CABJF - Carlsberg: Still Surprising To The Upside; Stock Now Expensive

2023-05-03 03:25:27 ET

Summary

- Carlsberg shares have continued to climb and are currently up over 40% since my opportunistic 'Buy' rating following the Russian invasion of Ukraine.

- Beverage volumes in Western Europe are holding up much better than I expected in the face of significant price increases, necessary to offset inflation in its cost base.

- While performance at the business and stock level is surprising me in a good way, these shares now look expensive.

Danish brewer Carlsberg A/S ([[CABGY]], [[CABJF]], [[CABHF]]) has performed a lot better than I expected it to over the past year or so. Covering it with an opportunistic 'Buy' rating following the Russia-Ukraine war sell-off, my main worry was the near-term impact of significantly higher energy and commodity prices on margins, driven by the conflict.

Knock-on effects were also a source of downside here, with inflation and worsening consumer finances the most obvious one. That was perhaps a slightly more pressing concern in Carlsberg's case as its operating footprint skews heavily toward Europe, where I feel consumers are a bit more fragile financially than, say, in the United States.

These shares have returned over 40% since then inclusive of dividends. That is a reflection of how well the business has held up in that time, with profits and beverage volumes both holding up better than I expected in the face of input cost inflation and offsetting price hikes.

Looking ahead, I am concerned that the hitherto resilience in the European consumer may finally start to give way as we head deeper into FY 2023, and that would have negative implications for price elasticity here.

My main concern, though, is the stock's valuation. I already thought Carlsberg was close to fair value in my last update back in Q4, and with these shares up over 20% in that time I now think we are heading toward overvalued territory.

A Solid Performance Last Year

Between significantly higher input costs and weakening European consumer finances, what should have been a fairly straightforward year for Carlsberg instead produced major headwinds.

Lager is a fairly fungible product, and I had my doubts that Carlsberg would be in a position to raise its prices without sacrificing an inordinate amount of volume in the process. While that sentiment applies on an industrywide basis - brewing is not the best place to look for pricing power - in previous articles I also mentioned that I felt that Carlsberg's beverage portfolio was a little bit light at the premium end, and that would have exacerbated any pricing/volume issue even more.

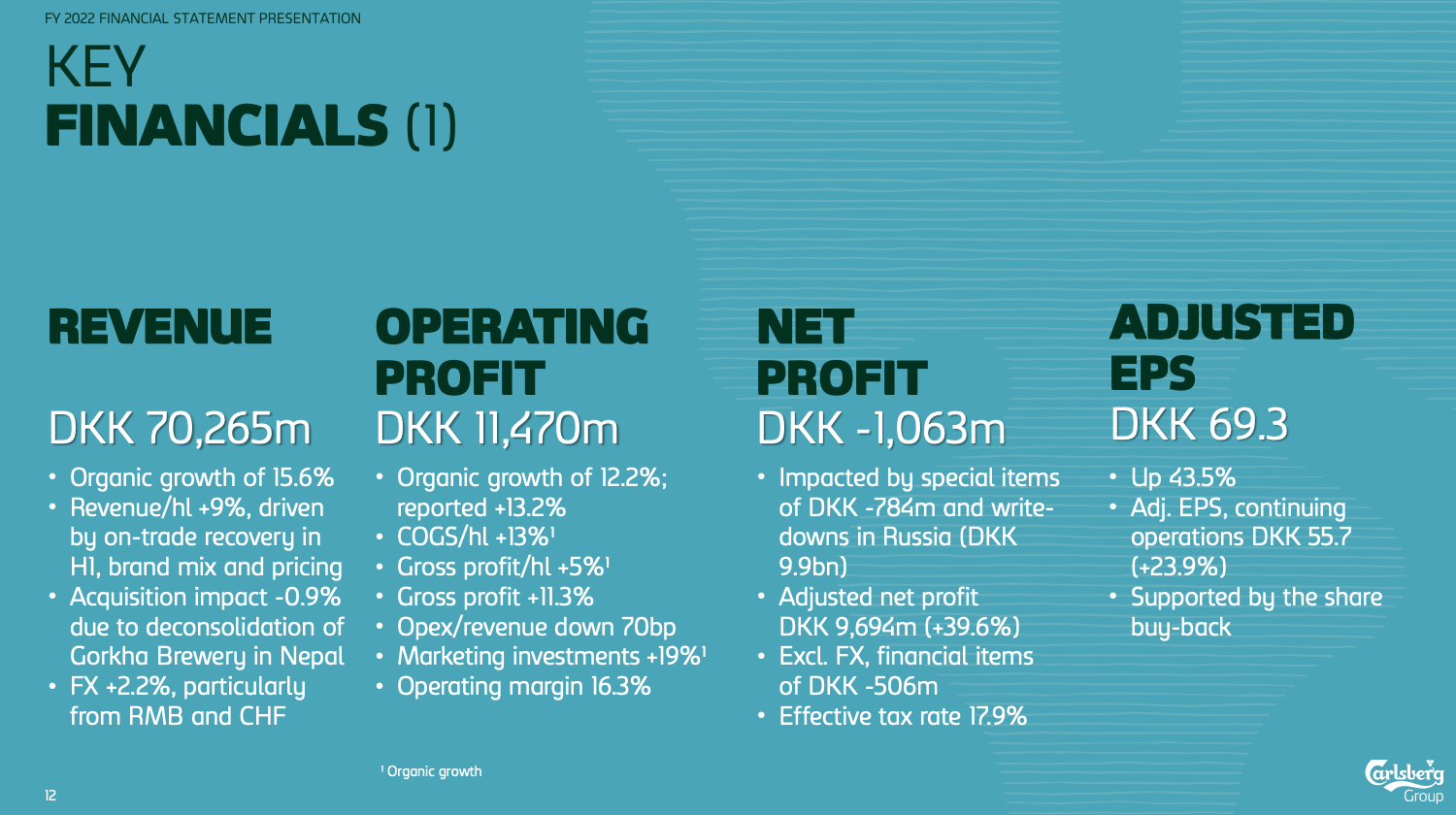

Suffice to say the company has surprised me in a positive way. Carlsberg's cost of sales did increase sharply last year, with higher energy and commodity prices leading to a circa 25% rise in its cost of materials. That, in turn, pushed margins lower, with the firm's gross and EBITDA margins slipping 190bps and 160bps, respectively, to 45.6% and 22.3%, respectively, in FY 2022.

{kind=link}

Source: Carlsberg FY 2022 Results Presentation

Price elasticity was much better than I expected, though, particularly in Western Europe. There, the company realized 8% higher sales per hectoliter last year, with volume up 5.4%. Taking Q4 2022 in isolation, Western European beverage volume was flat at 10.2m hectoliters, but with positive sales/hl taking revenue up around 5% YoY. That strikes me as a particularly strong performance given it was not a COVID-affected comp, while consumer health would have been worse at the end of the year than the start.

All told, the above ultimately helped push group revenue up 15.6% last year. That led to a rise in gross levels of profit, with FY 2022 gross profit per hectoliter up by 5%. Group EBITDA increased 9% year-on-year to DKK 15.7B - slightly higher than levels attained before COVID.

And A Good Start To This One

Lapping a soft prior period due to COVID meant that 2022 still offered low hanging fruit on the volume and channel/mix side. At the same time, consumers entering a period of sharply higher inflation were doing so off the back of COVID-related stimulus and elevated household savings, and that possibly gave firms quite a bit of cover in terms of raising prices without encountering much push back.

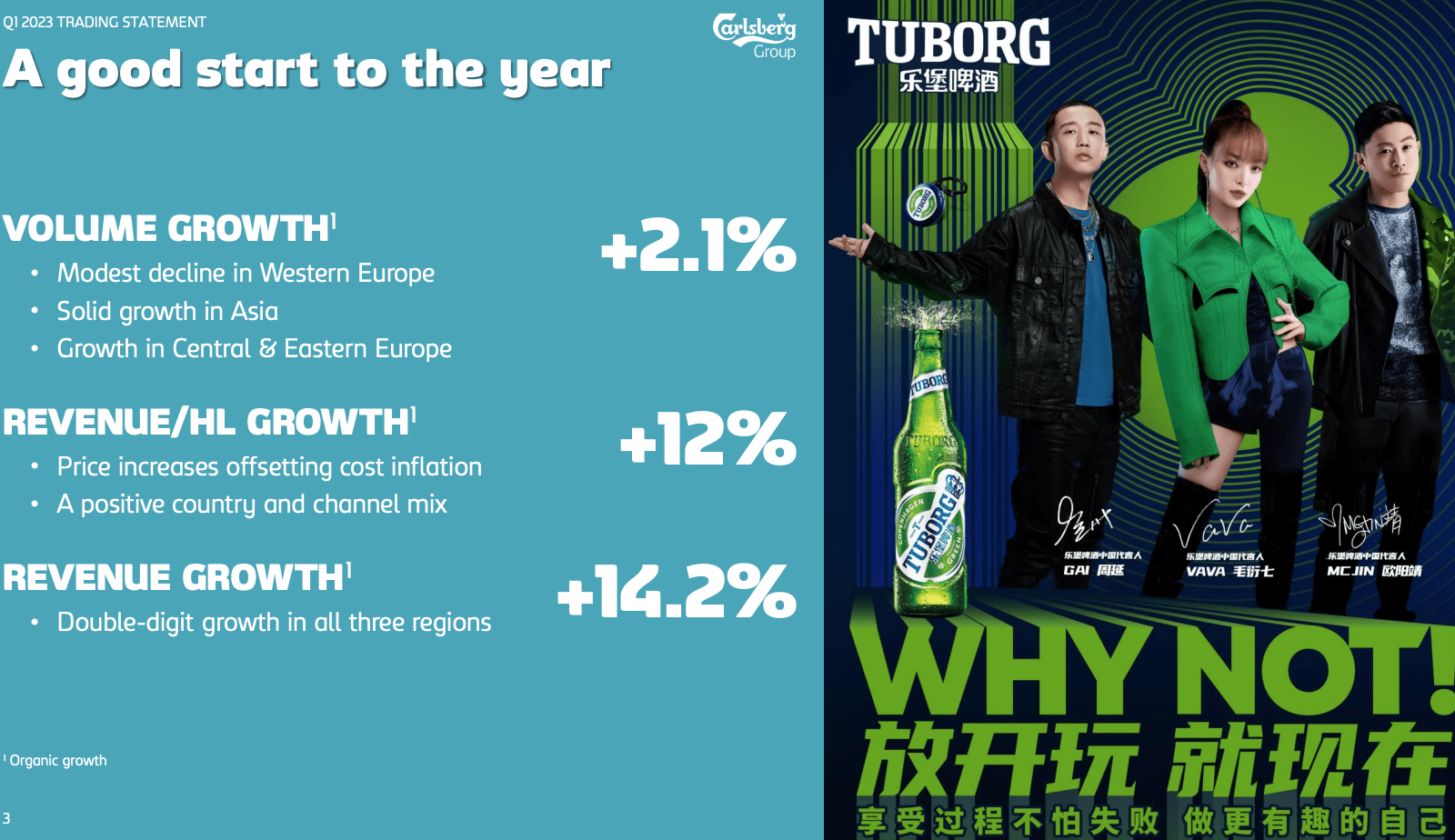

With those factors diminishing, 2023 will likely provide a much sterner test for consumer defensive firms, especially those with outsized exposure to Europe. With that in mind, Carlsberg has started the year strongly, with Q1 volume up 2.1% along with 12% revenue per hectoliter growth.

{kind=link}

Source: Carlsberg Q1 2023 Results Presentation

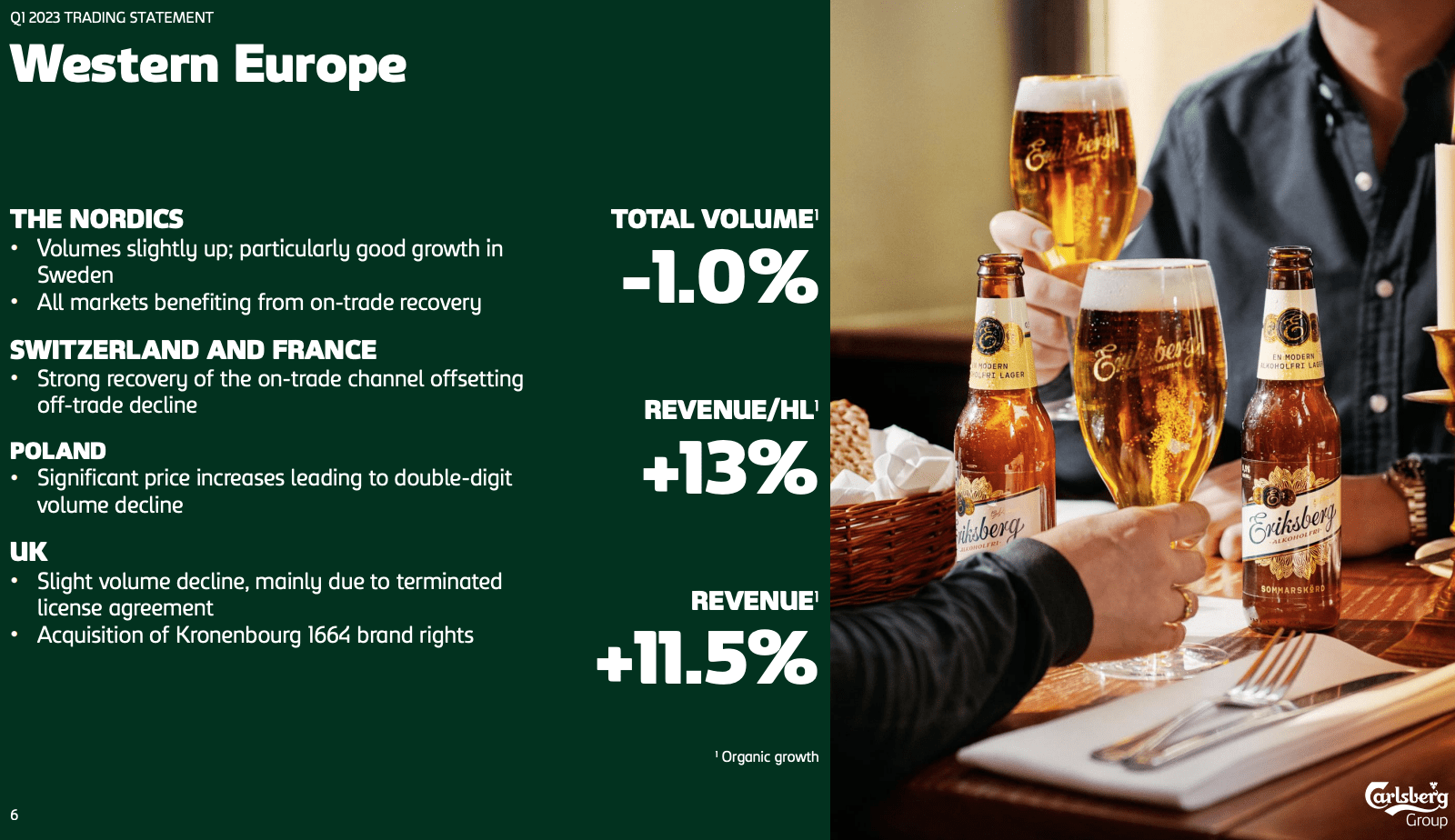

Western European volumes remain much more resilient than I would have anticipated, only declining by 1% YoY in the face of a double-digit increase in revenue per hectoliter. Asia is still reporting against easy comps given China's lockdowns, but volume there was up 4.9% with positive pricing leading to 12.4% revenue growth.

{kind=link}

Carlsberg Q1 2023 Results Presentation

Valuation Looks A Little Rich

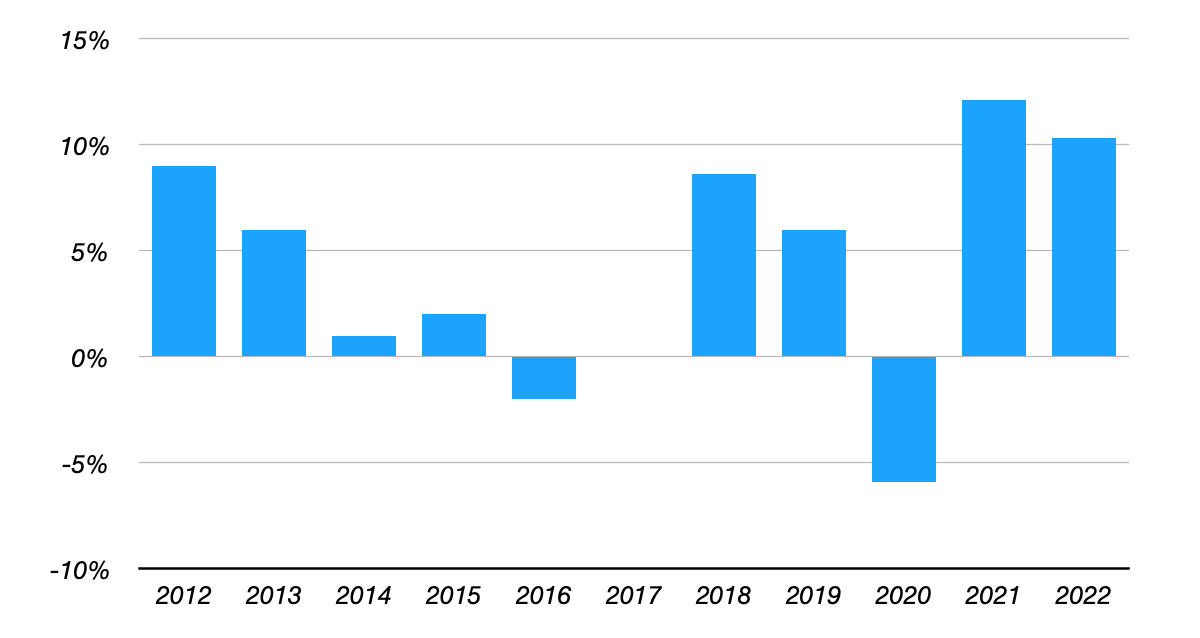

Business and stock returns: in both senses Carlsberg is performing much better than I would have expected at the start of last year. My main concern now is the valuation. At circa 19x forward earnings estimates , these shares just look too expensive relative to the growth prospects of the underlying business. Carlsberg has its bright spots in an otherwise unremarkable operating footprint: Asia offers tangible long-term volume growth, and its beverage portfolio there does skew more to the premium-end.

Carlsberg Asian Segment Organic Annual Beverage Volume Growth

{kind=link}

Data Source: Carlsberg Annual Reports

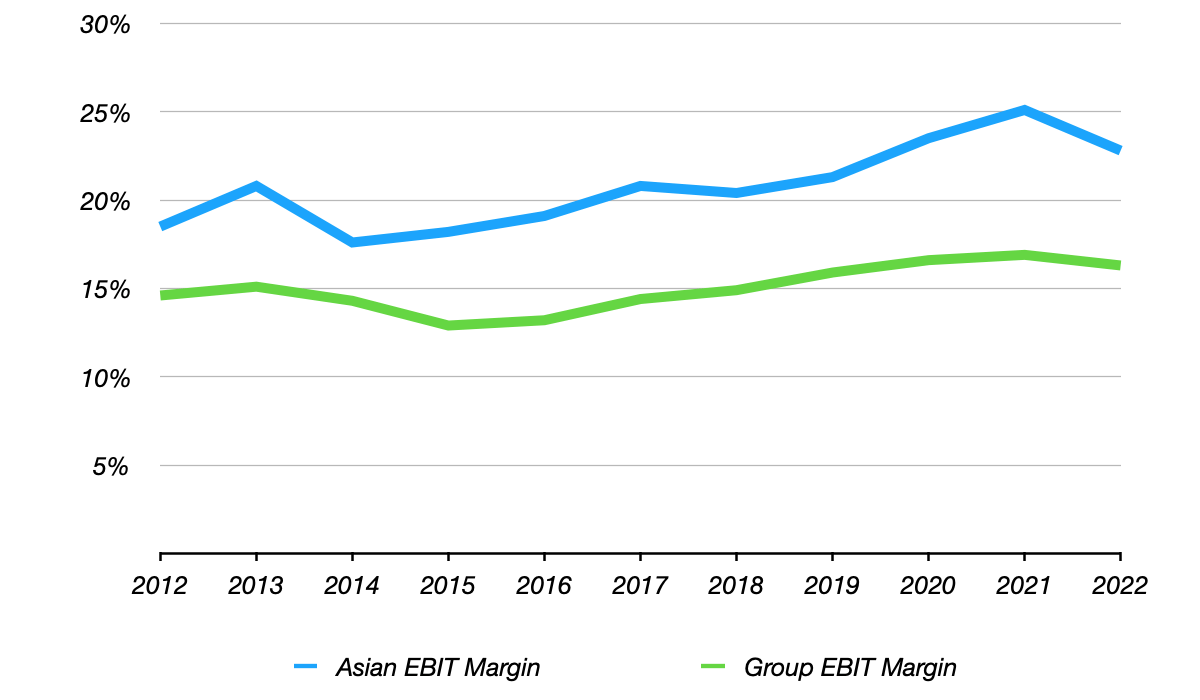

EBIT margins in its Asian segment are also higher than in Europe:

Carlsberg Asian And Group EBIT Margins

{kind=link}

Data Source: Carlsberg Annual Reports

Even so, with the shares currently at around DKK 1,125 (versus my DCF-derived price of DKK 965, unchanged from last time) I would like to be comfortable in forecasting high-single-digit annualized free cash flow growth over the medium-term, and that strikes me as a tad aggressive given the company's profile. Hold.

For further details see:

Carlsberg: Still Surprising To The Upside; Stock Now Expensive