CG - Carlyle Group: Great Value For A High-Quality Asset Manager

2023-11-06 09:11:54 ET

Summary

- Many of the top alternative asset managers including Blackstone Inc., The Carlyle Group Inc., and Kohlberg Kravis Roberts & Co. L.P. have underperformed the S&P 500 Index.

- Underappreciated assets, however, are precisely what value investors look to for alpha.

- For long-term investors looking to buy quality companies at attractive discounts, adding these alternative asset managers should be a no-brainer.

- In terms of value, Carlyle is the most attractive at just 9.7x forward P/E.

- We believe that Carlyle is undervalued, and we see the potential for P/E multiples to improve from its current 9.7x to a more reasonable 12x within the next 12-24 months, translating to a potential 23.7% gain on its share price over this period.

Alternative asset managers are lagging behind the equity bull market due to ongoing concerns that high-interest rates would cap investor appetite for risk, limit deal flow, and raise the cost of leverage. Meanwhile, private equity ((PE)) portfolio companies are under increasing pressure to temporarily shelve expansion plans, conserve cash, and cut costs in order to assuage investor concerns over financial prudence.

With the immediate prospects of alternative asset managers still looking vulnerable and fee-related earnings not likely to rebound anytime soon, it is no surprise that share prices for these asset managers have underperformed lately. Especially with risk-free cash, money market funds, and short-term Treasuries yielding around 5% at the time of writing, it is also understandable that investors are not too keen to take on risk.

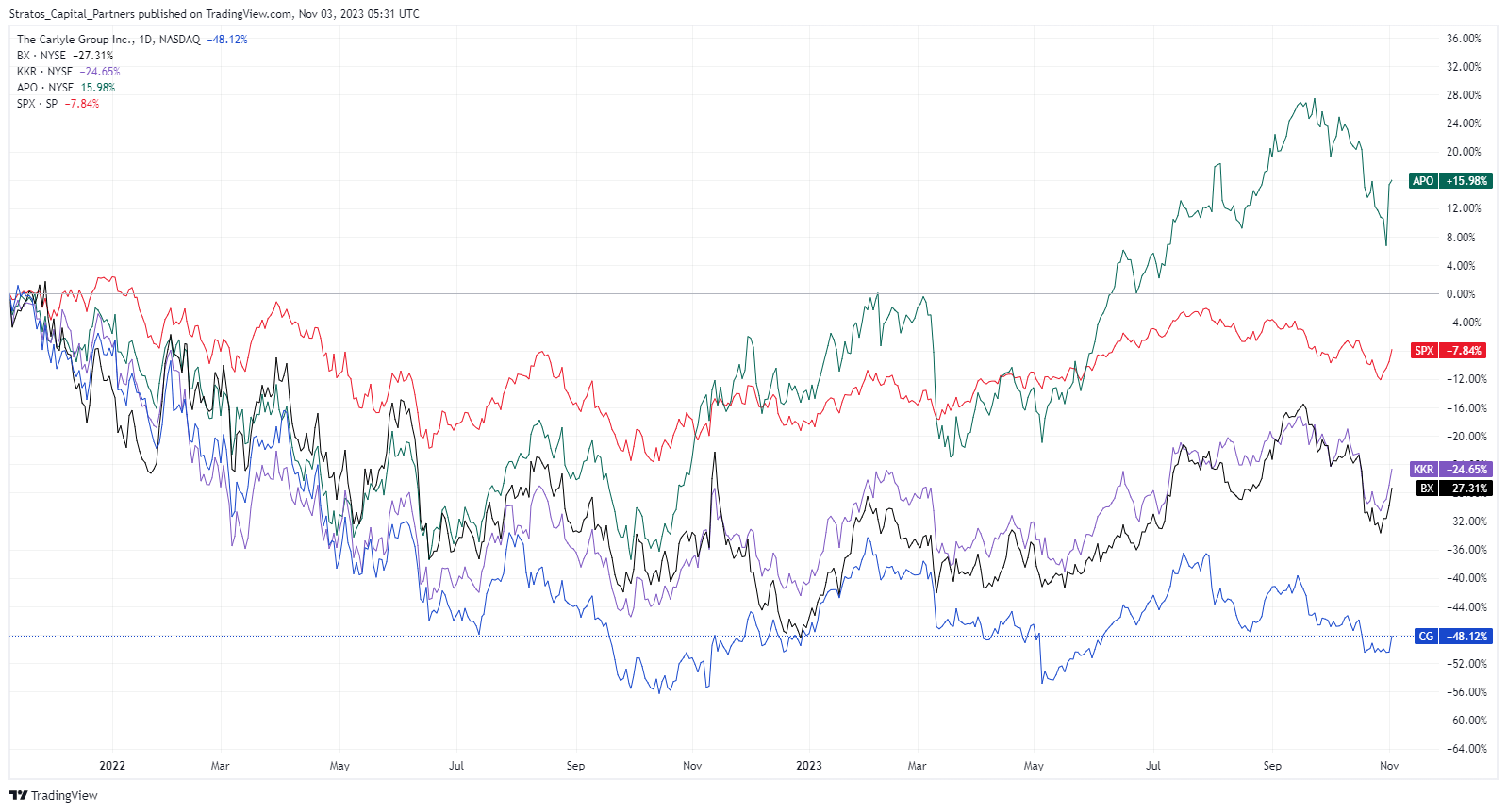

As the accompanying chart shows, many of the top alternative asset managers including Blackstone Inc. (BX), The Carlyle Group Inc. (CG), and Kohlberg Kravis Roberts & Co. L.P. (KKR) have underperformed the S&P 500 Index (SPX) since the beginning of 2022. The only exception is Apollo Global Management Inc. (APO), which has benefited from its concentrated bet on private credit compared to its more diversified rivals.

{kind=link}

Underappreciated assets, however, are precisely what value investors look to for alpha. For long-term investors who couldn't care less about precise market timing and prefer to stick to the simple strategy of buying quality companies at attractive discounts, adding these alternative asset managers should be a no-brainer.

Comparing some of the highest-quality alternative asset managers, BX remains our favourite pick overall in terms of quality, greater exposure to the real estate theme, and scale. Accordingly, we reiterate our "Strong Buy" rating on BX, a view that we established earlier in January .

| Market Cap |

| TTM Rev |

| TTM P/E |

| FWD P/E |

| TTM ROE |

| 5Y Avg ROE |

| APO |

| 48.3 bn |

| 26.3 bn |

| 13.6 |

| 12.9 |

| 56.5% |

| -28.9% |

| BX |

| 118.1 bn |

| 8.2 bn |

| 25.8 |

| 25.8 |

| 24.3% |

| 31.8% |

| KKR |

| 52.4 bn |

| 12.1 bn |

| 18.0 |

| 18.1 |

| 5.4% |

| 15.5% |

| CG |

| 10.6 bn |

| 3.1 bn |

| 7.5 |

| 9.7 |

| 6.9% |

| 30.6% |

Source: Seeking Alpha. APO 5Y Avg ROE is negative due to outlier losses and a merger with Athene Holding in 2022.

In terms of value, however, we think Carlyle is the most attractive at just 9.7x forward P/E. This makes Carlyle an ideal candidate for a more conservative or value-oriented portfolio. Despite Carlyle being the smallest within the group by market capitalization, the company has managed to deliver the second-highest 5-year average ROE of 30.6%. Thus, investors are not sacrificing quality or returns by choosing value.

Strategic Overhaul To Pursue Growth

Carlyle has also recently undergone a strategic overhaul to pursue opportunities in sectors that should allow the company to boost its assets under management ((AUM)) in the coming years. According to a recent report by Reuters , management will reduce exposure to U.S. consumer themes including media and retail due to an increasingly challenging investment environment. Carlyle's private equity business will instead focus on U.S. health care, government services, industrials, technology and financial services.

The strategic overhaul should also allow Carlyle to increase fund sizes for future fundraising due to a healthy investor appetite for deals in technology and healthcare. These are also areas that we think will deliver better returns for private credit due to tighter lending restrictions being imposed on mid-to-large-sized banks. New rules introduced by the Federal Reserve, Federal Deposit Insurance Corp., and the Office of the Comptroller of the Currency, would require large banks to set aside an additional 16%-19% in capital to absorb unexpected losses.

Credit Is Where The Alpha Will Be

The strategic overhaul at Carlyle is led by new Chief Executive Officer Harvey Schwartz, who is keen to expand the firm's capital markets business. Carlyle's capital markets business, which generated around US$50 million in fees last year, structures and underwrites debt for its own portfolio companies. By acting as the equivalent of an in-house investment bank, Carlyle is able to reduce costs in the form of fees it pays to banks.

Bloomberg

Carlyle's PE-heavy business model largely explains why the company has underperformed its more diversified peers in the current high-interest rate environment. Not only are high-interest rates undermining new PE deal flows, but higher borrowing costs are also hurting the performance and valuation of portfolio companies. However, the private credit space should perform well given that floating-rate loan terms have become more attractive for providers of private credit.

Given Carlyle's relatively small private credit exposure compared to its peers, we think there is significant headroom for the company to expand in this area over the coming years.

In Conclusion

Overall, we view Carlyle's strategic overhaul as a great move that will ultimately benefit shareholders and we expect Carlyle's valuations to catch up with its peers. We believe that Carlyle is undervalued, and we see the potential for P/E multiples to improve from its current 9.7x to a more reasonable 12x within the next 12-24 months, translating to a potential 23.7% gain on its share price over this period.

We initiate our coverage of Carlyle with a "Buy" rating.

For further details see:

Carlyle Group: Great Value For A High-Quality Asset Manager