CGBD - Carlyle Secured Lending: Well-Structured But With Deeply Hidden Risk

2024-01-12 09:33:37 ET

Summary

- Carlyle Secured Lending is a conventional BDC with a market cap of $785 million, focusing on US middle market companies with EBITDA between $25 to $100 million.

- While CGBD has a well-structured portfolio with the right focus on first lien in a diversified manner, there are some elevated risks associated with subpar performance of the underlying investments.

- In this article, I elaborate on the key details behind my thesis of avoiding CGBD.

Carlyle Secured Lending ( CGBD ) is a rather conventional BDC with a market cap of ~$785 million, which is slightly above the industry's median of ~$650 million .

Just as it is for most of the BDCs, CGBD's investment objective is to primarily focus on the current income, keeping the capital appreciation as a secondary objective. In terms of the investment focus, CGBD allocates into U.S. middle market companies that have an annual EBITDA generation of $25 to $100 million. This is also quite typical across the BDC space.

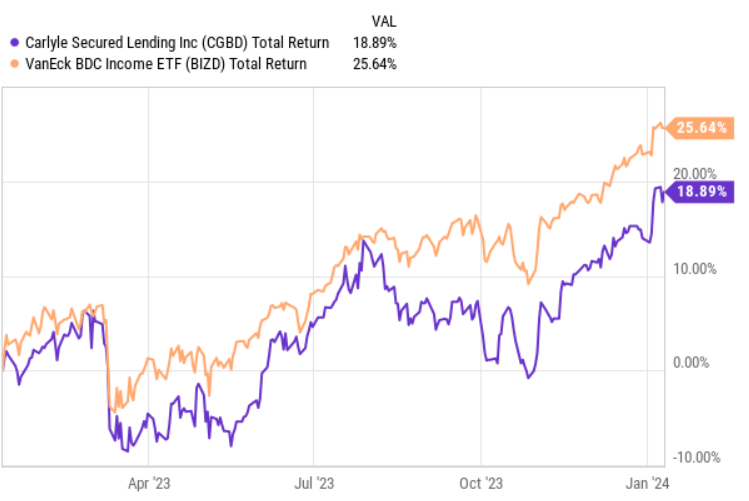

Performance-wise, CGBD has historically outperformed the BDC market, while exhibiting rather similar price (performance) swings as the index. Yet, if we look at the trailing twelve-month period (on a total return basis), we notice a slight divergence from the BDC index, which theoretically might signal that now might be an interesting moment to enter CGBD.

{kind=link}

From here, I will assess CGBD's fundamentals and try to determine whether it is an attractive buy for investors, who seek to capture high yielding income streams that are underpinned by prudently structured portfolio and resilient financials.

Thesis

One of the most important metrics in the context of BDC risk profile is the portfolio breakdown across different investment types. The higher the exposure to senior secured first lien the better, as it brings an increased level of protection for BDCs in the case of struggling or non-performing investments (or companies). Typically, in the BDC sector we can observe on average around 60-75% concentration in the first lien spectrum with the rest being distributed among riskier investment types such as second lien and equity.

Carlyle Secured Lending Q3 earnings report

In CGBD's case, the first lien (which is based on senior secured structures) constitutes 68% of the total exposure, thus falling somewhere in the middle of the industry average.

However, if we peel back the onion and assess the underlying structure of Investment Funds category, which takes another 14% of the portfolio, we will notice that the actual exposure to first lien is higher than 68%. Namely, the underwritten investments, which are conducted via two separate investment funds, where CGBD has 50% and 84% equity ownership, are mostly (~98% of them) comprised of first lien loans.

So, effectively, we are talking about a net exposure to first lien at an ~82% level with the remaining piece allocated in second lien and to a lesser extent in equity. This could definitely be considered an advantage for CGBD, de-risking the overall structure.

Another element of defense is associated with the industry diversification, where there is no overwhelming skew towards a single industry, which is not that common for a BDC with a market cap below $1 billion.

Carlyle Secured Lending Q3 earnings report

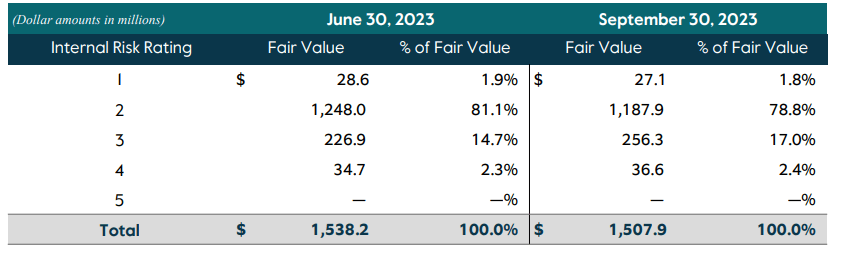

With all of this being said, the current performance of the underlying holdings does not signal a comforting trajectory going forward. As reflected in the table below, while CGBD has no defaulted investments yet, there are many that embody elevated risk.

{kind=link}

I am not that concerned about rating category 4, which indicates that companies are already out of the compliance with the stipulated debt covenants and are not able to service their debt in a timely manner. Roughly 2.5% exposure, on a FV basis, to category 4 is quite common across the BDC space and not that significant to inflict damage on the BDC's ability to accommodate the existing dividends.

I am, however, more concerned about ~17% concentration in category 3, which implies the following :

Borrower is operating below expectations and level of risk to our cost basis has increased since the time of origination. The borrower may be out of compliance with debt covenants. Payments are generally current although there may be higher risk of payment default.

Now, the combination of ~2.5% in category 4 with ~17% in category 3 is a potential problem, especially considering the fact that up until now there have been nothing but favorable tailwinds for CGBD (e.g., no systematic defaults).

So, having ~20% of the total exposure in companies which are not directly performing as planned, despite favorable market conditions, for me introduces too much of a risk (i.e., no inherent margin of safety in the case of rising corporate defaults in the economy).

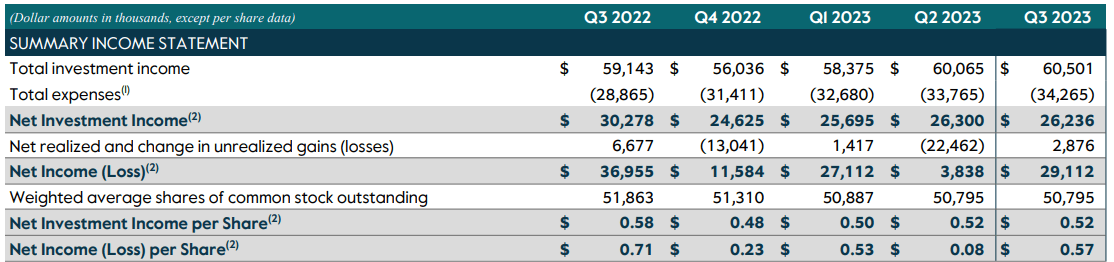

Nevertheless, if we assess the recent performance, we can observe nothing but remarkable results across the board. The most important component - net investment income per share - has consistently improved (with an exception of one slight one-off in Q4, 2022).

{kind=link}

Adding up the TTM distributions (including special dividends) and contextualizing them with the TTM net investment income results, we arrive at a dividend coverage of 118%. Adjusted for the special dividends, the coverage increases to ~125%.

Finally, before I summarize, let's take a quick look at CGBD's leverage profile.

{kind=link}

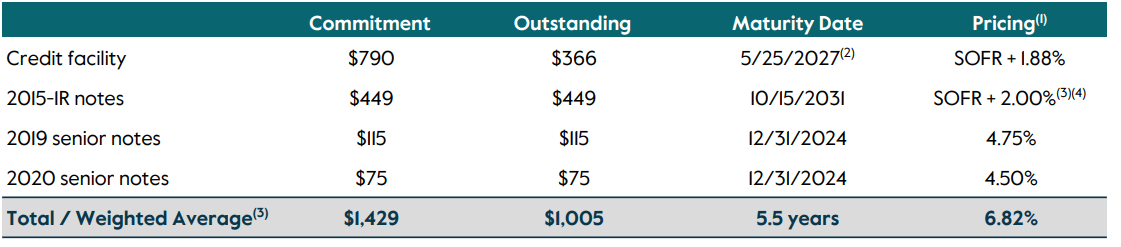

In terms of the debt to equity level, CGBD ranks slightly below industry average , which has 116% as median (while for CGBD the relevant measure is at 110%). On an absolute level this could be deemed as an acceptable measure bringing no elevated risk in the BDC (but no extra protection either).

The debt maturity profile of CGBD is less favorable than for some of the peers since the lion's share of the borrowings have been signed at variable rates, which have not been allowed to lock in cheap cost of debt and extract greater benefits from higher spreads, while SOFR continues to remain elevated. Yet, this fact has no bearing on the incremental (future) results relative to what CGBD has delivered recently.

An aspect to take into account here is the debt maturity profile of the two fixed rate notes that fall due in December, 2024. This means that CGBD will have to rely on more expensive cost of debt (unless SOFR suddenly reverts back to accommodative levels) to refinance, thereby increasing the overall cost of debt. Granted, the outstanding amounts are not that significant to materially move the needle, but it will still be made more difficult for CGBD to deliver improving results.

The bottom line

There are a couple of things, which clearly support the attractiveness of CGBD's investment case. The dominant exposure to first lien investments, diversified portfolio and a dividend yield of ~9.5% that is backed with ~118% coverage ratio make this BDC interesting from the yield and overall structure perspective. Plus, the fact that CGBD has recently lagged behind the index renders the story even more appealing.

However, the situation that we see in CGBD's risk ratings is not good, to say the least. Currently, about 20% of the investments exhibit patterns of potential difficulties - and all of this while having industry-wide tailwinds (e.g., depressed level of corporate defaults). This in conjunction with a relatively narrow margin of safety (not sufficient to account for the potential risk) in CGBD's dividend imposes just too high risk for me, questioning the underlying sustainability and durability of the current yield levels.

For further details see:

Carlyle Secured Lending: Well-Structured But With Deeply Hidden Risk