BLDR - Carlisle Companies: Shares Are Worth Considering After Tumbling To Fresh 52-Week Low

2023-04-11 08:41:19 ET

Summary

- Shares of Carlisle Companies hit a fresh 52-week low point on April 5th and have only recovered marginally since then.

- This comes at a time when financial performance is robust and the company's overall health is positive.

- Add on top of this favorable guidance and how shares are priced, and it's now worth considering.

One of the great things about the market is that the picture for a business can change. Just because an opportunity looks mediocre or bad at one point does not mean that it can't turn good. A great example of this change taking place can be seen by looking at Carlisle Companies ( CSL ), a business engaged in a variety of activities centered around building products. Given everything that is going on in the economy, with high interest rates aimed at combating inflation, and both inflation and interest rates serving as a deterrent to significant capital investments, you might think that it would be crazy to touch anything in the building space. In recent months, the market has generally agreed with this assertion, pushing shares down significantly even as the broader market increased. But given how far the stock has fallen, and management's own expectations for the current fiscal year, I would make the case that now represents a good time to consider looking at Carlisle Companies through a bullish lens.

Shares have fallen… hard

From their 52-week high mark, shares of Carlisle Companies have fallen hard. As of this writing, the stock is down an impressive 33.9% compared to where it peaked late last year. The stock is also very close to its 52-week low, hovering just 3.4% above that mark. You can imagine my dismay, then, when I look at my own track record in looking at the enterprise. Since I last wrote about it in September of last year, the stock has fallen approximately 30%. That means it was awfully close to the 52-week high mark when I put my thesis out on the company. Over that same window of time, the S&P 500 has generated upside of 4.3%, translating to a rather significant delta for shareholders. Fortunately, while my call on the company wasn't the greatest, it definitely could have been worse. Instead of rating it a 'buy' or something even more aggressive than that, I rated the business a 'hold' to reflect my view that it should have generated returns that would more or less match the market moving forward.

This rating came about even in spite of strong revenue and profit growth generation achieved by management. The company was moving nicely toward achieving its objectives for the 2025 fiscal year through a combination of acquisitions and organic growth. However, I did feel at that time that recent fundamental performance might not have been sustainable and I believed that shares were rather pricey. That led me to my more cautious, but ultimately overly optimistic, 'hold' designation.

{kind=link}

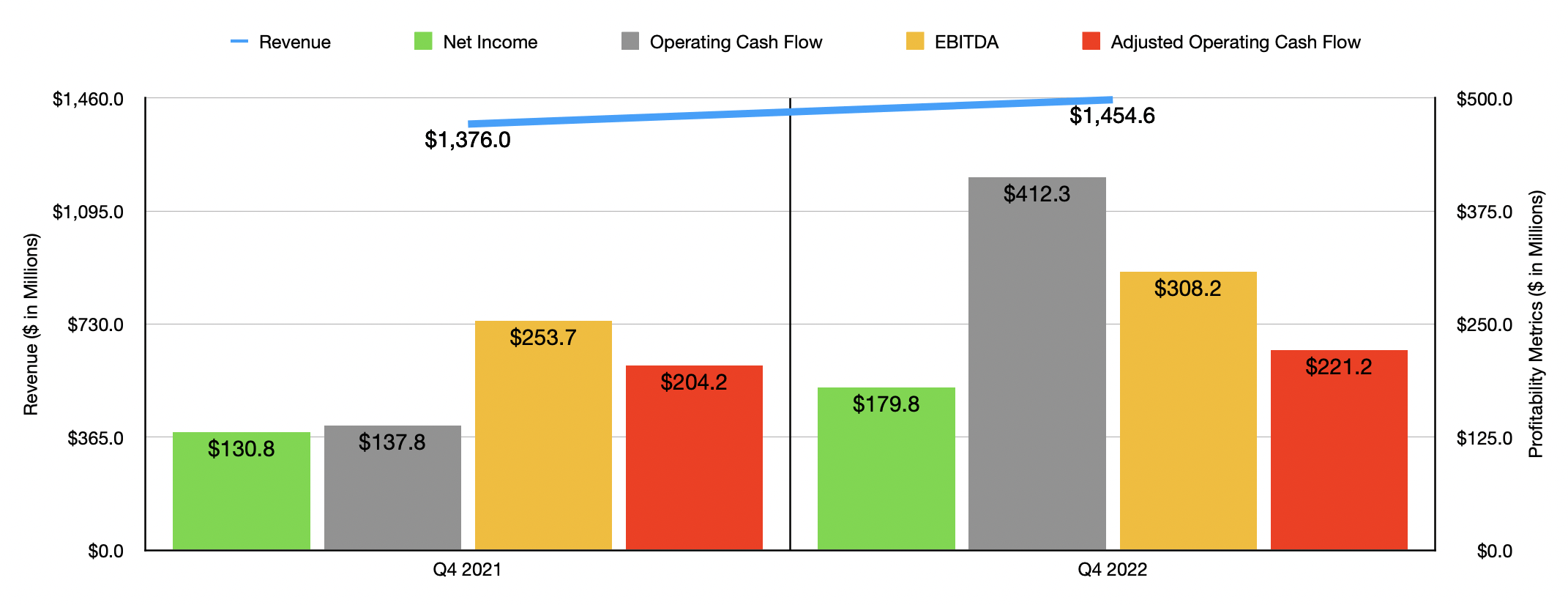

Looking at this return disparity, you might think that the company was exhibiting significant weakness. But this couldn't be further from the truth. Consider how the company performed during the final quarter of its 2022 fiscal year . Sales during that time came in at $1.45 billion. That's 5.7% higher than the $1.38 billion generated only one year earlier. Actual organic revenue achieved by the company was even more impressive, coming in at 6.6%. Revenue associated with acquisitions added another 0.2% to the company's top line. However, the firm was negatively impacted to the tune of 1.1% from foreign currency fluctuations.

The greatest growth for the company during this time came from its Carlisle Interconnect Technologies segment. Through this segment, the company produces wire and cable, including optical fiber, for the commercial aerospace, military, medical device, industrial, and other end markets. Products made under this segment also include sensors, connectors, cable assemblies, racks, and other related offerings. The firm also provides customers with installation kits, as well as services associated with both engineering and certification. Revenue here spiked 21.5%, soaring to $224.1 million, on the back of strengthening aerospace and medical end markets. All of the other segments of the company have also grown year over year, but they were less significant from a revenue growth perspective. The largest segment, for instance, is known as Carlisle Construction Materials and it is responsible for things like roofing products and related offerings. Year-over-year growth for this segment was a much more modest 2.2%, with that number rising to 3% on an organic basis.

On the bottom line, the picture for the company continued to improve as well. Net income of $179.8 million was 37.5% higher than the $130.8 million reported one year earlier. A rise in the company's gross profit margin from 28.4% to 30.4% aided on this front and was attributable to an increase in pricing that was greater than inflationary pressures, as well as certain cost-cutting initiatives management enacted. The company also benefited from a reduction in its selling and administrative expenses from 14.1% of sales to 13%, though management has not provided any significant discourse on why this was. Other profitability metrics followed a similar trajectory. Operating cash flow, for instance, skyrocketed from $137.8 million to $412.3 million. Though if we adjust for changes in working capital, we would have seen that number rise more modestly from $204.2 million to $221.2 million. Meanwhile, EBITDA managed to grow from $253.7 million to $308.2 million.

{kind=link}

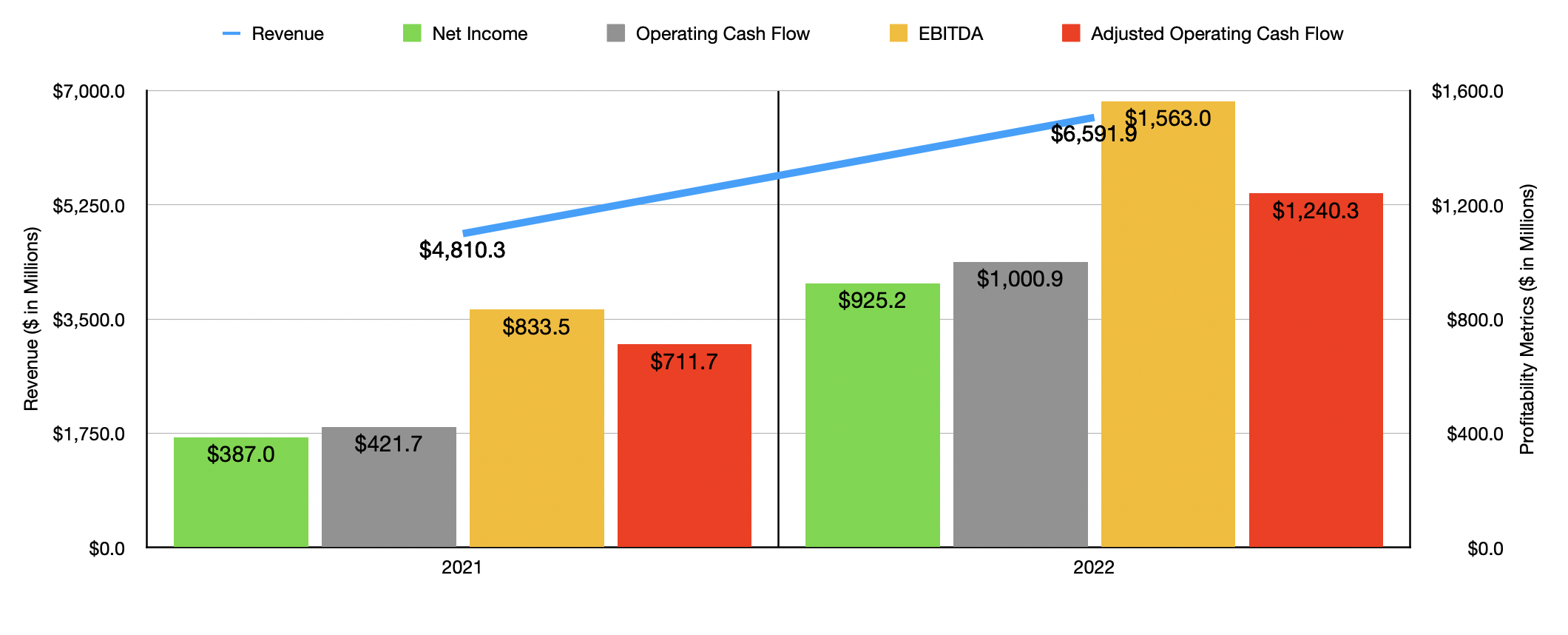

In the chart above, you can see results for the entirety of the 2022 fiscal year compared to the 2021 fiscal year. As you can see, the year-over-year growth experienced in the final quarter of the year was not a one-time event. But when you do compare the growth data, you would see a bit of weakening in the fourth quarter compared to the fiscal year as a whole. Sales growth, for instance, shot up 37% in 2021 compared to the 5.7% seen in the final quarter of the year only. Net profits, meanwhile, more than doubled.

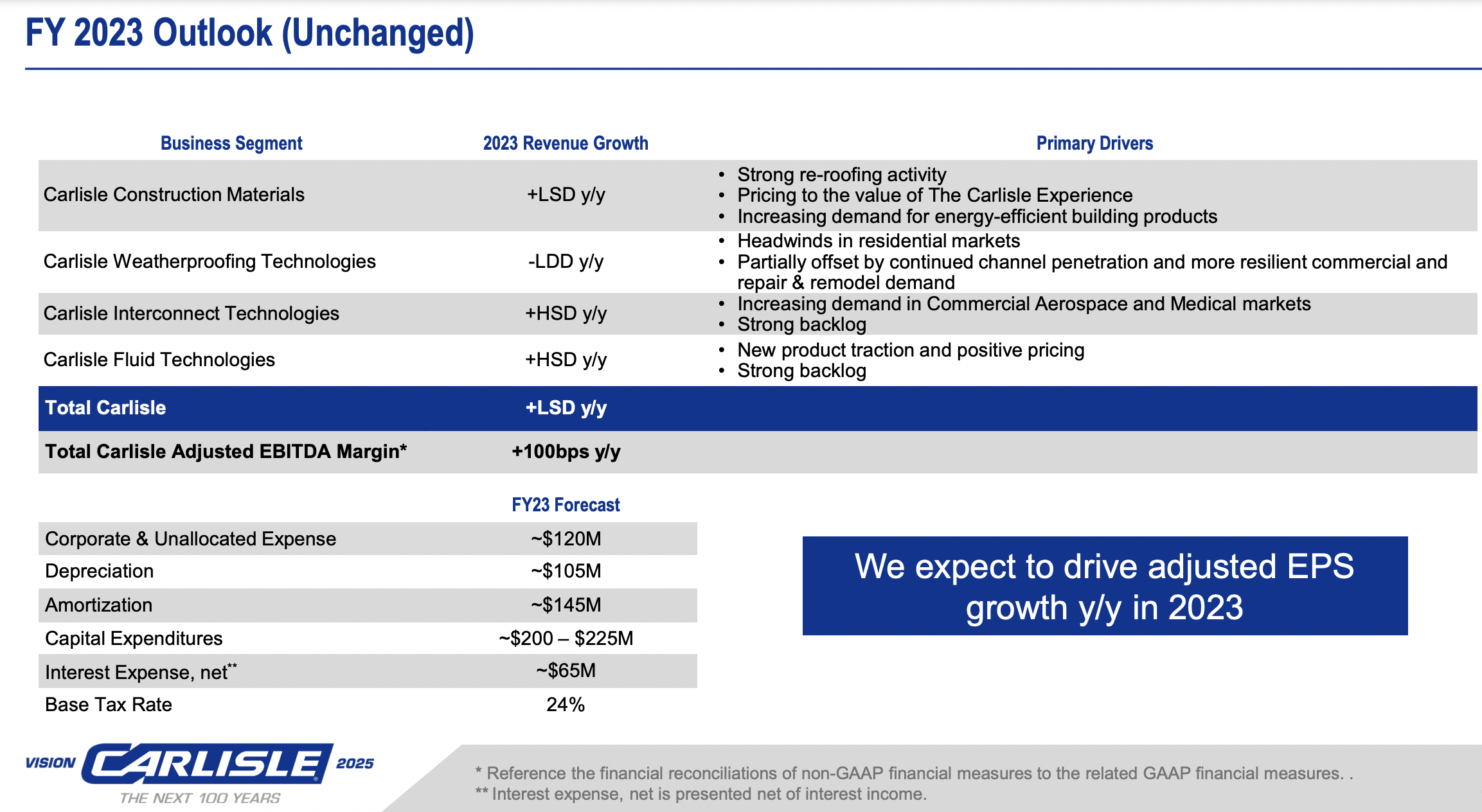

Given this slowdown, you might think that the market's decision to push the stock lower is an appropriate reaction to concerns about the future. However, management remains optimistic. They haven't provided comprehensive guidance for 2023. But they do expect three of the four operating segments to report growth this year compared to last. The Carlisle Construction Materials segment, for instance, is supposed to grow at a rate in the low single digits thanks to strong re-roofing activity, higher pricing, and a rise in demand for energy-efficient building products. The Carlisle Interconnect Technologies Segment, meanwhile, should grow at a high single-digit rate because of rising demand associated with the commercial aerospace and medical markets. In the past, I have written a good deal about the aerospace markets. And I will say that I agree with their assertion that it should be a bright spot in 2023.

{kind=link}

And finally, the Carlisle Fluid Technologies segment should also grow at a high single-digit rate, thanks to new product traction and higher pricing, as well as strength in the company's backlog. The only weakness will come from the Carlisle Weatherproofing Technologies segment, with sales contracting at the low double-digit rate because of headwinds in residential markets that will more than offset more attractive commercial and repair and remodel demand activities. No specific guidance was given on the bottom line. But management did say that the firm's EBITDA margin should grow by about 1%. Overall revenue for the company is forecasted to increase at a low single-digit rate. If we assume that this would translate to a 3% rise in sales, and we factor in the assumed EBITDA margin improvement, this would translate to a reading of $1.68 billion for the year. That would be about 7.3% above the $1.56 billion experienced in 2022.

{kind=link}

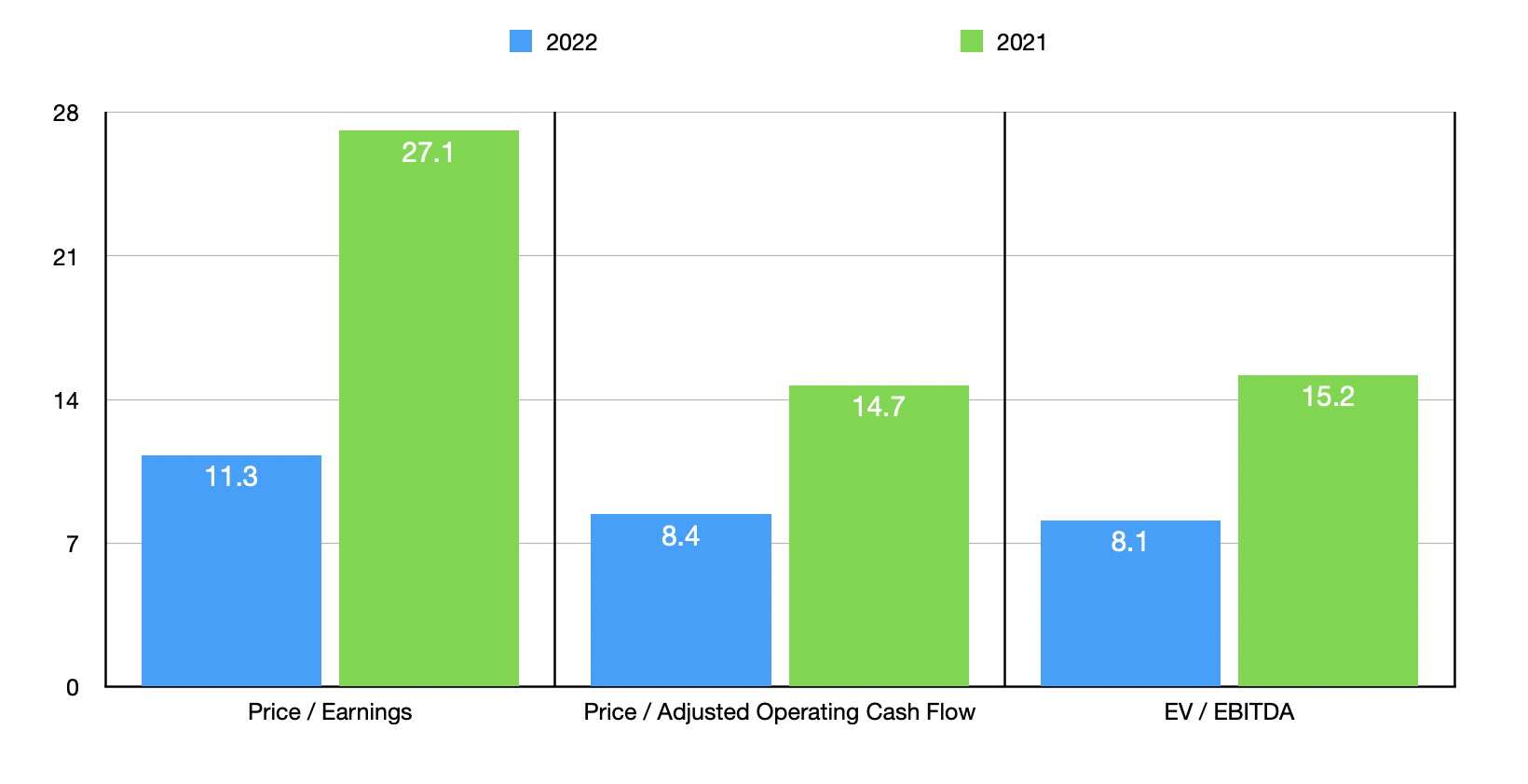

Absent some major shift in management's thinking, 2023 is slated to be a good year for the company. But even if we assume that results won't be any better and that they will, instead, match what was achieved last year, the picture for the company looks quite promising. On a price-to-earnings basis, Carlisle Companies is trading at a multiple of 11.3. This is down considerably from the 27.1 reading that we get using data from 2021. The price to adjusted operating cash flow multiple of 8.4 is nearly half the 14.7 that we would get using data from one year earlier. And the EV to EBITDA multiple over this time has plunged from 15.2 to 8.1. As you can see in the table below, I also compared the company to five similar firms. Using all three of the valuation metrics, I figured that only one of the five firms was cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Carlisle Companies |

| 11.3 |

| 8.4 |

| 8.1 |

| Advanced Drainage Systems ( WMS ) |

| 14.5 |

| 8.8 |

| 8.7 |

| Masco Corporation ( MAS ) |

| 13.1 |

| 13.2 |

| 10.4 |

| Builders FirstSource ( BLDR ) |

| 5.3 |

| 4.0 |

| 3.4 |

| Lennox International ( LII ) |

| 17.1 |

| 28.1 |

| 13.3 |

| A.O. Smith ( AOS ) |

| 44.1 |

| 26.1 |

| 31.0 |

Takeaway

The past few months have been rather painful for investors in Carlisle Companies. Although I didn't buy shares in the company, I understand all too well what it's like riding shares of an enterprise down so much over such a period of time. At present, the market seems to be worried about the future for anything related to the building or construction space. This is also logical. However, management remains optimistic about 2023 at this time, plus shares are trading at levels that make a great deal of sense. Even if we see financial performance revert back to what it was in 2021, the stock would be, perhaps at worst, only slightly overvalued. This creates a favorable risk-to-reward opportunity and justifies a more bullish soft 'buy' rating in my book.

For further details see:

Carlisle Companies: Shares Are Worth Considering After Tumbling To Fresh 52-Week Low