WMT - CarParts: Immense Upside And Takeover Potential

2023-05-25 10:46:39 ET

Summary

- CarParts.com, Inc. is an online provider of aftermarket auto parts and accessories in the United States.

- Revenue has grown at a CAGR of 10%, driven by an aggressive digital strategy.

- CarParts' current margins are unattractive, but we think improvement is likely in the coming years as the company focuses on profitability.

- The parts industry is robust and has the characteristics to generate attractive growth in the coming years.

- CarParts is extremely undervalued, with our DCF implying a 153% upside (analysts see 151.2%). We also think the company could be a takeover target.

Investment thesis

Our current investment thesis is:

- CarParts ( PRTS ) is a relatively good business and growing well as its low-cost e-commerce strategy allows it to gain market share relative to its larger peers.

- We expect the parts industry to remain strong as vehicles continue to age.

- CarParts' margins are poor, but the business remains focused on growth. We expected some improvement in the coming years.

- PRTS is extremely cheap and represents an attractive takeover target.

Company description

CarParts.com, Inc. is an online provider of aftermarket auto parts and accessories in the United States and the Philippines. The company offers a wide range of replacement parts for automobiles, including exterior parts, mirrors, engine and chassis components, as well as other mechanical and electrical parts.

Share price

CarParts' share price made impressive gains during the pandemic/post-pandemic period, as the industry experienced a rapid uptick in the demand for parts. Since then, things have cooled, with the share price responding disproportionately.

Financial analysis

{kind=link}

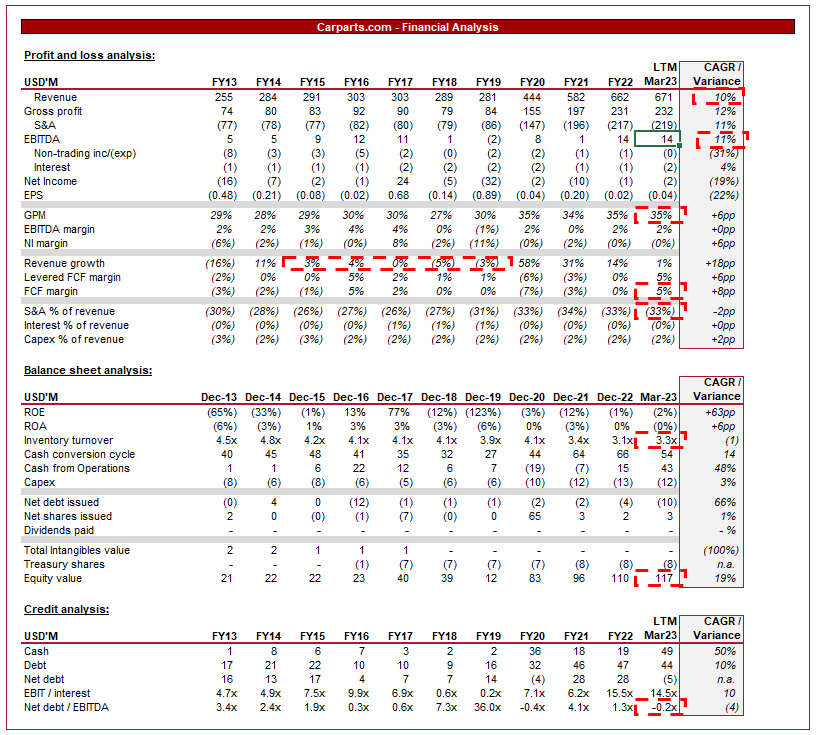

Presented above is CarParts' financial performance for the last decade.

Revenue

CarParts has grown revenue at a CAGR of 10%, reflecting a period of rapid expansion of what is a smaller player in the market.

CarParts is operating in a highly competitive industry, with the "big 3" auto parts businesses having a combined market cap of c.$108bn (AutoZone ( AZO ), O'Reilly ( ORLY ), and Advance Auto Parts ( AAP )) v. CarParts' $240m.

CarParts has carved out a share of the market and can grow rapidly due to its sole focus on e-commerce. The traditional incumbents have driven the majority of their traffic through physical stores, presenting an opportunity for the likes of CarParts to offer the benefit of convenience and pricing to those who are willing to forego the benefits of brick-and-mortar. As an e-commerce retailer, the company lacks the fixed location cost of its competitors, giving it a pricing advantage.

Within the industry, there are several key contributors to growth, both historically and going forward.

One of the significant trends driving the growth of the automotive aftermarket industry is the increasing age of vehicles on the road. With vehicles continuing to age, the demand for aftermarket parts will continue to rise. This was accelerated by the Covid-19 pandemic, with supply-chain issues causing the production of new vehicles to rapidly slow. The impact of this will be felt for many years as vehicles purchased in the last 3 years will be owned for many to come.

Many retail industries have seen rapid digitalization in the last decade, with consumers increasingly choosing convenience and pricing. This does bring the likes of Amazon ( AMZN ) and Walmart ( WMT ) into the market (among others), but we think CarParts is positioned well due to its sector focus, allowing the business to benefit from supply chain capabilities for stocking on the supply-side, and brand trust on the selling side.

Unlike other industries, the automotive industry has been slower in its transition, primarily due to the complexities of the products sold. The staff at AutoZone or O'Reilly are invaluable for a consumer who requires advice before purchasing, which is not as readily available with an e-commerce offering. This potential downside has been offset by many individuals preferring to perform basic repairs and maintenance on their vehicles. This has been possible due to the increasing availability of information, such as YouTube. We think this will continue to be an underappreciated revenue driver as consumers continue to identify areas of cost-saving by doing the work themselves.

Our concern with the digital transition is that although CarParts has done well, AutoZone and O'Reilly are investing heavily in growing their online sales. Both businesses are offering DIY guides on their respective websites, for example, as a means of both driving e-commerce sales and tapping into the DIY crowd. Both businesses have substantially larger resources, making us hesitant about CarParts' long-term competitive position should AZO/ORLY catch up.

The global shift towards electric vehicles presents a yet-to-be-wholly understood risk/opportunity in the parts market. With EVs having fewer moving parts, requiring less frequent maintenance, and having more complex OEM parts, there is a risk that the parts market experiences a period of correction as the annual demand for parts per car declines as the weighting shift toward EVs. Equally, there could be opportunities for businesses that can pivot and innovate to the current changing conditions, such as partnering with OEM manufacturers. We consider this to be a long-term risk to the business but will contribute to a slight slowdown in demand in the medium term in our view.

Economic considerations

Current weak market conditions represent both an opportunity and risk for the business. With inflationary pressure impacting consumers, we are seeing a slowdown in consumption across many industries, as spending slows. We expect this impact to be less pronounced in auto parts due to many purchases being required in order to maintain necessities in life (commuting to work, etc.).

The opportunity we see is that consumers are more likely to be price-conscious, allowing CarParts to benefit from its pricing competitiveness. LTM Revenue growth is disappointing, with only 1% gains, but Management should seek to exploit this.

Margin

CarParts' margins are disappointing. The highest EBITDA-M achieved during the historical period was 5%.

The reason for this is twofold. Firstly, the company's GPM is lackluster, although rapidly improving. This is a reflection of developing scale benefits. We expect the business to continually improve so long as revenue does. AZO, for example, has a GPM of 51%.

Secondly, CarParts is investing heavily in S&A, as a means of driving growth. This is a reasonable strategy given the company's current trajectory, and we expect this to continue. AZO for example spends c.32% of revenue on S&A expenses, which also includes D&A on stores, property costs, and operational staff to support locations.

For these reasons, we scope for margin improvement in the coming 5-10 years, as Management transitions from growth to profitability. From a relative basis, we are slightly concerned by the degree to which CarParts is currently underperforming. AZO/ORLY have EBITDA margins in the 20s, half of which looks out of reach for CarParts at the current trajectory.

Balance sheet

CarParts' inventory turnover has been gradually declining, reaching 3.3x in Mar23. Given the company is an online retailer, optimizing cash is critical for investing in growth and maintaining healthy liquidity. Our view is that the company should be targeting 4-5x as a minimum.

Solvency is not a risk for CarParts, with the company at a negative net debt position. This should allow CarParts to be flexible with debt raising if required.

Outlook

{kind=link}

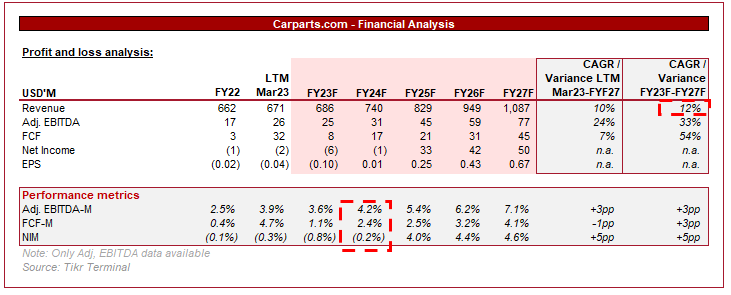

Presented above is Wall Street's consensus view on the coming 5 years.

CarParts is expected to continue its current growth trajectory, with a 12% CAGR. We believe this to be reasonable given the attractive industry dynamics, and CarParts' positioning in the market. We do expect the impact of greater EVs to have some effect, as well as AZO/ORLY increasing their online presence.

Further, margins are expected to improve, with EBITDA-M more than doubling to 7.1% by FY27F (From FY22 levels). Based on the cost profile we have assessed, this looks reasonable. Our only concern is the delta to peers.

Valuation

CarParts is currently trading at 17x EBITDA and 0.35x Revenue. This reflects poor sentiment around the business, with little value attributed to revenue.

Given the requirement for improvement in the medium term, we have valued CarParts with a DCF valuation. Our key assumptions are:

- Revenue growth averaging at 8% in the coming 5 years. We are not bullish to the extent analysts are but do believe CarParts can reach close to 10%.

- A perpetual growth rate of 2.25%, reflecting inflationary benefits long term.

- An EBITDA margin of 3%, improving to 6.5% in the coming 5 years. This is likely the most conservative estimate in our analysis and reflects hesitancy in Management's ability to execute.

- FCF conversion of 3-5%, moving in line with EBITDA-M.

- An exit multiple of 10x, reflecting a c.40% discount to AZO/ORLY due to its inferior margins.

- A discount rate of 9%.

Based on this, we calculated an implied upside of 153%. Although outlandish in size, this is almost identical to the consensus analyst upside of 151.2%.

Takeover target

Given CarParts' current characteristics, the company looks to be a fantastic takeover target. It is extremely cheap and has the infrastructure and customer base to provide value to a larger player.

We can easily see a takeover by Amazon seeking to expand into the parts space. The synergies would be fantastic with warehouse costs, distribution, and marketing plummeting.

Key risks with our thesis

The risks to our current thesis are:

- Near-term margin contraction due to economic conditions extending the time required to consistently exceed 5-6%.

- Near-term growth slows down, impacting sentiment/share price.

Final thoughts

CarParts has done well to establish a market position in a highly competitive industry. Many criticize its margins, but many companies at this point in the growth cycle are loss-making. We like the industry and have written positively about both AZO and ORLY (find here and here ). CarParts is unlikely to become more than a mediocre market participant, but at its current price, this could create substantial value for shareholders.

There are near-term risks given the slowdown the company is facing (which could make this dead money for 6-18 months) but we think the potential for a takeover implies awaiting a positive catalyst is a mistake.

For further details see:

CarParts: Immense Upside And Takeover Potential