CRS - Carpenter Technology: Good Near-Term As Well As Long-Term Prospects At An Attractive Valuation

2023-09-05 12:21:49 ET

Summary

- Carpenter Technology Corporation is experiencing solid demand across its end markets.

- The company's revenue grew by 34.5% YoY in the fourth quarter of 2023, driven by double-digit sales growth across multiple end-use markets.

- Carpenter Technology Corporation's margin prospects look favorable, with benefits from increased sales, improved production efficiency, and a focus on high-margin businesses.

Investment Thesis

Carpenter Technology Corporation’s ( CRS ) stock is up over ~40% since my previous bullish article in May. The company is experiencing solid demand across its end markets which are seeing good volume and pricing growth. CRS also has a strong backlog across its end markets and geographic regions. This, along with continued focus on high-growth, high-value end-use markets and diversifying business portfolio to meet the needs of its current and future customers should help the company post good growth in the near as well as long-term. Further, the company’s margin prospects also look favorable with benefits from volume leverage due to increased sales, improved production efficiency, and a focus on high-margin businesses to improve product mix. The good revenue growth and margin expansion prospects, combined with lower-than-historical valuation, make CRS stock a buy.

Revenue Analysis and Outlook

In my previous article , I talked about CRS’ growth prospects benefiting from robust demand across its end-use markets, solid backlog levels, primarily in the Aerospace and Defense sectors, and strong pricing. The company has reported its 4Q23 results since then, and similar trends were seen.

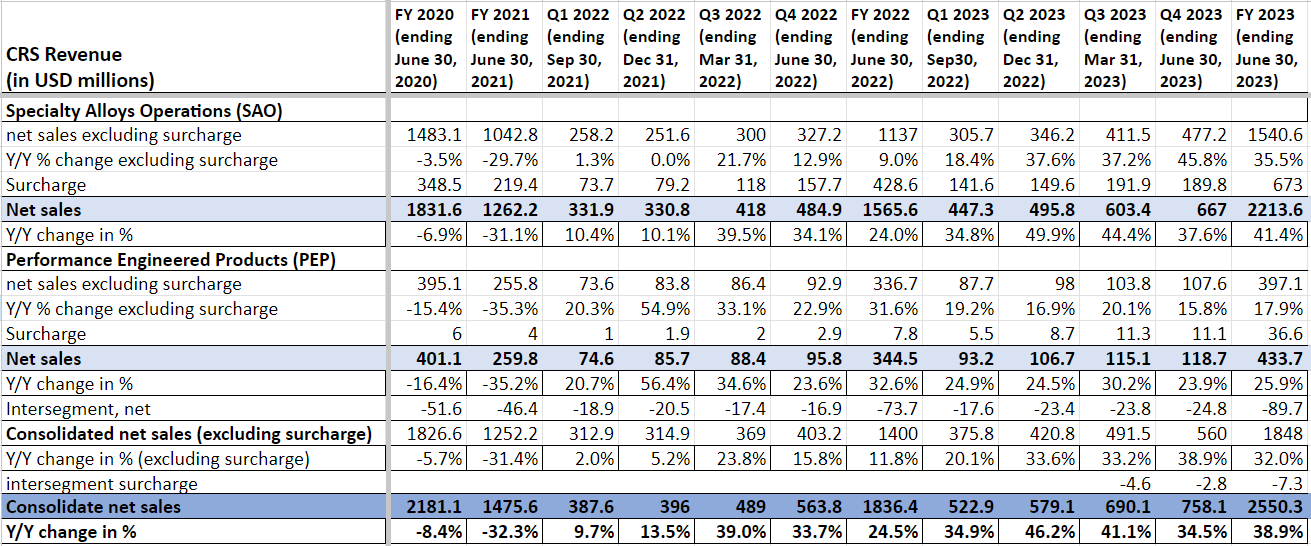

In the fourth quarter of 2023, the company’s sales growth momentum continued. The company witnessed double-digit Y/Y sales growth across its Aerospace and Defense, Medical, Energy, and Industrial and Consumer end-use markets. On a segment basis, the Specialty Alloy Operation (SAO) segment sales increased 46% YoY, reaching $477.2 million (excluding surcharge). This growth is augmented by 9% higher shipment volumes (due to productivity gains), strong pricing, and an improving product mix as demand across the key end-use markets, particularly in Aerospace and Defense remains robust. On the other hand, the Performance Engineered Products ((PEP)) segment achieved 16% YoY growth, reaching $107.6 million (excluding surcharge), driven by strong demand for titanium materials used in Aerospace and Defense, and Medical end-use markets. The remarkable double-digit growth in both segments led to a significant 34.5% YoY increase in revenue to $758.1 million. Excluding the surcharge, revenue grew by an impressive 39% YoY, reaching $560 million.

CRS' Historical Revenue Growth (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I am optimistic about the company's near-term as well as long-term growth prospects.

In the near term, the company's growth should be driven by a strong backlog as well as solid end-market demand. The company's backlog improved 4% sequentially and 38% Y/Y last quarter, which provides good visibility for the company's revenues in the coming quarters. The company is witnessing strength across all of its key end markets. The Aerospace and Defense end market is seeing continued momentum as global aerospace traffic continues to increase, resulting in ramping up of production of new planes.

Airplane Build Rates (CRS Investor Presentation)

The defense market is seeing demand driven by next-generation missile, fixed wing and rotorcraft platforms. On the medical side, there is pent-up demand for elective surgeries which were postponed during the pandemic. Similarly, the transportation market remains strong due to high demand and low inventory of light-duty vehicles; the energy end market is benefitting from continued capital investment; and the industrial and consumer end market is seeing strong demand for semiconductor fabrication and consumer electronics.

Longer term, the company's focus on high growth, high value end-use markets and applications as well as continued focus on innovation and new product launches to meet customer requirements should help it post above-market growth. The company’s focus on addressing key demand and application trends like requirement of light weight, more fuel-efficient planes in Aerospace and Defense end market, requirement of longer lasting implants and minimally Invasive surgeries in Medical end-market, etc. has helped gain market share as well as improve product mix with value increase outpacing volume. While the pandemic has caused some disruption in the recent year, the company has a solid track record of outperforming markets. For example, the company posted almost 3x the end market growth of the medical-device market between FY 2017-19. I expect to see a good outperformance looking forward as well.

CRS growth vs medical device market’s growth pre-Covid (CRS Investor Presentation)

Margin Analysis and Outlook

During 4Q23, the company’s adjusted operating margin substantially increased 750 bps YoY to 11.2%. This impressive expansion in margin can be attributed to increased productivity and capacity optimization, improved product mix and higher selling prices, particularly in the SAO segment which more than offset the increased inflationary costs.

CRS Adjusted Operating margin (Company data, GS Analytics Research)

Looking forward, I expect the company's margins to continue benefiting from improving production efficiency. Given the level of volatility in volumes and the kind of supply chain disruptions we have seen in the recent years, it is natural for inefficiencies to creep in any manufacturing facility. However, with the situation normalizing, I expect the company's production efficiency to continue improving in the coming quarters. Further, the company should also benefit from volume leverage due to increasing sales.

In addition, the company should see a meaningful benefit from improving price/mix as it continues to focus on high value products. The company's focus on application areas where consumers are willing to pay a premium for longer lasting, high performance and innovative materials positions it well to improve product mix. Think of it like this - an airplane manufacturer will likely be willing to pay more for lightweight durable material for aircraft parts and a patient will always prefer a stronger, smaller, and longer-lasting implant. The company’s focus on these areas should help charge more and improve its long-term product mix and margins. So, I am optimistic about the company's margin prospects.

Valuation and Conclusion

CRS is currently trading at 17.80x FY24 consensus EPS estimates of $3.61 and 14.42x FY25 consensus EPS estimates of $4.46, which is at a good discount versus the Company's 5-year average forward P/E of 21.75x.

Management has given a target of ~40% CAGR on the operating income from FY23 through FY27 based on the strong end market demand, market share gains and margin improvement. The good thing about this target is it is not back-end loaded and, according to management , the company will start seeing a step-up in its results starting FY24 itself. Although the stock has risen by over 40% in just three months since my previous article , it still looks undervalued when one considers the company's growth prospects. The market does not seem to be fully factoring in the company's potential for growth yet. Therefore, I maintain my buy rating on the stock.

For further details see:

Carpenter Technology: Good Near-Term As Well As Long-Term Prospects At An Attractive Valuation