CRERF - Carmila: The 7.9% Yield Should Be Safe

Summary

- Carmila is a French REIT which owns the non-grocery store real estate assets within the building.

- The REIT was spun out of Carrefour, which remains the largest shareholder.

- Rent hikes should mitigate the impact of increasing interest rates.

- The 75% payout ratio implies the dividend for FY 2022 will come in at around 1.10 EUR per share, for a dividend yield of almost 8%.

Introduction

Carmila (CRMIF) was created by Carrefour to create more shareholder value by optimizing its own real estate assets. Whereas Carrefour used to own the entire floor space of their large shopping malls, upper-level management made the decision to split these malls in two parts. One part would be the Carrefour owned and operated "anchor store," but the non-Carrefour space (which is usually taken up by smaller tenants which aren't competitors) was spun out into Carmila. Carrefour (CRERF) (CRRFY) still is the largest shareholder with a 36% stake in Carmila.

Carmila Investor Relations

Carmila's primary listing is in France where it is trading on Euronext Paris with CARM as its ticker symbol . The average daily volume in Paris is 57,000 shares, which clearly makes it the best option to trade in the REIT's shares. There are about 144M shares outstanding , resulting in a market capitalization of approximately 2B EUR.

{kind=link}

A closer look at the financial performance and interest rate sensitivity

French companies rarely provide a detailed overview on a quarterly basis, and generally only publish financial statements every six months. Carmila is no exception and the Q3 update was a bit light on details. Nonetheless, it does appear to confirm my previous thesis the REIT remains on track for a very strong 2022 and has reaffirmed its guidance for a 20% recurring earnings growth for this year. Considering Carmila generated 1.24 EUR per share in recurring earnings in 2021, it's basically implying this year's result will come in pretty close to or perhaps even exceed 1.50 EUR per share. The recurring earnings in the first half of the year came in at 0.83 EUR, but I expect the second semester to be weaker.

That's one year ahead of schedule as I had only expected to see the 1.5 EUR milestone in 2023. While we may come in a little bit below that the 1.5 EUR seems to be a "given" considering most inflation-related rent increases will happen in H1 2023. So unless a wave of bankruptcies rolls over the tenant base of Carmila, the near-term outlook for 2022 and 2023 is looking bright. This also means we can look forward to seeing a dividend hike of approximately 10%. Based on an anticipated recurring EPS of 1.47 EUR per share, the dividend will likely come in at around 1.1 EUR based on the dividend policy which includes a payout ratio of 75%.

This represents a yield of 7.9% based on the current share price of 13.62 EUR per share and given this (fully-covered) yield and the fact that Carmila appears to be trading at just over 9 times this year's earnings and likely just over 8 times next year's recurring earnings, Carmila is still cheap enough to be picked up in a portfolio.

Sensitivity analyses

I wanted to work on some sensitivity analyses to see how the book value and the LTV ratio of REITs would come under pressure when the capitalization rates of the properties are increased. Fortunately this has been a pet peeve of mine for years and most REITs in the portfolios are in safe territory (as mentioned before, it's mainly DIC that is in the danger zone so I will be looking forward to seeing how the situation is evolving there).

In Carmila's case, we know the net rental income in the first nine months of the year was just under 254M EUR, indicating a Q3 NRI of approximately 83M EUR. That's a bit lower than I had anticipated although Carmila obviously also sold some assets while the net rental income also includes real estate expenses and I expect the heating and power bills to increase). So rather than annualizing the 254M EUR, I will annualize the Q3 NRI to 332M EUR per year. Applying a portfolio-wide 5% rent hike should result in a 348M EUR NRI in 2023. The table below shows the fair value of the assets, the NAV and NAV/share using four different capitalization rates. The other parameters used below are a net financial debt of 2.27B EUR (the official net debt position as of the end of June) and a current share count of 144M shares (it should be a little bit lower but I'm erring on the side of being cautious here).

Author Table

According to my calculations, even applying a required 7.5% net rental yield would still result in a book value about 15% above the current share price while the LTV ratio remains below 50%. Meanwhile, hoarding 25% of the recurring earnings means Carmila would retain approximately 50-55M EUR per year in cash, which would further reduce the LTV ratio by 110-120 base points in the 7.5% scenario. This means that the YE 2023 LTV ratio should still come in below 48%.

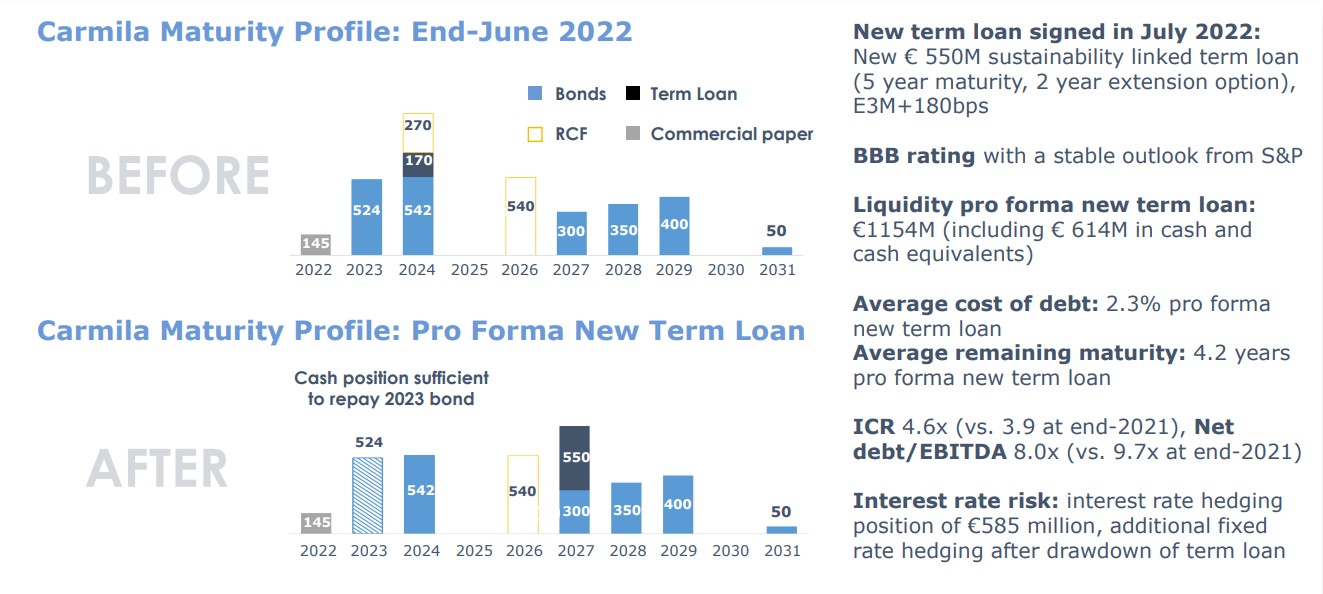

A second sensitivity analysis I wanted to work on is how the REIT would be impacted by higher interest rates. And there's a silver lining here. As Carmila's average cost of debt is currently approximately 2.3%, its average cost of debt should increase at a much lower rate than most of its competitors of which many have a sub-2% interest rate.

The next two maturities are a 2.375% bond in both 2023 and 2024 , and after that, Carmila is pretty much in the clear until 2027 when a 1.625% bond matures. A portion of the 2023 bond was already called early. Looking at the bond market, Carmila's six year bonds currently have a YTM of approximately 6.4%. Side note: Given the sensitivity analysis above, I think the Carmila debt is a strong buy here. Unfortunately the minimum size of these bonds is 100,000 EUR and that's the sole reason why I haven't dipped my toe in the bond-water yet.

{kind=link}

If the bond market remains this unreasonable, I do expect Carmila to increase its ratio of credit facilities and bank loans as that should for sure be cheaper. In the scenarios below, I will show how the recurring earnings will be impacted by an increase in interest rates across the board. Note: this is a very conservative scenario assuming all debt becomes more expensive overnight while only half of the debt is up for refinancing before 2027. So Carmila has the time working in its favor.

Carmila Investor Relations

The table above also does not take two important elements into consideration: It does not account for asset sales or cash hoarding: Should Carmila hoard the 50-55M EUR in non-distributed cash flow per year, it would hoard in excess of 400M EUR by the end of 2030 which would save the REIT about 25M EUR per year at a 6% cost of debt) Secondly, it does not take the rent hikes into consideration. If Carmila is able to hike the rent at a rate of 3% per year from 2024 on, it would add 80M EUR in additional annual net rental income by the end of this decade, which is when the last tranche of low-cost debt will be refinanced.

Investment thesis

This means that if Carmila doesn't develop its pipeline and if it's able to increase the rent throughout the next decade the impact of a 400 bp increase of the average cost of debt (implying a 6.3% interest rate on all of its outstanding debt) would be completely covered. Food for thought, and the main risk if obviously keeping the occupancy high and retain the tenants.

I have a long position in Carmila as I like the relationship with Carrefour and the strong footfall by owning the retail space related to a grocery-anchored superstore. As Carmila's debt repayment schedule is well spread out, I think the gradual rent hikes will be able to compensate for the increasing interest rates and the recurring earnings should continue to hover around the 1.50-1.60 EUR mark. The dividend yield of almost 8% is comfortably covered, making Carmila an interesting income-pick with exposure to European commercial real estate.

For further details see:

Carmila: The 7.9% Yield Should Be Safe