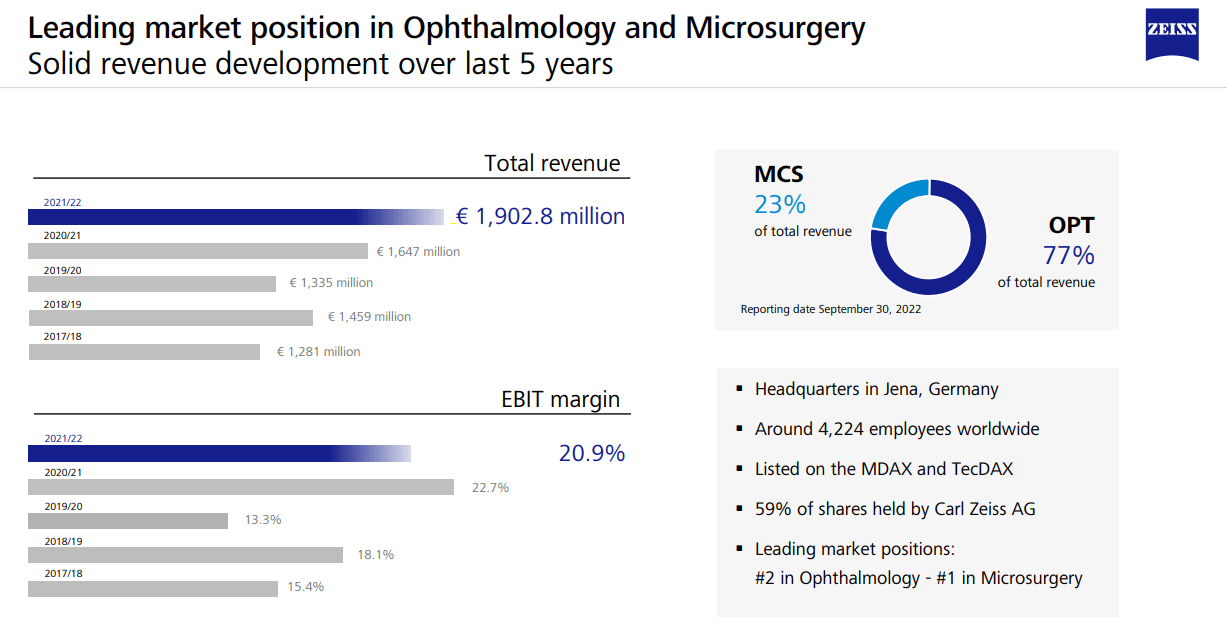

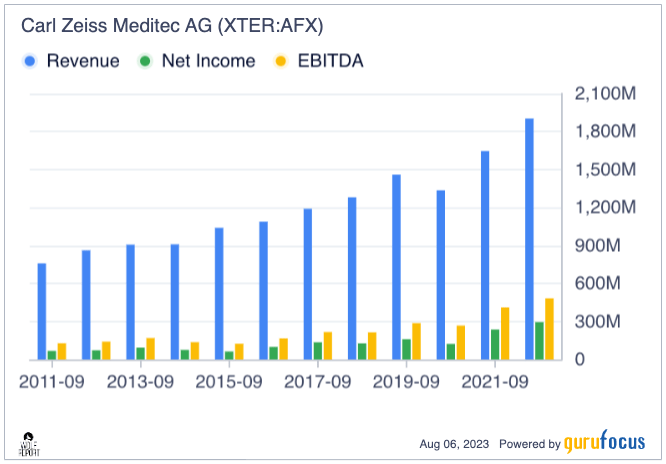

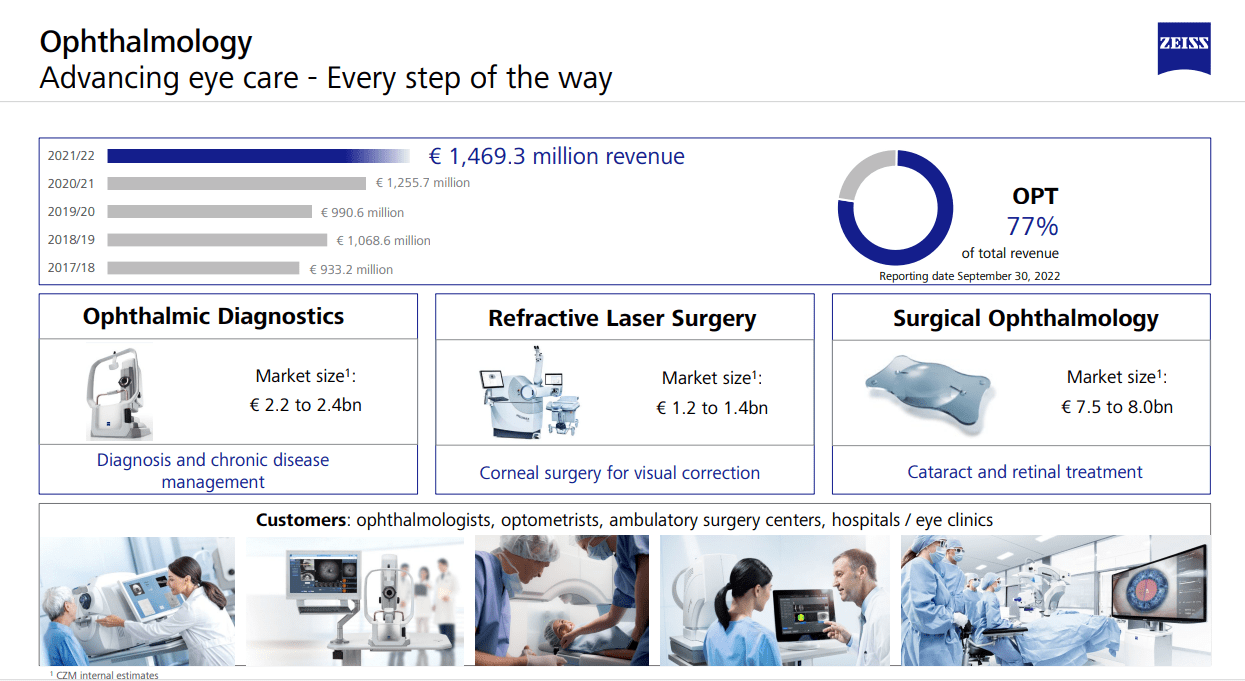

The company reports in two segments. Ophthalmic devices make up about 77% of the sales mix, with Microsurgery at around 23%. On this sales mix, the company manages a gross margin of about 60%, a pre-tax margin of about 21.2% for EBIT, and a very impressive net margin of 15%+. This is among the better in the sector and amongst its peers.

The company is compared to other Meditech and optic firms. This includes Sartorius Stedim, West Pharmaceutical Services, Resmed, Gerresheimer AG, and others.

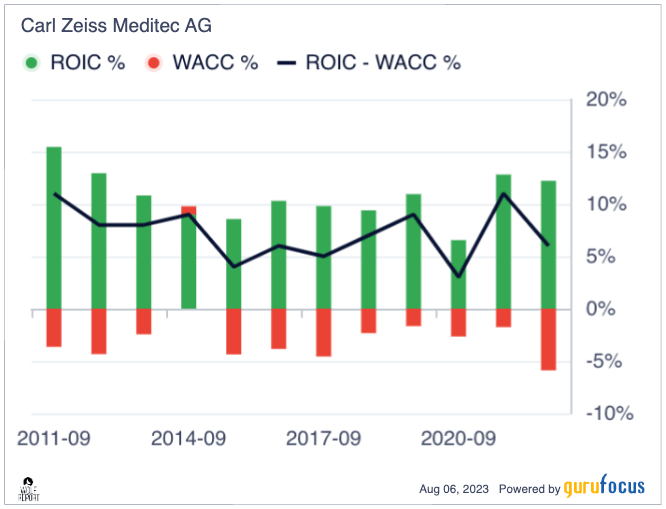

The company's return metrics put it at the top 84th percentile above in terms of percentile. Overall, the company has the sort of economic tendencies you'd expect from a business of this quality level.

{kind=link}

Generally overall stable growth. You won't, of course, find much dividend yield here. It's rare for German companies overall to be above 3.5%, and especially rare for companies in this sector or subsector. Carl Zeiss Meditech gives you a current total of 1.1%, though only at a 30% EPS payout ratio and a relatively high growth rate. Almost 18% over the last year, which does put it above its peers in terms of dividend growth. Due to the ownership structure though, I would be careful about expecting significant streaks of dividend growth for the company.

What's impressive here is the company's profitability and the sky-high shareholder equity in relation to total assets. This is a quality business, it's a world leader in a field, and it's not going anywhere. Despite one of the most difficult business environments in over 10-20 years, the company has remained profitable at a very high level.

{kind=link}

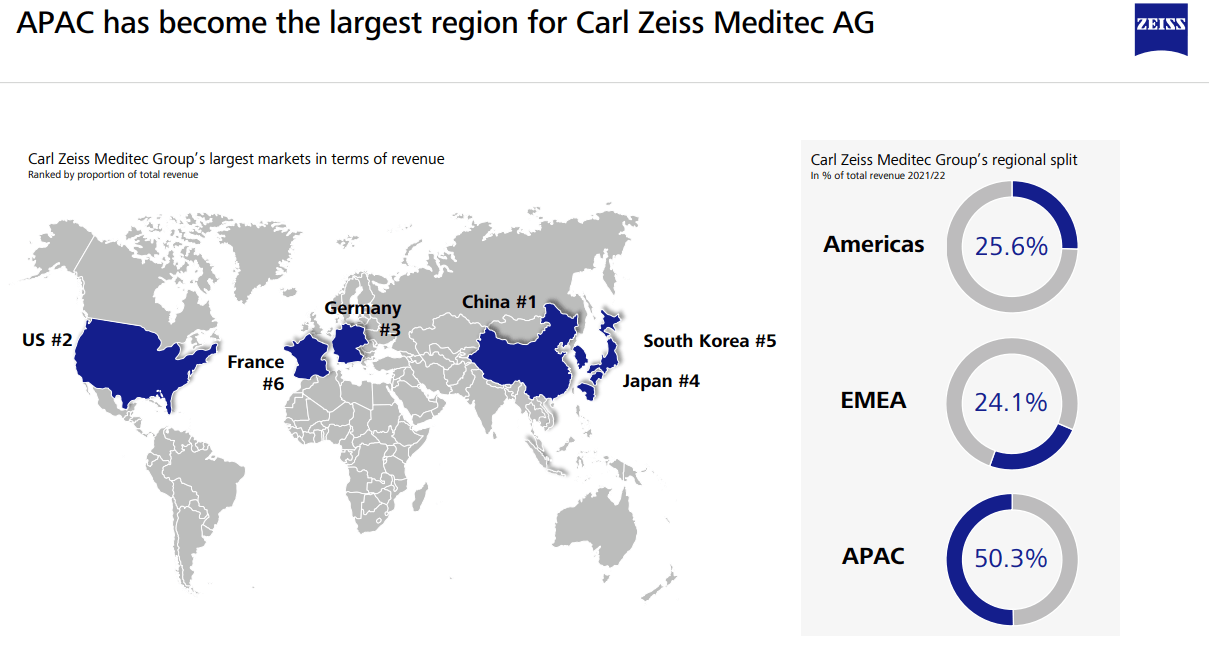

The company is attractively split in terms of its geographic base. APAC is now the largest region for the company, with China, South Korea, and Japan as major markets, followed by the USA, with large portions in EMEA as well, of course.

{kind=link}

However, it's been less than 3 days at the time of writing this article that we have the 9M22/23 results, the results were solid. The period saw strong top-line growth with a continued high order backlog. The company's EBIT margin was at 16.2%, down some but mostly due to investment OpEx for growth - I consider it likely that the ground lost here will be recovered. It's also part of why we're seeing an opportunity in the company as an investment here.

And, EPS is up due to a product of volume and interest income as well as FX hedging. 7.3% EPS growth and 13.3%% YoY revenue growth tell us a tale of growth in both of the company's business units, despite significant SCM constraints and logistical challenges.

It shows the company's quality that things are as good, despite the market being as challenged as we're seeing here.

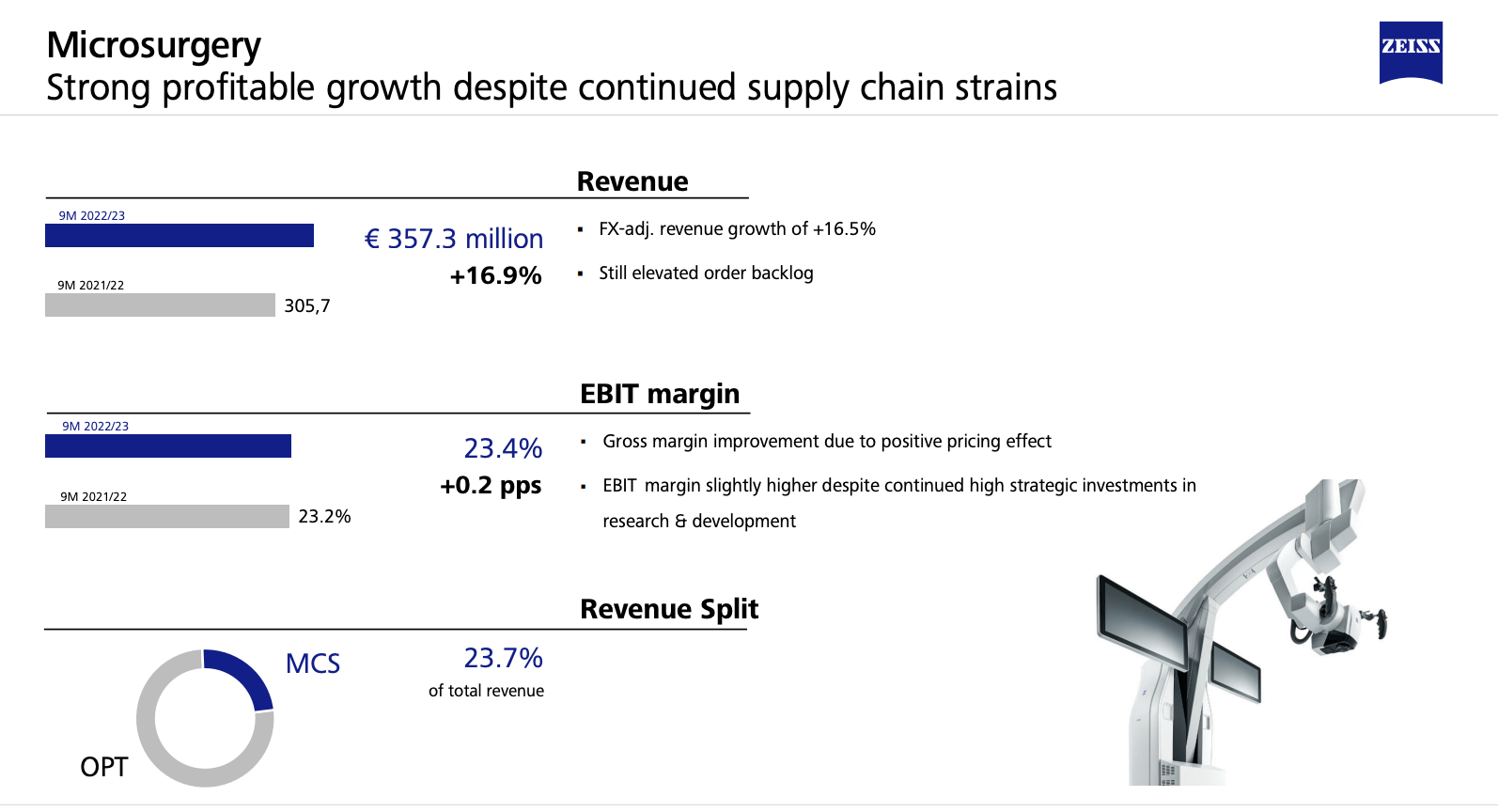

Some granularity from segments here. The company's main segment, Ophthalmology, which by the way is the surgical subspeciality of diagnosing and treating eye disorders , saw growth related to higher and higher delivery rates for the company's devices. Some weaker margins due to a less ideal product mix, some supply constraints, and above-average CapEx percentage of sales are going into both R&D and SG&A - but overall, very good results at a 76.3% part of the revenue mix.

{kind=link}

As you can see, Microsurgery saw similar, and even better trends in terms of profitability, and a slightly growing share of the overall revenues. Geographically speaking, NA was the strongest, inclusive of SA, which is encouraging, as the company needs to grow in its non-legacy geographies.

The underlying trends and fundamentals for this company are extremely solid. Because of the aging population and growing affluence in certain sectors and geographies, the demand for the company's services, including cataract surgeries, is going to continue to climb. There's also the trend of accelerating myopia and the high prevalence of conditions like these, which will continue to drive underlying demand for what the company offers.

The increased workflow will increase demands for solutions that the company offers, and with increasing access to health care in emerging economies and markets, there exists a significant, untapped market with massive potential for this company.

The coupling of eye care...

{kind=link}

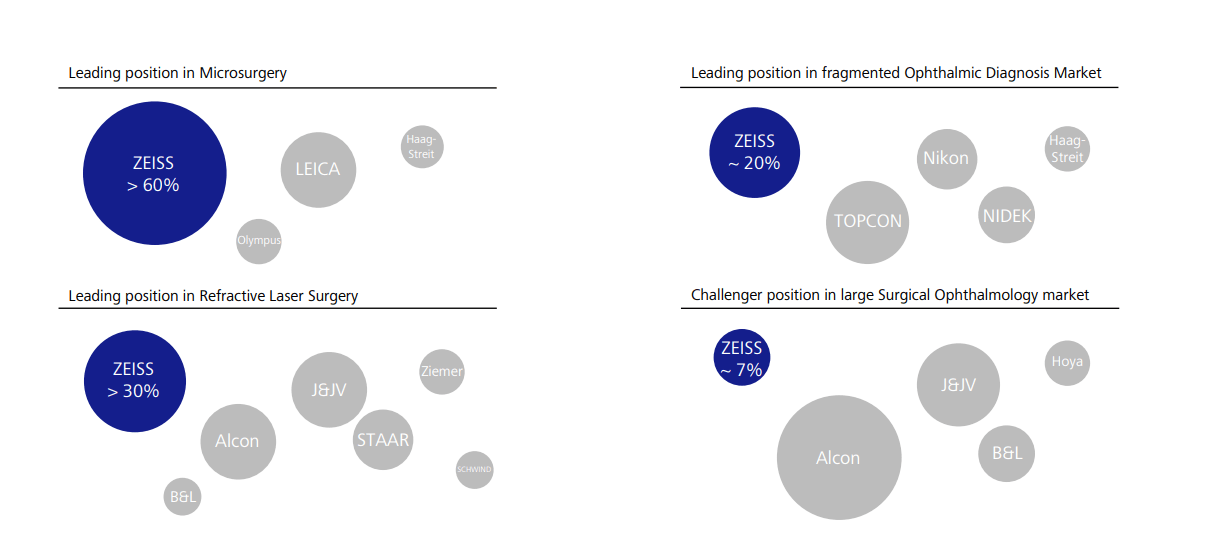

...with its microsurgery appeal, including things like surgical oncology, visualization tech, and in-Vivo pathology is driving sales here. Company customers are hospitals, clinics, dental offices, and other similar areas. Despite only being at $2B in revenue, the company actually has a market-leading position in 3 out of 4 relevant markets for the business.

{kind=link}

So - plenty to like here, as I see it. I've been keeping an eye on this business for several years, and while it has never been my #1 investment due to the moderate growth/RoR profile, it's quickly becoming an interesting potential in this market, to where I bought my first shares less than a week ago.

Let me show you the valuation and showcase why that is

Carl Zeiss Meditec - Plenty of things to like in quality German Meditech - but valuation isn't one of them

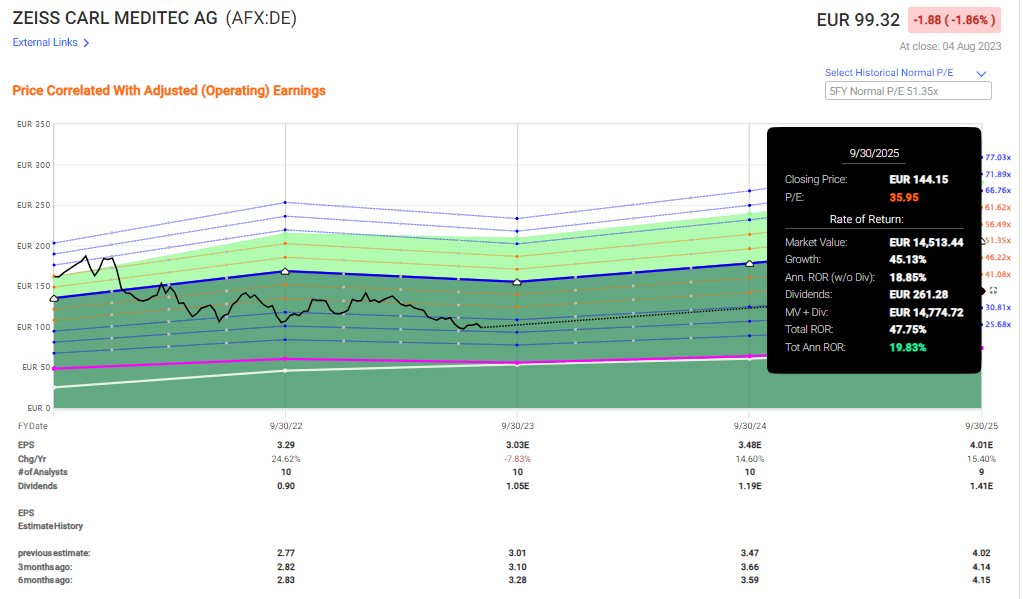

So, this is the highest premium I'll probably ever write about in this sector. This is because the typical average valuation for this company if we look at 5-15 year trends comes to well over 40x P/E.

On a 5-year normalized, this comes to 51x+ P/E.

You may already realize at this point that there is no way on this green earth that I'm paying 50x P/E for a business - and you'd be right, I'm not. That's not how I'm calculating the company. For as long as 50x P/E was the basic expectation here, I was uninterested.

But, it's not anymore.

Based on the assumptions that, first, Carl Zeiss Meditech has expanded its moat in the last 20 years, and second, new entrants into the field are unlikely to see immediate traction, I'm willing to put Carl Zeiss Meditech at a range of 30-37x P/E. That's the 15-20 year average of this company, which I view as being far more realistic than what we've seen previously.

Based on a 20-year average of 30x P/E, the lowest RoR based on current returns would be close to 12% per year until 2025 , but as high as 20% per year once we start expecting 37x.

{kind=link}

The piece that's amazing here is that there is actually a 2025E upside to this company on the basis of a sub-40x P/E. That's not something we've seen for several years prior to this.

S&P Global analysts put the company at an average of around €90/share to €175/share, but this is down from highs of €240+ per year a few years back. The company's average PT is now €130/share.

A good price target at this juncture, I believe, would be the midpoint target in my range of around 33x P/E, which comes to around €125/share for the native ticker on the ETR with the symbol AFX. I would not buy the ADR - it has too low liquidity.

This is a company that due to its very strong market position deserves at the very least your attention. I will understand though, if this is a company you may not want to add to your portfolio. However, keep in mind that it's been entirely possible to "ride" this company to overvaluation and make over 200-300% RoR in a relatively short amount of time.

That's not what I am expecting here. I actually see significant value in investing in this company at such a comparatively fair multiple going by how high it usually is.

However, it's also a very long-term and "slow" investment. So I'm adding slow, in small batches, and it's one I intend to hold "forever" unless it goes back into overvaluation.

I give you my introductory thesis here. Risks are obvious, to me. This is highly premiumirized. I view it as justified based on market share and performance - but if this were to change, or the premiumization was to change, we could be flat for years here.

However, I view that as unrealistic.

Thesis

- Carl Zeiss Meditech is an incredibly qualitative Medtech business originating out of Germany but with an international growth and sales profile. It does not offer a compelling yield, but what it does offer is a very compelling overall long-term upside. Even conservatively speaking if you accept some of the premiumization here, you have triple-digit upside potential

- However, this requires you, as mentioned, to accept one of the highest premiums I've ever seriously considered for this market. Provided it's essentially a market leader in extremely specialized areas, this might make sense to you as well - but I would size your position with extreme care.

- Nonetheless, I add my voice to the chorus of "BUY" with this company. A quality company has the right to cost quite a bit - and this is the highest I accept for a business like this. I say "BUY".

- My PT comes to a 33x forward P/E, which puts the company at around €125/share long-term.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has realistic upside based on earnings growth or multiple expansion/reversion.

It's even possible for me here, to call the company actually "Cheap" - and that is rare for this business.

For further details see:

Carl Zeiss Meditec: One Of The Highest Premiums I'll Accept